Overview

- Packaging Overview

-

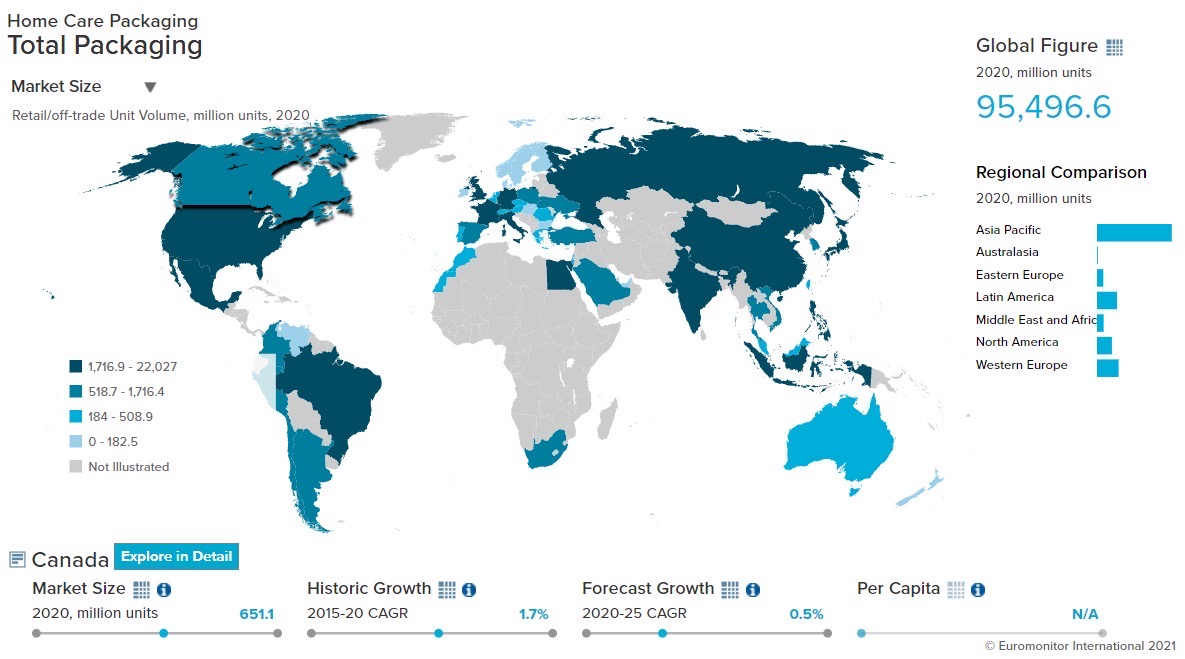

2020 Total Packaging Market Size (million units):

51,153

2015-20 Total Packaging Historic CAGR:

1.5%

2021-25 Total Packaging Forecast CAGR:

