Overview

- Packaging Overview

-

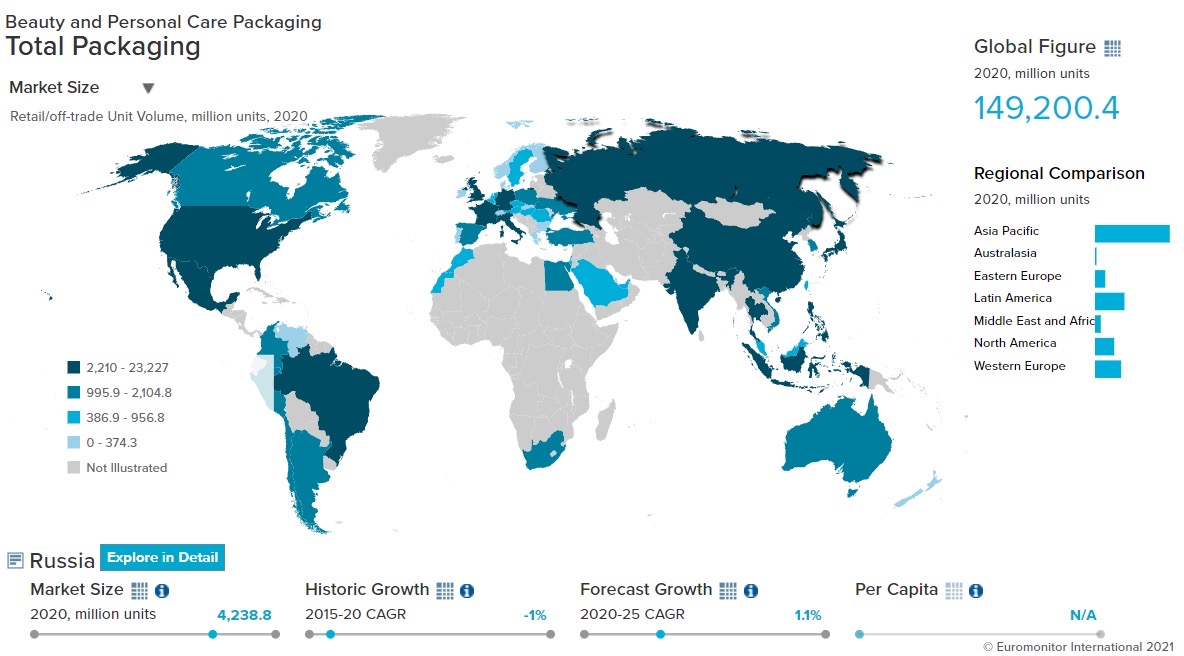

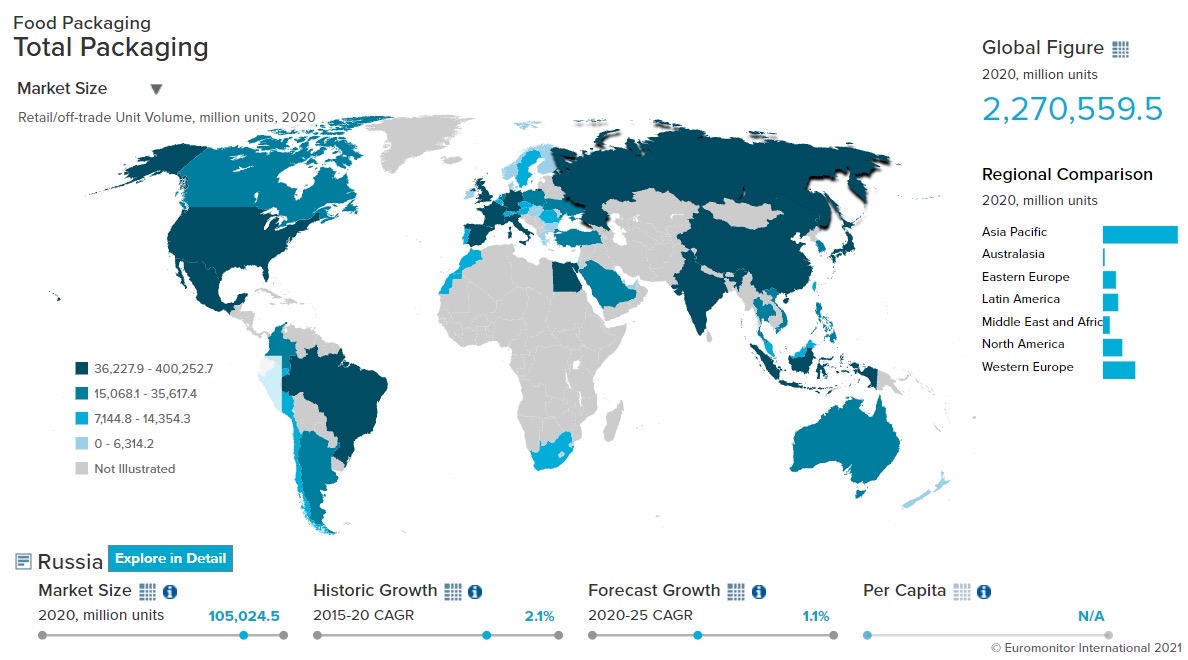

2020 Total Packaging Market Size (million units):

151,990

2015-20 Total Packaging Historic CAGR:

1.4%

2021-25 Total Packaging Forecast CAGR:

-0.4%

Packaging Industry

2020 Market Size (million units)

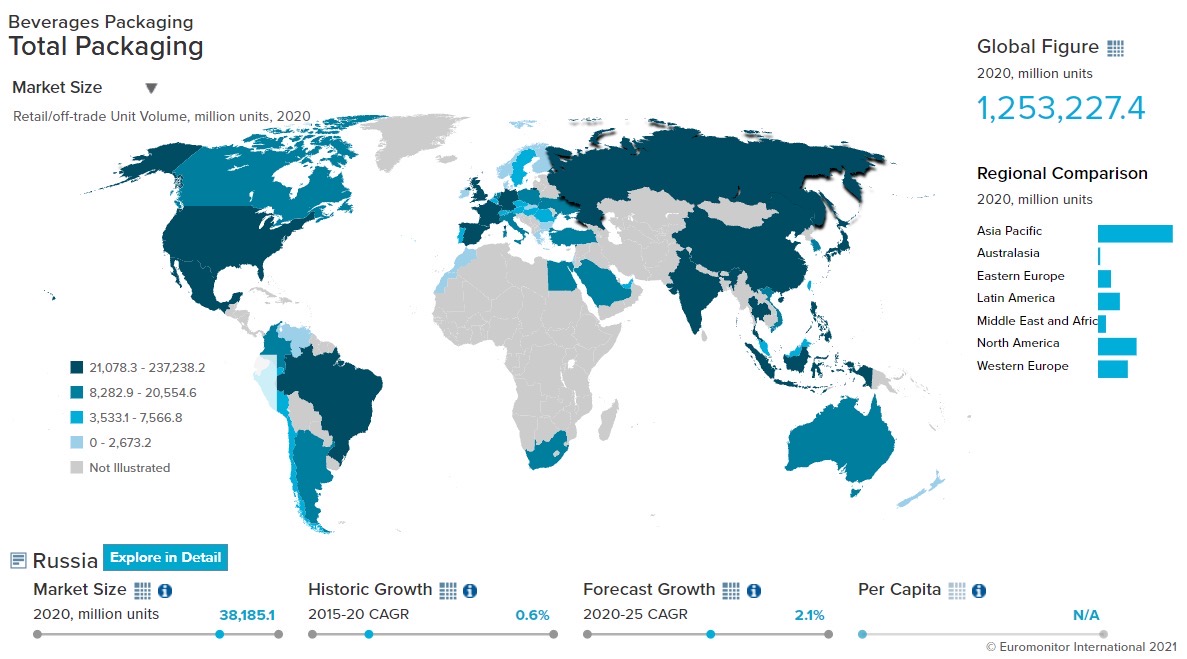

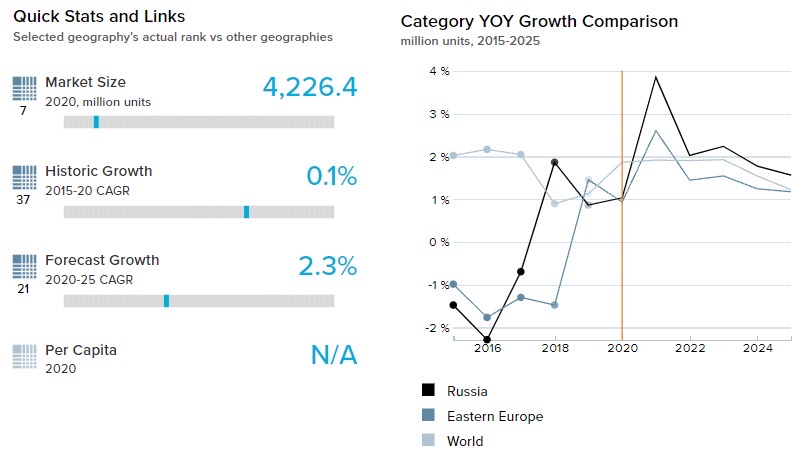

Beverages Packaging

37,880

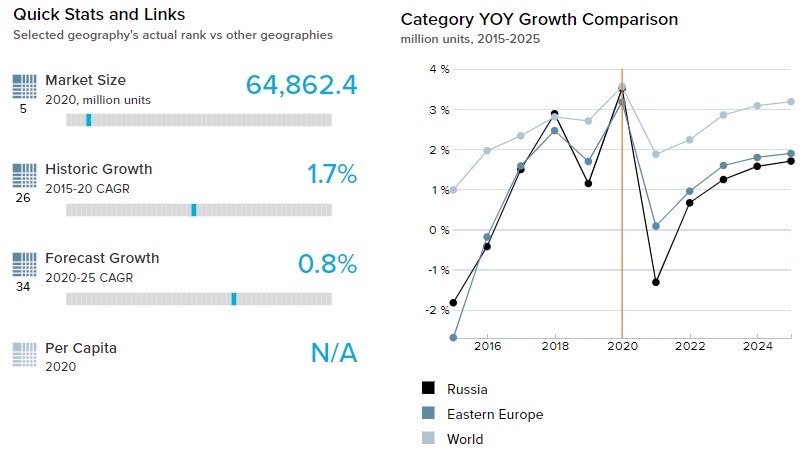

Food Packaging

105,024

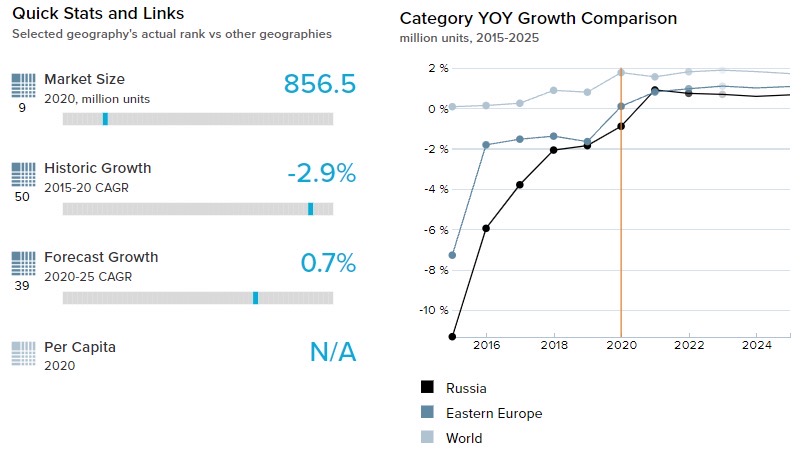

Beauty and Personal Care Packaging

4,239

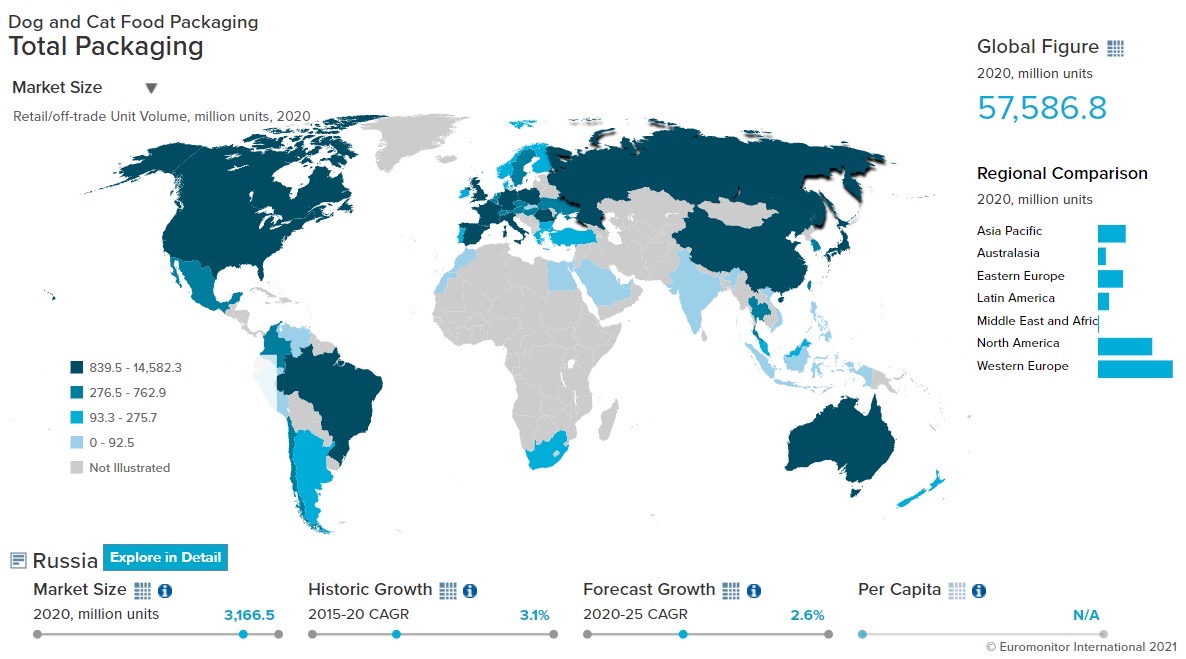

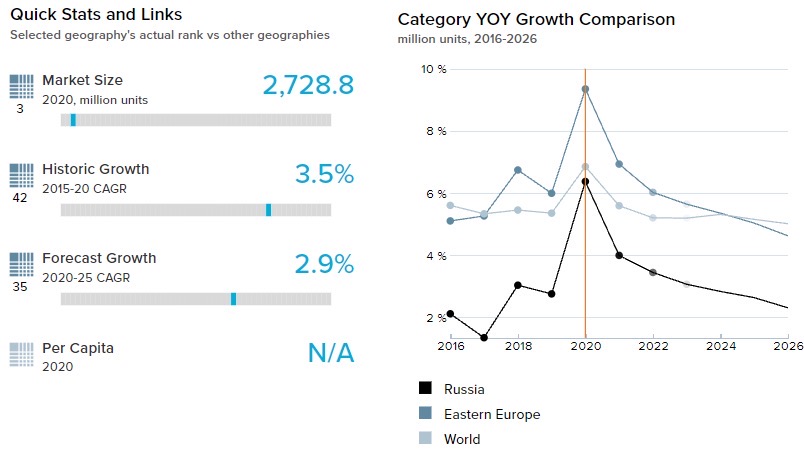

Dog and Cat Food Packaging

2,953

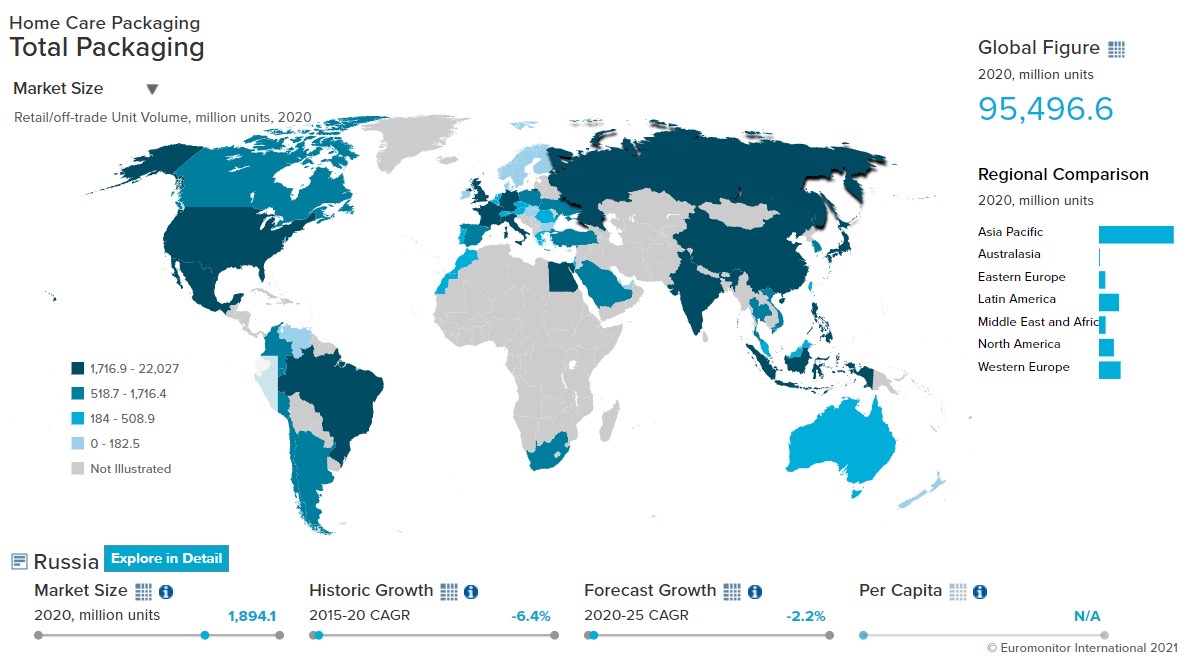

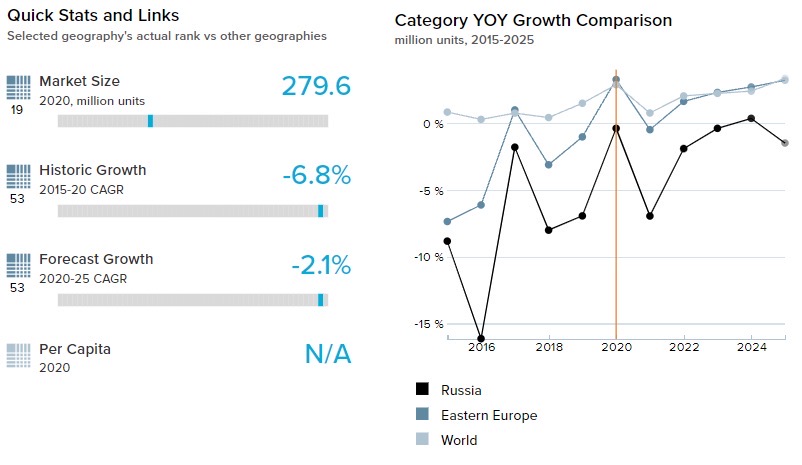

Home Care Packaging

1,894

Packaging Type

2020 Market Size (million units)

Rigid Plastic

35,507

Flexible Packaging

72,757

Metal

11,110

Paper-based Containers

8,994

Glass

15,124

Liquid Cartons

8,434

- Key Trends

-

The sale of larger packs has been a major trend in Russia during the pandemic. This is because, initially due to panic buying, consumers preferred larger pack size as it helps them stock products and offers lower per-unit price. Later, the popularity of e-commerce contributed to their growth as products were delivered at home, and consumers did not need to carry them. For example, Danone launched a 1.5-liter bottle of Prostokvashino milk in direct response to this demand shift while in personal care, Henkel Rus OOO launched Fa Cream shower gel in 2020 in a 750ml format and marketed it as being suitable for use by the whole family. Similar shifts towards larger pack sizes were observed in dog and cat food and in home care products like surface cleaners and laundry care.

