Overview

- Packaging Overview

-

2020 Total Packaging Market Size (million units):

56,067

2015-20 Total Packaging Historic CAGR:

4.4%

2021-25 Total Packaging Forecast CAGR:

3.0%

Packaging Industry

2020 Market Size (million units)

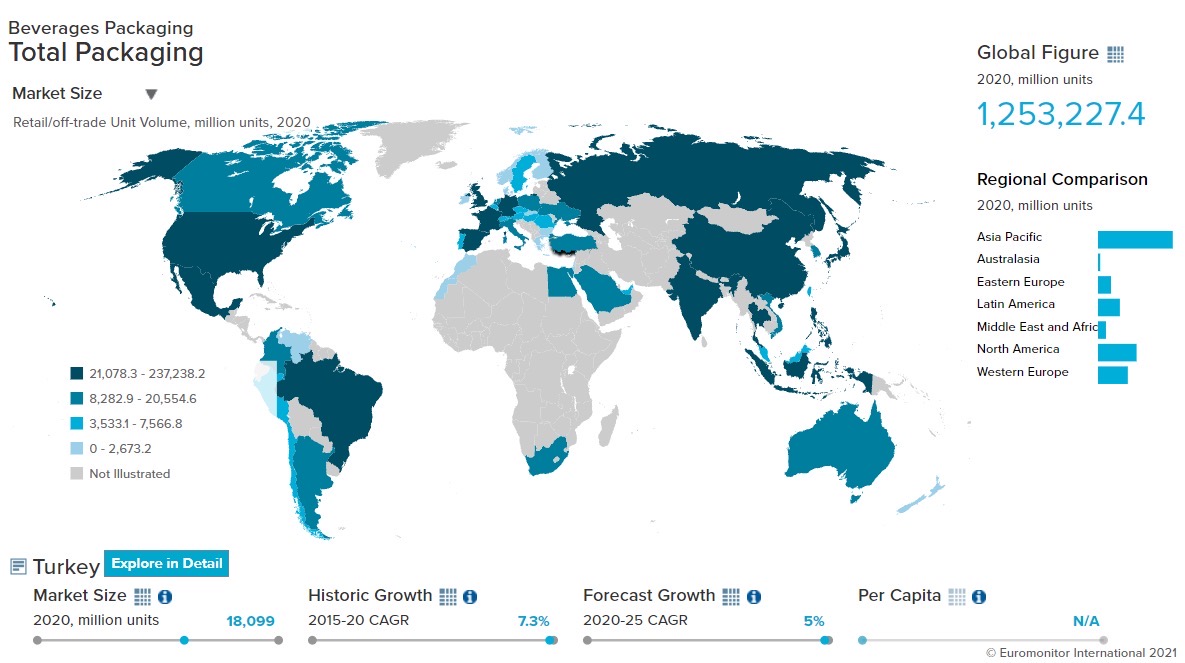

Beverages Packaging

18,005

Food Packaging

35,617

Beauty and Personal Care Packaging

1,243

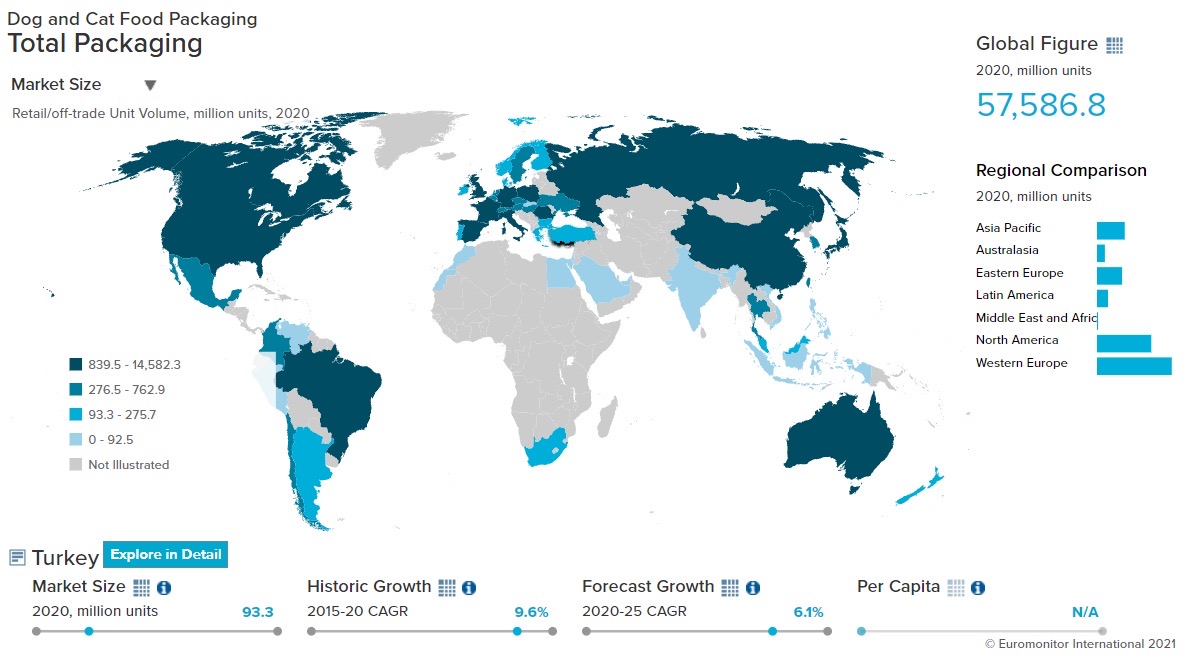

Dog and Cat Food Packaging

75

Home Care Packaging

1,127

Packaging Type

2020 Market Size (million units)

Rigid Plastic

14,737

Flexible Packaging

26,775

Metal

4,047

Paper-based Containers

2,215

Glass

5,119

Liquid Cartons

2,984

- Key Trends

-

Consumer confidence in the Turkish economy has been falling due to the economic crisis, high inflation, devaluations of the local currency, and Turkey’s increasing involvement in the Syrian conflict. This was exacerbated by pandemic-induced economic uncertainty that impacted consumers' disposable incomes. As a result, price sensitivity is the most important trend in the Turkish market as consumer preferred low-priced products. Manufacturers responded to this shift in buying patterns by using less expensive materials for packaging to make their products affordable for the cash-strapped consumers. As a result, there was rising popularity of low-cost flexible packaging in hot drinks, bath and shower, home care, and confectionery products.

- Packaging Legislation

-

In 2019, the Turkish government tightened requirements to the labeling guidelines in beauty and personal care. As per this guideline, manufacturers cannot support a free-from claim on its labeling without an approved laboratory test. Moreover, packaging and labels must not carry any free-from claims which may be reasonably interpreted as promoting a product’s benefit. For example, terms such as “hypoallergenic” or “free from allergens” cannot be used on the products’ packaging as allergies are highly dependent on body type and manufacturers cannot be 100% sure that the product will not cause allergies.