-2.1%

Packaging Industry

2020 Market Size (million units)

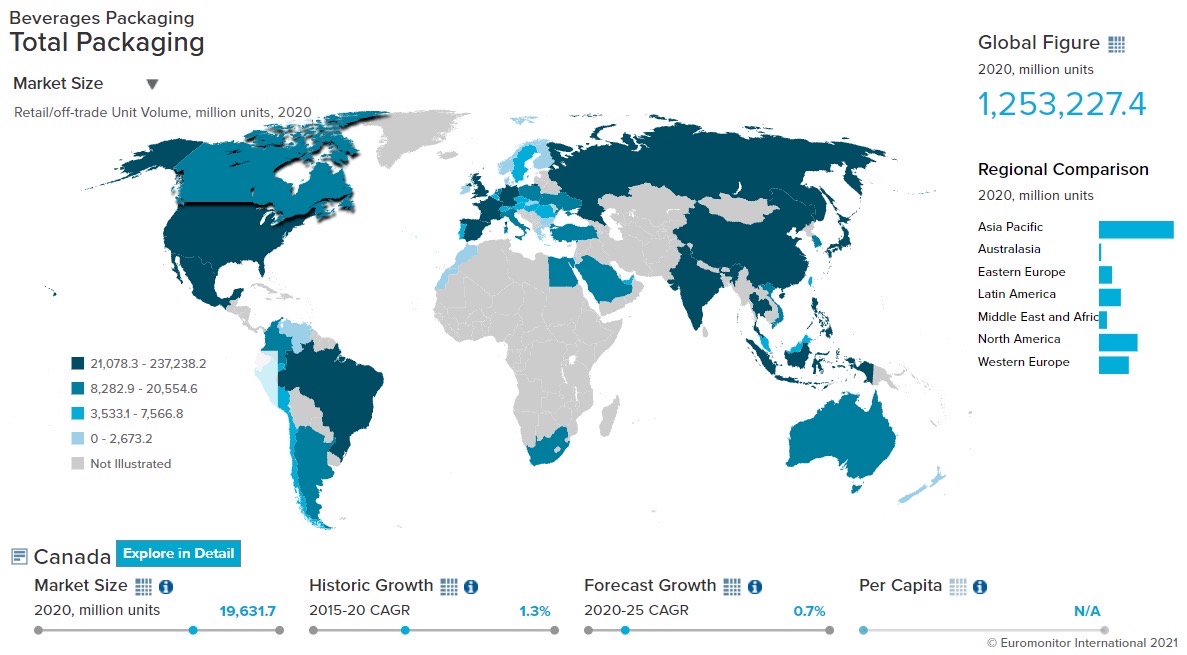

Beverages Packaging

19,343

Food Packaging

28,528

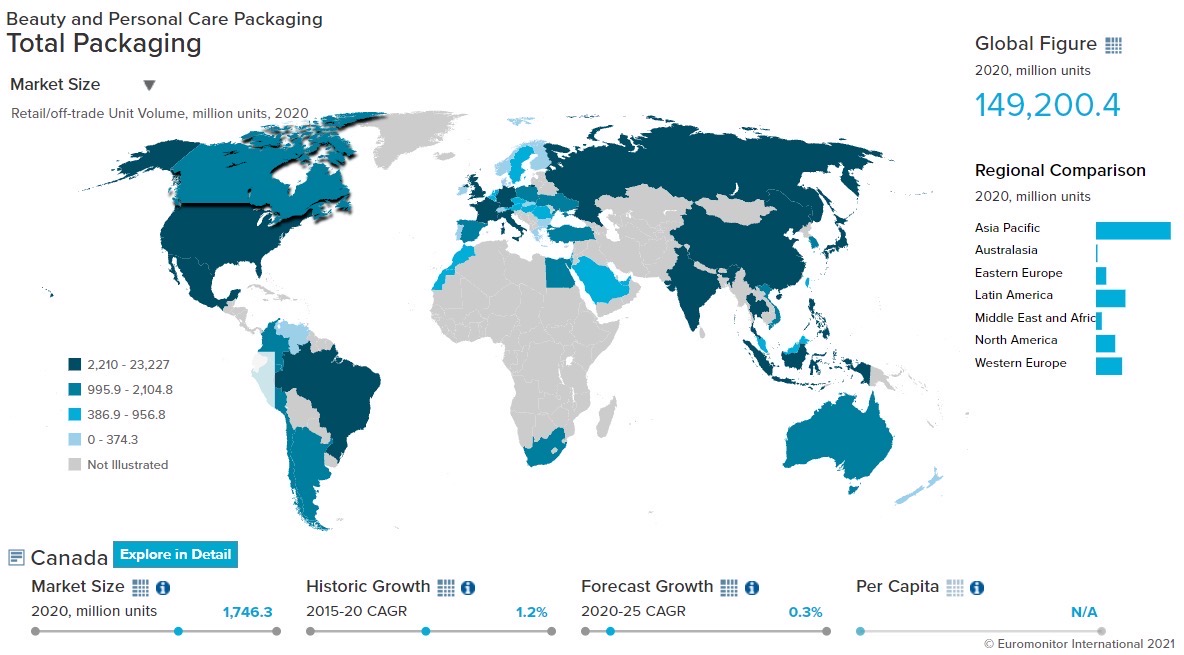

Beauty and Personal Care Packaging

1,746

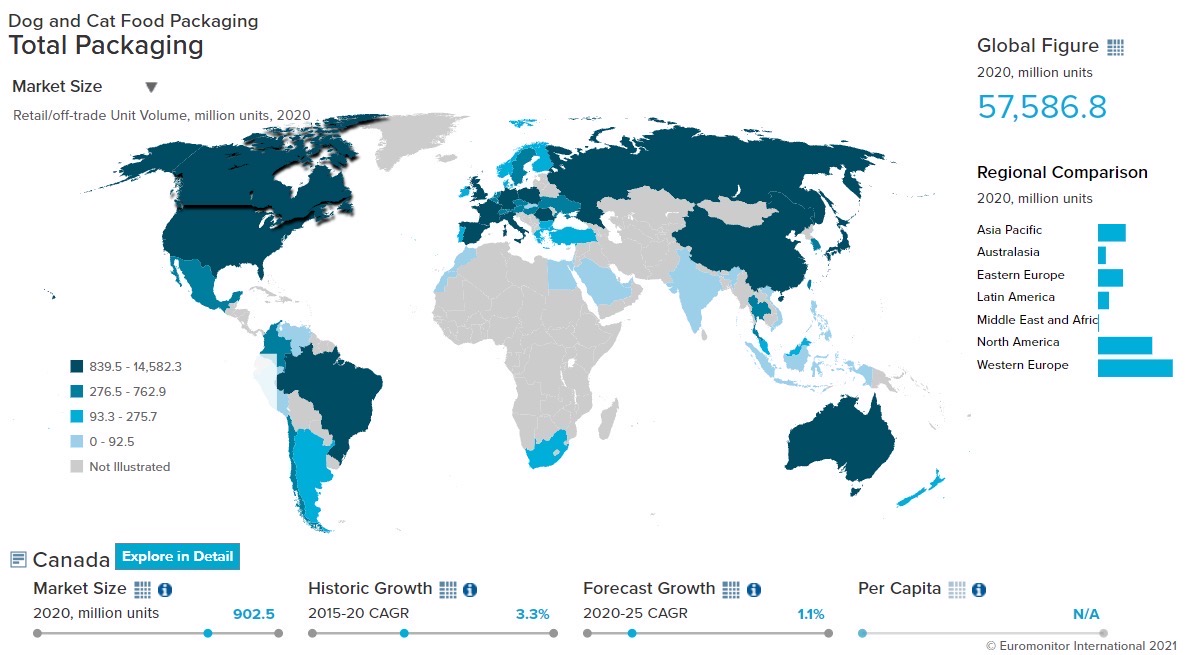

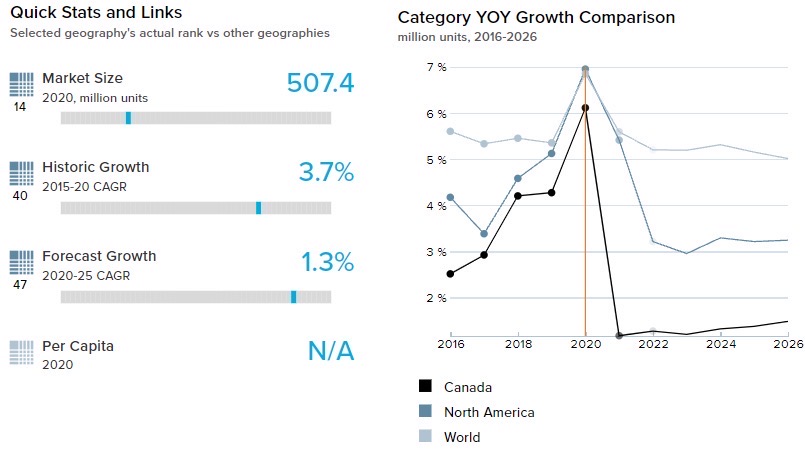

Dog and Cat Food Packaging

884

Home Care Packaging

651

Packaging Type

2020 Market Size (million units)

Rigid Plastic

13,906

Flexible Packaging

15,205

Metal

10,004

Paper-based Containers

5,785

Glass

4,423

Liquid Cartons

1,826

- Key Trends

-

COVID-19 has driven the demand for larger pack sizes as consumers chose to stockpile products to minimize trips to stores/outlets. Bigger pack sizes were also benefitted from e-commerce platforms as they can be easily transported and safely delivered.

As pandemic-related restrictions are set to subside, both trends, the demand for larger pack sizes and the growth of shelf-stable products will reverse. Once consumers revert to pre-COVID-19 lifestyles, demand for a larger pack size will be reduced as consumers will no longer stockpile products. Shelf-stable products will face the same fate as they are perceived as health hazardous because of the high content of preservatives and coloring.

- Packaging Legislation

-

Biodegradable and compostable plastic is gaining momentum, but the waste management authorities have yet to catch up with the growth rate of these pack types. Hence these sustainable pack types end up in landfills. The local municipalities are asked by the government to beef up their capacity to process biodegradable and compostable plastic waste.

- Recycling and the Environment

-

Canada aims to eliminate plastic waste by 2030. To achieve this goal, the government implemented a ban on single-use plastic so as not to shock small businesses with sudden changes. The companies are responding to the legislation by launching new innovative pack types such as recyclable packs, the circular economy, returnable packs, biodegradable packing material, etc.

- Packaging Design and Labelling

-

Canada introduced new changes to the design of nutrition labels and proposed warning labels for food with high content of sugar, salt, saturated fat, and calories. These changes aim at bringing transparency and awareness about the nutritional value of food.

Sustainable packaging persists as a trend and is widely accepted by consumers as well. Companies are positioning sustainable packaging in the premium segment. Companies are innovating with pack designs and packaging materials to cope with the innovative packaging types launched by rivals.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Flexible packaging witnessed a 5.0% volume growth in beverages in 2020. The growth can be attributed to its features such as flexible design, easy maneuverability, and attractive design. To tackle the economic impact of COVID-19, some companies launched small pack sizes such as 100gm packs which further boosted flexible packaging type.

- Flexible packaging showed robust growth of 19.2% and 10.2% by volume in 2020 for the hot drinks and alcoholic drinks industry respectively. COVID-19 induced lockdown and social distancing measures that contributed to the significant decline of on-trade sales within the beverages category in 2020. Being a relatively essential product, prevalent consumer demand drove up the sales of such products through retail off-trade channels during the same period.

- Trends

-

- Glass packaging, which consists of glass bottles and glass jars, declined by 9.1% in 2020 and lost its market share to metal packs and flexible packaging in the beverages industry. This change occurred due to the fragility of glasses as it creates transport and storage challenges whereas flexible packaging offers greater maneuverability and can be easily shipped. As a result, flexible packaging grew by 10.9% by volume in 2020 in the soft drinks segment.

- Metal pack types, specifically metal cans, are easy to carry, can be consumed on-the-go, and is easy to store, making it more acceptable to consumers than glass pack types in alcoholic beverages. As a result, the metal pack type grew at the cost of the glass pack type. Duebto COVID-19 related restrictions, off-trade sales increased but on-trade/foodservice sales declined which benefitted the metal pack type as it is one of the common off-trade packaging formats for the category.

- Outlook

-

- COVID-19 induced restrictions in 2020 boosted the demand for products with a longer shelf life. This trend is likely to persist as consumers continue to reduce the frequency of trips to store-based retailers to reduce the risk of contracting the virus. This trend will boost the market share of flexible packaging formats by a volume CAGR of 14.6% in hot drinks over 2020-25. While flexible packaging is a preferred pack type for the off-trade channel, glass packaging formats are preferred in the on-trade/foodservice channel. The latter is expected to continue losing market share as the on-trade/foodservicendustry is disrupted by lockdowns/closures.

- Home carbonation systems from brands such as SodaStream benefited from increased at-home consumption during 2020. The home carbonation system brands are driving a shift from plastic to metal bottles, thus saving close to another 200 million single-use plastic bottles by 2025.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Growing demand for smaller dog breeds has resulted in more demand for smaller pack sizes. Budget-conscious pet owners also prefer smaller pack sizes over larger ones. As a result, one of the common pack types present within smaller pack sizes, flexible packaging, has grown by 5.8% within dog and cat food in 2020.

