Overview

- Packaging Overview

-

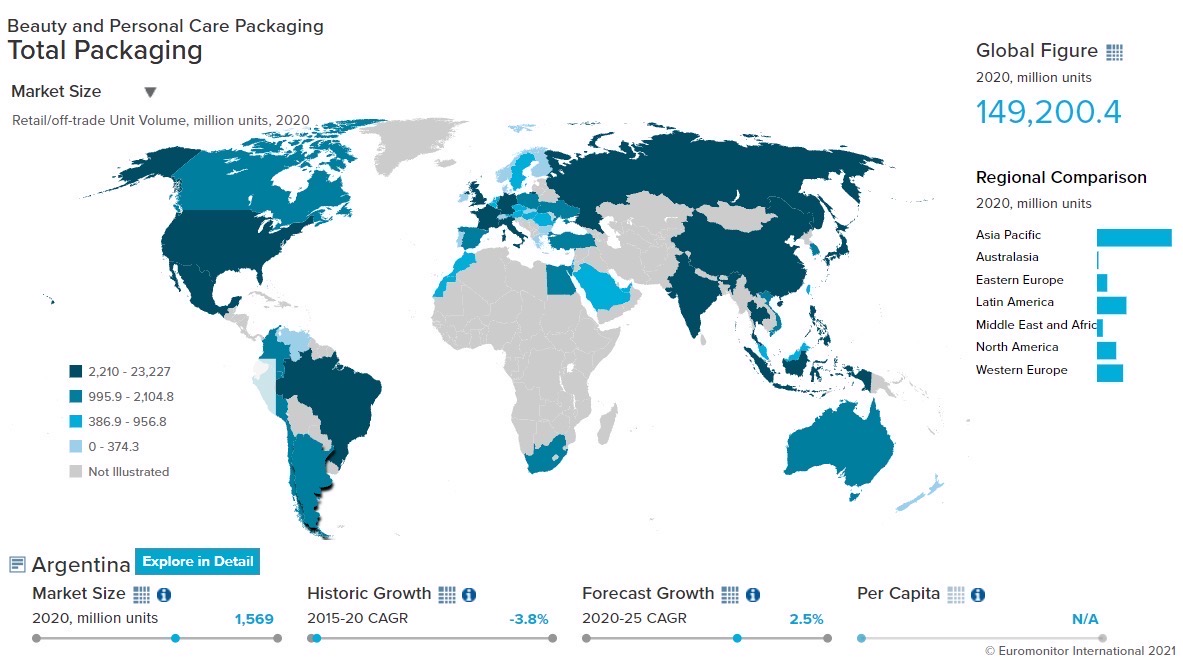

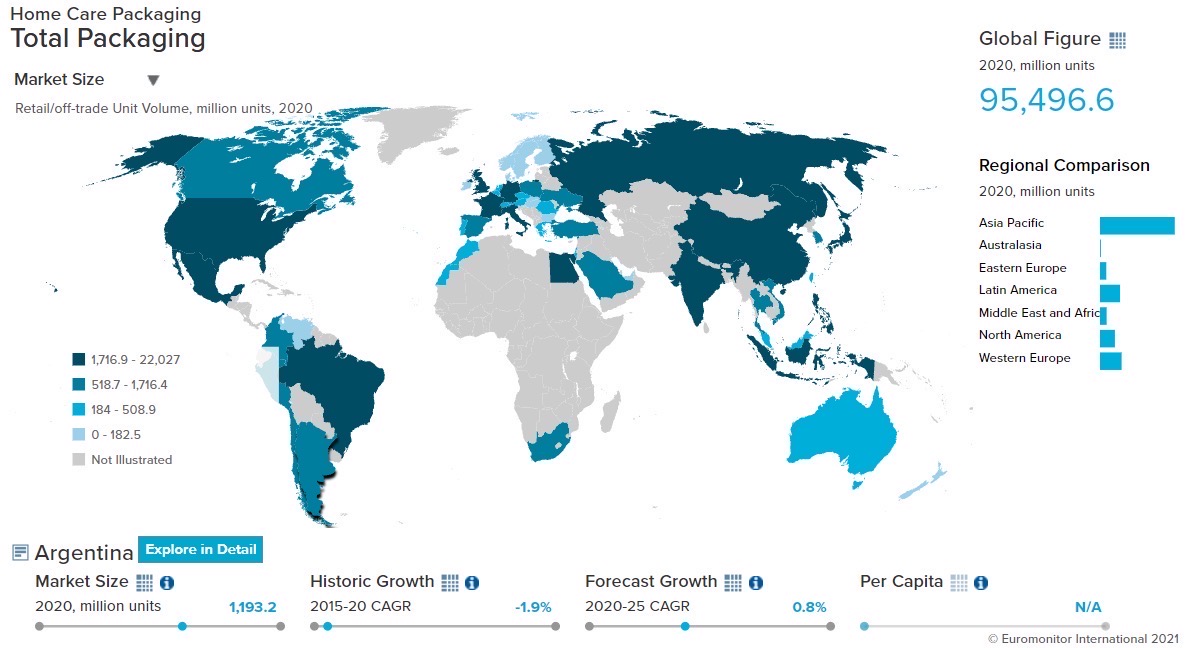

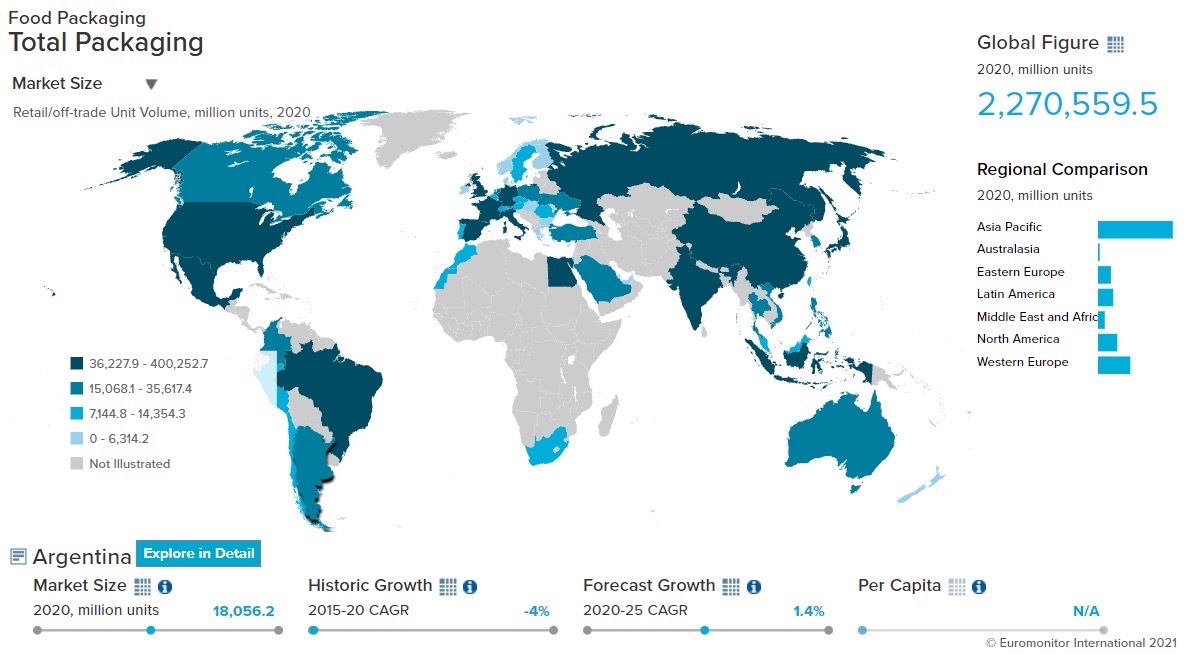

2020 Total Packaging Market Size (million units):

34,790

2015-20 Total Packaging Historic CAGR:

-3.0%

2021-25 Total Packaging Forecast CAGR:

-0.1%

Packaging Industry

2020 Market Size (million units)

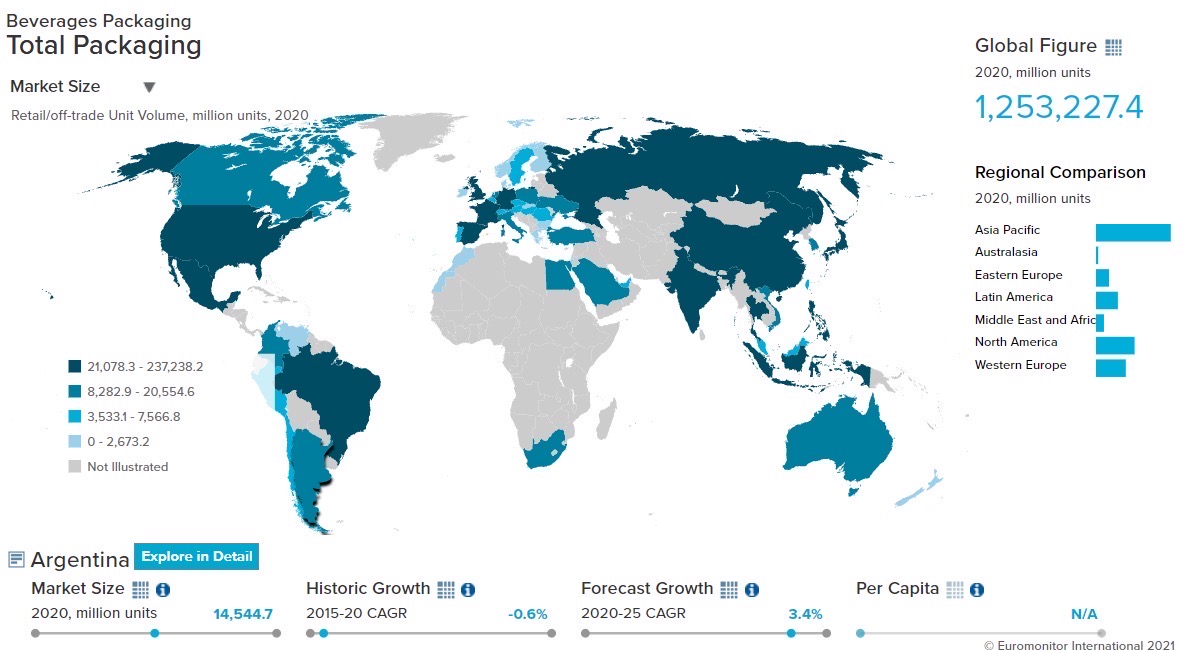

Beverages Packaging

13,757

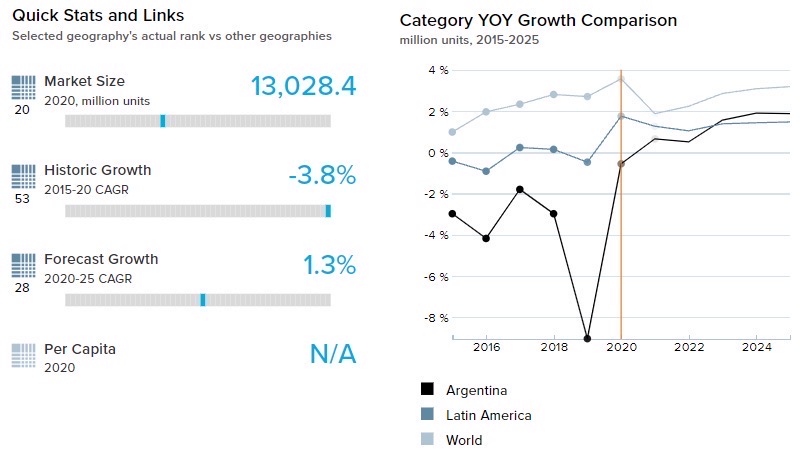

Food Packaging

18,056

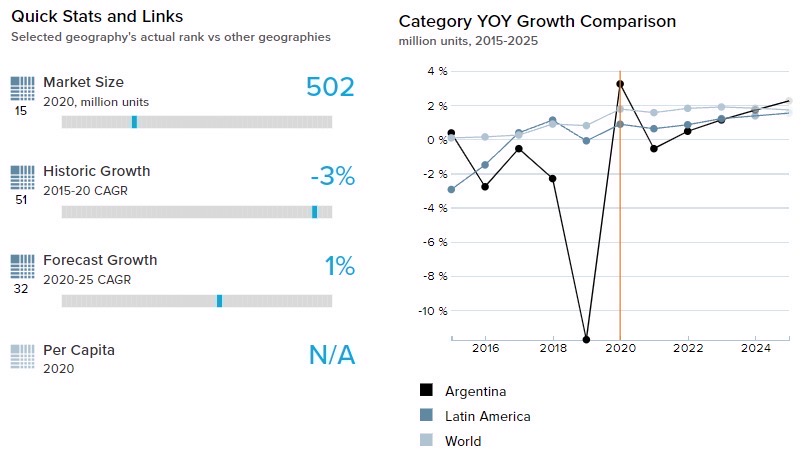

Beauty and Personal Care Packaging

1,569

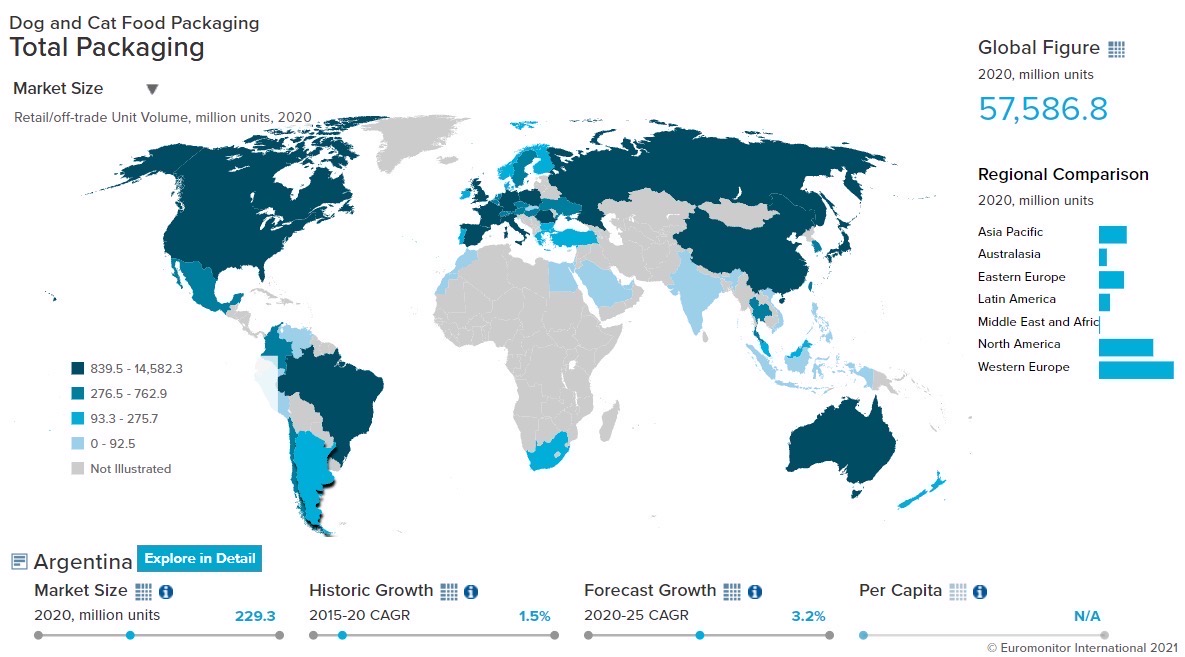

Dog and Cat Food Packaging

215

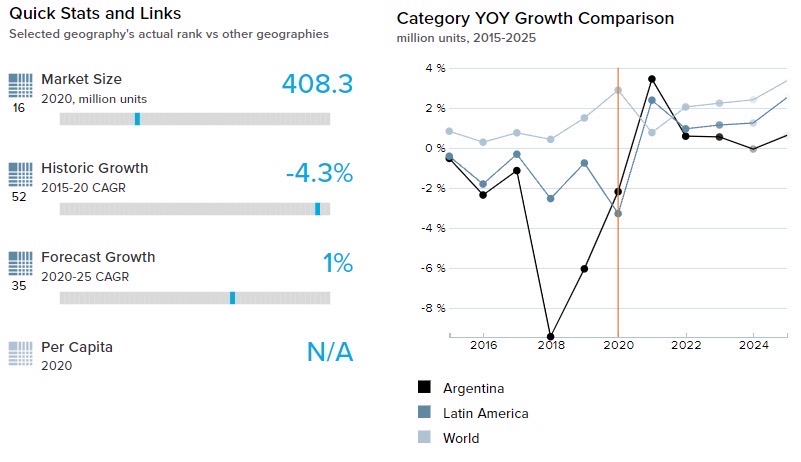

Home Care Packaging

1,193

Packaging Type

2020 Market Size (million units)

Rigid Plastic

8,975

Flexible Packaging

16,991

Metal

2,641

Paper-based Containers

1,774

Glass

2,688

Liquid Cartons

1,718

- Key Trends

-

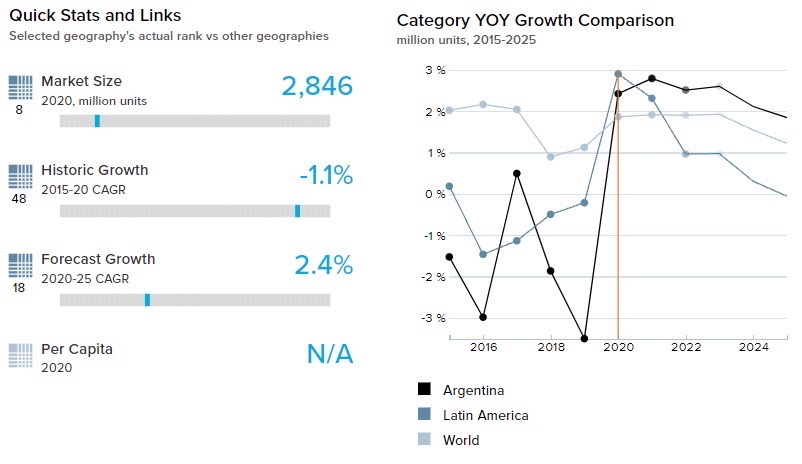

The economic impact of COVID-19 and home seclusion favored the sales of larger value packs in most of the categories. The large value pack offered lower cost per kg which proved popular in the food, home care, beauty, personal care, and beverages category. Larger value packs mostly come in flexible pack types. Hence, flexible packaging type witnessed growth over the 2021 period.

Smaller pack sizes that had previously gained ground from on-the-go trends in food, beverages, fragrances, and color cosmetics have suffered severely due to the COVID-19 pandemic. Small formats of 200ml Tetra Pak flavored milk and juices, which are ordinarily popular for school children’s lunchboxes, have seen demand nosedive as schools across Argentina closed. 1-liter packs of milk and family-size juice packages have fared much better. Small packets of salty snacks usually purchased in kiosks also suffered as kiosks in some of Argentina’s cities were closed during the pandemic’s longest lockdowns..

- Packaging Legislation

-

Updated and empowered legislation to handle packaging waste is urgently needed in Argentina. Argentina produces over 900,000 tons of waste each year, of which only around 26% is recycled. The remaining waste goes into landfills and garbage dumps. The recycling industry in Argentina is working well below capacity and holds the potential to be a source of employment for thousands of Argentines.

The Packaging Law failed to be successfully promoted for over 25 years. Part of the problem is the disconnect between authorities in Buenos Aires and those who live and work in the provinces.

- Recycling and the Environment

-

Argentina’s government continues to encourage the separation of waste. The Ombudsman’s office of Buenos Aires presented a bill to the legislature to reward residents who separate waste in their homes with discounts of up to 50% on their lighting, street sweeping, and cleaning tax (ABL). Multiple collection points have been arranged to collect dry waste or recyclable material. The material collected at these collection points is further sent to specialized processing units, called Green Centers, for separation and recycling.

- Packaging Design and Labelling

-

As the competitive landscape became even tougher against the backdrop of the economic impact of COVID-19, companies are investing heavily in the research and development of new pack designs and new pack types. Recent times have seen a rise of packs with zip/press closure, new folding cartons, and new graphics/prints in packaging.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh-cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Due to increased health awareness among the consumers, perceived health benefits of hot drinks boosted its sales in 2020. Being the dominant pack type for the category, flexible packaging grew by 3.9% by volume in 2020. However, premium products in this category such as instant coffee packaged in glass jars saw a decline owing to the economic impact of COVID-19. On the other hand, consumption of instant coffee packaged in plastic pouches, stand-up pouches increased which further boosted the flexible pack type.

- The popular plant-based hot drink yerba mate, which is packaged in flexible paper, saw a decline of 2.9% by volume in 2020. This can be attributed to the low spending power of consumers and the consumer shift towards beverages such as herbal tea and green tea as they have perceived health benefits.