- Recycling and the Environment

-

Turkey is the leading importer of waste from the EU, but how much of that waste is recycled is unclear, as reports suggest that some of it ends up dumped in rural areas, on roadsides, or burned. Due to this, in September 2020, Turkey imposed limits on paper and plastic scrap recycling imports to 50% of the receiving companies’ production facilities, which will free some capacity for recycling domestic plastic waste.

- Packaging Design and Labelling

-

Brands are using packaging designs to create a more premium-like image for their products and help them differentiate from their competitors. For example, in confectionery, Nestlé introduced folding cartons for its product in a bid to boost the premium appeal and gain customers’ attention. In bottled water, Hayat developed 330ml PET bottles featuring QR codes with a theme of Hayat’la Kesfet (“Explore with Hayat/Life”). Upon scanning of code, consumers could listen to stories, play games, and explore the worlds of animals. In soft drinks, Coca-Cola launched a 250ml metal beverage can in the shape of the classic Coca-Cola glass bottle, aiming for a distinctive and premium image on shelves.

Click here for further detailed macroconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Price is the major purchase factor for hot drink consumers in Turkey, meaning manufacturers are constantly looking for packaging materials that have the lowest price points. Since flexible packaging is relatively affordable, pack types of flexible plastic continued to dominate hot drinks packaging, recording a volume share of 71.9% and volume growth of 3.4% in 2020.

- The pandemic forced people to go for at-home consumption of coffee. This boosted the demand for aluminum/plastic pouches which are used as refill packs. Consumers buy the original packaging only once and then buy refill packs as they are cheaper and convenient in terms of storage. This helped aluminum/plastic pouches to record a strong volume CAGR of 14.8% in coffee over 2015-20.