- Consumer demand for packs that are easy to open and reseal continued to grow in 2020. These zip/press closures are preferred for small stand-up pouches and freeze-dried products to preserve their freshness and authentic flavor. This has boosted the demand for flexible packaging formats such as flexible plastic in 2020.

- Trends

-

- The manufacturers have grown conscious of the sustainability trend prevalent in the market and are utilizing it to gain popularity as well as greater consumer loyalty. For example, Petcurean launched Tetra packs that are easy to open and are resealable. These cartons are recyclable and are more cost-effective for transport as they occupy 40% less storage space. They are made from 65% renewable materials and are 100% recyclable. Another player, PureForm launched biodegradable canisters and compostable packaging material within its dog and cat food products. This new packaging type aims to replace HDPE packaging material in the future.

- Metal cans continue to be the main pack type in wet dog and cat food but PET jars are set to gain ground in this segment owing to the benefits it offers in comparisons such as easy handling, less storage space, and easy transport. Downsizing of packs, for example, downsizing larger packs to 100gm pouches, will further support this trend.

- Outlook

-

- The growth of smaller pack types using innovative and attractive packaging as a tool to achieve greater product sophistication and a premium perception towards sustainable and eco-friendly packaging will help the packaging industry to achieve value as well as volume growth over 2020-25.

- The growing pet humanization trend has contributed to the growth of premium-priced quality dog and cat products in the country. Moreover, since eco-friendly and sustainable pack types are perceived to be premium, manufacturers have started innovating on new sustainable and convenient packaging formats such as recyclable packs with zip/press closures.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- As consumers prioritize hygiene-related products over beauty products, products such as sanitizers, body wash, shower gel, and liquid soaps recorded historic growth. These products are mostly sold in flexible pouches, flexible paper, and PET bottles. As a result, flexible packaging grew by 4.4% in 2020 in the beauty and personal care industry.

- Small-sized formats enjoy continued growth as consumers want to try out new products and different brands by using their small-pack-sized variants. This led to volume growth of 3.4% for flexible pack types in 2020. Since small pack sizes made of flexible and paper-based material are easy to manufacture, transport, and shelf as compared to their metal and glass counterparts, this further led to a decline amongst the latter packaging formats.

- Trends

-

- Fragrances are still dominated by glass packaging formats, but pack sizes have reduced over the years. Portable and “Go Anywhere” small-sized packs are being introduced by brands along with new innovative pack designs. For example, Dior’s Miss Dior Blooming Bouquet Roller-Pearl is packaged in a 20ml format with a glass bead tip, which allows for easy and precise fragrance application.

- Sustainability initiatives such as package-free products, refillable containers, green delivery channels, and circular shopping schemes such as reusable and refundable packaging are gaining momentum. These sustainable pack types are perceived as sophisticated. Hence, brands, such as Saponetti, a Toronto-based soap delivery company, are positioning these products in the premium category.

- As the zero waste trend gains momentum, new refillable and minimal packaging solutions are emerging. This trend resulted in a decline of 3.8% and 0.6% in glass and metal pack types respectively. On the other hand, flexible packaging grew by 3.4% in the beauty and personal care industry in 2020.

- Outlook

-

- Consumer perception towards sustainable and eco-friendly packs as premium and sophisticated products will make manufacturers pledge for more green initiatives to launch new sustainable pack types. On the other hand, glass pack types pose transport, handling, and storage challenges which makes it unattractive for retailers as well as consumers. Hence, the glass pack type will decline by 0.4% in 2021.

- In bath and shower packaging, PET bottles will continue to lead as they are convenient to use whereas in fragrance packaging glass pack type is expected to dominate the segment as they are perceived as premium and sophisticated. Circular shopping initiatives and refillable packaging formats are expected to gain significant ground, as is the trend towards package-free products.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- Enhanced hygiene awareness because of COVID-19 led to a major spike inhome care products which further boosted the packaging in thehome care industry. Flexible pack types grew by 5.5% in 2020 as e-commerce sales rose exponentially during the pandemic. Flexible plastic and stand-up pouches, are economical, durable, and take up less space, hence it is favored by e-commerce trade channels.

- Despite the rise in sustainability packaging trends, the safety concerns among consumers about the usage of the circular economy scheme (a scheme wherein materials constantly flow around a 'closed loop' system, meaning packaging material once disposed of will again be used to make a new package), reusable bags and containers negatively impacted sustainability initiatives such as returnable packs, reusable bags, and refillable packs as they pose a risk of contracting the virus at touchpoints.

- Trends

-

- Pandemic-linked restrictions in movement outdoors have significantly impacted consumer behavior as consumers now prefer stockpiling home care products as reserves. This trend resulted in the introduction of larger and value-for-money pack sizes in the home care industry.

- Outlook

-

- The Canada Plastics Pact was launched to chart a plan towards a circular economy for plastic by 2025. The pact will help support efforts towards ensuring that 100% of plastic packaging is reusable, recyclable, or compostable, aim for a target of at least 50% of plastic packaging being effectively recycled or composted, and see that at least 30% of recycled content is used across all plastic packaging by weight. This will eliminate single-use plastic. Also, this will require both trade channels (on-trade and off-trade) to accommodate and make arrangements for returnable and refillable products.

- Despite sustainability being deprioritized due to COVID-19 in the immediate future, it is likely to re-emerge as an important packaging trend within the country. This is mainly because more and more Canadians are getting environmentally conscious and are demanding products that can help make a positive impact on the environment. As a result, while some players are planning to offer reusable and returnable packaging formats within the home care segment, some others are planning to launch innovative product dispensing channels such as vending machines for refillable home care products.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- The pandemic-induced closure of foodservice/restaurants benefited the packaged food industry as consumers chose convenient meal options such as ready-to-cook meals including frozen meals and frozen pizzas. Frozen meals are mostly packed in flexible packaging material, which boosted the packaging format by 7.1% in 2020 in terms of volume.

- Despite the growth in the ready meals segment, on-the-go meal consumption declined. Before the pandemic, on-the-go meals such as chilled lunch kits and prepared salads were preferred by consumers in offices and schools. Owing to pandemic-related movement restrictions on-the-go meal sales declined. Instead, consumers chose ready-to-cook options rather than buying prepared meals. As ready-to-cook food is mostly packed in flexible packaging material, it further boosted flexible packaging.

- Trends

-

- Dinner mixes exploded in 2020 owing to pandemic-related restrictions. Since folding cartons is the only pack type within this category, it witnessed 7.9% growth in 2020. Within the diner mixes category, 200gm folding cartons were the most popular pack size as this pack size is sufficient for a small family of 3.

- As Canada aims to eliminate plastic waste by 2030, companies such as FreshPrep are using new trays that are reusable and recyclable. As FreshPrep’s innovative packaging received consumer acceptance, other companies are expected to follow suit and adopt new sustainable packaging solutions.

- Outlook

-

- Once the pandemic subsides, consumers will revert to their pre-COVID-19 lifestyle. This is expected to boost on-the-go consumption of prepared meals which will further benefit flexible packaging formats. As flexible packaging is widely accepted by consumers, companies are innovating within this packaging type. For example, Vegpro, which previously used virgin plastic, now uses 100% recycled plastic for packaging. This is expected to inspire other players to follow suit over 2020-25.

- The shelf-stable ready meals category grew exponentially in 2020. This category is expected to revert to its declining trend once the pandemic-related restrictions are lifted. Consumers are losing interest in shelf-stable ready meals as they are usually perceived as high on preservatives and coloring. This will drastically hinder the growth of metal food cans in the forecasted period of 2020-2025.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Canada

-

Travelers to Canada are still expected to wear a mask

- According to the World Health Organization (WHO), on May 2022, Canada’s total confirmed cases stood at 3,850,782, the total number of deaths reached 40,706, and the number of new cases on the day reached 2,919.

