- Overview of COVID-19 conditions in United Kingdom

-

The UK lifts all travel-related COVID-19 restrictions

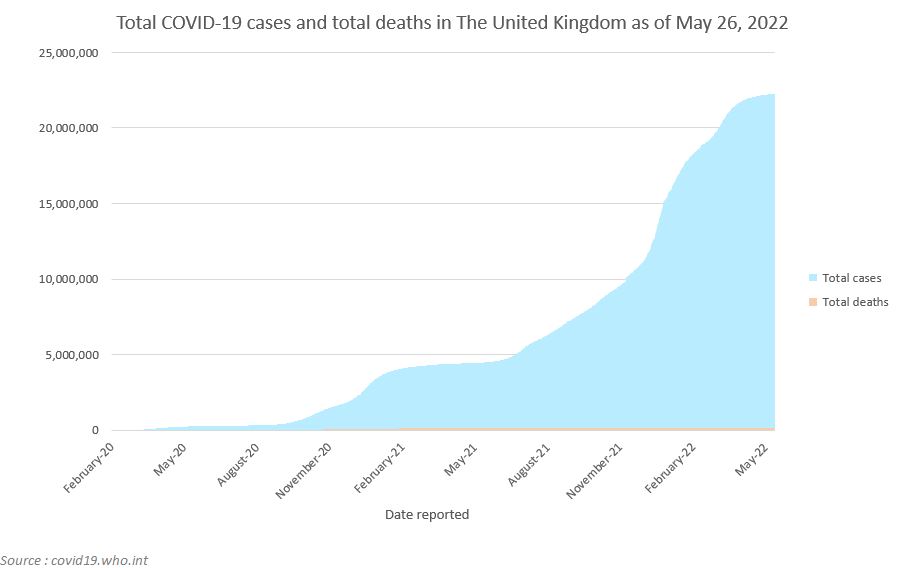

- According to the World Health Organization (WHO), the UK had 22,271,126 COVID-19 cases, 178,221 deaths, and 332,278 cases per million inhabitants as of May 2022.

- In April 2022, as the UK continued to lift all COVID-19-related bans, the country was faced with a renewed surge in COVID-19 hospitalizations due to the new Omicron subvariant detected. Nonetheless, the country further loosened restrictions; lifting all requirements for international travelers and announcing that as of late March 2022, people arriving in the UK will no longer need to take a COVID-19 test, even if they have not been vaccinated.

- According to the WHO, on May 15, 2022, the UK’s total vaccinations reached 142,796,436. The total number of fully vaccinated people per 100 reached 73.2.

