- Overview of COVID-19 conditions in Philippines

-

The Philippines government is not likely to remove the alert status until Q3 of 2022

- According to the World Health Organization (WHO), as of May 2022, the Philippines had 3,688,750 confirmed COVID-19 cases, with 60,455 deaths, and 245 new cases.

- On May 19, 2022, the total number of vaccinations in the Philippines reached 149,025,442. The share of the fully vaccinated population was 63.4%, with 12.6% of Filipinos having received booster doses.

- As per the Inter-Agency Task Force, effective May 30, 2022, adult passengers (aged 18 or above) entering the Philippines, will no longer be required to provide a pre-departure COVID-19 negative test report (RT-PCR or Rapid Antigen Test). However, they will have to be fully vaccinated and have at least one booster shot before entering the Philippines. If they do not get the booster dose before entering the country, they will have to provide a negative RT-PCR test result taken 48 hours before departure, or a rapid antigen test result taken 24 hours prior to departure. Travelers between the ages of 12-17 do not need to show any negative test results, provided they are fully vaccinated and have the certificate. Lastly, travelers under age 12 will be exempted from pre-departure COVID-19 measures if their parents are fully vaccinated.

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Philippines

Quarterly Recovery Index is currently unavailable for the Philippines.

- Impact on GDP

-

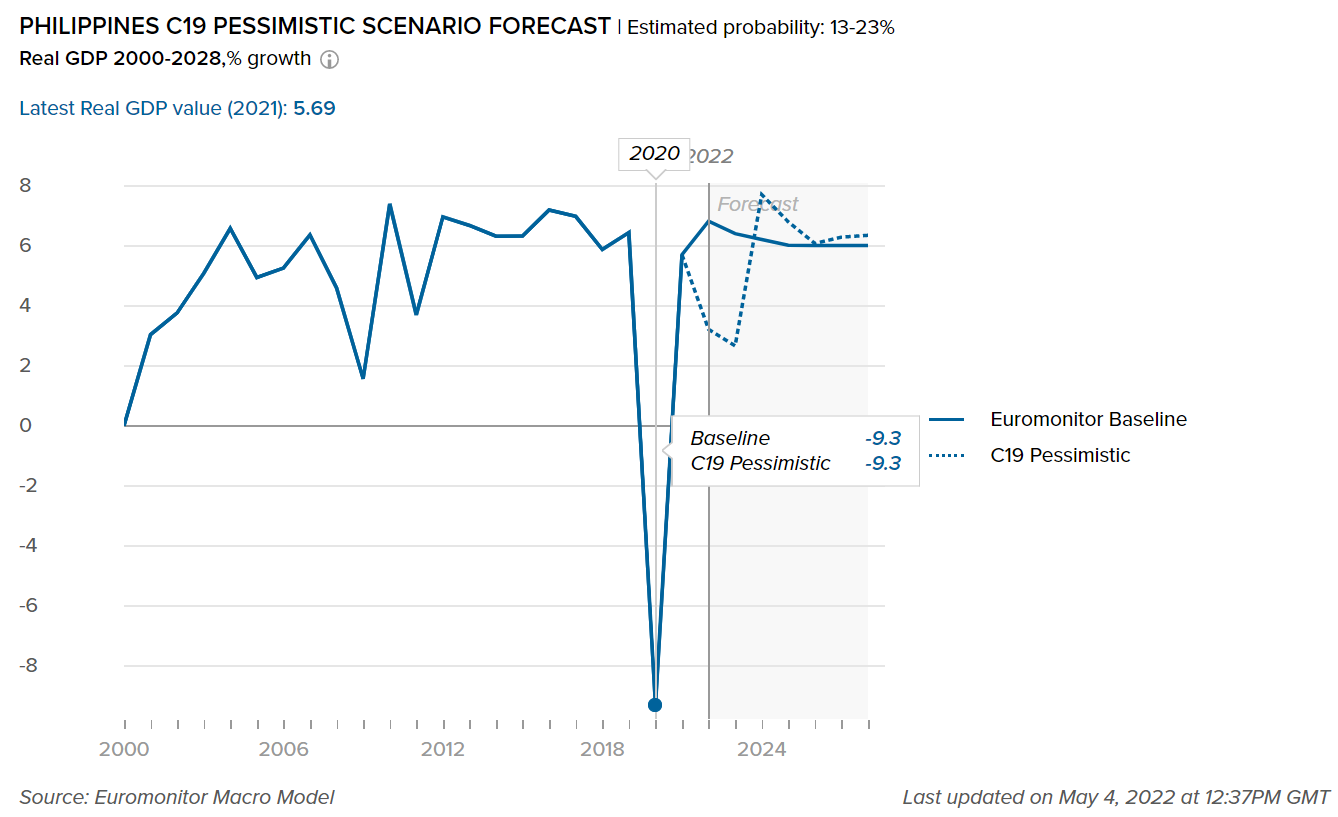

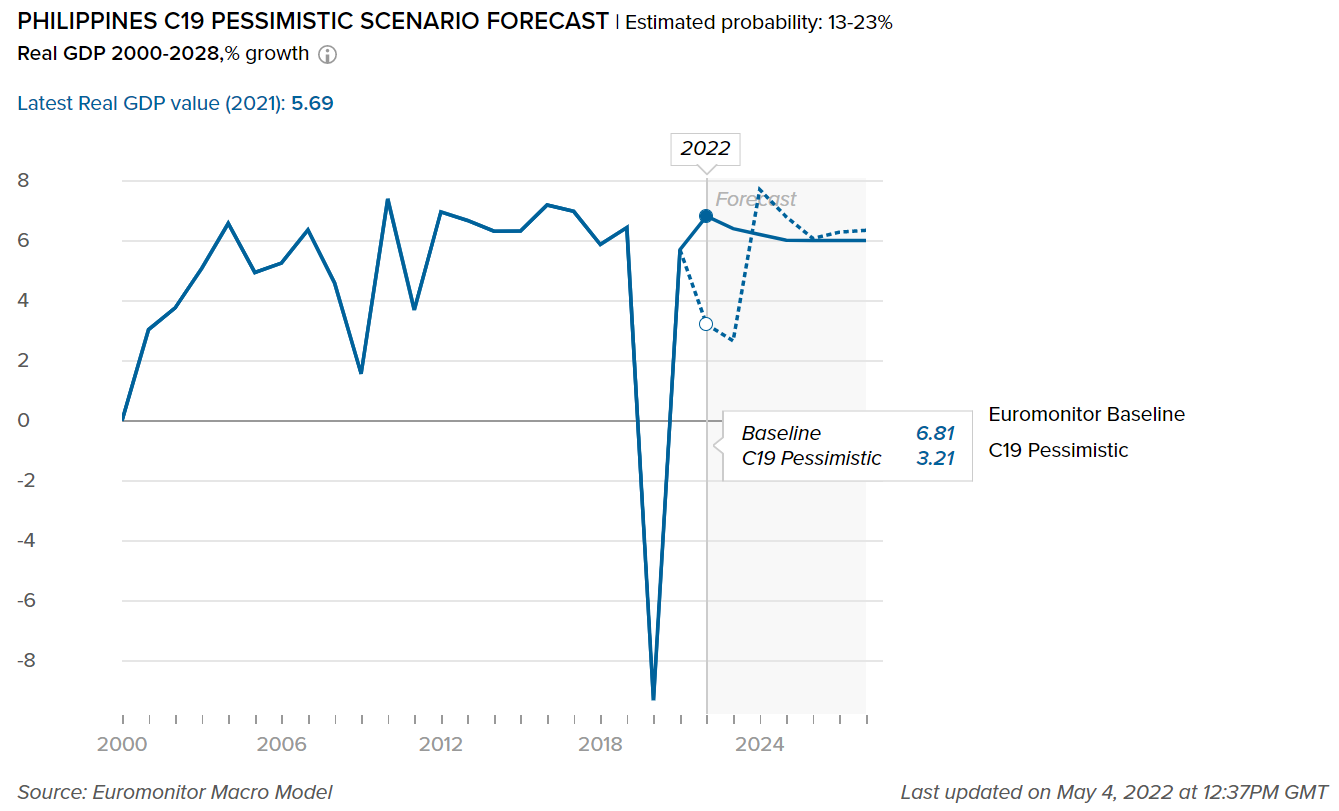

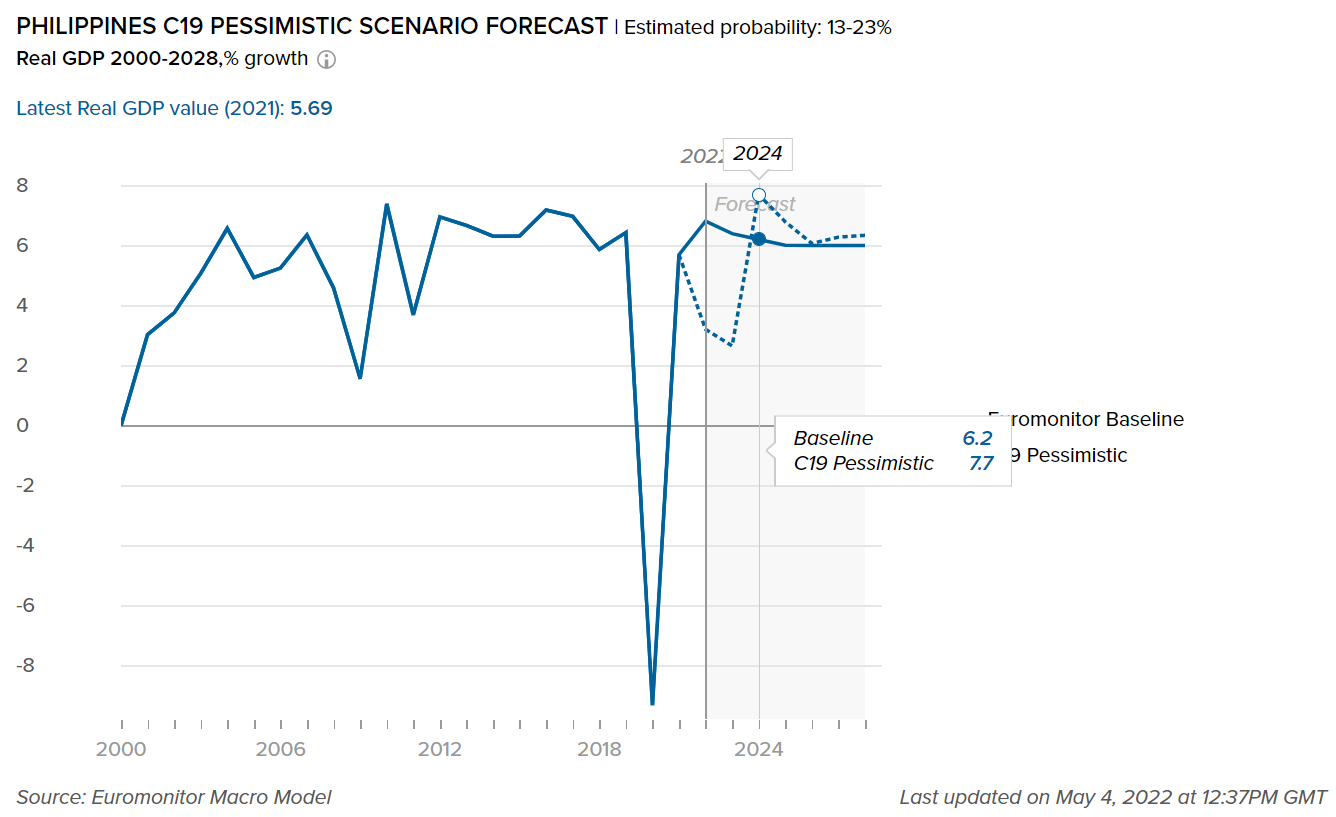

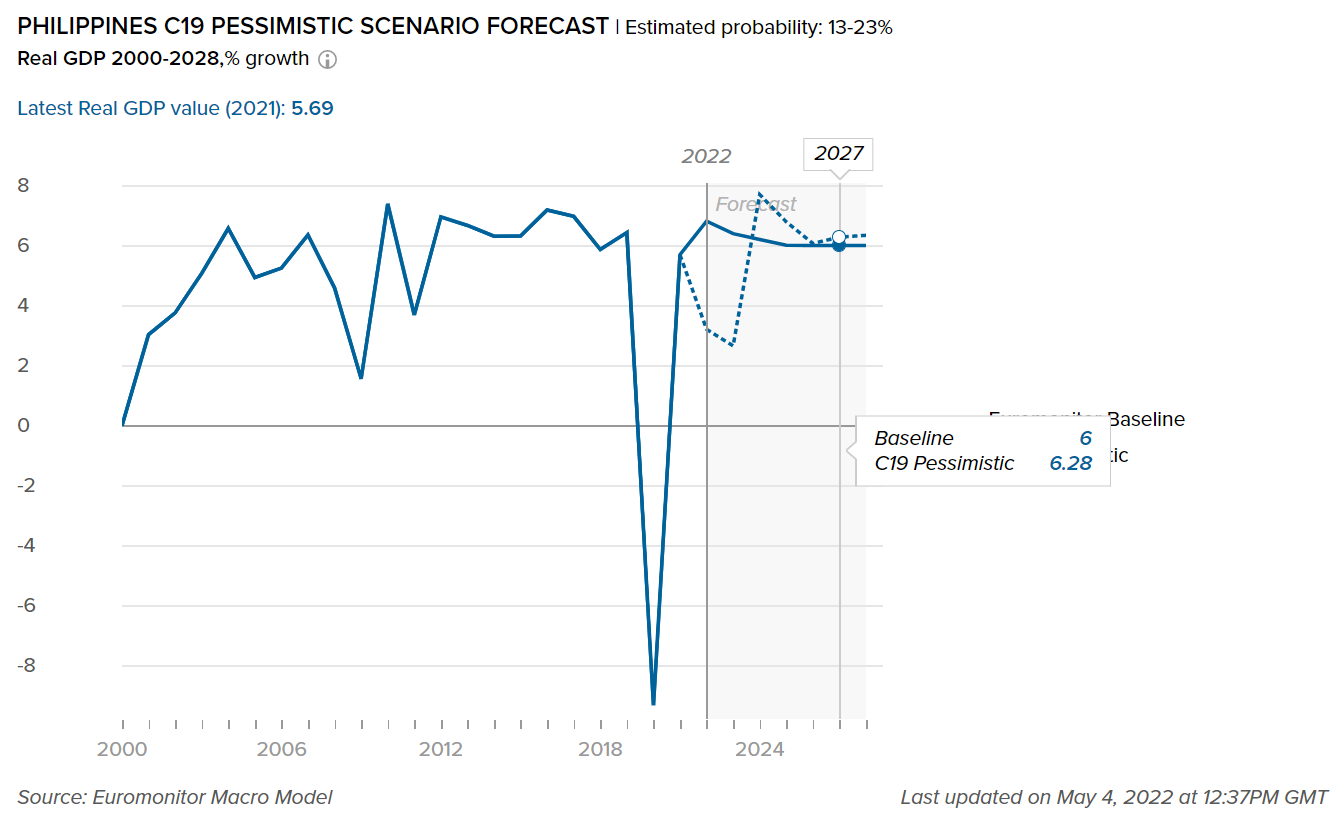

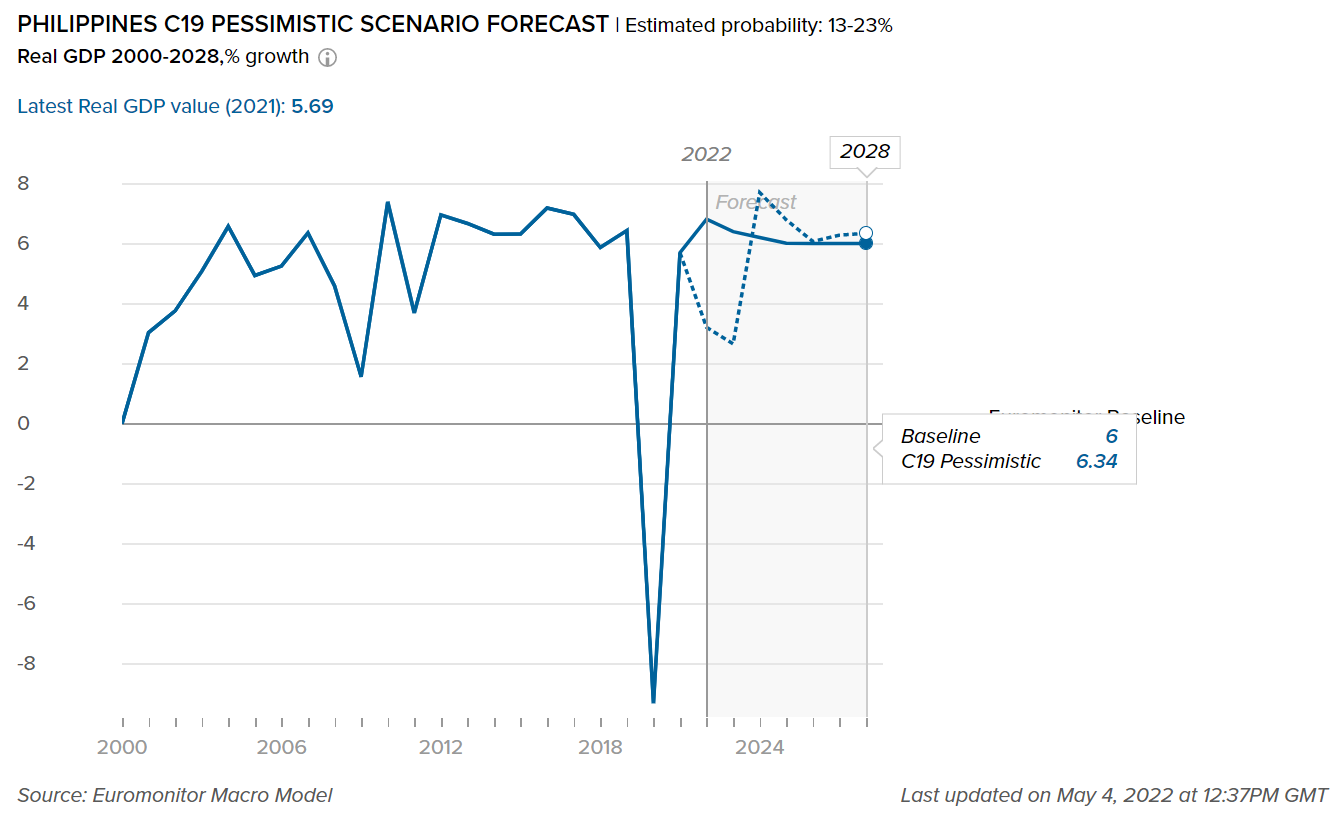

This graph shows our “most probable” and “worst case” scenarios of how COVID-19 will impact real GDP value in the Philippines. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

GDP is predicted to grow as economic uncertainty subsides over 2022-2026

- In 2020, the Philippines recorded a massive contraction of 9.3% owing to the COVID-19 pandemic. The country experienced significant declines in consumption and investment growth, as well as a sharp slowdown in exports, tourism, and remittance inflows. In addition, consumer and business confidence dropped due to containment measures, elevated uncertainty, and lower household incomes. However, the economy bounced back in 2021, supported by economic stimulus measures, recovering global demand, and the gradual lifting of coronavirus curbs. This momentum is expected to help the country’s economy to grow by 6.8% and achieve upper-middle-income country status by late 2022, as per the Philippine Statistics Authority. The economy is expected to remain one of the most dynamic in the Asia Pacific region over 2022-2026.

- Over 2019-2021, the government proposed a series of reforms to boost foreign direct investment (FDI) inflows. For example, the Philippines government relaxed the local employment requirements for foreign investors and plans to reduce corporate income tax from 30.0% to 20.0% over the next 10 years. In addition, the country also allowed 100.0% foreign ownership in large-scale geothermal projects such as Tongonan Geothermal Project and MakBan Geothermal Project. However, despite the progress, barriers such as high transaction costs, currency volatility, and liquidity risks to foreign investment remain in the country. As a result, the country’s FDI inflow is expected to lag behind the Asia Pacific average.