- Trends

-

- Turkey was already facing high inflation and an economic crisis, which further worsened in 2020 due to pandemic-induced lockdown restrictions. It resulted in the shrinkage of consumer budgets and they shifted from premium alcoholic drinks to mass-produced cheaper alternatives. For example, premium lager sales showed a volume decline of 15.1% in 2020 as consumers shifted to lower-priced alternatives, such as brandy, which showed a retail volume growth of 15.6% in the same year.

- PET bottles continued to dominate soft drinks packaging with a volume share of 48.4% in 2020, owing to their availability in larger pack sizes, which were in demand during the pandemic. This was because of many reasons; larger pack sizes such as 2,000ml and 5,000ml provided lower per-unit prices, helped in stockpiling products, and helped consumers reduce their frequency of outside trips. As a result, PET bottles recorded a volume growth of 22.1% in 2020 with 2,000ml and 5,000ml PET bottles showing volume growth of 12.1% and 37.3% respectively in the same year.

- Outlook

-

- Turkey’s zero-waste project, which aims to reduce the usage of single-use plastic and achieve 100% recyclability by 2023, is helping create awareness of the detrimental effects on the environment through the utilization of single-use plastic. In response, soft drinks manufacturers are expected to shift from their dominant packaging PET bottles to recycled PET (rPET) bottles or 100% recyclable plastic material over 2021-25.

- Since the economic effect of the COVID-19 pandemic is expected to linger over 2021-25, cash-strapped consumers are expected to buy larger packs of hot drinks to get better per unit value. Therefore, pack sizes like 500g and 1,000g folding cartons are expected to show a volume CAGR of 2.5% and 4.2% respectively over 2021-25.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Flexible packaging, like flexible plastic and plastic pouches, continued to dominate dog and cat food packaging with a volume share of 80.7% and volume growth of 7.8% in 2020. This is because the packaging helps preserve the freshness of the content for longer periods and helps provide the convenience of storage due to their compactness and lightweight.

- The sale of larger packs of 10kg and more increased in 2020 as it helps the consumers to spend less money per unit. Also, buying larger packs means less frequent trips to shops, which helped in following the lockdown restrictions in Turkey. As a result, 10 kg and 12kg plastic pouches and 15kg flexible plastic showed a volume growth of 23.6%, 8.6%, and 5.9% respectively in 2020.

- Trends

-

- Dry dog food continued to outperform wet dog food in Turkey. Customers perceive wet food as inconvenient as it must be consumed in a short amount of time or the food gets spoiled. As a result, dry dog food showed a volume growth of 2.6% in 2020 while wet dog food showed a volume decline of 5.9% in the same year. This helped dry dog food packaging such as plastic pouches grow by 12.4% in 2020. Meanwhile wet food packaging formats, such as metal food cans, showed a volume decline of 6.5% during the same year.

- Due to the weak economy exacerbated by the pandemic, people are looking for cheaper products in the pet food segment. Therefore, manufacturers are opting for cheaper packaging material to reduce product costs, which has helped less expensive pack types like flexible aluminum/plastic show a strong volume CAGR of 15.7% over 2015-20.

- Outlook

-

- The popularity of smaller dog breeds such as pugs, French bulldogs, and chihuahuas is expected to increase. Younger members of the workforce are expected to move to urban cities for better job opportunities and therefore will have space constraints. As a result, smaller pack types such as 100g and 200g are expected to show a volume CAGR of 7.2% and 5.3% respectively over 2021-25.

- E-commerce shopping is expected to remain in trend as the threat of the COVID-19 virus is likely to persist. This channel helps owners compare different products easily and helps them to make an informed decision concerning the product’s nutrients and price point. Further, the convenience of home delivery provided by this channel is likely to increase the demands of multi-packs, as it removes the need for consumers to carry heavy pack sizes. Therefore, plastic pouches, which are suitable for transportation and can be packed together easily are expected to show a volume CAGR of 13.8% over 2021-25.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- To protect themselves and their families against COVID-19 infection, the demand for bath and shower products saw an uptick in 2020, growing 33.0% in value terms. This helped the growth of flexible packaging formats like flexible plastic and plastic pouches. These forms are the dominant pack types and recorded a volume share of 48.3% in 2020 for bath and shower products. Flexible plastic showed a volume growth of 15.7% in 2020, thanks to the increased sales of bar soap, while plastic pouches showed a volume growth of 43.1%, albeit from a small base, thanks to the increased sales of liquid soaps.