- The Canadian government announced several changes to current border policies, the most significant to date. Fully vaccinated travelers do not need to do a pre-entry test after April 1, 2022. They may still be subjected to random testing upon arrival, but they are not required to quarantine.

- That being said, even though most pandemic restrictions, including mask mandates, have been withdrawn by provinces and territories, the federal government still compels incoming tourists to wear a mask for two weeks.

- According to the WHO, on May 22, 2022, Canada’s total cases per million inhabitants reached 101,323, while the total vaccination per 100 people reached 82.7 totaling 82,754,363 on May 20, 2022.

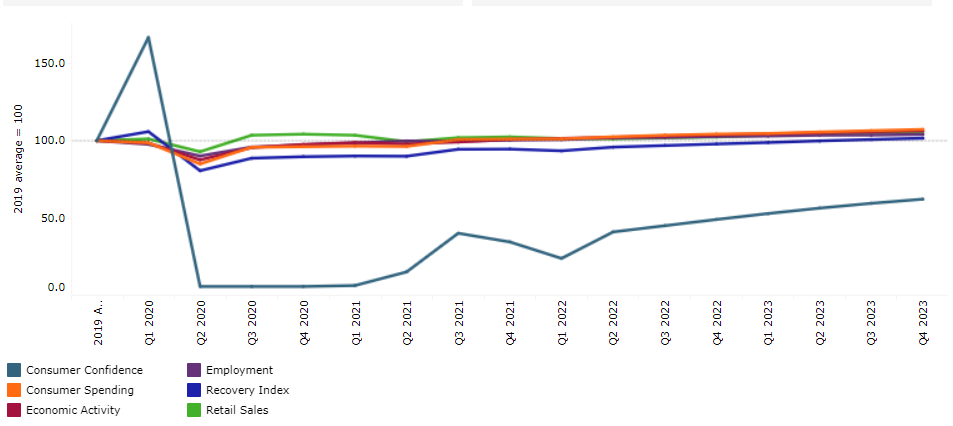

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Canada

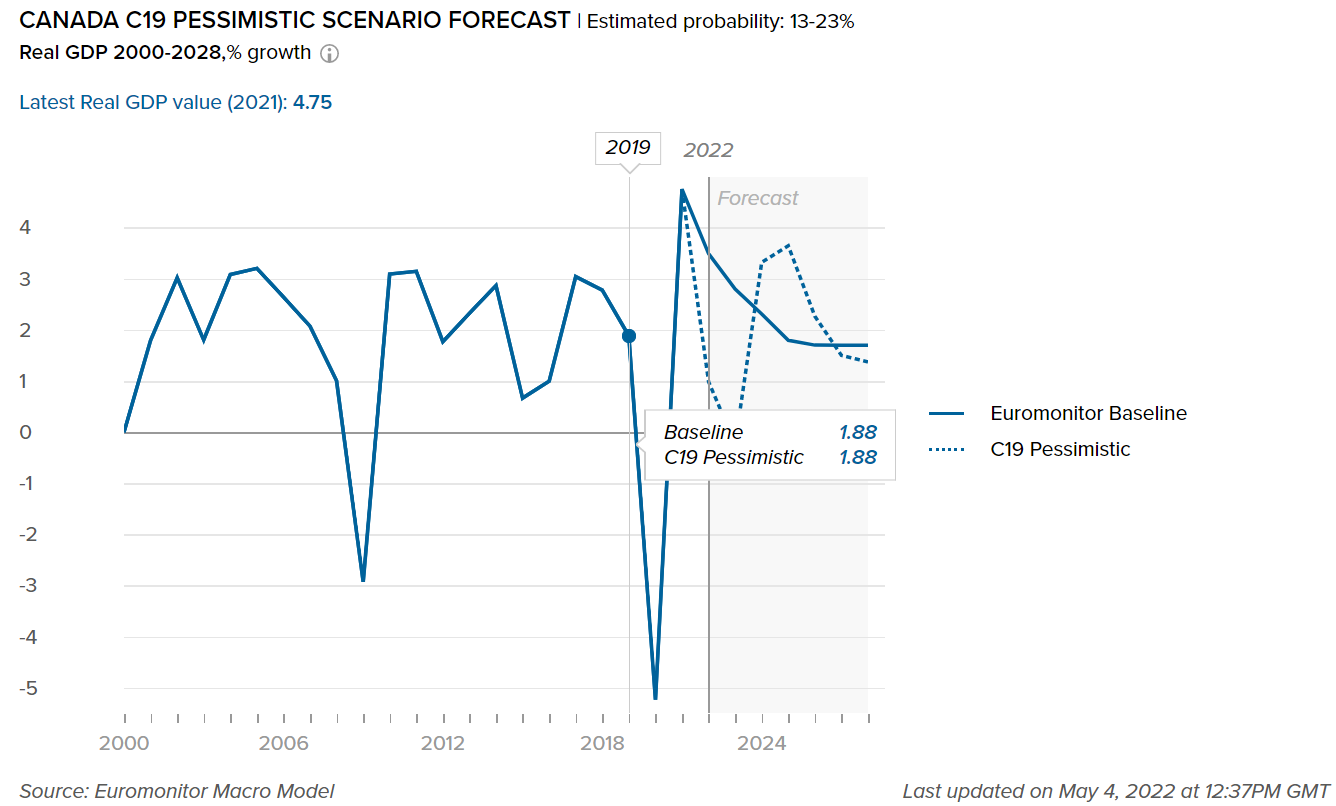

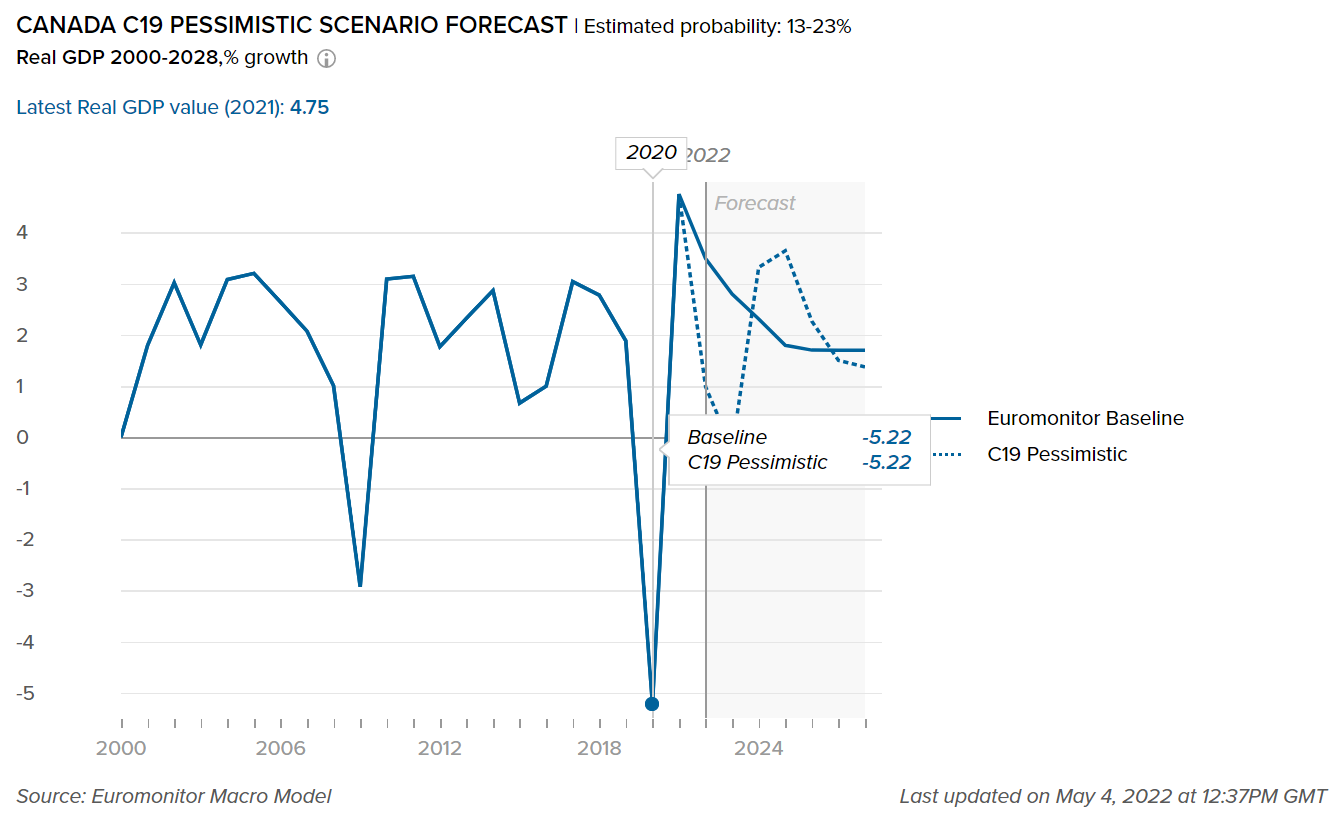

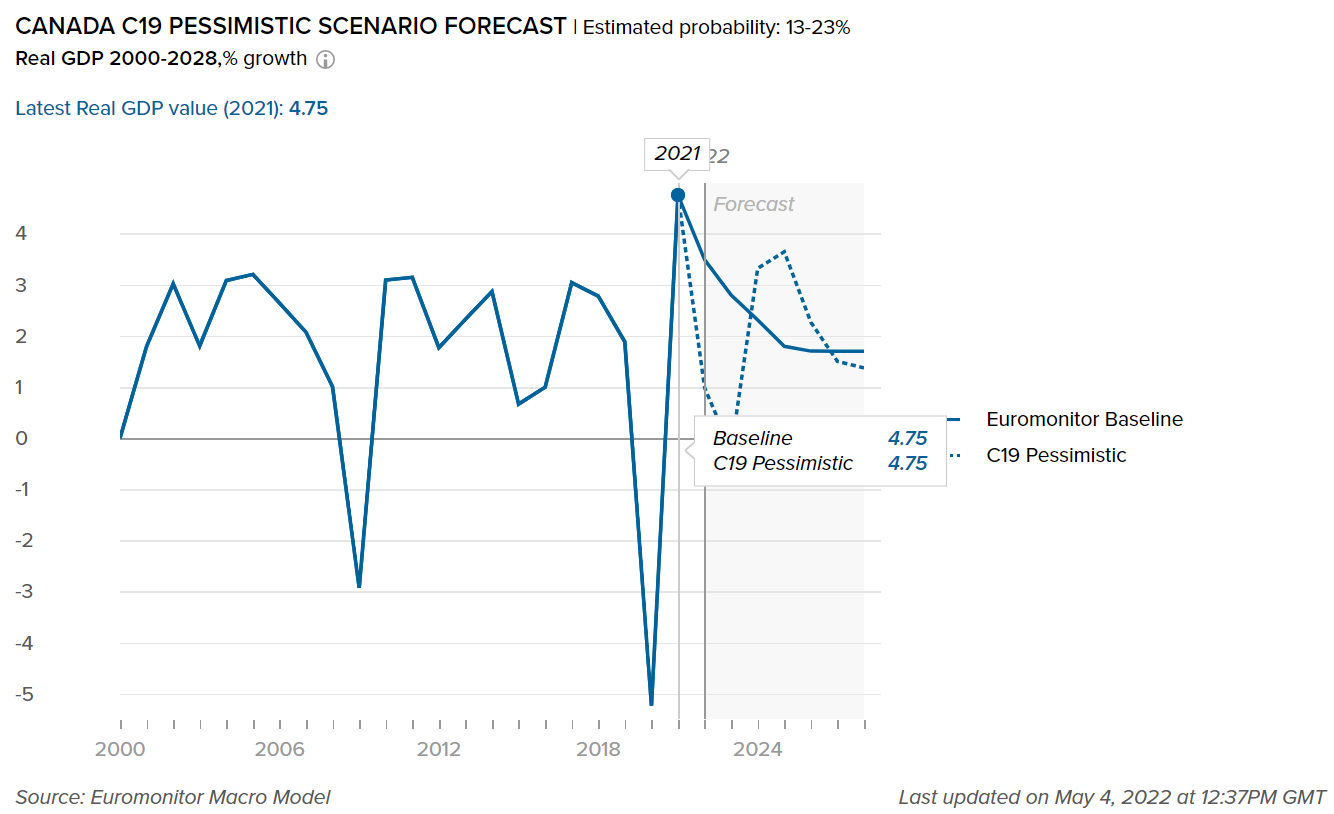

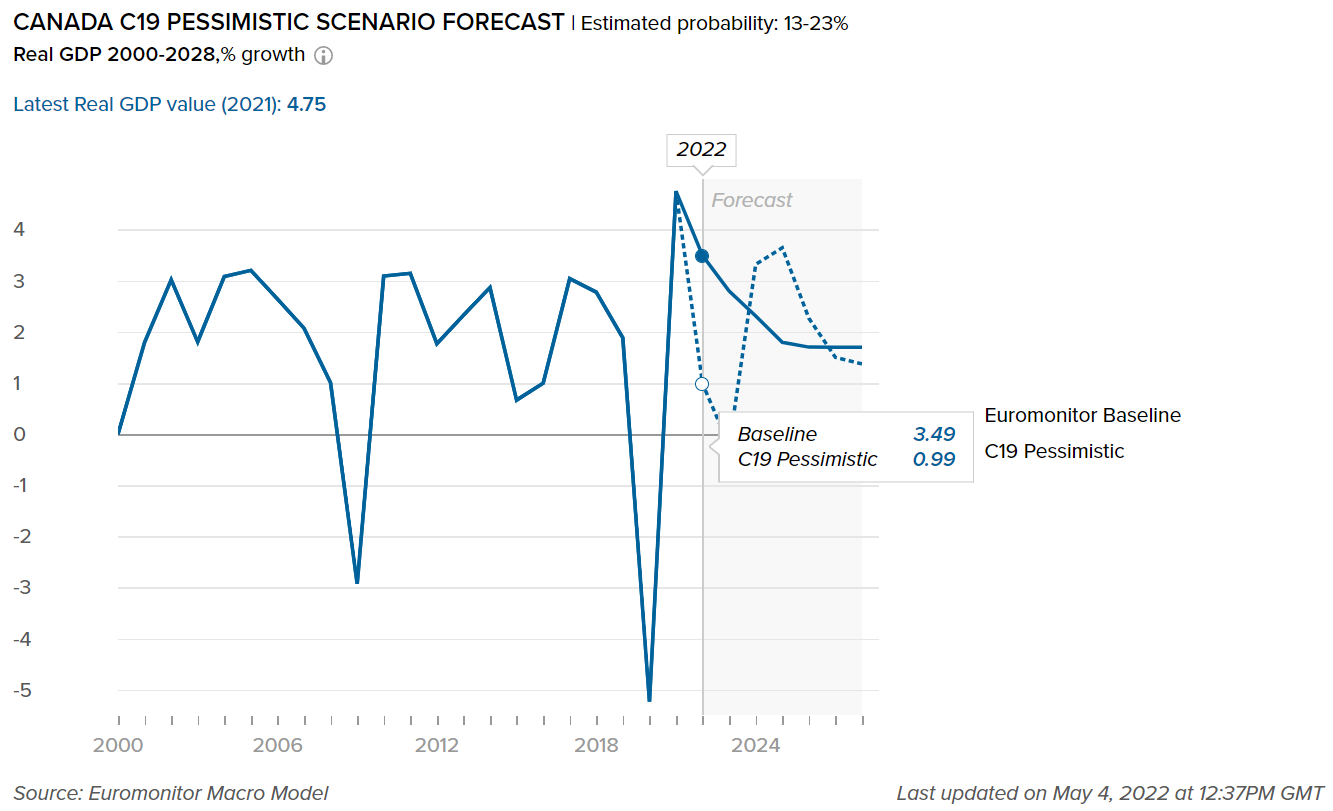

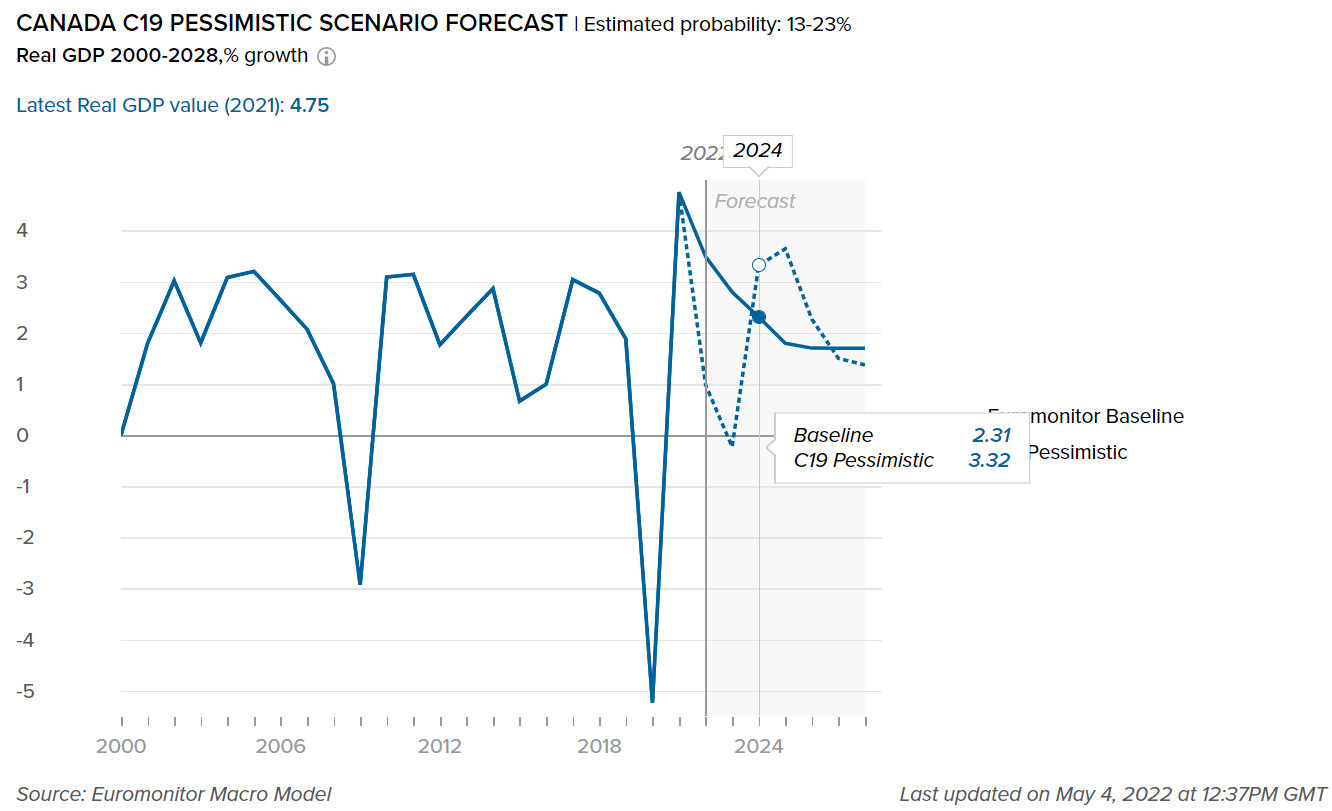