- Impact to Sector Growth

-

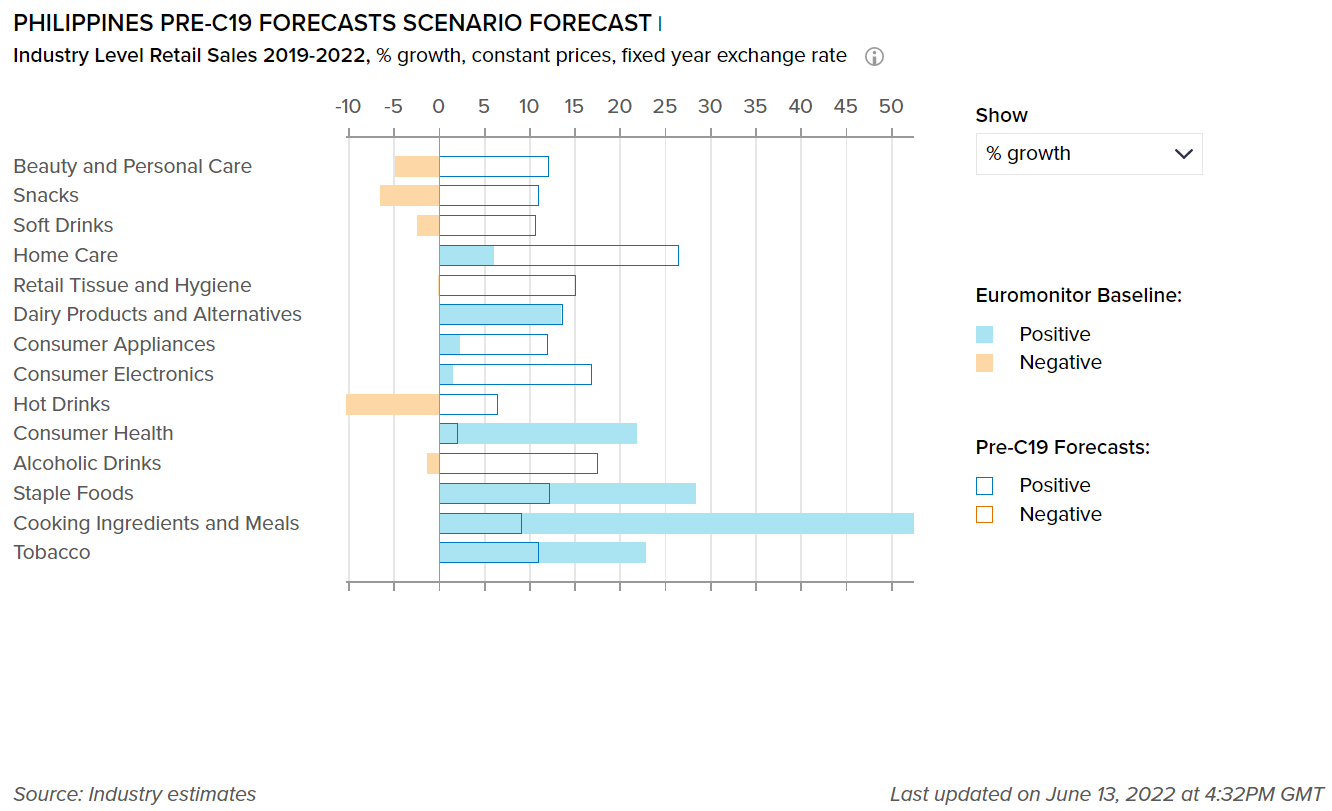

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below shows the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

Snacks, cooking ingredients, and meals are set to witness a strong rebound as foodservice outlets reopen

- With the outbreak of COVID-19, snacks declined as foodservice outlets, restaurants, pubs, and other eating facilities were closed in 2020. Moreover, restricted spending from Filipinos also added to this decline. However, as restrictions eased and the country rolled out its vaccination program, snacks saw stronger growth in 2021. In addition, businesses returned to relative normalcy, and tourism and foodservice resumed. As a result, products associated with indulgences such as ice cream, chocolate confectionery, and sweet biscuits registered the quickest recovery, as they fulfilled the need for comfort food. Over 2022-2026, snacks are likely to witness significant growth, spurred by new product development and innovation.