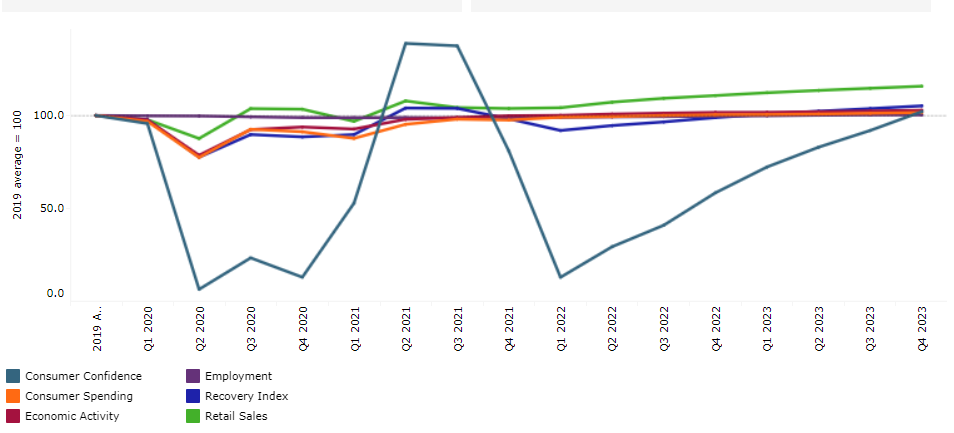

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, United Kingdom

- Impact on GDP

-

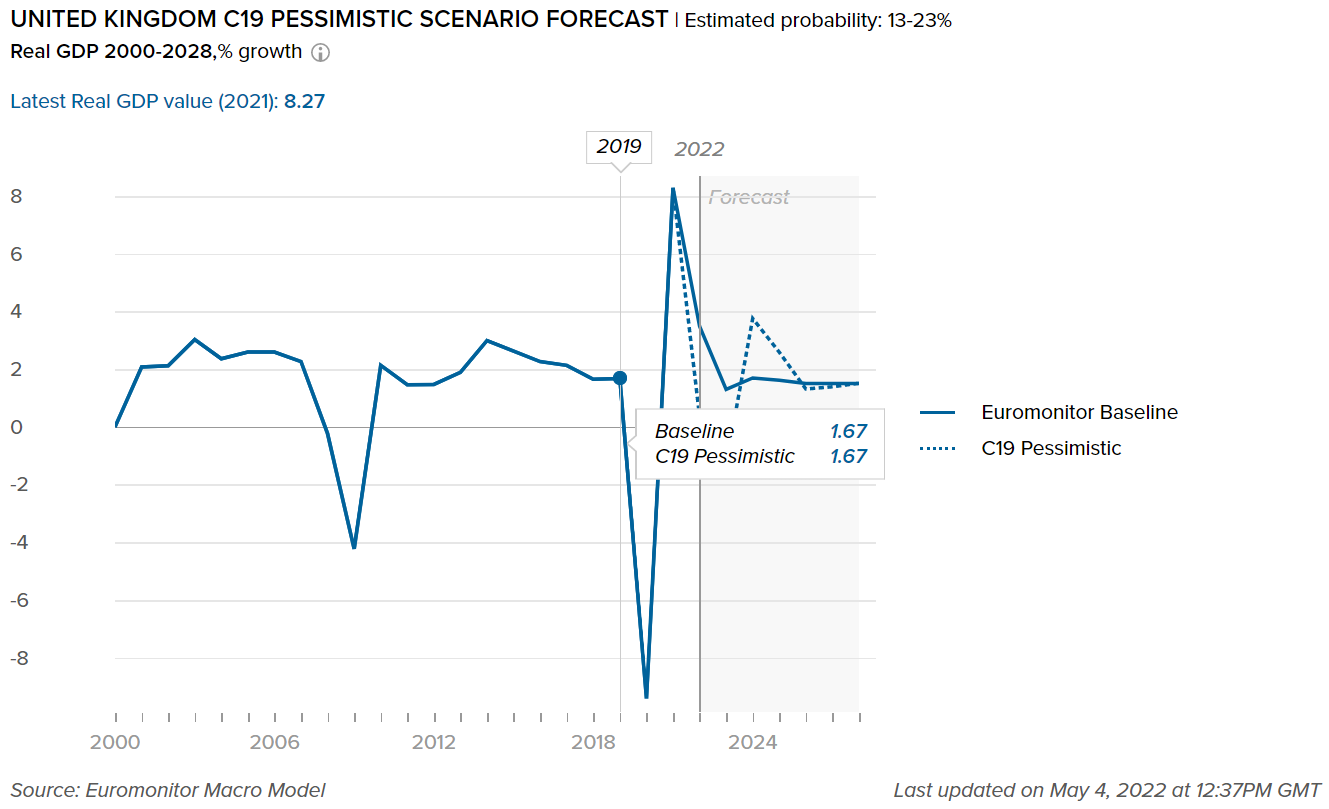

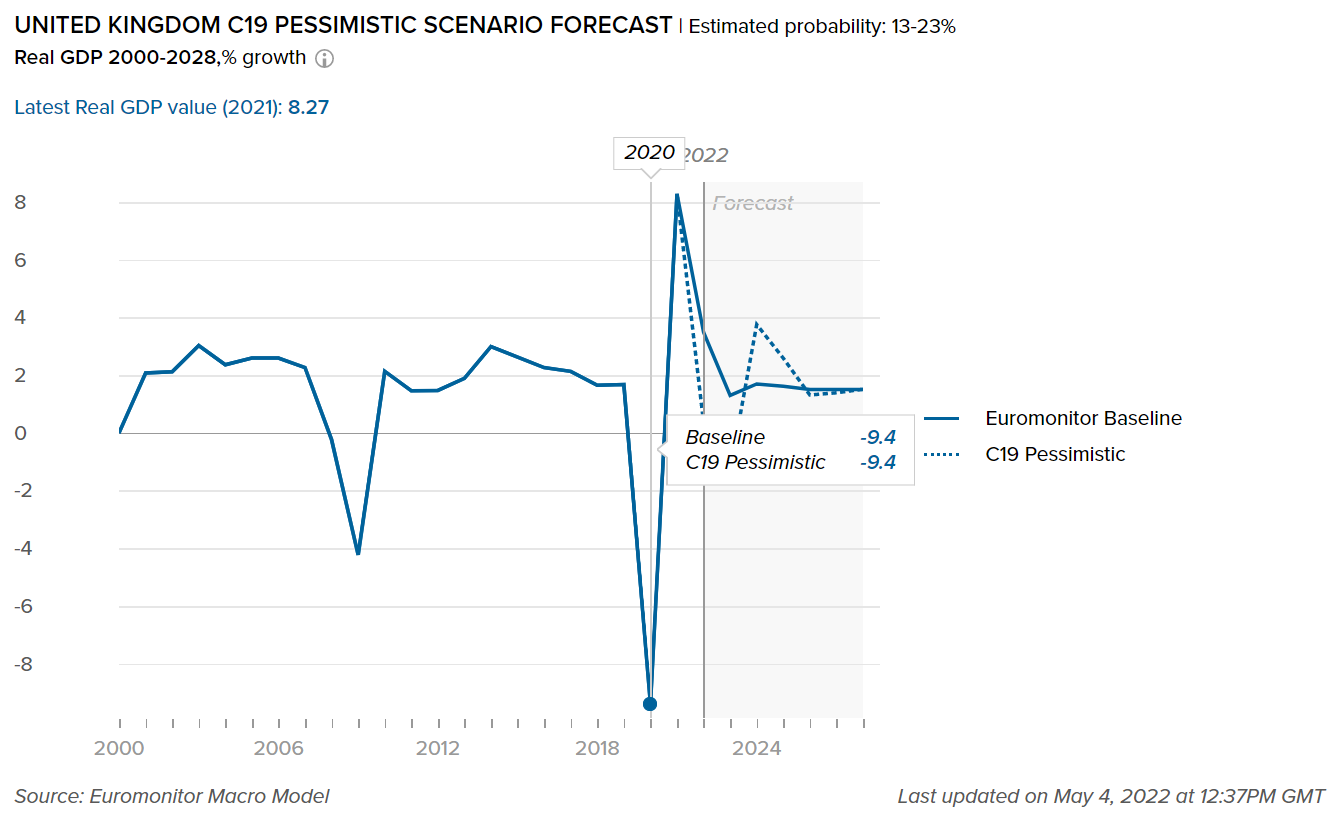

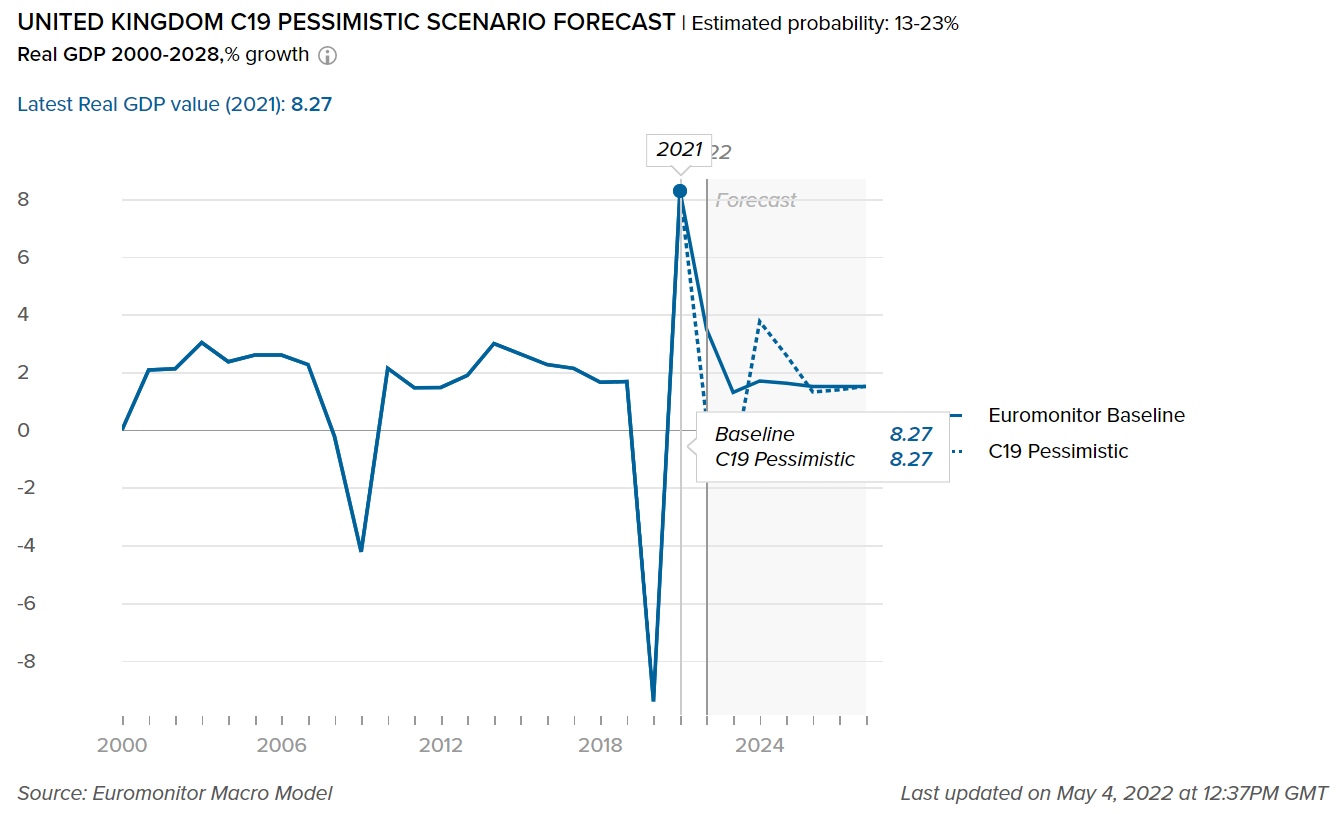