- The healthy perception of tea variants such as green tea, herbal tea, and fruit tea helped tea grow in 2020. These products are mostly packaged in flexible plastic as it offers convenience and keeps the product fresh for a longer period. As a result, flexible plastic grew by 1.1% by volume in 2020, driving the overall growth in flexible pack type in 2020.

- Trends

-

- The soft drinks industry witnessed disruption in 2020 as foodservice/restaurants faced closures and the purchasing power of consumers declined. The players reacted to this situation by launching larger value pack sizes of 600ml, 750ml, and 1l PET bottles. As a result, PET pack types grew by 3.9% in terms of volume in 2020.

- The sales of returnable glass bottles were affected negatively by health and hygiene concerns as consumers preferred one-way packaging which reduced their trips to outlets/shops. As a result, sales of glass pack types declined by 2.6% by volume in 2020. This trend further boosted the revenue of PET bottles and metal beverage cans.

- Outlook

-

- Alcoholic drinks witnessed major challenges owing to the closure of foodservice channels (including restaurants) and reduced purchasing power. As glass bottles dominate the foodservice channel, they will continue to lose ground to metal beverage cans. The latter is expected to gain momentum as they are easy to transport, store, and consume. As a result, it will be a popular packaging choice in beer, wine, and RTD alcohol. For 2021-25, metal beverage cans are likely become the main pack type in beer, wine, and RTDs category.

- With the gradual relaxation of the restrictions imposed on society due to the COVID-19 pandemic, the sale of smaller pack sizes is expected to start to improve as on-the-go consumption begins moving back towards normal levels. In addition, foodservice sales of both soft drinks and their packaging are expected to see a strong rebound in 2022 with growth remaining strong in 2023 and positive over the 2021-2025 period.

- With gradual relaxation of COVID-19 restrictions, hot drinks are expected to return to their normal levels of consumption due to a decline in at-home consumption, which will, in turn, impact major pack types such as glass jars. Flexible packaging such as flexible plastic is expected to grow over the forecast period as it offers convenience and is economical. In addition, these pack types keep product quality intact for longer periods, thus making them the preferred pack types for various categories, such as flavored powdered drinks.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

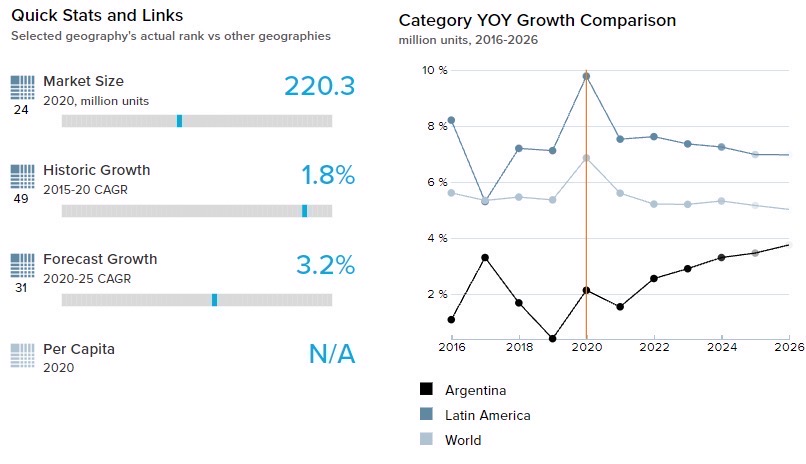

- Due to the dominance of flexible packaging in dry cat and dog food, it has a stronghold on dog and cat food packaging in Argentina. Flexible plastic offers a wide range of design and color options which helps to differentiate it from the competition, and it is also an economical option. Flexible packaging is witnessing a surge of creativity such as attractive designs, and colors, pouches with zip/press closures.

- Despite the dominance of flexible packaging in the dog and cat food industry in Argentina, the economic impact of COVID-19 made a dent in flexible packaging in this category. Flexible plastic recorded a 3.4% decline by volume in 2020 as overall sales of dog and cat food declined due to the COVID-19 pandemic. Despite the adversities, stand-up pouches made their way into cat and dog treats and mixers. Stand-up pouches grew by 0.8% by volume in 2020. The growth can be attributed to consumer demand for affordable cat and dog treats and mixers.

- Trends

-

- Several brands in the economy and mid-price segments are changing their product appearance to bear more resemblance to premium packaging. The strategy behind this move is to lure new and young pet owners. For this purpose, companies changed the color combination of the packaging as well as they replaced cartoons on the packaging with real photos of cats and dogs. For example, brand Kongo by Agroindustrias Baires designed a new package that reflects the product’s 100% natural content.

- Previously wet cat and dog food categories were dominated by metal food cans, however, price sensitivity caused brick liquid cartons such as Tetra Recart to grow exponentially in the last two years. Brick liquid cartons are eco-friendly, economical, easy to transport, and easy to store. The national company Sagemuller launched the first Tetra Recart in wet dog food in 340g and 500g sizes during 2019 and after that other players followed the suit.

- Outlook

-

- Family pack sizes could become appealing to lower and middle-income consumers as their price per volume is much lower than smaller pack sizes. Dry cat and dog food benefit from the rising popularity of larger flexible plastic packs such as 15kg and 21kg. E-commerce is expected to further boost this trend as they can deliver heavy packs to the consumer’s doorstep.

- On the other hand, dog and cat treats and mixers will see a rising popularity of smaller pack sizes due to the economic impact of COVID-19. Dog and cat treats and mixers are expected to grow at 2.4% by volume over 2021-25.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- Increased hygiene awareness due to the pandemic led to more demand for personal care products such as bar soaps, liquid soaps, shampoo, etc. These products are mainly packaged in flexible plastic, stand-up pouches, and PET bottles. The increased demand helped flexible packaging record a 3.2% growth by volume in 2020.

- As demand for larger pack sizes rose during the pandemic, companies preferred stand-up pouches for larger packs of products such as liquid soaps and hand sanitizers. As a result, the stand-up pouch pack type rose by 19.3% by volume in 2020.

- Trends

-

- The COVID-19 pandemic negatively impacted color cosmetics packaging in Argentina, including categories such as blusher/bronzer/highlighter, lipstick, and foundation/concealer. This could be attributed to the decline in social or work gatherings outside the home. As a result, rigid plastic in the color cosmetics category declined by 19.0% by volume in 2020.

- During the pandemic, people wore masks that left the eyes exposed but covered most of the face. As a result, women continued to invest in eye make-up but cut back on most facial makeup. This led to a 26% decline in HDPE bottles in color cosmetics in 2020.

- Before the pandemic, Argentinians preferred smaller pack types over larger ones as the consumers are more price sensitive. But to reduce trips to the store, consumers started preferring larger and more value-for-money pack sizes. In the same period, larger metal packs over 120ml in deodorants, and flexible plastic packs over 400ml in hygiene products, gained popularity.

- Outlook

-

- Increased vaccination rates and effective social distancing measures should lead to declining COVID-19 infection rates, allowing a resumption of outdoor activity, social occasions, and business travel. This is expected to boost demand for products such as baby and adult sun care, salon hair care, foundation, lip liner, and eyeliner. As a result, sun care packaging, skincare packaging, and color cosmetics packaging will grow at 10.5%, 3.1%, 4.0% CAGR over 2021-25 in terms of volume.

- As online retailers increasingly become more important in the beauty and personal care industry, brands are adjusting and repositioning their packaging strategy. As a result, brand owners are coming up with new and innovative packaging solutions, keeping hygiene, touchpoints, and safety in mind, as these attributes are expected to be a key driver for beauty and personal care product packaging over the 2021-2025 period.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- Plastic pouch packaging has continued to be a key pack type, helping to meet the unprecedented demand for liquid cleaners, sanitizers, and detergents. Apart from its convenience and cost-efficiency, flexible packaging is being chosen by leading brands for its sustainable nature and role in plastic waste reduction – for example, one 3-liter plastic pouch is equivalent to twelve 250ml surface cleaner bottles. As a result, flexible plastic grew 5.7% by volume in 2020.

- During periods of financial adversity, middle- and low-income households look for the best value products. Low and middle-income families are typically targeted by local brands with new larger value pack sizes. Large packs are mostly packaged in plastic pouches. Thus, plastic pouches have now become the most important type of packaging for liquid fabric softeners, laundry aids, bathroom cleaners, kitchen cleaners, and glass/window cleaners, while also accounting for a strong share in liquid detergents.

- Trends

-

- Home care products saw a spike in demand due to COVID-19 as customers stockpiled these products in anticipation of supply shortages and movement restrictions. Products such as disinfectants, bleach, bathroom cleaners, and toilet care products were stockpiled to reduce the frequency of shopping trips and minimize the amount of time spent outside their homes (to avoid contracting the virus).

- Reckitt Benckiser has begun to discontinue its rigid plastic bottles and replace them with plastic pouches. The company has already made the switch for Woolite in fine fabric detergents and Vanish in in-wash stain removers. Sales of refill packs are also being driven in Argentina by the economic recession that was already affecting the country before the pandemic and has since been exacerbated by the measures taken to try and contain the spread of the virus.

- Outlook

-

- Sales of concentrated liquid detergent have huge potential over 2021-25 as they are easy to transport and store, help save water, and are eco-friendly as they save packaging material. The substitution of powder detergents with liquid detergents will boost demand for plastic pouches and HDPE bottles, which are the typical pack types for liquid detergents. But players in concentrated liquid detergents will need to continue to invest in consumer education and marketing to promote the benefits of these products over powder detergents.

- Increasing awareness about pollution among consumers is pushing the players towards sustainable packaging solutions. The outlook for environmentally friendly packaging is positive, as younger consumers are considerably more concerned about protecting the environment than middle-aged and elderly consumers, suggesting a potential for the trend towards such packaging to further build momentum over 2021-25 and beyond.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- Flexible plastic is becoming more prevalent in ready meals packaging thanks to interest from private-label lines and brands that are positioned in the economy price segment. The great advantage of flexible plastic is its lower cost and it eliminates the need to use secondary packaging. Despite the trend, the pandemic-induced movement restrictions reduced ready meals sales as consumers had more free time to cook, which resulted in an overall sales decline of 0.8% by volume in 2020.

- Consumer demand for milk products in 2020 shifted from flexible plastic packaging formats to brick liquid cartons as consumers stockpiled shelf-stable milk as reserves due to the COVID-19 pandemic. Many new players introduced new lines in Tetra Pak and began to offer shelf-stable milk in brick liquid cartons at low prices. As a result, flexible packaging declined by 0.4% by volume in 2020.