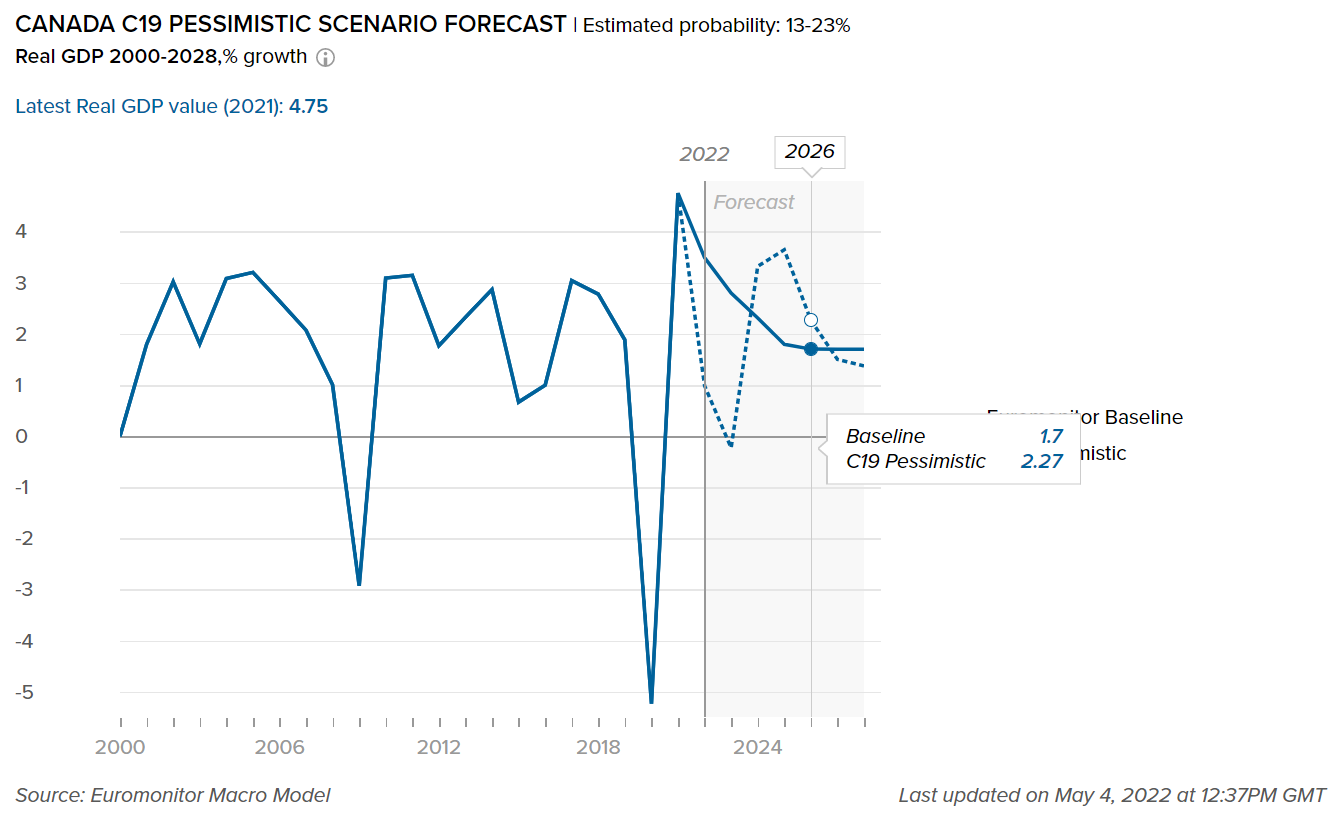

- Impact on GDP

-

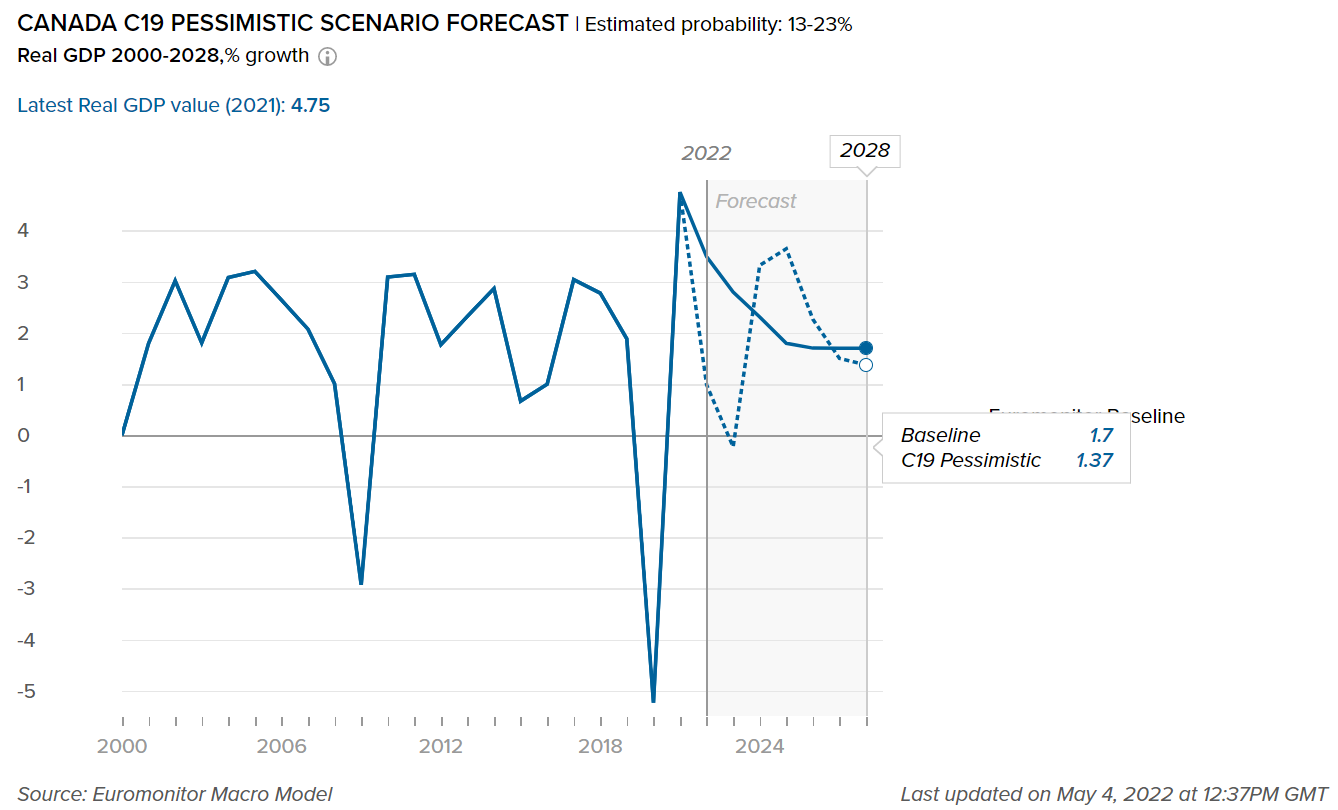

This graph shows our “most probable” and “worst case” scenarios of how COVID-19 will impact real GDP in Canada. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast, which has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast, which has an estimated probability of 13-23%.

Canada’s economy returning to normalcy

- Following the detrimental impact of COVID-19 on the Canadian economy, annual real GDP growth in 2021 was 4.7%, compared to 5.1% for the developed world. Higher oil prices are expected to enhance Canada's vital energy exports. In the short term, consumers are projected to sustain economic momentum by resuming consumer spending and returning to more normal activity levels, due to a successful immunization program. In 2022, annual real GDP growth is expected to be 3.4%, compared to 2.9% for developed countries.