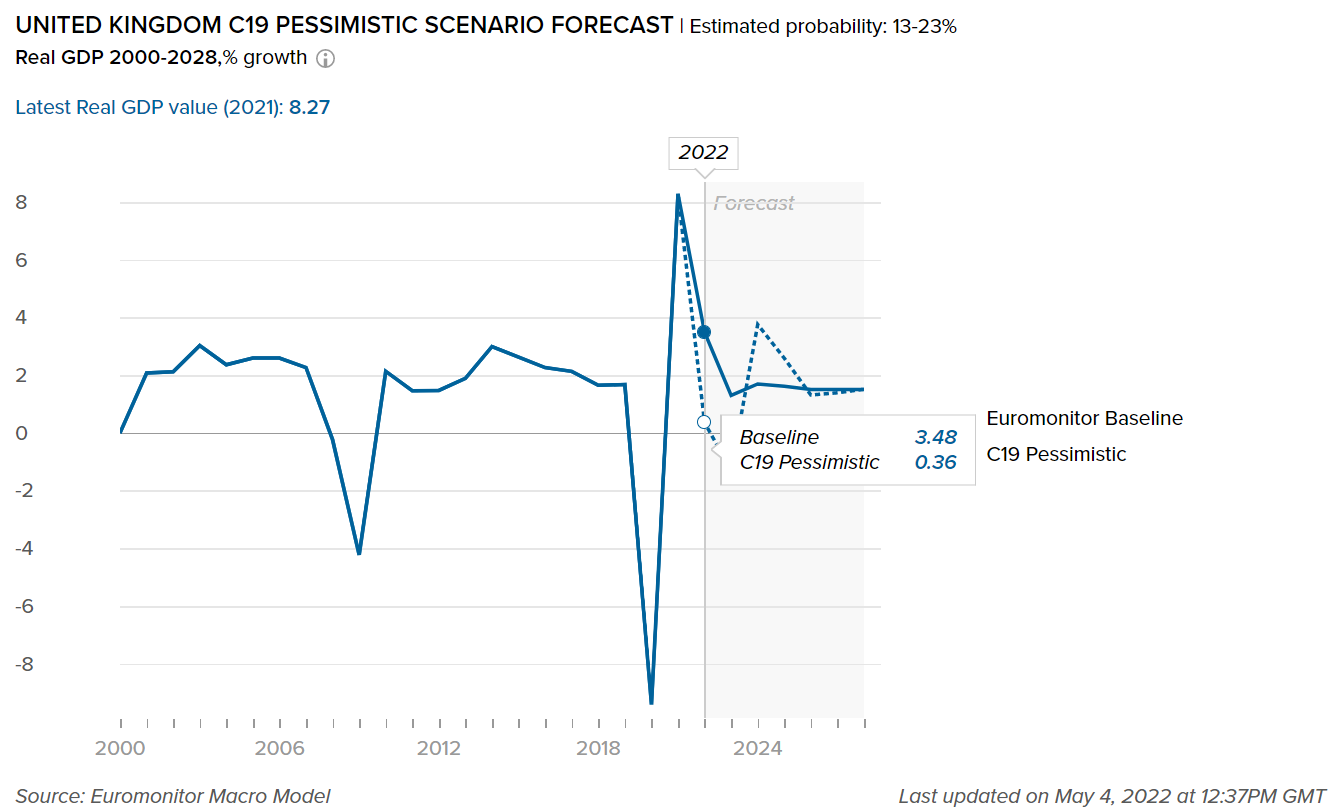

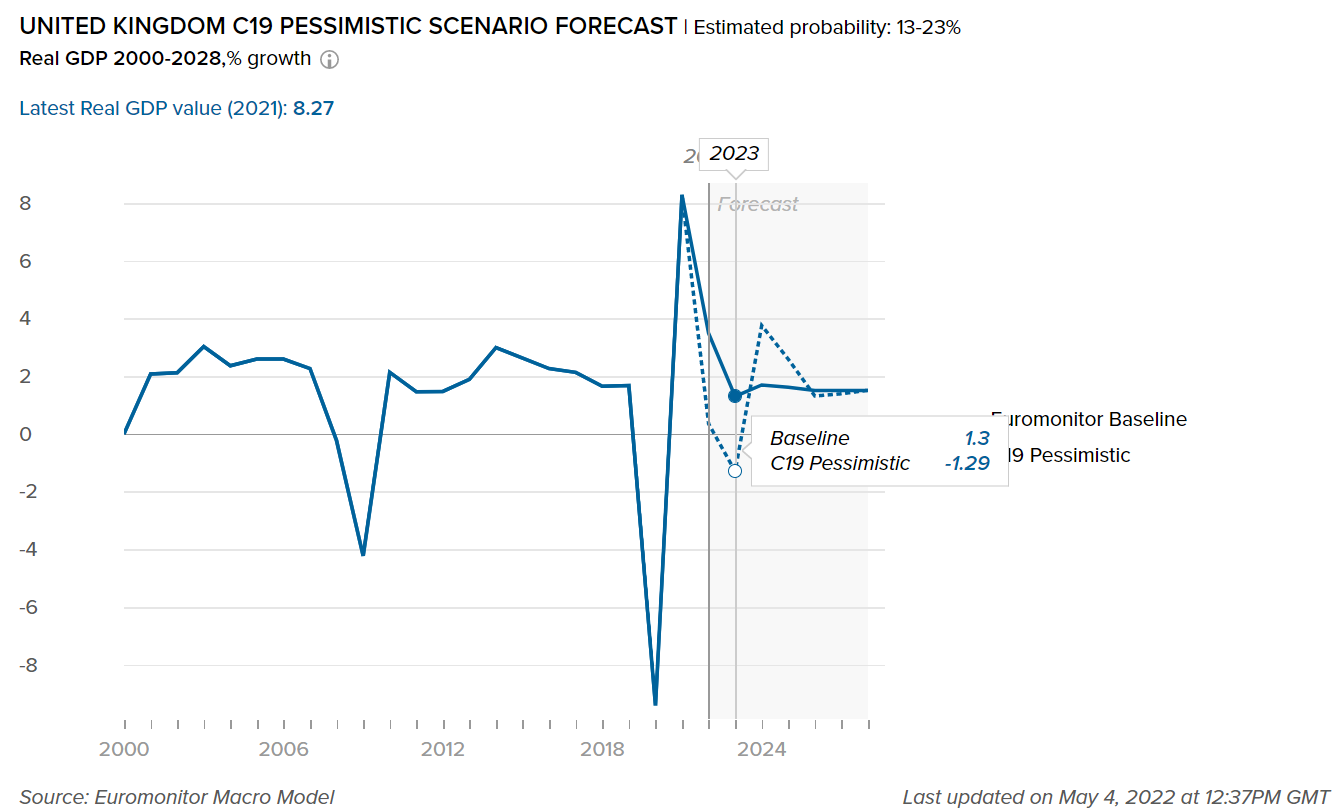

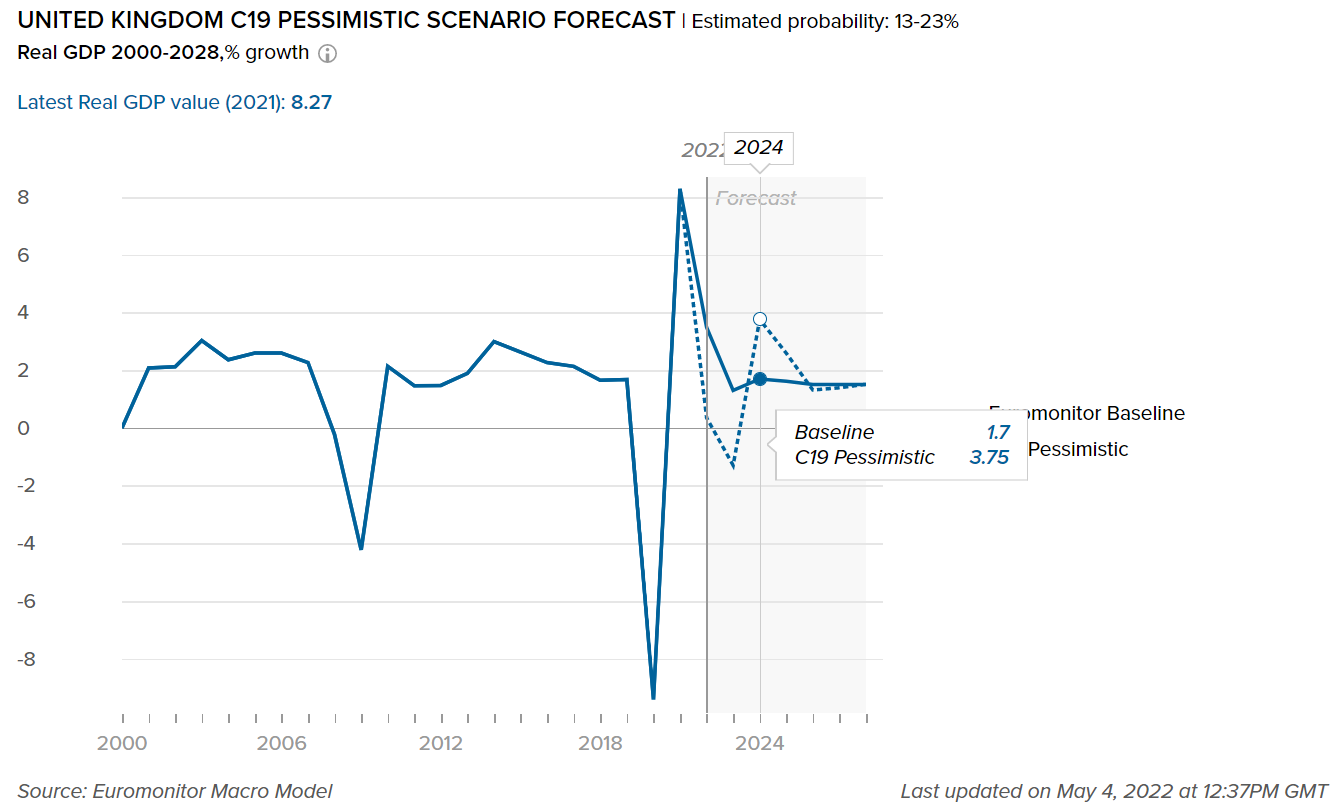

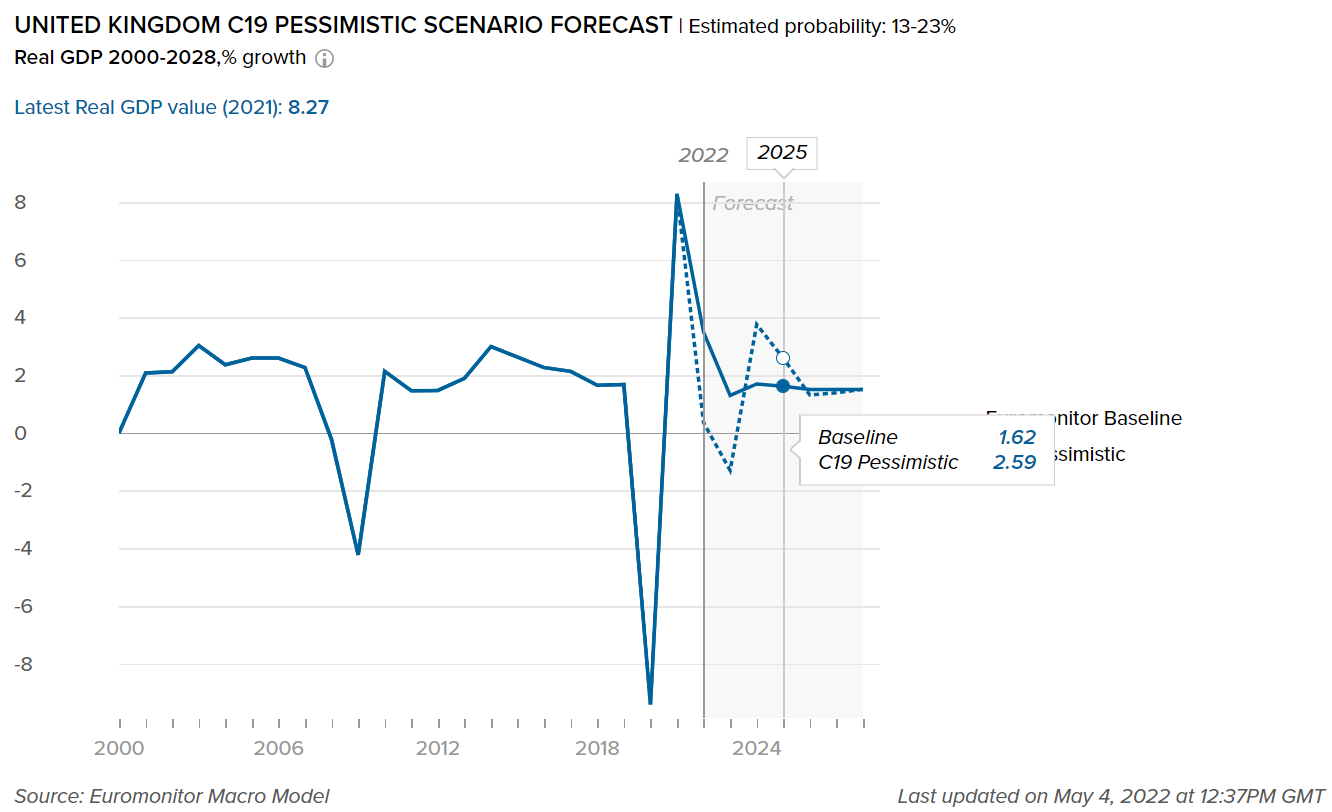

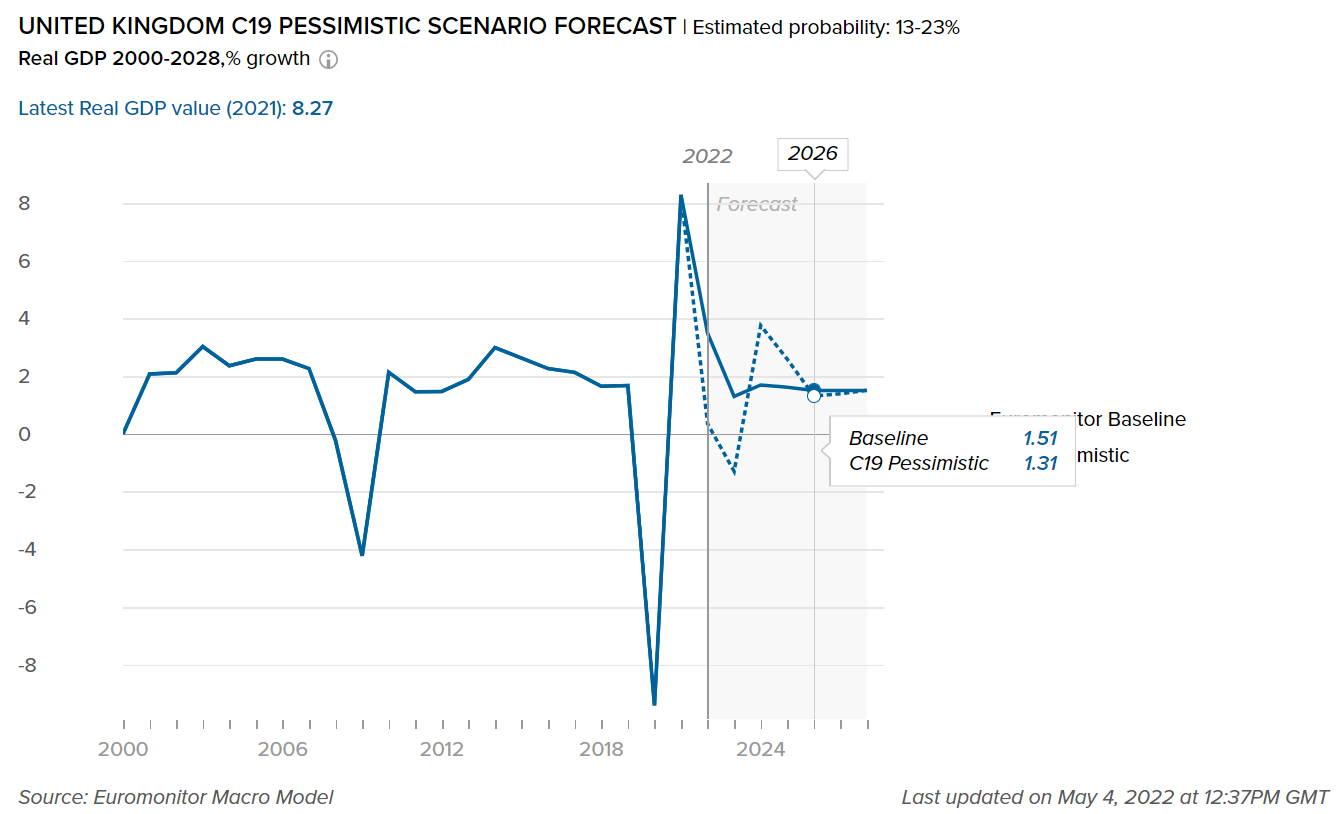

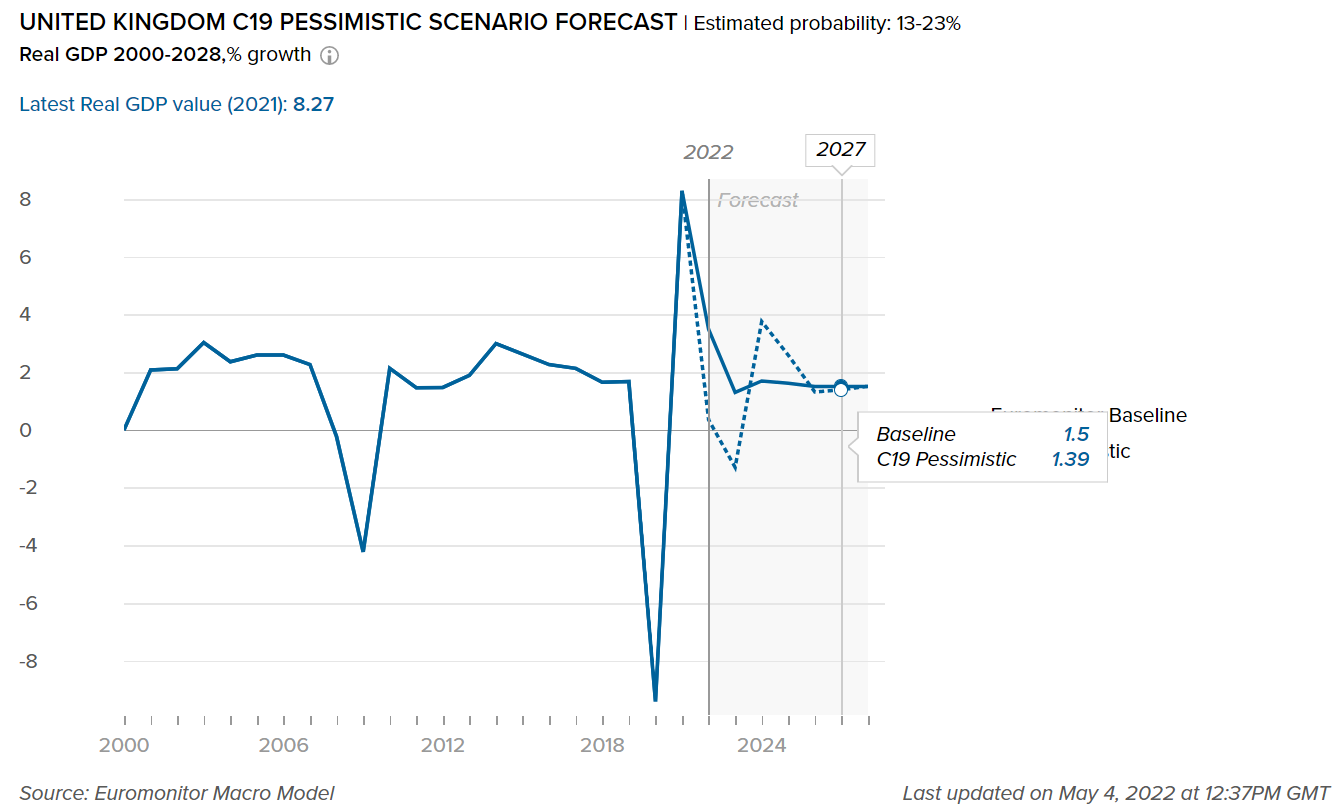