- Packaging Legislation

-

In 2019, dairy packaging came under strict regulations as dairy products that do not contain milk fat substitutes had to be kept on different shelves. Therefore, retailers such as X5 Retail Group adapted the new requirements with price tags clarifying the milk fat substitute content situation. Manufacturers are also required to update the labels that clearly tell the consumers about the presence or absence of milk fat substitutes, as products containing these substitutes are believed to be unhealthy. As a result of this rule, many players changed their portfolio by providing more high-quality products in line with trends towards naturalness, while managing to keep prices affordable to most Russian consumers.

- Recycling and the Environment

-

Russian Prime Minister Dmitry Medvedev signed the approved state strategy for the development of establishments that process, utilize, and recycle industrial waste by 2030. With the rising occurrences of illegal dumping of industrial waste in Russia, this strategy aims to halt the dumping of 182 types of recyclable waste and intends to convert the suitable waste to energy.

- Packaging Design and Labelling

-

COVID-19 increased the popularity of online shopping in Russia and people are increasingly using this medium to order products. As a result, manufacturers are increasingly focusing on those packaging designs that can attract consumers' attention on device screens. Therefore, the use of such color combinations that can be highlighted on screens and help them stand out is coming to light and being adopted.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- At-home consumption of tea increased in 2020 in the country as COVID-19 lockdown restrictions forced people to stay at home. Since tea products have a longer shelf life, pack types such as flexible plastic which are resealable and help with extended storage are preferred. As a result, flexible plastic, which is widely used for pack sizes of 200g and more, showed a volume growth of 2.8% in 2020.

- Liquid cartons continue to dominate juice packaging with a volume share of 63.0% in 2020 but showed a volume decline of 0.8% in 2020. This is because plastic pouches, which are light and convenient to transport, are gaining popularity in this segment. As a result, pouches recorded a strong volume growth of 23.0% and a volume share of 3.4% in 2020.

- Trends

-

- The COVID-19 induced economic slowdown made consumers price-sensitive as there were salary and job cuts. To save money, people shifted from glass packaging in carbonates to larger PET bottles, which give a better per unit value and are easy to transport. As a result, glass bottles showed a volume decline of 20.1%, while PET bottles grew 6.8% in 2020.

- The sale of multi-packs in alcoholic drinks, especially beer, picked up pace in 2020. These pack types are convenient to store and limited the frequency of outside trips. As a result, metal beverage cans, which usually come in multi-packs, showed a volume growth of 7.8% in 2020.

- Outlook

-

- Metal beverage cans and paper-based packaging like bag-in-box are expected to perform well in soft drinks, with an expected volume CAGR of 6.2% and 6.7% respectively over 2021-25, owing to its sustainability and low environmental impact. Also, recycled PET is expected to be adopted more as major brands like Coca-Cola and PepsiCo are refocusing their manufacturing from regular PET bottles to recyclable variants.

- The trend to focus on personal health and well-being is expected to continue over 2021-25 and hot drinks which are positioned as being natural and organic are expected to do well as products made from natural ingredients are perceived to be healthier. Manufacturers are expected to prefer pack-types that can help maintain the freshness and essence of natural products. Thus, flexible packaging such as resealable flexible aluminum/plastic is likely to show a volume growth of 2.1% over 2021-25.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Owing to its light weight and ease with which it can be transported and stored, flexible packaging continued to dominate the dog and cat food market with a volume share of 85.9% in 2020 showing volume growth of 2.9%.

- Among flexible packaging, stand-up pouches were the leading pack type with a volume share of 91.6% and volume growth of 2.9% in 2020. This is because stand-up pouches can be easily molded into various pack designs and sizes, which helps customers choose from a variety of options as per their pet size and needs.

- Trends

-

- Shopping from e-commerce websites is increasing as it helps the customers to reduce their outside trips and the product is delivered at their doorstep. As a result, many manufacturers are shifting from metal cans to plastic pouches as the latter is more suited for transportation. This resulted in a volume decline of metal beverage cans in dog and cat food by 1.1% in 2020.

- Folding cartons saw a strong increase in its sales, although from a small base, which showed a volume growth of 9.5% in cat food in 2020. This is because they help the brands to stand out from their competitors as plastic pouches dominate the segment. Folding cartons can be seen differently from the rest in terms of shape and can help attract the customers’ attention.

- Outlook

-

- The popularity of e-commerce websites is expected to continue over 2021-25 as it allows customers to easily compare various brands and their price points, thereby making third-party marketplaces such as Wildberries, Ozon, and Beru popular websites for pet food shopping. As a result, flexible packaging, which is most suited for transportation, will continue to show a strong volume CAGR of 2.5% over 2021-25.

- The trend of differentiating from the competitors using different pack types is expected to remain in Russia. As a result, folding cartons, which is a good material for secondary packaging, as it is environmentally friendly, is expected to show a volume CAGR of 12.1% over 2021-25.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- The COVID-19 induced fear of virus contraction led to an increased focus on personal health and hygiene. As a result, bath and showering products witnessed strong demand in 2020. Flexible packaging, which remains the leading pack type with a volume share of 69.4% in 2020, showed a volume growth of 0.8% as opposed to a decline at a CAGR of -3.4% over 2015-19.

- Due to pandemic-induced economic uncertainty, sales of larger pack sizes such as 500ml plastic pouches in beauty and personal care grew by 31.3% in 2020 as they provide better value for money. Plastic pouches also provide convenience in terms of transportation and storage, which contributed to their growth.

- Trends

-

- Due to COVID-19 restrictions, consumers were forced to spend their lockdown time alone with limited trips outside and almost no physical social interaction. As a result, consumers cut their spending on products like color cosmetics and sun care. Their main pack type, rigid plastic, showed a volume decline of 9.8% and 22.0% respectively in 2020.

- There is an increasing demand for products packed in sustainable materials in beauty and personal care and many players are responding to it. For example, Lumene is offering packaging that consists of 50% recyclable plastic, whereas Procter & Gamble is selling its Head & Shoulders shampoo in Russia in new packaging composed of 20% plastic collected on Atlantic coast beaches and is 100% recyclable.

- Outlook

-

- Glass bottles are expected to do well over 2021-25. This is primarily because of its recyclability and it helps premium brands stand out from mass products. In skincare products, brands are introducing new hyaluronic acid or collagen-based products, for which glass bottles are a perfect fit as it does not react with the contents present inside. As a result, glass bottles are expected to show a volume CAGR of 1.7% in beauty and personal care and volume CAGR of 6.0% in skincare over 2021-25.

- With people becoming more aware of health and hygiene, demand for products composed of safe and natural ingredients is expected to increase. This is likely to encourage companies to improve both design and labeling, to convey a health-oriented image and deliver clear and precise product information.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- With people choosing to stay home and restrictions on out-of-home dining, time spent in personal kitchens increased. This boosted the growth of kitchen cleaners and dishwashing products. Their main pack type, PET bottles did well in 2020, showing volume growth of 11.6% and 8.7% respectively. However new pack types such as plastic pouches also started to gain popularity as refill packs in dishwashing products. This helped plastic pouches record a volume growth of 8.2% in 2020.

- Flexible packaging is a highly successful pack type in Russia as its lower price helps manufacturers gain a competitive edge. As a result, Dow Packaging and Specialty Plastics announced a new licensee agreement in December 2020 with Interpolychem LLC, a leading packaging producer in the Russian flexible packaging market, intending to produce 200,000 flexible packaging units a month.

- Trends

-

- Since the COVID-19 virus is perceived to transmit through interaction with infected surfaces, consumer demand for surface care products increased, showing a growth of 11.0% in 2020. The main pack type of surface cleaners, HDPE bottles, has a volume share of 86.2% and showed strong volume growth of 10.8% in 2020.

- Sales of home insecticides in Russia tend to depend on the weather conditions during the insects’ rearing period and spring 2020 in the country was very positive for the breeding of insects. Further, COVID-19 induced work from home enabled Russians to move and spend more time in rural areas away from the crowds of the cities. The use of home insecticides increased in rural areas thereby leading to the rise in demand for home insecticides in metal aerosol can formats such as 275ml and 400ml. The pack type has a volume share of over 50.1% and due to COVID-19 induced demand, registered a volume growth of 10.3% in 2020

- Outlook

-

- COVID-19 induced economic uncertainty is expected to persist, so manufacturers are likely to continue using flexible plastic as it helps drive the product cost down. As a result, flexible packaging, such as plastic pouches, is expected to show a volume CAGR of 3.3% in home care over 2021-25.

- Larger packs are expected to perform well over 2021-25 owing to their better price per unit. Therefore, larger packs such as 6kg and 9kg flexible plastic packs are expected to show a strong volume CAGR in home care products growing at 6.2% and 6.6% respectively over 2021-25.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- COVID-19 induced restrictions forced people to consume at-home meals since on-trade food establishments were shut down. The rise in home cooking consequently boosted the growth of frozen ready meals as it helped consumers reduce their cooking times. As a result, its leading pack type, flexible plastic, enjoyed a volume share of 37.5% in frozen ready meals and showed a volume growth of 3.9% in 2020.