- Trends

-

- Ready meals packaging saw very little development in 2020. Consumers showed a strong preference for homemade meals at the end of the review period, with ready meals viewed as excessively expensive in a time of declining disposable income levels and economic uncertainty. The serious economic crisis in the country is thus limiting the development of ready meal packaging, which is in turn, limiting manufacturers’ willingness to invest in the innovation and development of new pack types and sizes.

- Folding cartons has a monopoly on primary packaging in frozen pizza and is used by all brands, whilst flexible plastic is used as secondary packaging to maintain the quality of the product. Most companies use very similar formats, colors, and designs. According to trade sources, significant changes in packaging are not expected from the leading brands.

- Outlook

-

- There is expected to be a rise in single-person households in Argentina as consumers are getting married later in life and are living alone for a longer period. This will prompt manufacturers to offer smaller pack sizes in ready meals and will also stimulate demand for ready meals in general, as consumers living alone are usually less willing to spend more time preparing meals from scratch.

- In the prepared baby food category, Nutribaby launched the first plastic pouch in a 90g pack size in 2018. Since then, many companies have followed the same suit since plastic pouches offer several benefits over thin wall plastic. Companies are experimenting with plastic pouch designs and pack sizes to differentiate from their competitors. Hence, plastic pouches in the prepared baby food category are expected to grow at 8.7% CAGR by volume in the 2021-2025 period.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Argentina

-

Argentina’s Ministry of Health declares the country to be in the fourth wave of COVID-19

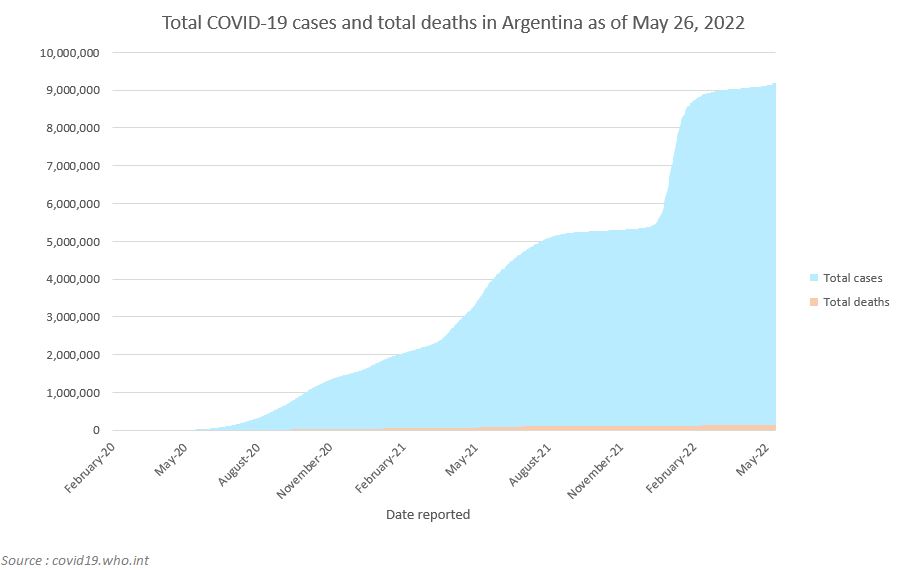

- According to the World Health Organization (WHO), Argentina had 9,178,795 COVID-19 cases, with 128,825 deaths as of May 26, 2022.

- The recent rise in COVID-19 cases in the country prompted the Minister of Health, Carla Vizotti, to state that the country is currently in the fourth wave of COVID-19. From April 18, the COVID-19 testing policy has been modified to prioritize the diagnosis of COVID-19 in people with respiratory diseases, those over the age of 50, and those with a recent history of travel.

- According to the WHO, Argentina administered a total of 100,976,399 vaccines as of May 20, 2022, with 82.7% of people fully vaccinated and 90.8% of people having received at least one dose of a vaccine.

- In October 2021, the World Bank announced a donation to Argentina’s national vaccine plan of USD500 million. This funding has been used to purchase 40 million vaccines to complete the adult program and move forward with vaccinations for teenagers by the end of 2021. The Argentinian National Administration of Drugs, Food, and Medical Technology (ANMAT) authorized the use of the Sinopharm vaccine for children aged 3-11 years.

- As per a report published by La Nacion, in terms of provinces with the highest percentage of doses, Buenos Aires leads with 17,541,141, followed by Santa Fe and Cordoba with 3,536,418 and 3,760,450, respectively. In addition, it is estimated that approximately more than half of the population has received a booster dose to safeguard against the virus.