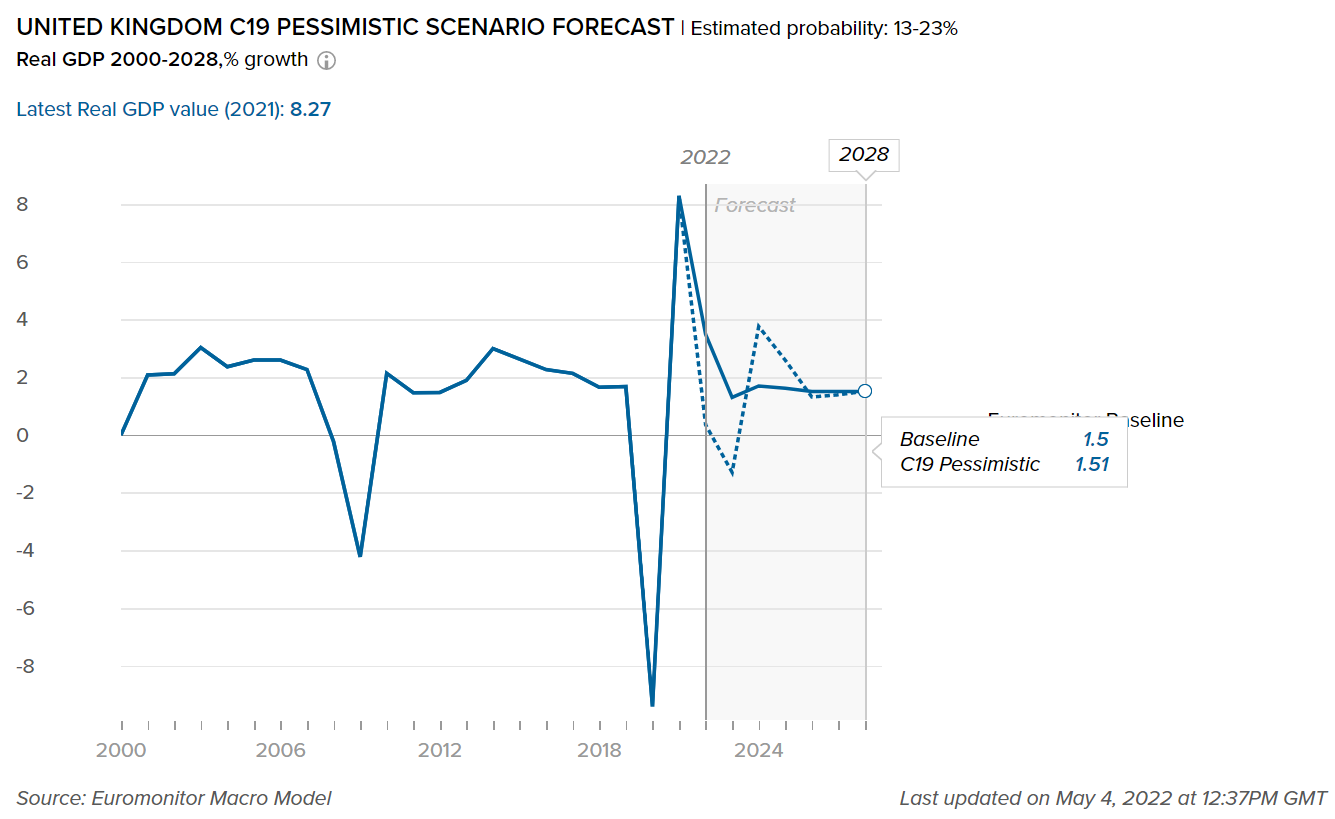

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in the United Kingdom. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Following one of the worst contractions in Western Europe, the UK economy bounced back in 2021

- Following a steep contraction of 9.4% in 2020 as a result of the COVID-19 pandemic shock, real GDP in the UK increased by 8.2 % in 2021, mainly due to improved private and public spending. In 2021, the UK's GDP per capita was USD46,638 compared to an average of USD40,083 in Western Europe. Although the UK economy is anticipated to recover to pre-pandemic levels in real terms by 2022, the persisting labor shortages, supply bottlenecks, and faster-than-expected monetary tightening continue to cloud the near-term economic outlook.