- Trends

-

- Over 2015-20, beauty and personal care brands continued to focus on millennials and Generation Z consumers, who are more open to experimentation and trying new products. Since smaller packs are best suited for trial purposes, manufacturers sold their products in such. As a result, 45g deodorant sticks and 125ml skincare creams showed a volume CAGR of 3.5% and 10.9% respectively over 2015-20.

- Since there were fewer events and social occasions to attend during the pandemic, the use of color cosmetics and deodorants were deemed non-essential. This negatively impacted the sales of their main pack types. Specialty cosmetic containers and glass bottles in color cosmetics showed a volume decline of -21.3% and -11.8%, while metal aerosol cans in deodorants declined -13.2% in 2020.

- Outlook

-

- The increased focus on personal hygiene is expected to continue over 2021-25, which is likely to help bath and shower packaging show a volume CAGR of 2.7%. Other categories such as skincare and fragrances are expected to return to growth following a decline in 2020 due to lockdown restrictions. This will help their packaging show a volume CAGR of 8.5% and 3.2% respectively over 2021-25.

- Rising consumer awareness about the effect of plastic pollution and wastage will likely shape the beauty and personal care packaging industry, as many brands and companies are shifting towards environmentally friendly packaging and setting sustainability goals. For example, in 2019 L’Oréal invested in biotech start-up company Carbios, which is working to develop improved plastic recycling technologies and has stated plans to use paper-based tubes in several of its products. Meanwhile, in 2020, Unilever pledged to cut down on its plastic use and to halve the levels of virgin plastic by 2025

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- Panic-buying for home care products in 2020 due to the fear of stock-outs boosted the demand for those pack types that provided the convenience of storage and usage. Due to this, flexible plastic and HDPE bottles, which are extremely durable, showed a volume growth of 12.8% and 7.3% respectively in 2020.

- COVID-19 had a huge impact on the already weak Turkish economy, leaving consumers with lower disposable incomes and forcing them to buy less expensive products. Owing to the lower price point offered by plastic pouches, manufacturers started using this pack type to cater to the demand of cash-strapped customers. As a result, plastic pouches showed a volume growth of 17.2%, albeit from a small base, in 2020.

- Trends

-

- Glass packaging sales suffered in 2020 due to the growing popularity of e-commerce, as people were afraid to go out due to COVID-19. Retailers avoided offering this pack types as glass would get damaged while transporting, a loss that retailers had to bear. As a result, glass jars and bottles showed a volume decline at a CAGR of -10.5% and -14.4% respectively in home care products over 2015-20.

- Shrink sleeve labeling is gaining popularity in home care products as it covers the entire surface of the product and gives a non-transparent look, which provides more space for brand communication. A shrink sleeve label is mainly used in rigid plastic formats such as PET bottles, which managed to register a volume CAGR of 4.2% over 2020-25.

- Outlook

-

- Rigid plastic is expected to continue dominating the home care packaging industry over 2021-25 because it is durability and can be easily stocked, stored, and transported. Pack types such as HDPE bottles, prevent spoilage of products due to the chemical reaction of acidic contents, especially in surface and toilet cleaners. As a result, rigid plastic is expected to show a volume CAGR of 1.1%, with HDPE bottles likely to show a volume CAGR of 1.6% over 2021-25.

- Since the Turkish government aims to reduce the usage of single-use plastic and achieve 100% recyclability by 2023, manufacturers are shifting away from plastic to recyclable plastic. For example, in March 2020, Henkel announced plans to increase the share of recyclable plastic in its plastic packaging to 100% by the end of 2025. Also, Procter & Gamble has targeted the year 2030 to achieve 100% sustainability through the use of recyclable and reusable packaging material for its leading home care brands.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- Flexible packaging continued to dominate confectionery packaging with a volume share of 85.0% in 2020. Within flexible packaging, flexible plastic is the most common pack type owing to multiple reasons. Flexible plastic is a non-sticky packaging material which makes it ideal for various categories across chocolate, gum, and sugar confectionery. Its’ lower price point also helps make it affordable for consumers. Finally, the property of being easily molded into different sizes helped this pack type register a volume share of 64.8% in 2020.

- The closure of foodservice outlets due to lockdown restrictions benefited the sales of ready meals as it was perceived as an ideal meal solution in the absence of outside dining. Within this category, refrigerated ready meals, shelf stable ready meals, and frozen ready meals led the growth. As a result, flexible plastic and folding cartons, two of the most common pack types of ready meals, grew 9.0% and 16.0% respectively in volume terms in 2020.