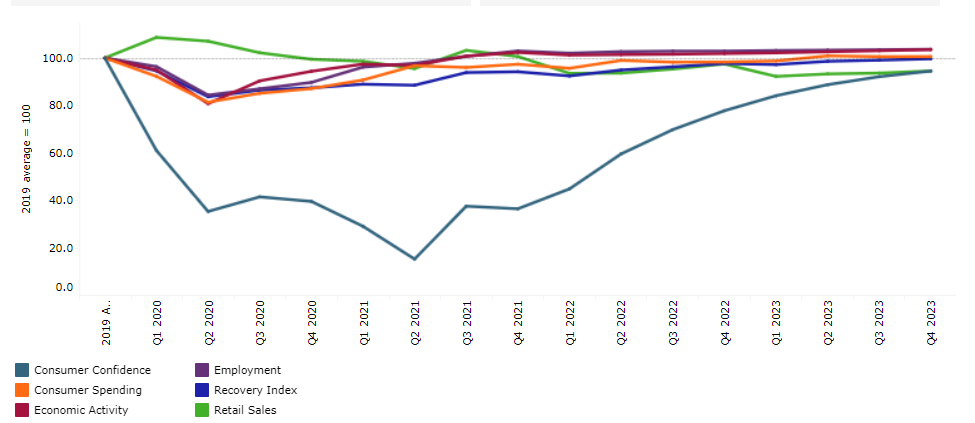

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Argentina

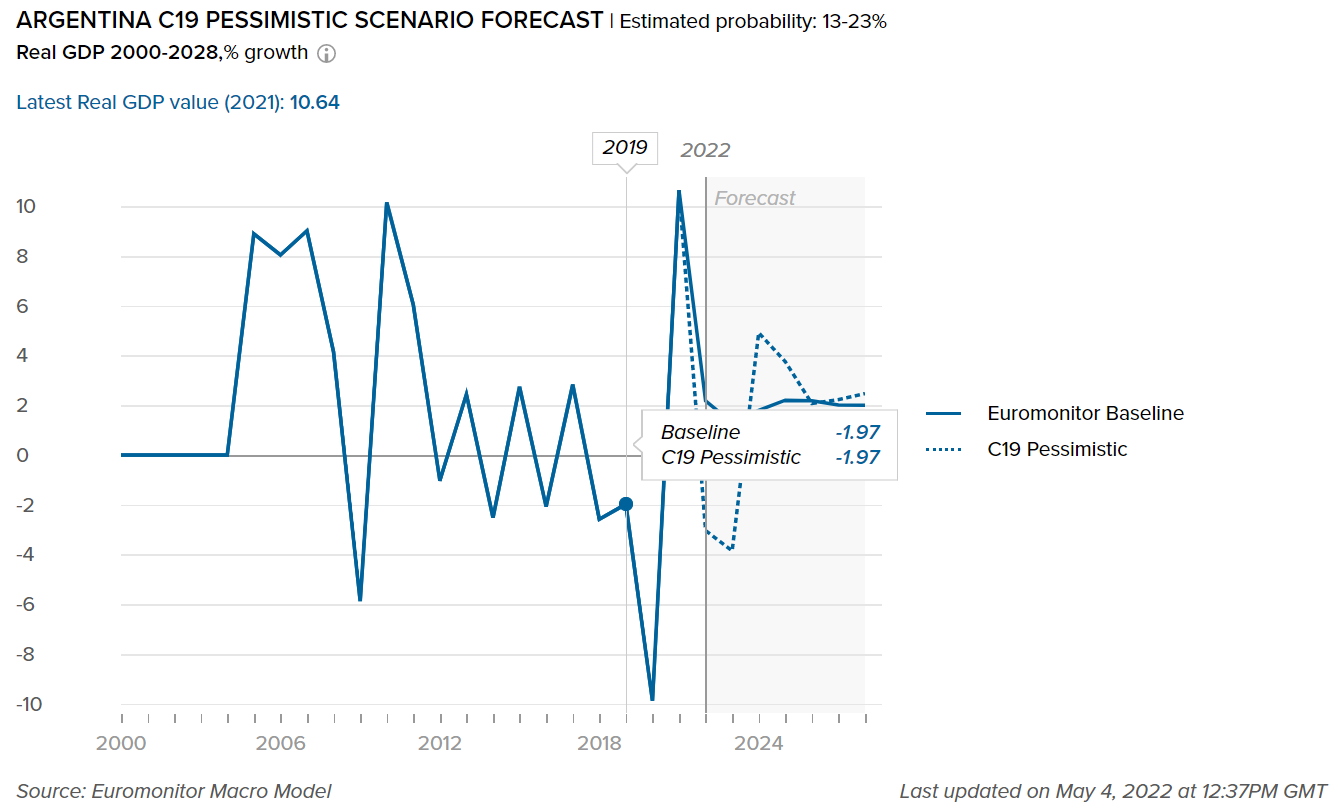

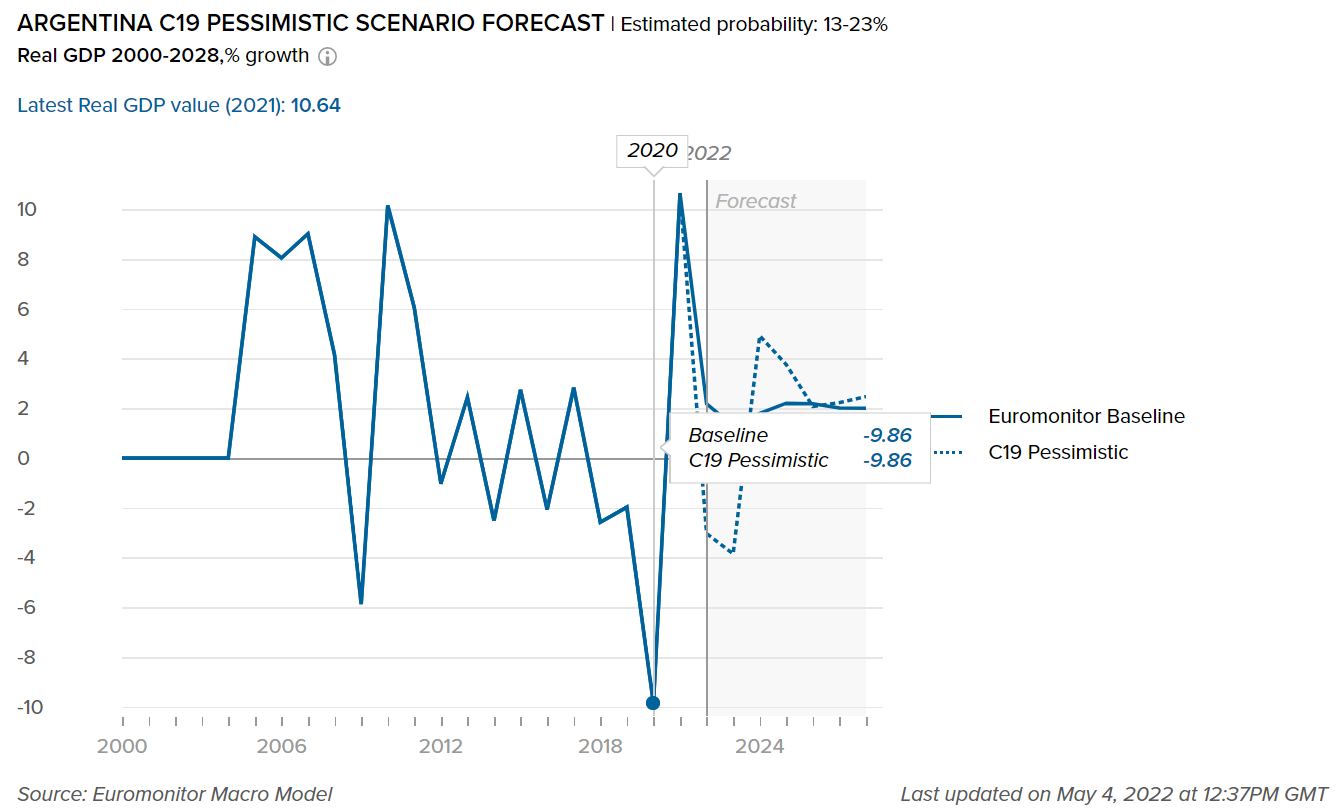

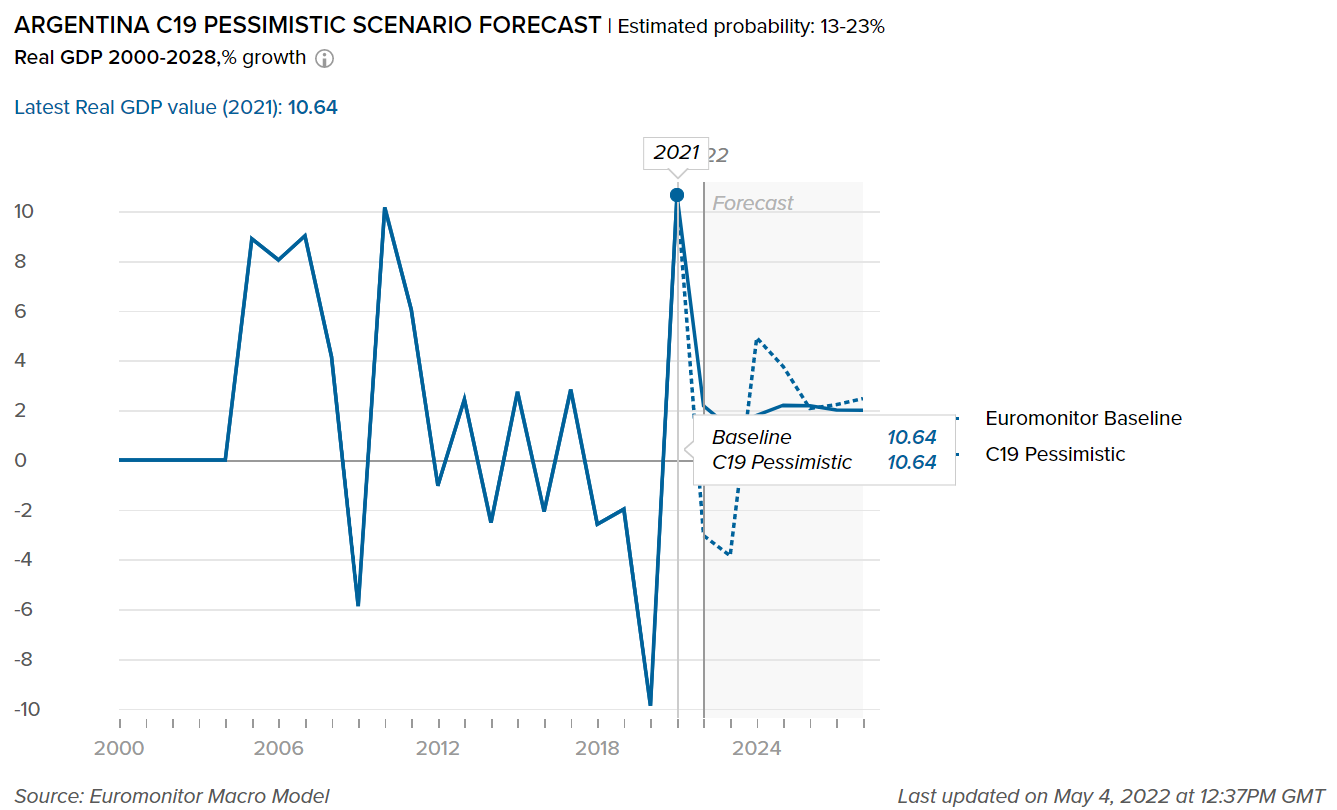

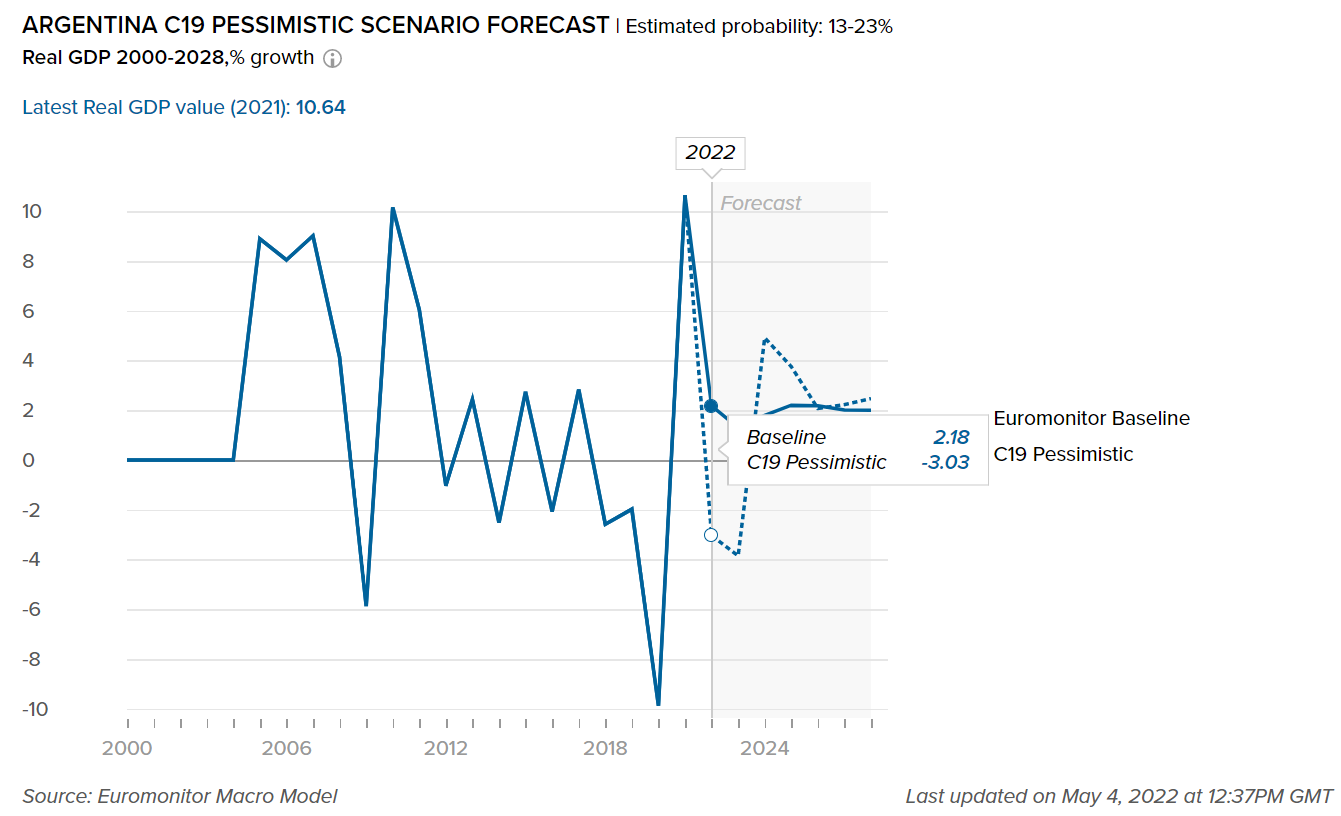

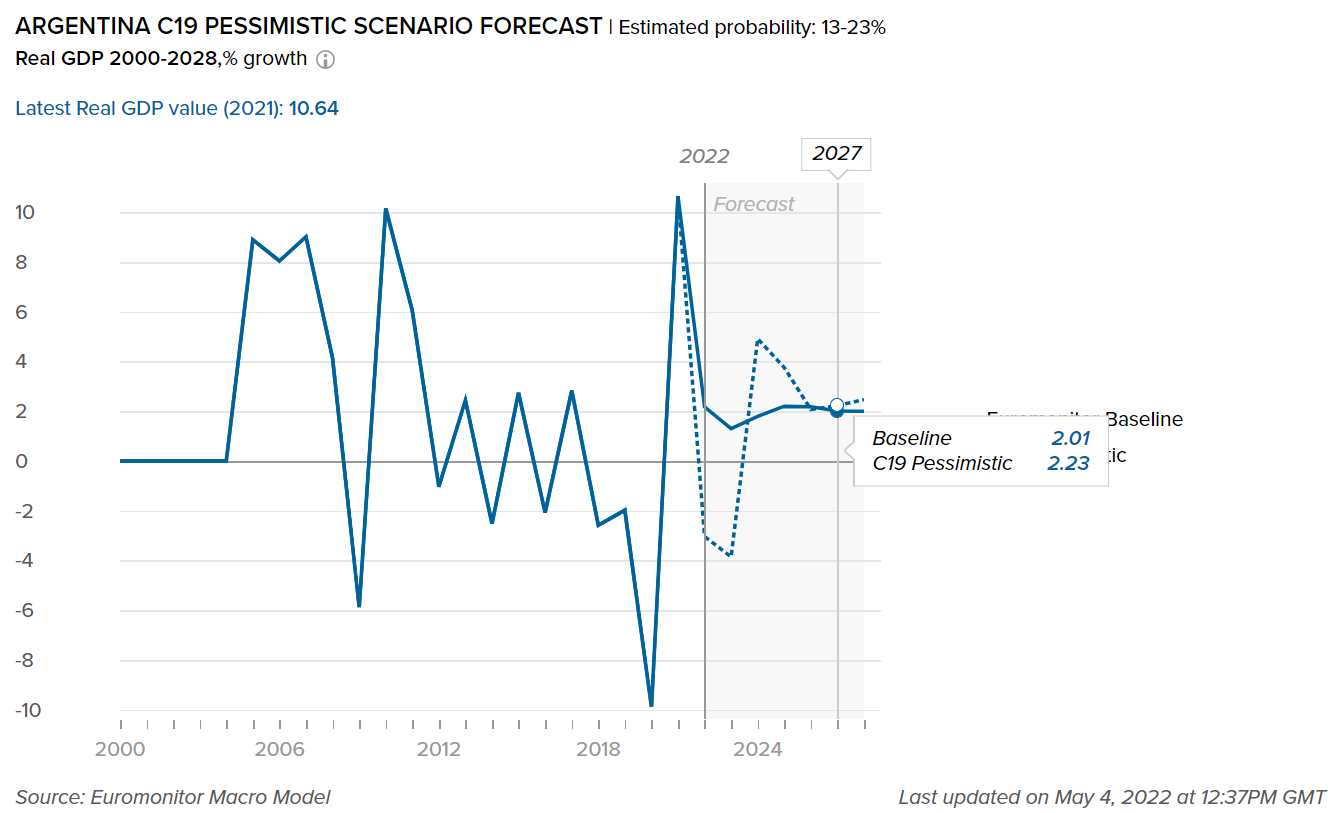

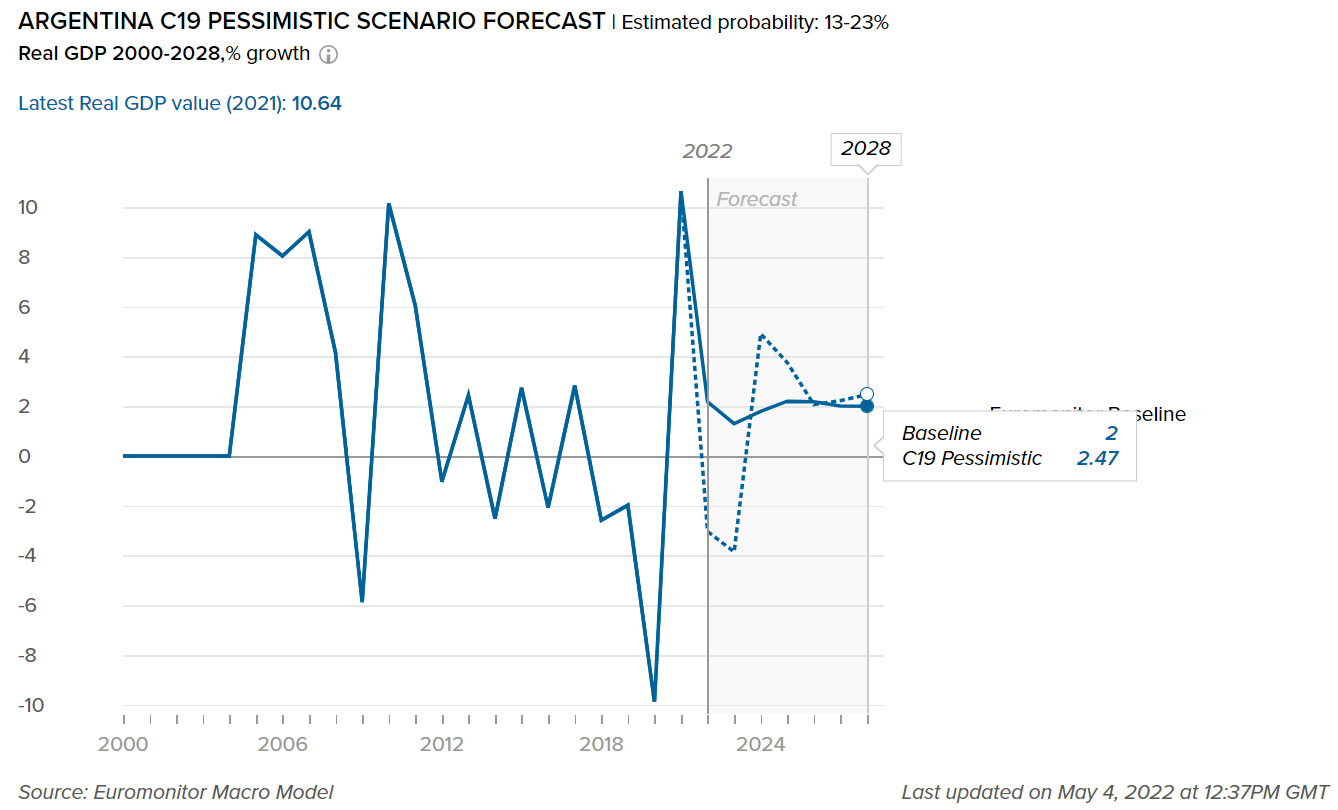

- Impact on GDP

-

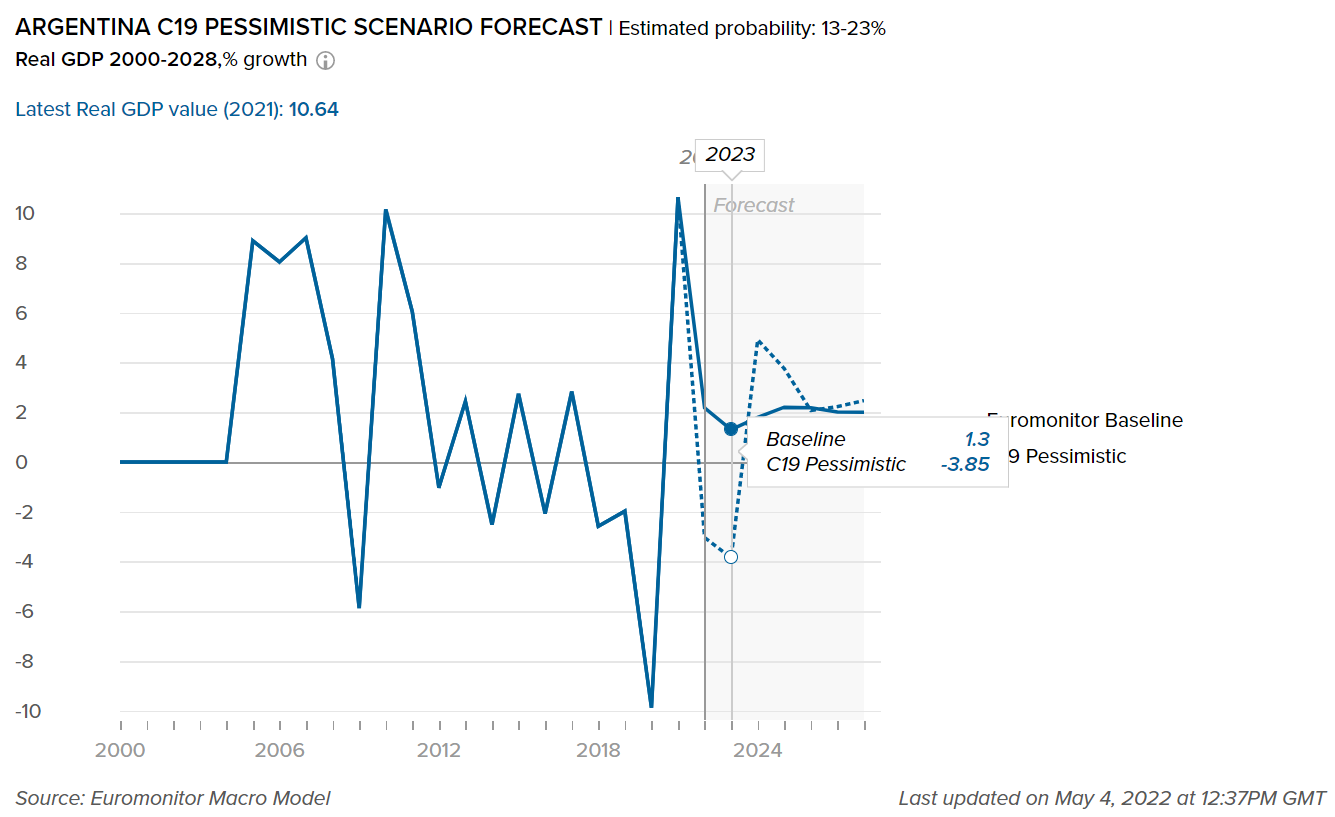

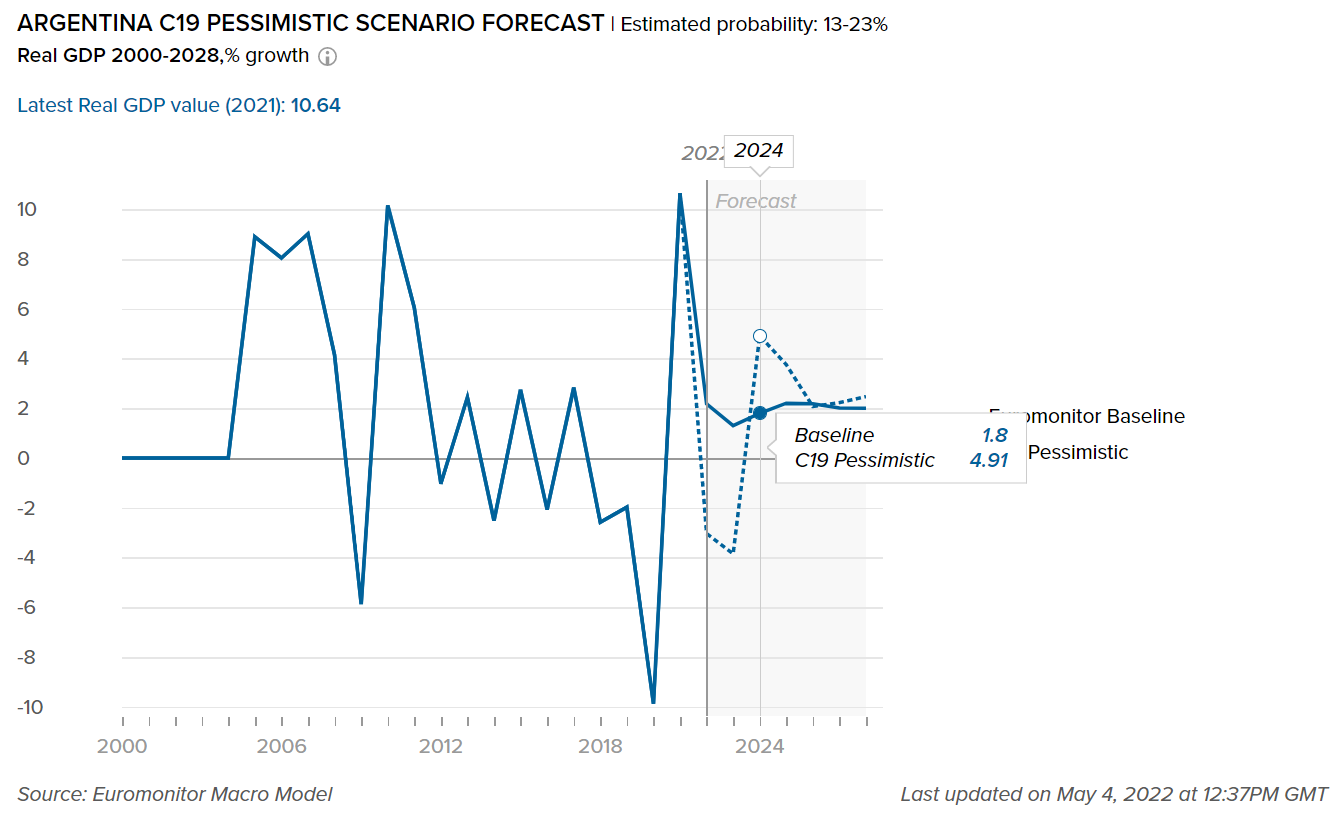

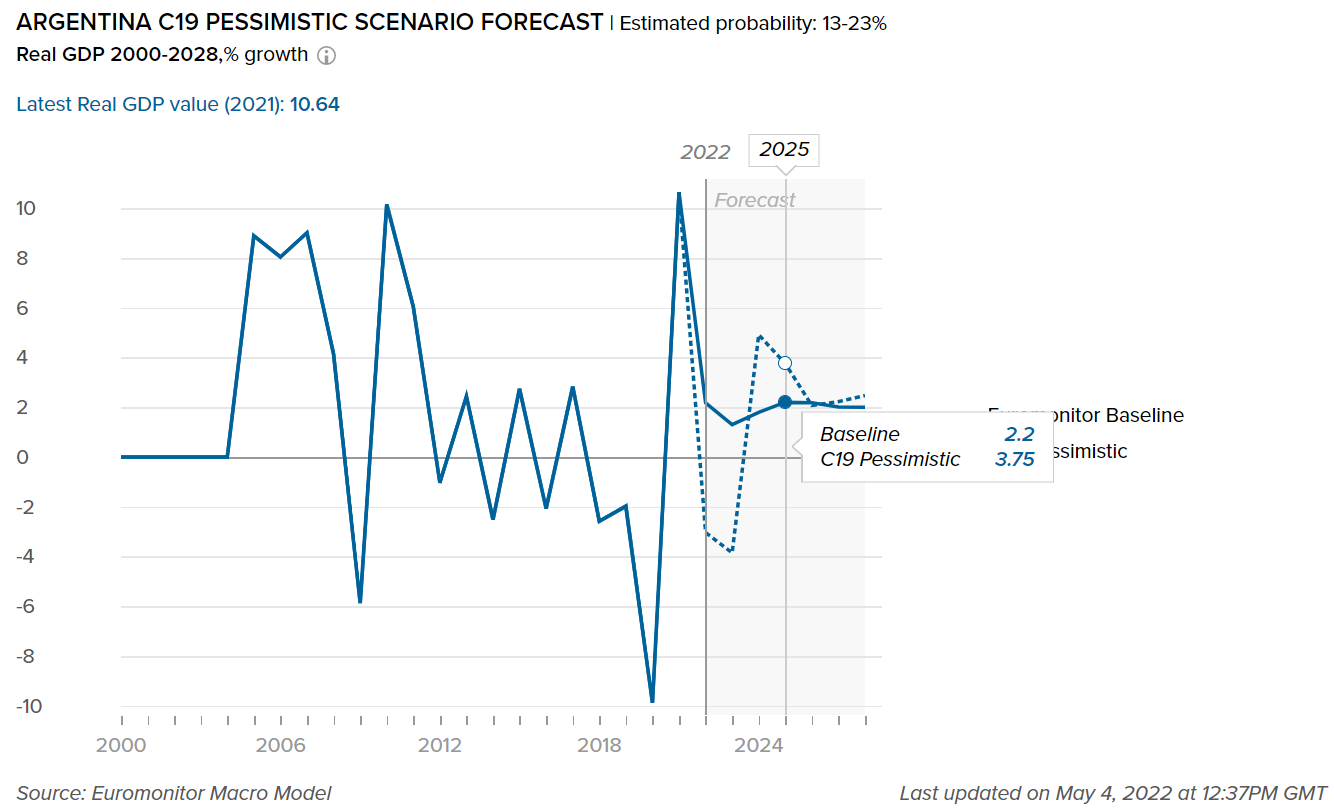

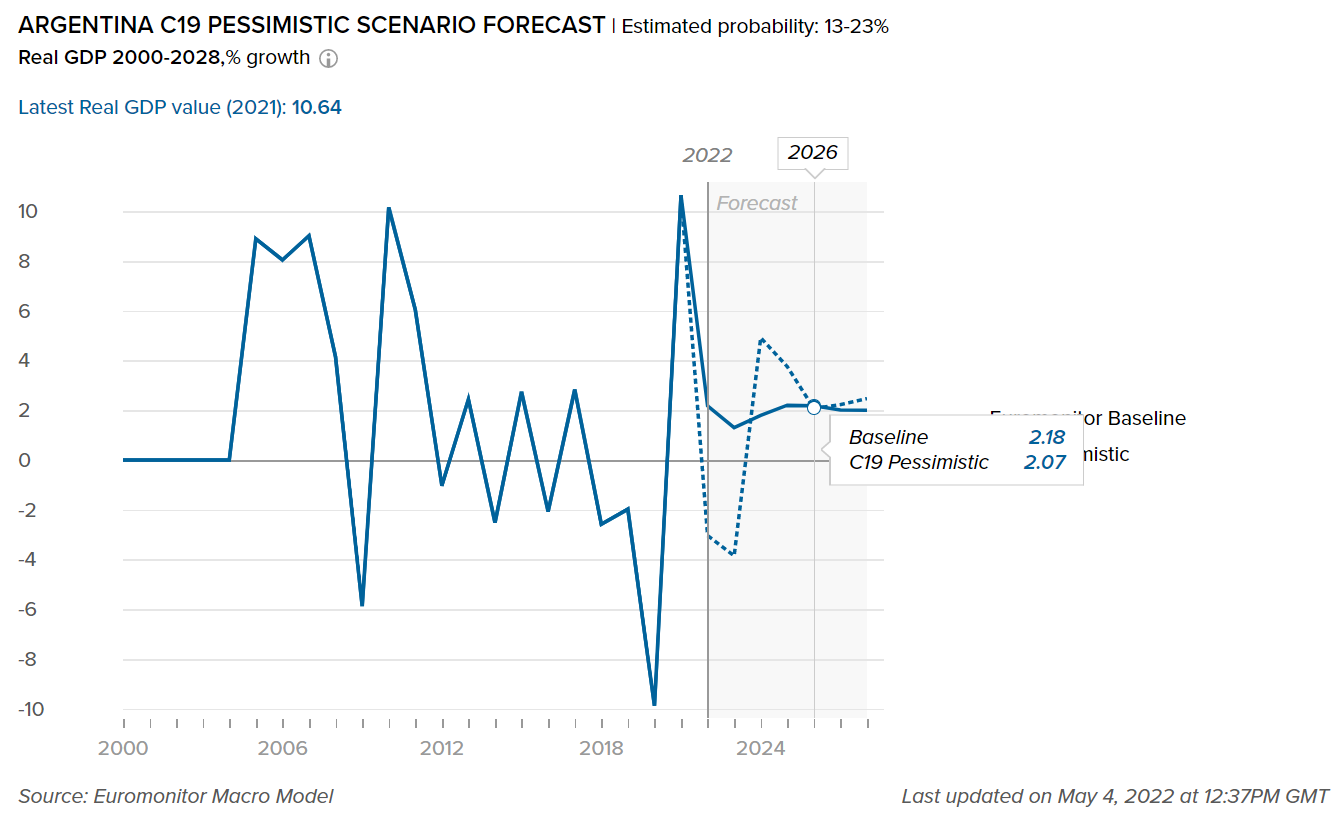

This graph shows our “most probable” and “worst case” scenarios of how COVID-19 will impact real GDP in Argentina. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Argentina’s real GDP exceeded growth expectations in 2021 but faces a slowdown in 2022

- Witnessing a contraction of 9.9% in 2020, real GDP in Argentina increased by 9.0% over 2021, outperforming the regional average of 6.3%. Real GDP in Brazil, for example, increased by 4.7% over 2021. Although Argentina’s economy, which was supported by increased domestic consumption and public investment, expanded in real terms in 2021, inflation remains a threat to the economic performance of the country.

- In 2021, the inflation rate in Argentina increased to 49.1% in comparison to 42.1% the previous year. Transport, health goods, and medical services, among other major groups of consumer goods and services, witnessed the maximum price increases in 2021. It is anticipated that the country will witness hyperinflation in 2022 resulting from surging global energy and food prices caused by Russia’s invasion of Ukraine. Expectations are that inflation could reach 60.1% in the short term. This is likely to cripple business investment and consumption and thus weigh the economy down.