- In 2022, the UK unemployment rate is predicted to be 4.5%, higher than pre-pandemic levels, but lower than the Western Europe average of 7.8%. The ending of the furlough program on September 30, 2021, did not affect unemployment. However, the UK’s labor market has been showing signs of tightening, as sharply rising numbers of vacancies and gradually declining unemployment have been pointing to difficulties in filling vacancies.

- Even though the EU-UK Trade and Cooperation Agreement preserved tariff-free trade between the two parties, the UK's exit from the European single market resulted in higher non-tariff barriers to goods and services mobility between the UK and EU member states. New border procedures, such as safety inspections and customs declarations, made trade with EU members less flexible and more expensive, and are projected to cause shipment delays for some time.

- On the other hand, the UK applied to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and began discussions on a new free trade agreement with India in January 2022, having already secured agreements with Japan, Canada, and Australia, among other countries.

- Impact to Sector Growth

-

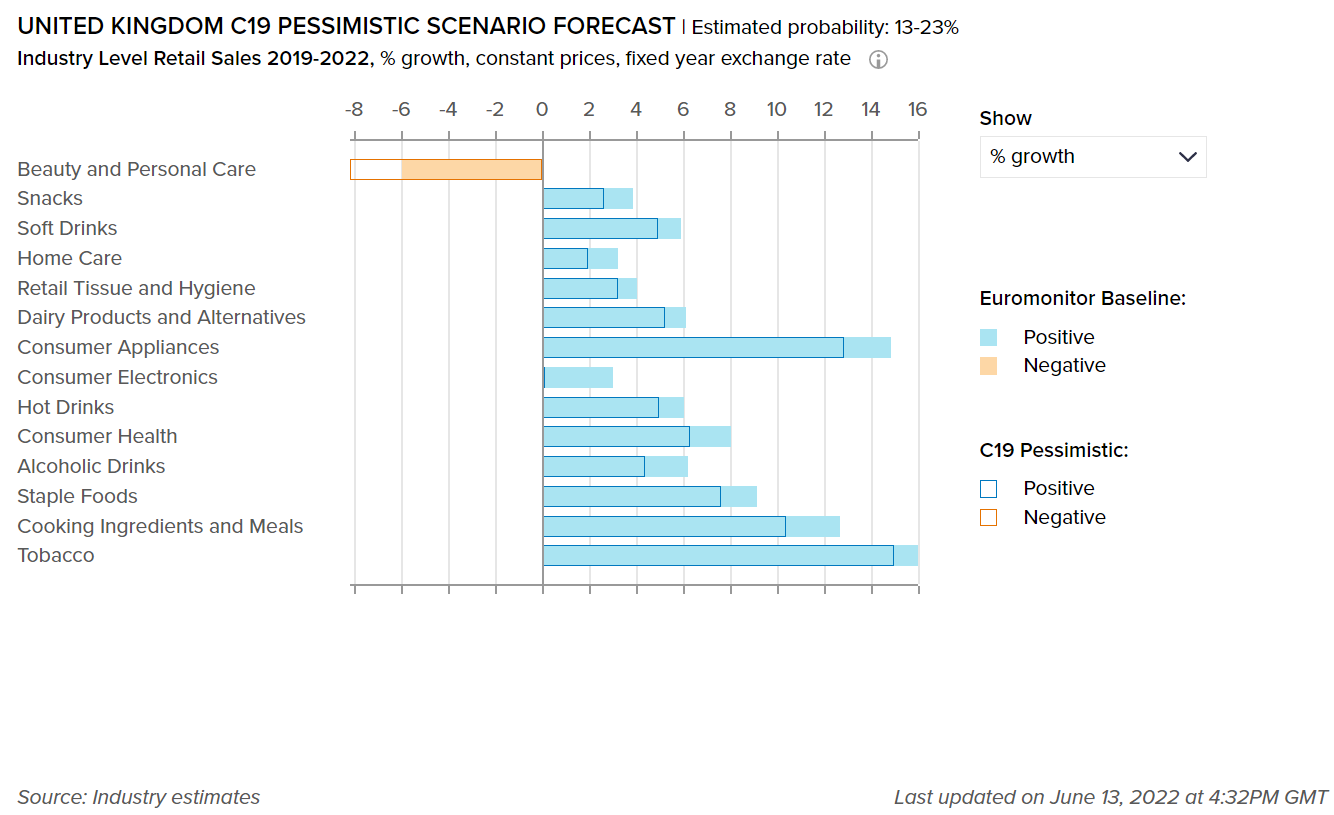

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

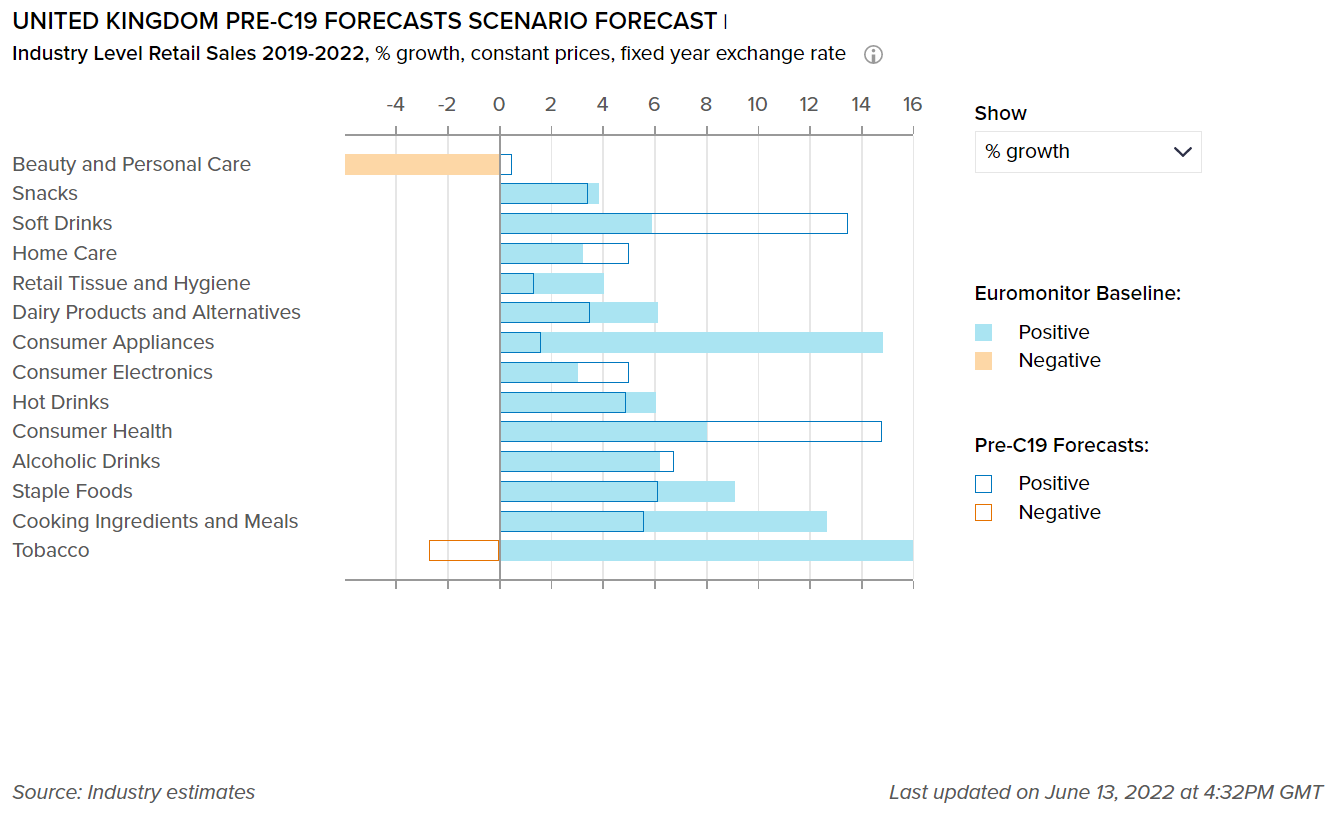

The graph below displays the adjusted forecasts of the percentage growth for the categories mentioned to highlight the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

Packaged food products continue their growth on the back of safety and convenience

- Although the lockdown limitations were lifted in the second quarter of 2021, some of the habits that people were forced to adopt during the pandemic were kept to some extent. Working from home was still used as part of a hybrid working approach, which appears to be popular with both employees and employers. This, combined with increased home isolation during the lockdown period, kept demand for cooking ingredients and ready meals strong, as consumers sought convenience, as well as health credentials in the foods they consumed.

- Organic packaged food in the UK is showing high growth potential within the packaged food category. With the pandemic highlighting the need for well-established supply chains in producing high-quality end-products, more consumers are opting for organic options, which are considered safer. Food safety is a major factor in why people seek organic products, but it is not the only one. Organic products are sought after, according to Euromonitor International's Voice of the Consumer: Health and Nutrition Survey 2021, because they are considered "better for you," and at the same time address environmental issues. In this sense, the expansion of organic packaged food is mostly driven by overarching trends toward health, nutrition, and sustainability.

- New items were introduced to the market in response to this need. Edible Oils Limited, manufacturer of Flora and Mazola oils, presented the U:Me brand, including an organic rapeseed oil for roasting and frying. With more meals prepared at home, customers have become more aware of the products they use, and they are keen to learn more about some of their favorite items.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors mentioned in the UK. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Despite the recovery of some segments, the beauty and personal care industry is still posting value declines