- In 2022, Canada's ranking in the Index of Economic Freedom places it in the “mostly free” group. However, the country's position dropped, pushing it more into the middle of this group. The government's spending and fiscal health pillars are the key reasons for the lower ranking, with the former being Canada's worst-performing pillar for the rating in 2022.

- Canada's budget went from a surplus to a large deficit of 10.7% of GDP in 2020 as a result of its robust fiscal response to the COVID-19 epidemic. The budget deficit shrank to 4.4% in 2021, although it remained substantial. In 2020, the public debt-to-GDP ratio reached an all-time high. While it was reduced to 111% of GDP in 2021, it is still above 100% and unsustainable. Low-interest rates, on the other hand, should help keep debt-servicing costs manageable in the medium run. As the pandemic fades and the economy recovers, the government is anticipated to implement fiscal consolidation to maintain long-term debt sustainability.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

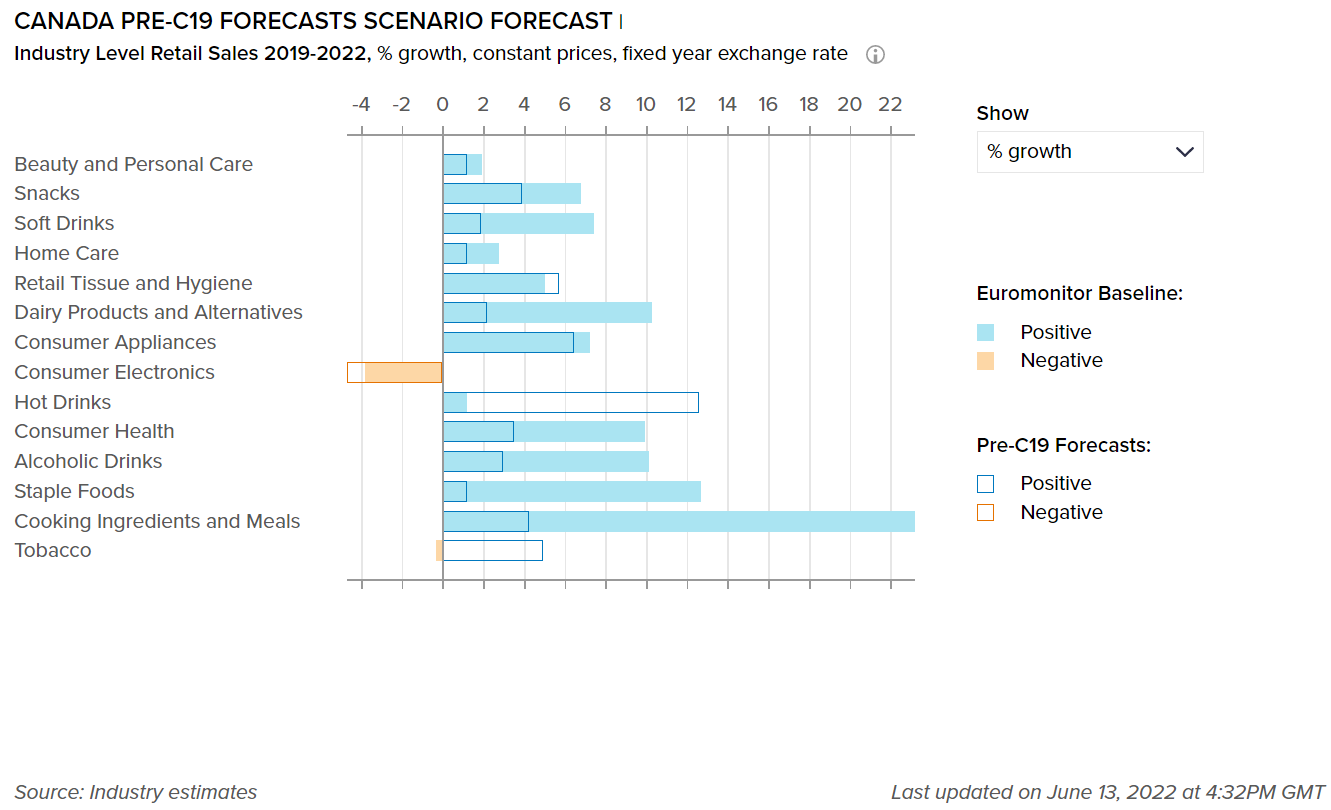

The graph below shows the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast, which has an estimated probability of 45-60%.

A return to normalcy hampers the growth of hot drinks in Canada

- At-home coffee consumption surged considerably in response to the COVID-19 epidemic in 2020, following the many COVID-19-related limitations, with many coffee shops across Canada forced to close or reduce their capacity. As a result, coffee consumption shifted from the on-trade to the off-trade. However, with the gradual relaxation of limitations and the reopening of foodservice establishments, at-home consumption dropped once again in 2021, and on-trade coffee volume sales rebounded after being devastated by the pandemic. Many Canadians began heading out for coffee during lunchtime after more than a year of being restricted to their houses, even if they continued to work from home. Hot drinks sales recorded 1.2% growth according to Euromonitor’s Baseline scenario forecast, as opposed to the 12.5% growth anticipated in the pre-C19 scenario forecast.