- Being forced to spend extended hours at home due to COVID-19 restrictions prompted consumers to search for comfort foods that would help break the monotony of daily life. This contributed to the rise in consumer demand for niche chocolate confectionery products that were perceived to be self-rewarding and stress-reducing. Consequently, its main pack type, flexible plastic, managed to register a volume growth of 3.1% during the same year

- Trends

-

- Demand for dairy products in 2020 was boosted by the pandemic as consumers sought immunity boosting foods during the year to prevent their chances of contracting the virus. This helped dairy packaging grow by 5.7% in terms of volume for 2020. In terms of pack types, the main formats such as brick liquid cartons, thin-walled plastic containers, and flexible plastic showed a volume growth of 5.9%, 8.2%, and 3.2% respectively during the year.

- Manufacturers of baby food are developing various new and innovative ways to attract consumers and differentiate themselves from their competitors. Brands like Danone introduced Augmented Reality (AR) into their Smeshariki brand of dairy products for children. They printed an interactive tag along with the Smeshariki cartoon characters on the packaging of the product that can be scanned through an app. Users can then play games featuring characters from the cartoon. Danone also signed a partnership with Disney to use Disney, Pixar, and Marvel characters in its packaging design.

- Outlook

-

- COVID-19 induced economic uncertainty made people price sensitive and this trend is expected to continue over 2021-25. Therefore, processed meat, especially ham and sausage, which is less expensive than processed seafood, is expected to grow in demand. Thin-walled plastic containers and flexible plastic, which are the main pack types for processed meat, enjoyed a volume share of 19.9% and 43.8% respectively in 2020, and are expected to show a volume CAGR of 6.7% and 3.9% over 2021-25.

- COVID-19 induced demand for those products that provide consumer convenience, be it in terms of storage, consumption, or transportation. Therefore, manufacturers are expected to increase their focus on convenience over 2021-25. For example, several yogurt manufacturers introduced plastic pouches with screw top closures that allow children to easily consume the contents of the product. Many players are expected to follow the suit over the same period.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Russia

-

Mask regime and other COVID-19 restrictions canceled in Russia

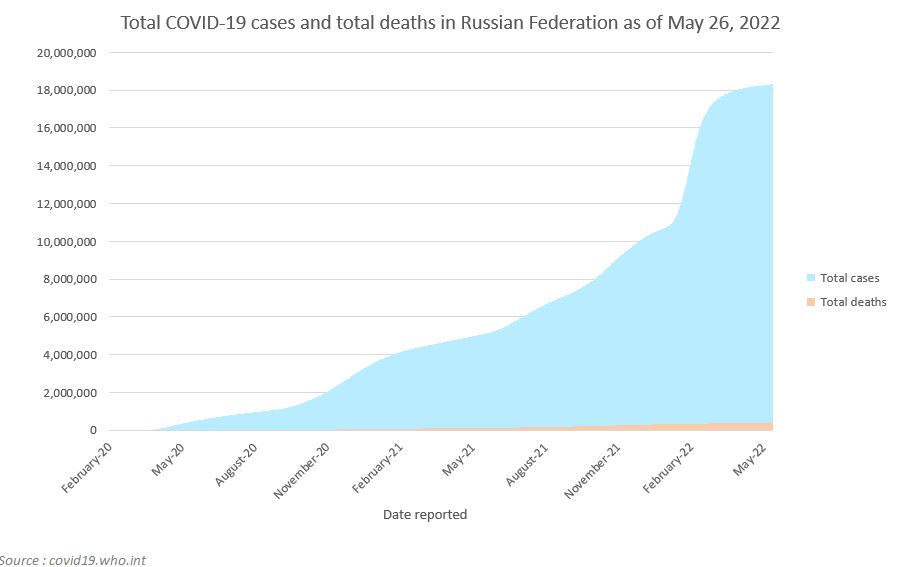

- According to the World Health Organization (WHO), Russia had a total of 18,310,673 COVID-19 cases, 378,700 deaths, and 126,817 cases per million inhabitants as of May 2022.

- In Moscow, the capital, the mask-wearing regime was lifted on March 15, 2022. Further, according to the report published on the website of the Ministry of Economic Development of the Russian Federation on April 4, 2022, 29 Russian regions have completely lifted the restrictions imposed on SMEs due to the pandemic.

- The limit on the maximum number of visitors (2,000 persons) for sports, physical, cultural, entertainment, and other activities was lifted on May 26, 2022, according to an order issued by Saint Petersburg's Chief Sanitary Inspector.

- According to the WHO, on May 24, 2022, Russia’s total vaccinations reached 166,534,236. The rate of the population that has been fully vaccinated stands at 50.4 per 100 people.