- The country has inflexible labor laws which is one of the major deterrents preventing Argentina from adapting quickly to the changing economic environment. For example, teleworking legislation restricts remote working and discourages businesses from authorizing flexibility in the workplace and cutting labor costs through telework, thereby adding to the country’s unemployment rate in 2021, which stood at 10.7%. Widened social inequalities caused by the pandemic and the uncertainty regarding the course of the pandemic are expected to negatively affect the labor market in the country in 2022.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

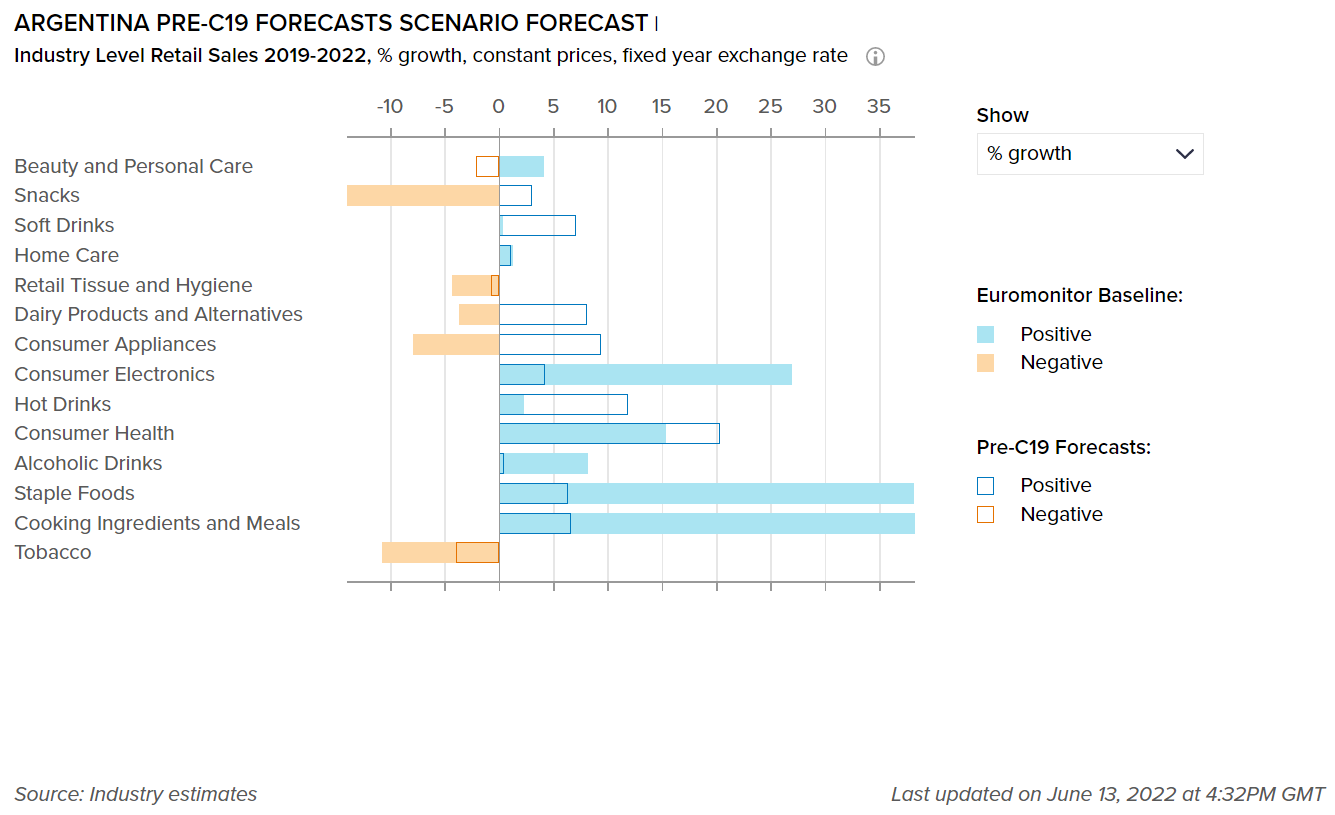

The graph below shows the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

The pandemic encouraged selective buying among Argentinian consumers

- The spread of COVID-19 forced the government of Argentina to impose strict measures such as the closure of non-essential stores, bans on social gatherings, etc. to protect the population from the virus. This severely hampered the economy as unemployment increased, businesses closed, and price sensitivity negatively influenced consumers’ purchasing decisions. This negatively impacted retail sales of several industries over 2019-2021. Products such as tobacco and snacks witnessed weakened demand. Rising health consciousness among consumers is likely to affect demand for snacks and tobacco in 2022 as well. Expectations are that retail sales will drop by more than 10% for both snacks and tobacco over 2019-2022.

- On the other hand, products that improve consumers’ immunity, such as multivitamins and herbal dietary supplements (garlic, ginkgo) witnessed massive demand over 2019-2021 due to the pandemic. This increased focus on preventive healthcare is expected to influence consumers’ buying decisions over 2022 as well. It is expected that retail sales of consumer health products will increase by some 15% over 2019-2022.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

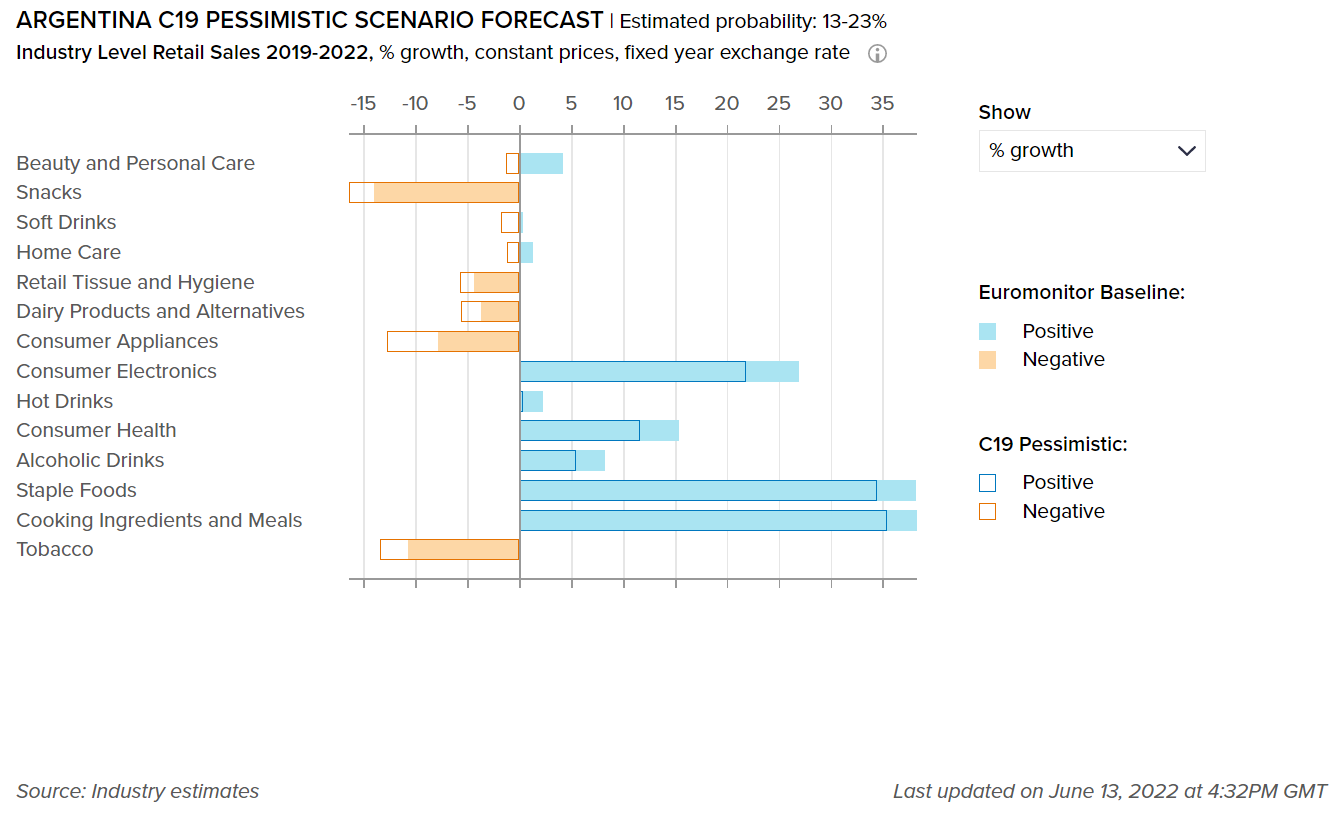

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors covered in Argentina. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Rising at-home demand revitalized alcoholic drinks consumption in Argentina

- The demand for alcoholic beverages soared during 2020 in Argentina. A national survey published by the Buenos Aires University found that the consumption of alcohol increased among consumers aged 35-44 years old. On the other hand, Argentinian consumers aged 18-24 years old reduced their consumption of alcohol due to the lack of social events.

- The liquor industry witnessed a surge in demand among Argentinian consumers over 2021 as well. Home seclusion, social distancing, and the closure of on-trade establishments led to consumers’ need for indulgence, increasing the consumption of wine and super-premium drinks at home. Relaxation of social distancing norms and the opening of on-trade establishments are a few factors that are likely to increase the demand for alcoholic drinks over 2022.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following tables cover the beauty and personal care and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

1,606

1,645

0.5%

Home Care Packaging

1,235

1,233

-0.1%

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

9,951

10,244

-0.09%

Flexible Packaging

15,713

16,516

0.00%

Metal

3,236

3,499

0.52%

Paper-based Containers

1,762

1,820

-0.16%

Glass

3,176

3,181

0.05%

Liquid Cartons

1,855

1,938

0.00%

Flexible packaging enjoys preference for home care, hair, and deodorant products

- In the category of home care packaging, plastic pouches witnessed healthy demand in 2021. Flexible packaging was a preferred packaging type for leading players of home care products for its sustainability profile and massive plastic waste reduction. For example, one 3-liter plastic pouch is equivalent to 12 250ml surface cleaner bottles. This packaging type also provides convenience and is cost-effective.

- Under hair care and deodorant packaging, a squeezable plastic tube was the key packaging type. For example, in hair care packaging, leading players including L’Oréal and Unilever launched squeezable plastic tube formats for high-end conditioners, while in deodorant packaging, brands such as Vichy, Ducray, and La Roche-Posay presented deodorant variants in squeezable plastic tubes.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recovery Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.