- One of the most important factors shaping consumer needs (and thus new product development) in 2022 and beyond will be sustainability. Products such as Loop, a brand that focuses on sustainability, recycling, and reusing all packaging materials, are now available in Canada. The company also caters to the growing health and wellness trend by including 40% fresh-pressed juice from various fruits and vegetables in its recently launched probiotic soda. Such products illustrate the expanding consumer base of younger Canadians who are looking for products that are both healthier and more sustainable. More corporations are expected to follow suit over the forecast period, including larger players such as Coca-Cola, which alongside 30 other companies, joined the Canadian Plastics Pact in 2021.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

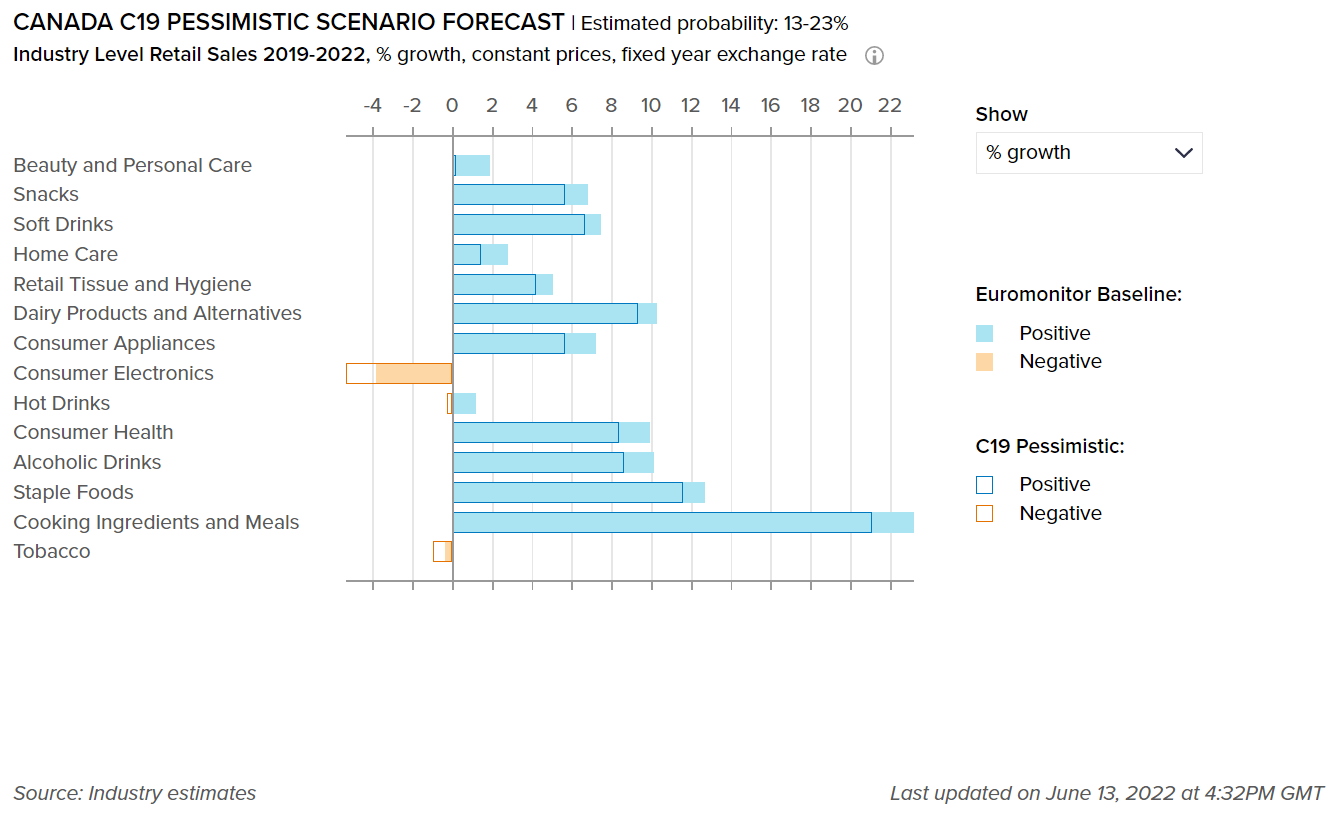

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors covered in Canada. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast, which has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast, which has an estimated probability of 13-23%.

Demand for home products and organic packaged food will increase further in the post-pandemic era

- Many packaged food producers and brands postponed new product introductions and marketing campaigns due to the impact of the COVID-19 outbreak and the associated uncertainty. For those players that launched new products during the pandemic, “organic” was one of the key claims that resonated with Canadian consumers across many categories for packaged food. In recent years, "organic" has been one of the most popular claims for new breakfast cereals for example. Aside from organic breakfast cereals, there were a slew of other organic launches, including Chickapea's organic chickpea elbows and lasagna pasta, Kraft Heinz's new organic versions, Once Upon A Farm's organic baby food, and Nuts for Cheese's organic dairy alternatives, with these all launched over 2020-2021.

- As the concern over COVID-19 fades, growth in home care stabilized starting in 2021. With the implementation of Canada's COVID-19 immunization program, the country is expected to return to normalcy by the end of 2021. COVID-19, on the other hand, is expected to have a longer-term impact on how customers view proper hygiene practices. Concerned about the spread of COVID-19, consumers are cleaning more surfaces and focusing on products that claim to be germicidal and virucidal, and this trend is expected to continue throughout the forecast period, helping home care sales overall. Manufacturers are also likely to take advantage of the situation, focusing on teaching consumers about the importance of good hygiene in all areas of the home.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table coversbeauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data (mn units)

2022 market size as per Jun 2022 data (mn units)

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

1,750

1,767

1.3%

Home Care Packaging

645

633

-7.9%

Packaging Type

2021 market size as per Jun 2022 data (mn units)

2022 market size as per Jun 2022 data (mn units)

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

13,694

13,889

-0.12%

Flexible Packaging

14,953

14,955

-0.27%

Metal

10,152

10,024

-0.13%

Paper-based Containers

5,658

5,694

0.55%

Glass

4,431

4,286

0.15%

Liquid Cartons

1,813

1,799

0.00%

The Canada Plastics Pact is slated to result in a circular economy for plastics by 2025

- On January 27, 2021, the Canada Plastics Pact was launched to reduce and eventually eliminate plastic waste and pollution. More than 40 partners joined forces to rethink how they design, consume, and reuse plastics, to achieve a circular economy for plastics by 2025. The Canadian Beverage Association, the Circular Innovation Council, and the Circular Plastics Taskforce are among the Pact's partners, along with several firms in the FMCG industry. Firms will work together to identify "problematic" or "unnecessary" plastic packaging and explore strategies to eliminate it. They will also support efforts to ensure that all plastic packaging is reusable, recyclable, or compostable, with a goal of at least 50% of plastic packaging being effectively recycled or composted and see that at least 30% recycled content is used across all plastic packaging by weight.

- Players began to offer reusable and returnable package formats within the home care sectors in response to the increased environmental awareness of packaging waste in Canada. For example, on February 1, 2021, the worldwide reusable packaging platform Loop, in collaboration with Loblaw Companies Ltd, launched in Canada to provide numerous refillable grocery and home care products. Over the review period, SC Johnson began to introduce its new line of concentrated home care products in North America. This included lines such as Scrubbing Bubbles, Windex, and Fantastik, as well as refills for these products, with the latter aimed at cutting plastic waste. Other lines that are also available in the concentrated refill bottles include Pledge and Shout.

- Reckitt Benckiser already teamed with Dow's Packaging and Specialty Plastics unit to create improved recyclable packaging for its perfume-free Finish dishwashing brand, echoing consumer demands for more environmentally friendly products and packaging. The resealable stand-up pouch is made of a polyethylene film created by Dow's Packaging and Specialty Plastics unit and is designed for recyclability and end-of-life disposal in existing recycling processes.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recovery Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.