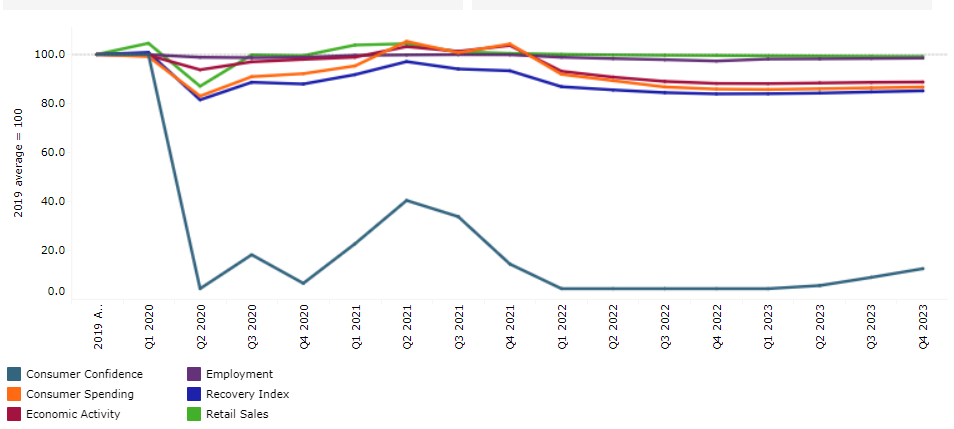

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Russia

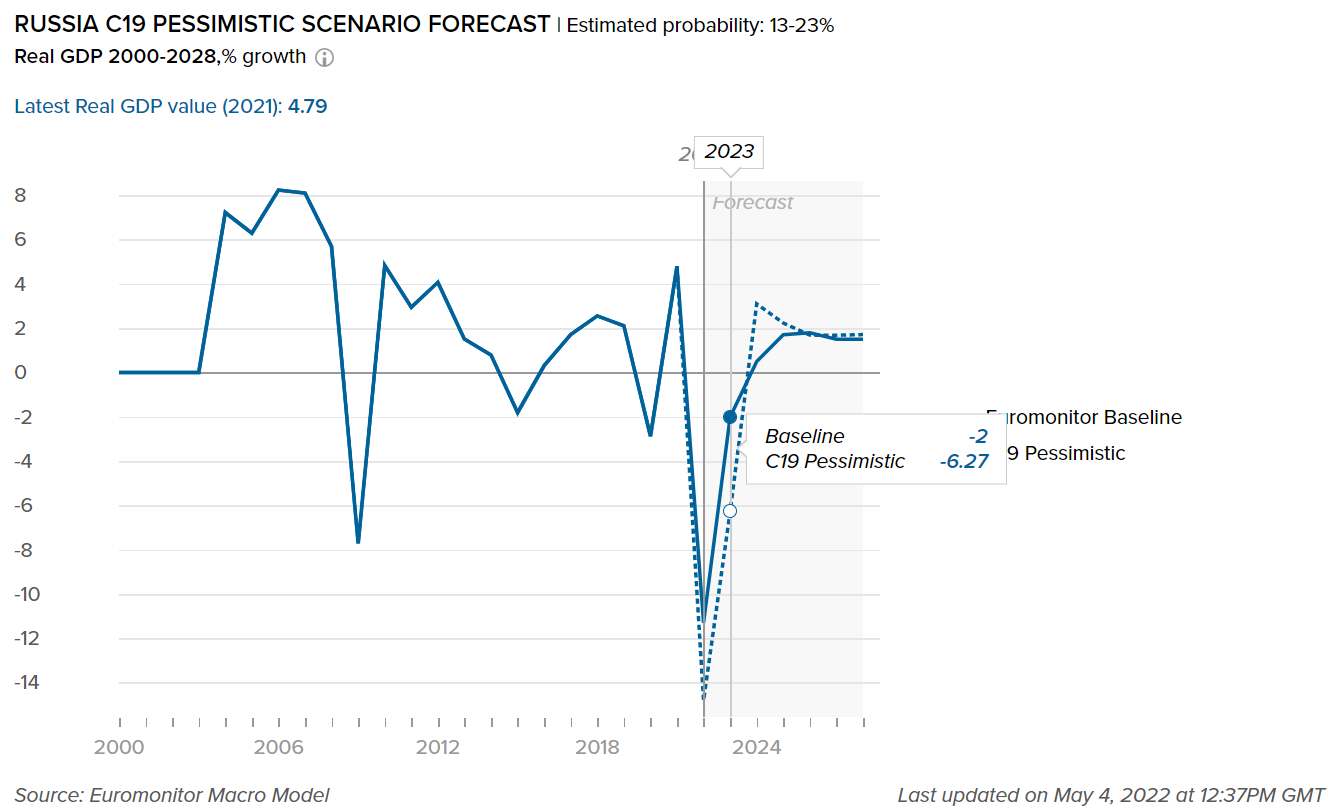

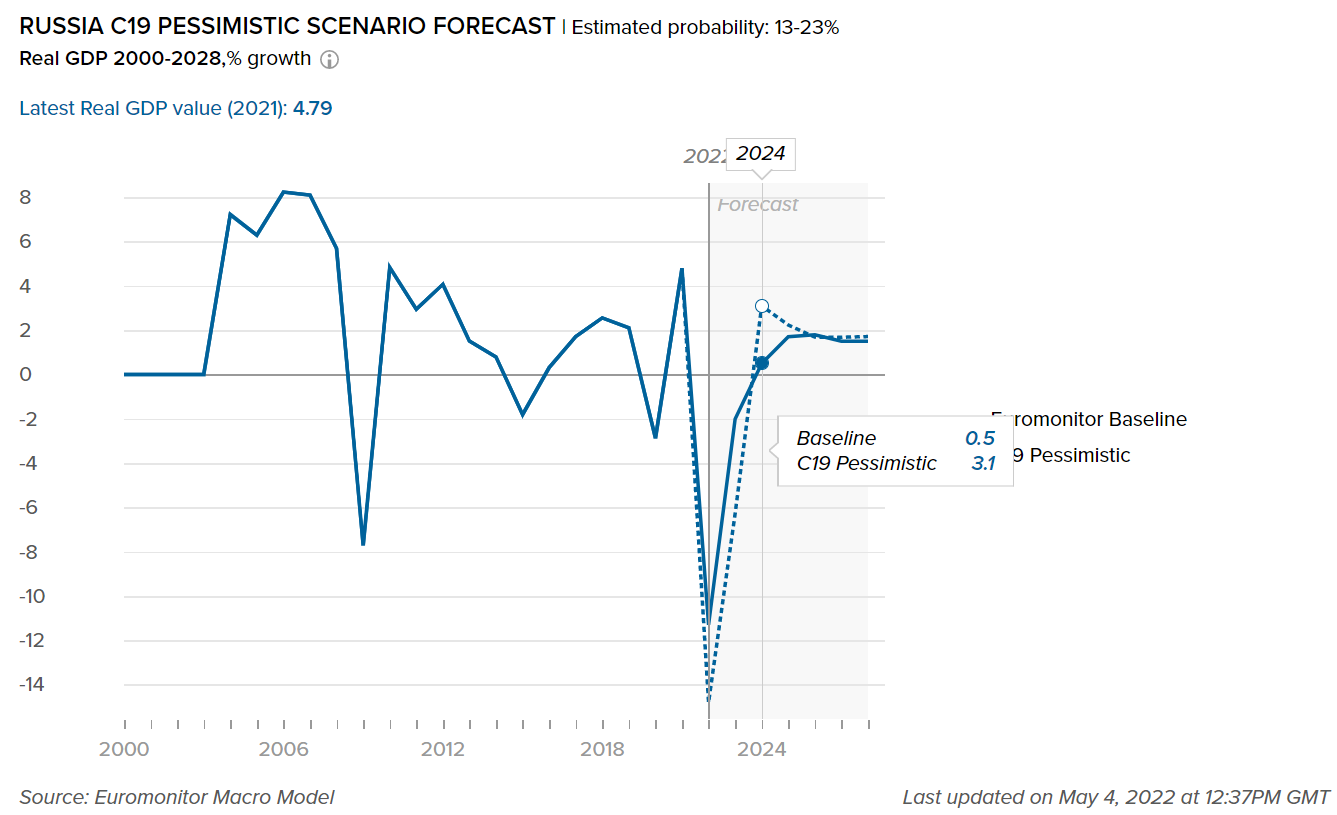

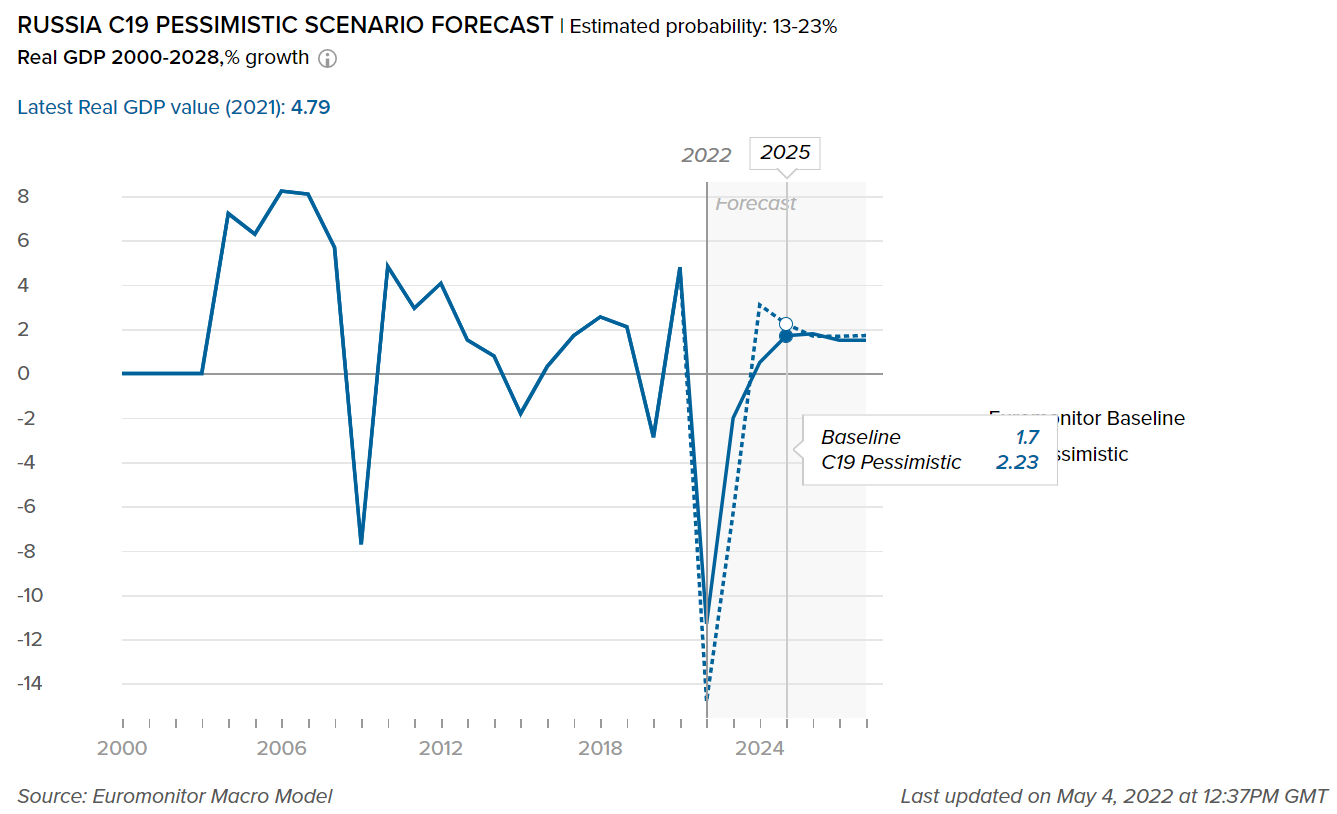

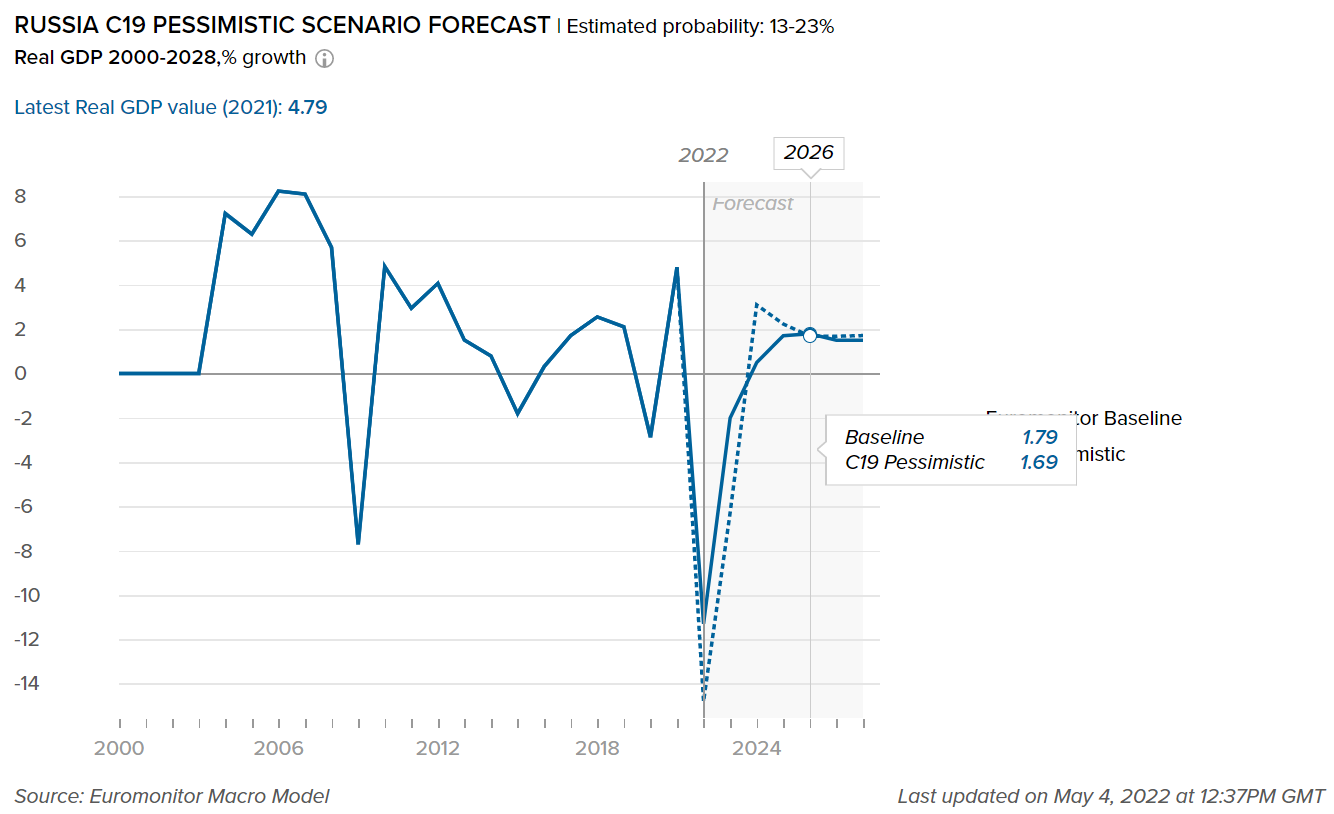

- Impact on GDP

-

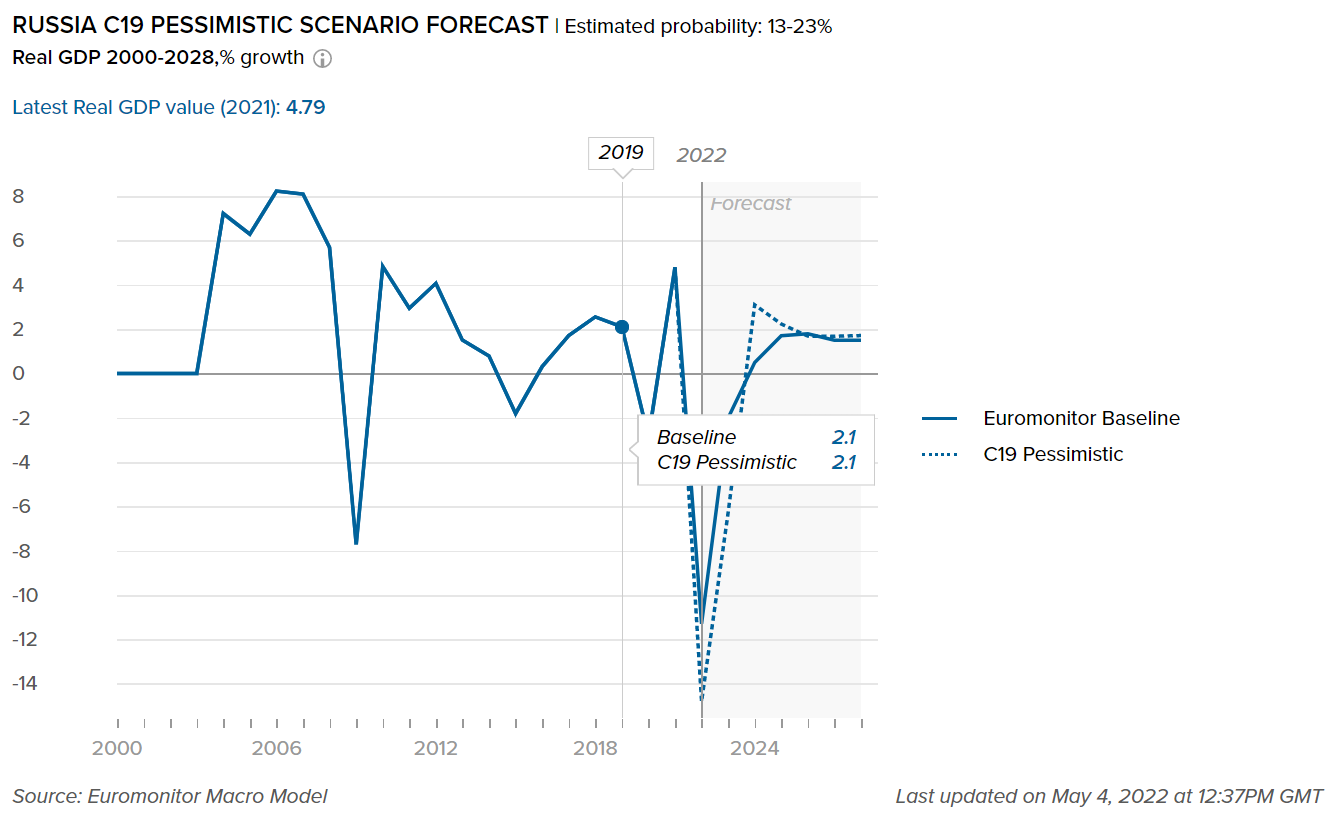

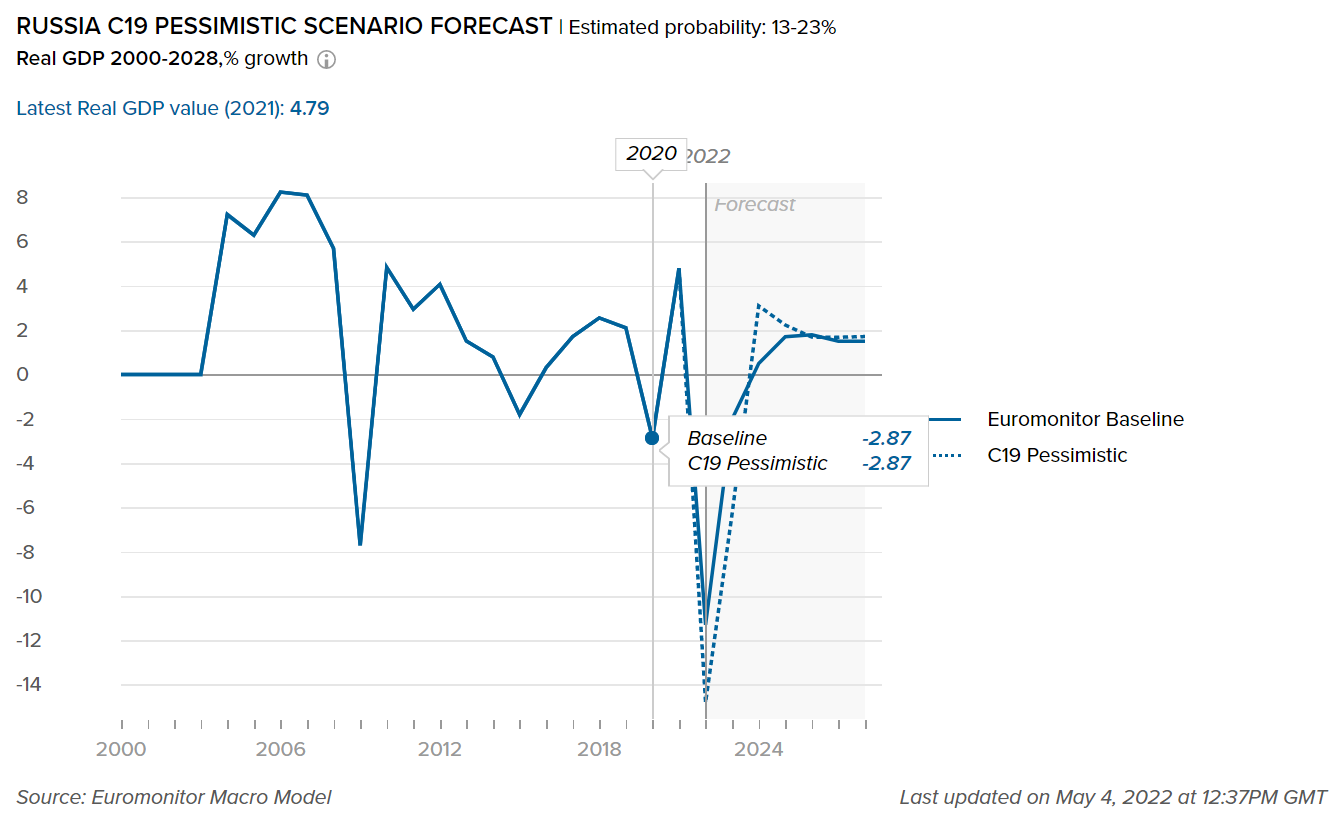

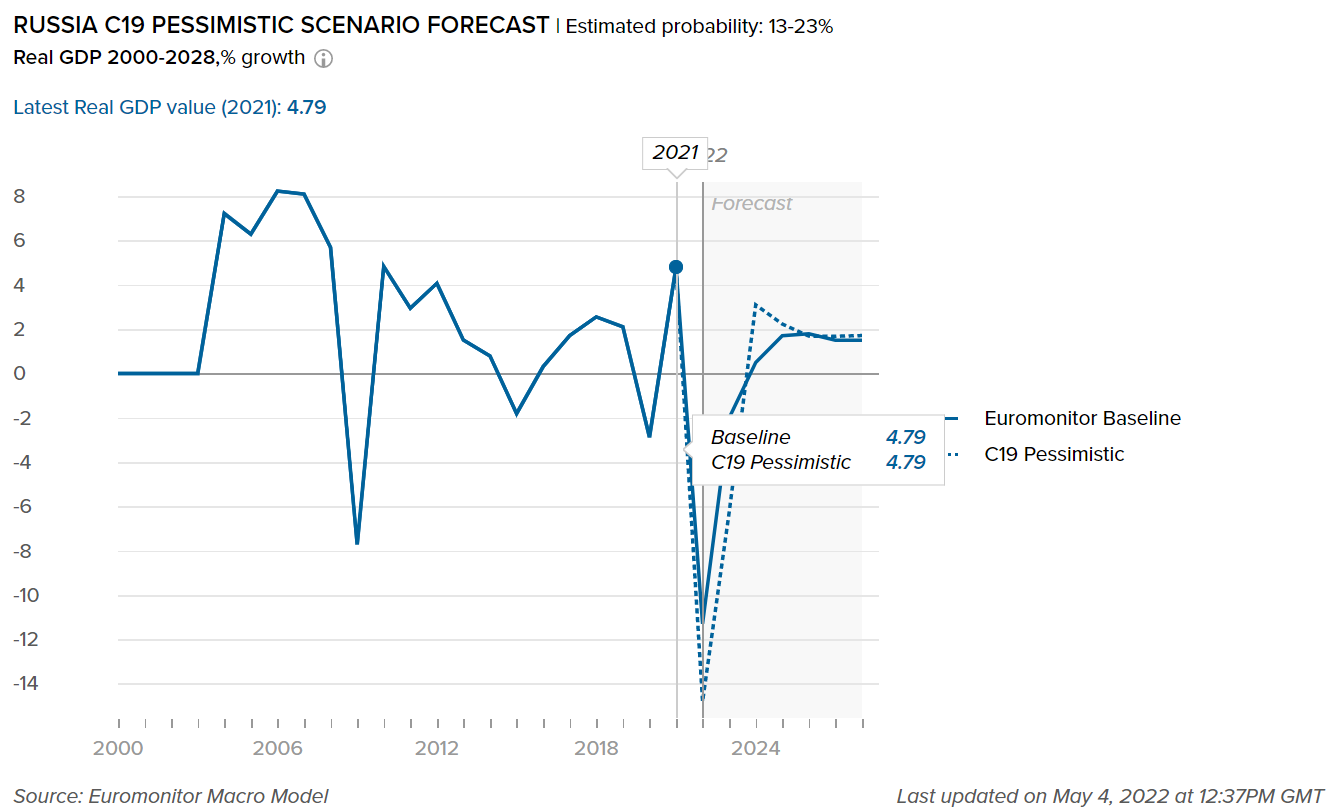

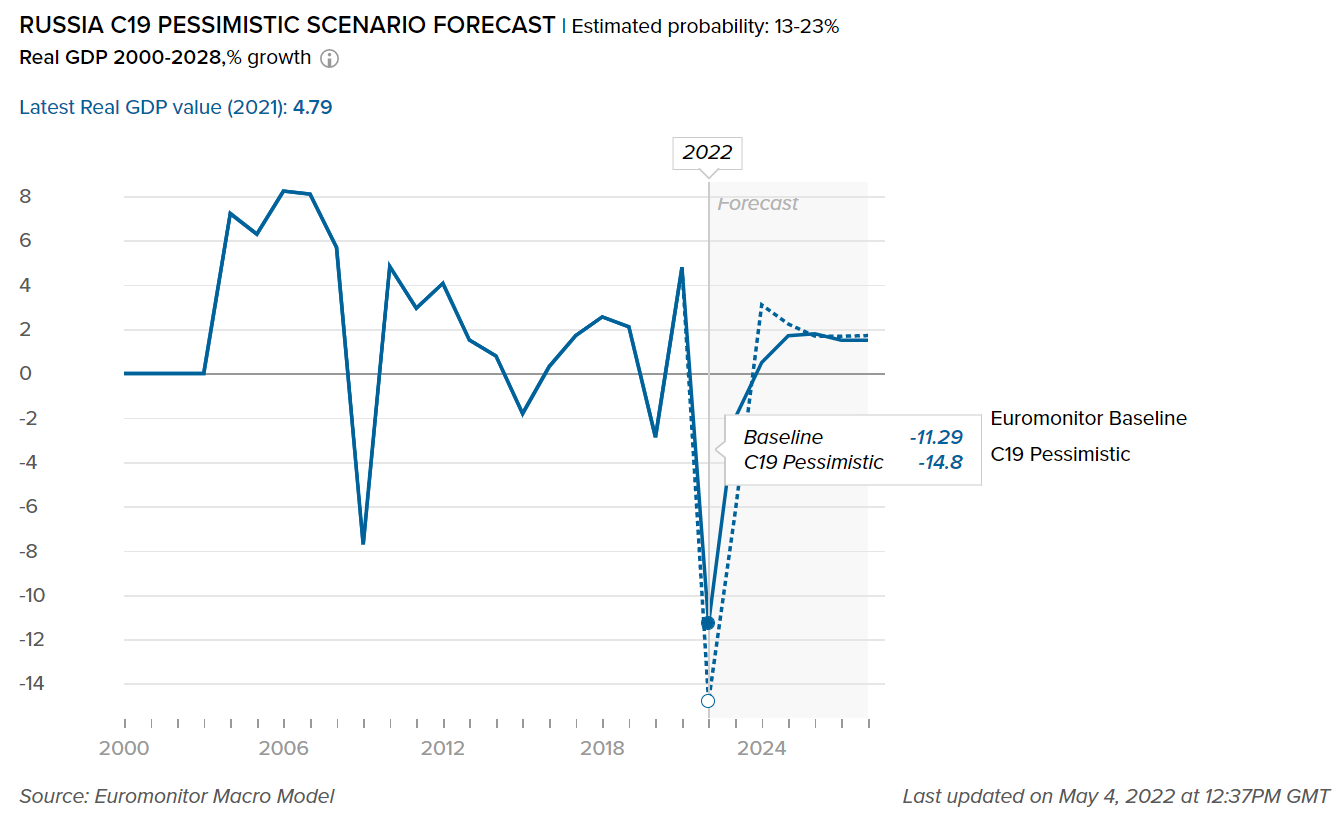