- Overall, beauty and personal care had a better year in 2021 than it did in 2020, though it still has yet to fully recover from the pandemic's effects. According to Euromonitor’s Baseline scenario forecast, beauty and personal care products declined by 5.9% over 2019-2022. However, demand for hand sanitizers remained high in 2021, especially at the start of the year, which the UK spent in lockdown, as concerns lingered over the COVID-19 pandemic and as regular hand washing is known to be an effective way to combat the spread of germs. Nonetheless, the demand for these products decreased compared to the previous year as the vaccine rollout gathered traction and many consumers may have had surplus products left from 2020. On the other hand, sales of depilatories also continued to decline in 2021 as a result of rising preference among UK consumers for longer-term solutions to hair removal, such as laser treatment.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

3,994

4,011

0.1

Home Care Packaging

2,116

2,112

-2.8

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

33,095

33,083

-0.37

Flexible Packaging

47,849

47,255

0.00

Metal

14,082

14,115

0.20

Paper-based Containers

9,699

9,618

0.04

Glass

8,095

8,131

0.44

Liquid Cartons

2,792

2,782

0.00

The UK introduces its Plastic Packaging Tax on April 2022

- To push sustainability efforts, the UK government implemented the Plastic Packaging Tax (PPT) on April 1, 2022. The tax's purpose is to encourage the use of recycled plastic in plastic packaging rather than virgin plastic. This will make it easier to collect and recycle plastic packaging waste in the UK. Any plastic packaging item that contains less than 30% recycled plastic and is made in the UK, imported into the UK, or imported into the country as a filled product, will be subject to tax, with HMRC charging GBP200 per ton. Non-plastic packaging such as folding cartons, glass bottles, and metal aerosol cans are anticipated to benefit from the new regulations.

- In 2022, there will likely be a growing number of items in home care that integrate recycled plastics in packaging, or refillable business models in closed-loop systems, as sustainability continues to impact new product development and strategies. Persil, for example, introduced 100% recyclable bottles. The bottles are now produced with 50% post-consumer recycled plastic, are 100% recyclable, and the dosing ball that was previously included with each bottle has been removed, reducing the quantity of virgin plastic in Persil bottles by over 1,000 tonnes yearly.

- As part of its #GetPlasticWise campaign, Unilever is evaluating the possibility of refill bottles for liquid detergents. The company launched refill trials in the UK for its brands Persil, Cif, and Simple. Unilever is experimenting with two refill models: touch-free refill machines that dispense Persil laundry liquid in reusable aluminum or stainless-steel bottles, and in-home refills, with Cif Ecorefills which offer an in-home refill experience to customers, using 10x concentrated refill for sprays allowing customers to use a Cif spray bottle for life. Ecorefills also use 75% less plastic than traditional cleaning bottles.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recover Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is officially the best measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.