- Cooking ingredients and meals are expected to record a significant CAGR of 7.0% over 2022-2026, which will be driven by the preference for a homebound lifestyle among Filipinos. Despite the reopening of outside eateries, Filipinos are predicted to feel less comfortable going out as often as they used to during pre-pandemic conditions, owing to the fear of contracting the virus. With in-home lifestyles set to linger, products used for at-home meal preparations such as spices, herbs, pulses, meat, and cereals are set to benefit, with frozen ready meals predicted to be in heavy demand over 2022-2026 owing to the long line of product options.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors covered in the Philippines. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Revival of social activities is set to improve the beauty and personal care market in the Philippines

- Over 2022-2026, beauty and personal care is expected to improve owing to the revival of social and economic activity. The reopening of offices and other public places are likely to encourage consumers to focus more on personal grooming. This will support renewed demand for subcategories such as color cosmetics, sun care, deodorants, and fragrances. However, the pandemic-induced economic impact and high inflation may impact consumer purchasing power. This heightened budget-consciousness is set to support demand for homegrown brands such as Silka, Bambini, and Hairworks, which offer similar benefits to premium brands but at mass-market prices.

- In dairy products and alternatives, shelf stable milk, cheese, and yogurt are expected to record the most favorable value sales growth rates over 2022-2026, owing to the newfound focus on home consumption. After the outbreak of the pandemic in 2020, many Filipinos started having breakfast at home rather than in a café or on their way to work. With shelf stable milk, cheese, and yogurt all considered to be ideal breakfast options, these categories are predicted to benefit substantially. In addition, drinking yogurt is expected to witness significant growth, owing to the health benefits such as strong immunity and improved metabolic and digestive function, that it provides.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

4,707

4,824

-2.4

Home Care Packaging

5,250

5,449

1.6

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

12,983

13,628

-0.37

Flexible Packaging

36,258

37,533

0.01

Metal

4,130

4,171

-0.08

Paper-based Containers

2,029

2,084

1.11

Glass

9,050

9,083

0.00

Liquid Cartons

910

957

0.00

Consumers look for less expensive packaging options as limitations on spending continue

- Within home care packaging, plastic pouches and HDPE bottles were among the most popular pack types, with flexible plastic packaging the dominant pack type over 2020-2021. The popularity of plastic pouches as refill packs aided its growth, whereas HDPE bottles were in demand owing to their availability in larger sizes. As Filipinos were stockpiling home care products such as surface cleaners, dishwashers, and detergents to maintain continuity of supply in their home, as well as avoid frequent shopping trips, larger pack sizes became the most preferred pack type. In addition, the larger HDPE bottles also tend to offer better prices per liter than smaller pack types.

- Less expensive packaging options like flexible aluminum/plastic, flexible plastic, or folding cartons for hot drinks generally have been growing in the Philippines over the past few years and are expected to see further growth over 2022-2026. Contrary to this, expensive pack types like glass jars and PET jars are expected to see declines as consumers continue to be price-conscious. In addition, leading players in hot drinks are set to continue to focus on flexible packaging as a means of differentiation, highlighting indulgent flavors, and high quality. For example, Universal Robina Corp launched Great Taste Vanilla Cream and Great Taste White Crema, with packaging claims such as “creamy linamnam” (“creamy flavor”) and “sweet linamnam” (“sweet flavor”).

- The increasing variety of pack sizes is becoming available in alcoholic drinks highlighting the continual engagement of manufacturers with consumers. Moreover, the demand for sake made the variety of pack sizes even more fragmented in wine. As compared to light grape wine and sparkling wine, which are dominated by the 750ml pack size, soju has 300ml, 750ml, 1,800ml, and other pack sizes.

- Similarly, in beer, AB Heineken’s recently launched Tiger Black, is available in 500ml metal beverage cans as well as 330ml, 500ml, and 1-liter glass bottles. This variety of pack sizes is set to have a positive impact on very price-conscious consumers. Hence, brands will be encouraged to either launch products in smaller pack sizes to reduce the necessary cash outlay or introduce larger-than-standard sizes to offer better value for money in terms of price per liter. It will contribute to a greater variety of pack sizes.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies

The spread of a more infectious and highly vaccine-resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe diseases from new coronavirus variants, with moderate vaccine modifications

Vaccination campaigns progress in developing economies is slower than expected

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and releasing pent-up demand

Longer-lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment, and wages relative to the baseline forecast in 2022-2023

- Recovery Index

-

Recovery Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.