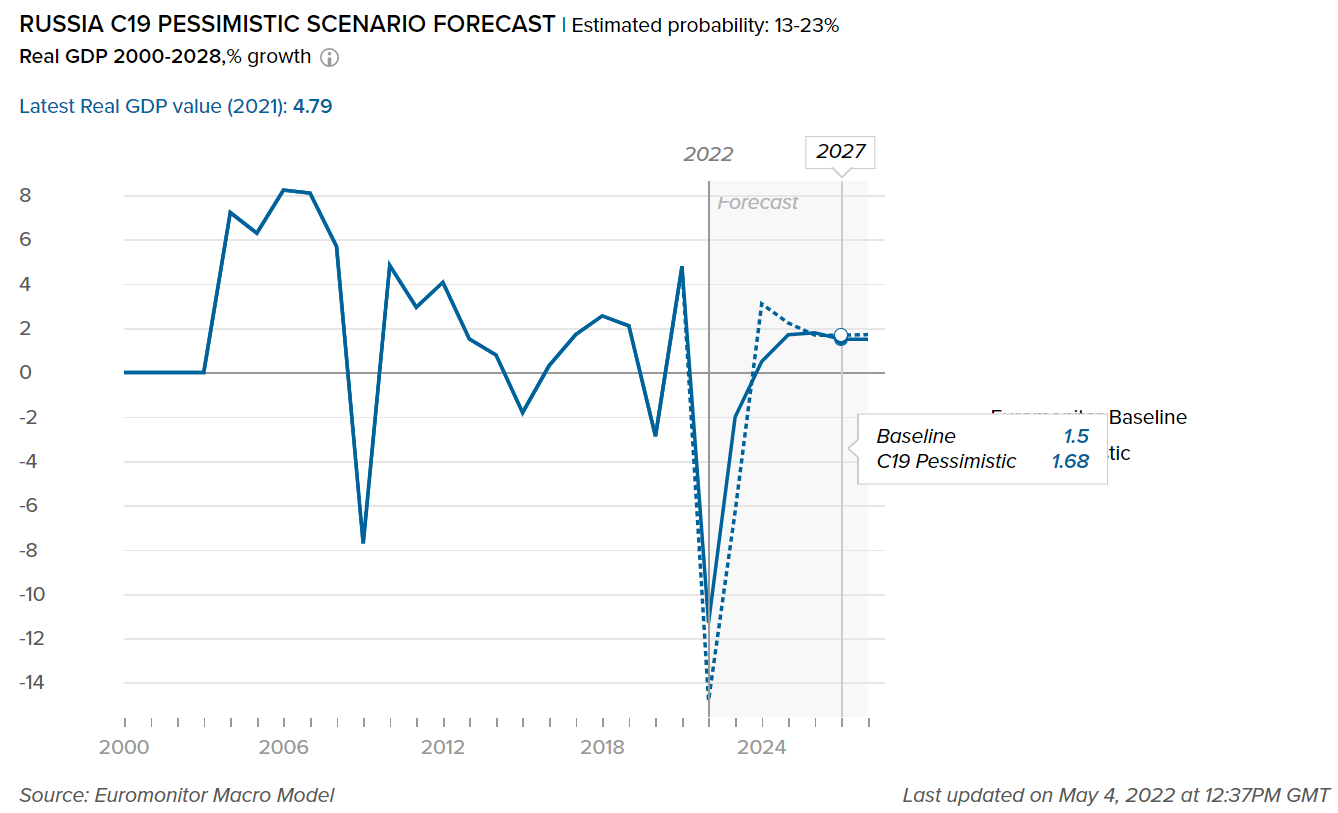

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in Russia. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Economic activity recovered slightly in 2021

- Due to the onset of the COVID-19 pandemic, in 2020, the Russian economy contracted for the first time since 2015. Private consumption and investment have been hampered by imposed cost-cutting measures and increased uncertainty about growth prospects. The country's economic damage was exacerbated by the collapse of oil prices and the country's oil production cuts under the OPEC+ agreement. However, in comparison to many other G20 economies, Russia's recession was comparatively moderate, supported by adopted economic stimulus measures.

- The National Plan for Economic Recovery, an accommodative monetary policy, an easing of containment measures, and a rebound in oil prices and demand helped the economy recover partially in 2021 with real GDP growing at 4.7%.

- Nonetheless, continuing geopolitical tensions, as well as sluggish productivity growth, pose threats to the economy's recovery. Annual real GDP growth is expected to be lower than the average for Eastern Europe over the long term, showing a projected massive decline in 2022.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

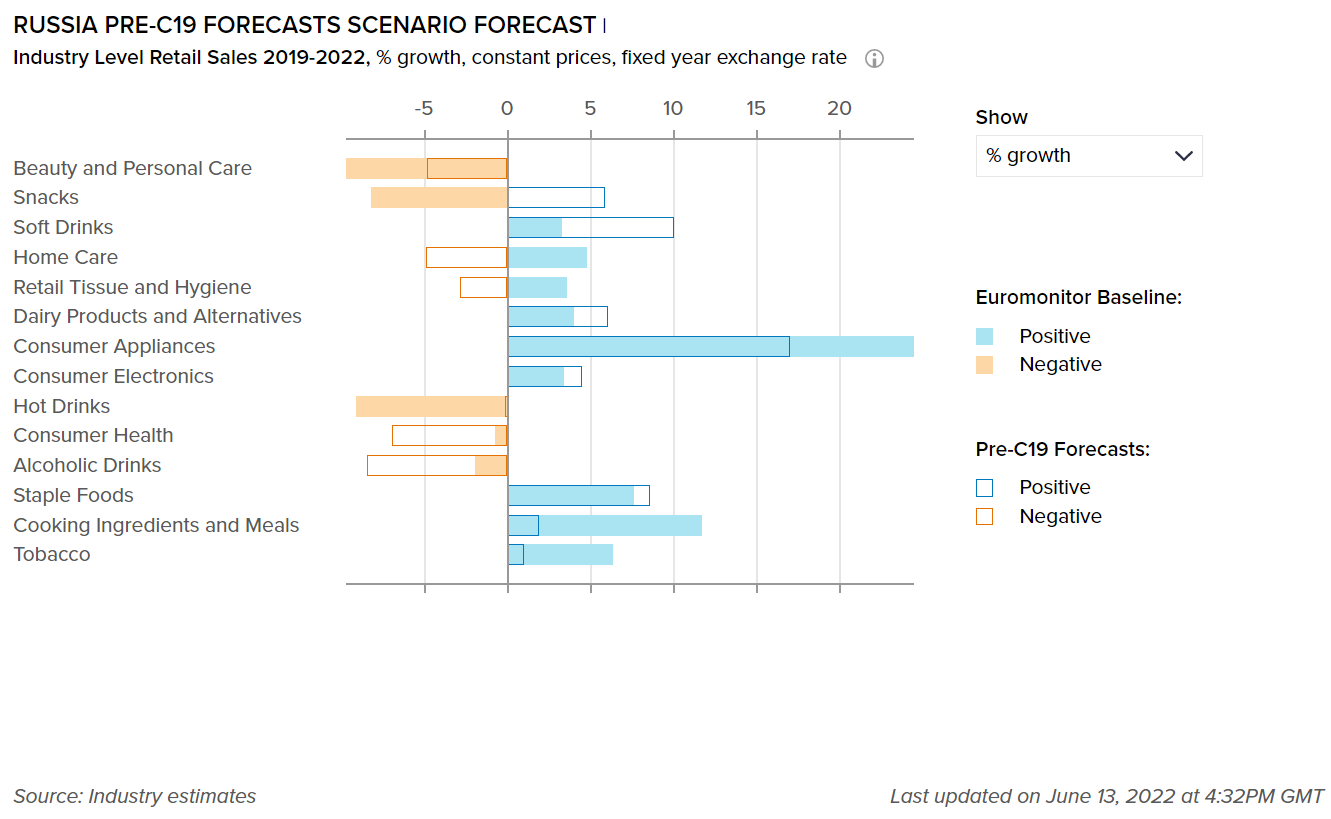

The graph below displays the adjusted forecasts of the percentage growth for the categories mentioned to highlight the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 65-75%.

Beer benefited from offering affordable price points

- Due to its affordability in a time of economic turmoil, standard lager remained by far the most popular type of beer in Russia, posting significant volume growth. As many Russians choose to downgrade to less expensive brands to save money, economy brands excelled. During the health crisis, players tried to keep price hikes to a minimum to drive volume sales. The top beer company, AB InBev Efes Group, was able to raise its overall volume share by maintaining a balance between its share and profitability.

- However, potential legislative changes may hurt the volume growth of beer in Russia. As part of its efforts to combat illegal sales and counterfeiting, the Russian Federation's government is proposing new labeling rules that would apply to beer and other alcoholic beverages. The measures are opposed by Russia's large breweries, which believe that the new labeling rules will increase production costs.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

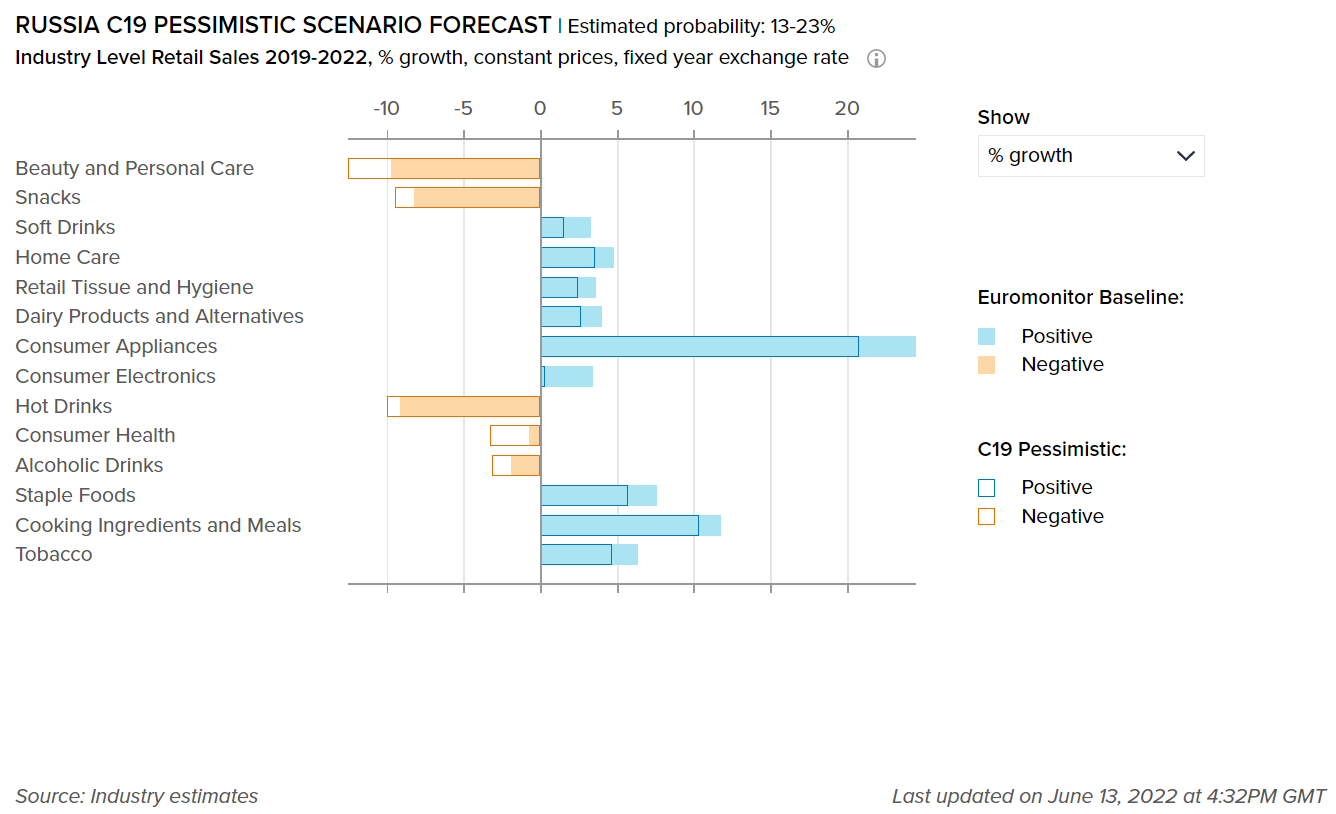

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors mentioned in Russia. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

The rising trend of home cooking pushes higher demand for staple and basic cooking products

- Products essential to home cooking have been in high demand, including edible oils, sauces, dressings, and condiments as well as staple foods. According to Euromonitor International’s Baseline scenario forecasts, cooking ingredients enjoyed 11.7% growth, while staple foods grew by 7.6% over 2019-2022. Russian consumers are becoming more demanding of the quality and safety of packaged food products, as well as seeking new experiences from food; as such, packaged cooking ingredients provide convenient value for money and easy solutions to consumers who due to economic hardship remain keen on home cooking.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

4,233

4,224

-1.8

Home Care Packaging

1,976

1,942

6.4

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

36,262

36,929

-0.01

Flexible Packaging

65,744

66,187

0.05

Metal

11,321

11,815

0.06

Paper-based Containers

8,413

8,373

0.02

Glass

14,841

14,749

0.01

Liquid Cartons

8,157

8,130

0.00

Rising environmental awareness fueling development in Russia’s packaging industry

- Over the review period, the ‘green’ trend gained traction in Russia, with increased local interest in environmental friendliness. As a result, there has been a growing focus on the sustainability of product packaging in the beauty and personal care industry, with firms increasing their investment in environmentally-friendly, recyclable packaging. Lumene offers packaging that is made of 50% recyclable plastic. Kalina Concern ensures that all its brands sold in cartons are labeled to indicate that the material was created sustainably using certified ecologically responsible resources. Procter & Gamble is introducing new packaging for its Head & Shoulders shampoo in Russia, made up of 20% plastic gathered on Atlantic coast beaches and 100% recyclable.

- Sustainability trends will also influence metal beverage cans and paper-based pack types, as well as boost the adoption of recycled PET, which is expected to see increased use. In the soft drinks industry, major brands such as Coca-Cola and PepsiCo can be seen refocusing their manufacturing from regular PET bottles to recyclable variants. This is of great importance for Russia, which, in January 2020, showed an increase of 9% year on year in PET consumption.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recover Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is officially the best measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.