- Trends

-

- Among dairy products, cheese and yogurt are staples in the Turkish diet. Due to COVID-19, the consumption of these products increased, owing to their health benefits of boosting immunity and enhancing nutritional intake. Within these subcategories, thin-walled plastic containers are particularly popular, owing to their rigidity and ease of use and disposal. Due to this, thin-walled plastic containers showed a volume CAGR of 6.5% and 8.1% in cheese and yogurt packaging respectively over 2015-20.

- The COVID-19 pandemic forced many families with babies to stock up on baby food, as it was considered to be an essential product. This benefitted baby food packaging, which plateaued in 2019, to grow by 9.6% in volume terms in 2020. Within baby food, powdered milk formula products did exceptionally well as it is considered to be non-perishable and can be stored for a longer time. As a result, larger pack sizes such as 1,000g and 1,200g in folding cartons showed a volume growth of 9.5% and 11.1% respectively in 2020.

- Outlook

-

- The trend to adopt healthier eating habits among Turkish consumers to boost their immune system is expected to continue over 2021-25. This trend is expected to benefit the sales of processed meat and seafood as Turks believe that these products are nutritious and a key part of a balanced diet. As a result, the main pack types, flexible plastic and plastic trays, are expected to record a volume CAGR of 6.3% and 5.4% over 2021-25.

- Folding cartons, which is already a leading pack type in ready meals with a volume share of 38.0% in 2020, are expected to gain more share over 2021-25. This is because of its biodegradable properties and flat and easy to print surface, which brand owners can use to provide relevant information in eye-catching designs. As a result, this pack type is expected to show a strong volume CAGR of 10.3% over 2021-25.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Turkey

-

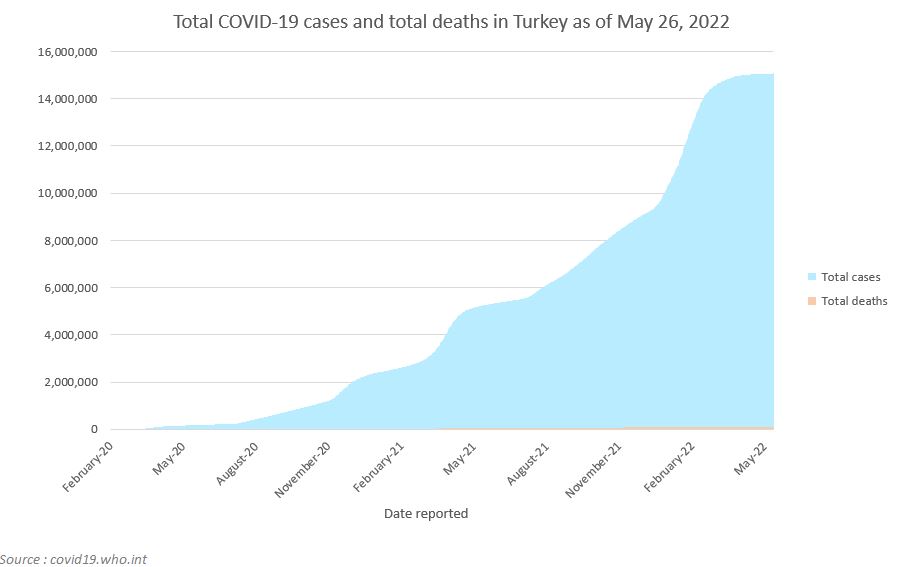

As the number of cases continues to decline, Turkey lifts all regulations regarding mask-wearing

- According to the World Health Organization (WHO), Turkey had 15,066,784 total COVID-19 cases, 98,943 deaths, and 1,260 new daily cases reported in May 2022.

- At the end of April 2022, Turkey lifted one of its final remaining COVID-19 requirements, the wearing of masks in crowded indoor settings. Mask use will be limited to public transportation vehicles and health facilities for the time being until the number of daily cases falls below 1,000.

- Earlier, in March 2022, the government relaxed requirements on wearing masks outdoors or in interior locations with adequate air circulation and social distancing. It also removed the need for consumers to present a smartphone app with their personal health records when entering locations such as shopping malls.

- According to the WHO, on May 24, 2022, Turkey’s total vaccinations reached 147,625,535. Overall, the country reached a full vaccination rate of 63.7 per 100 people.

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Turkey

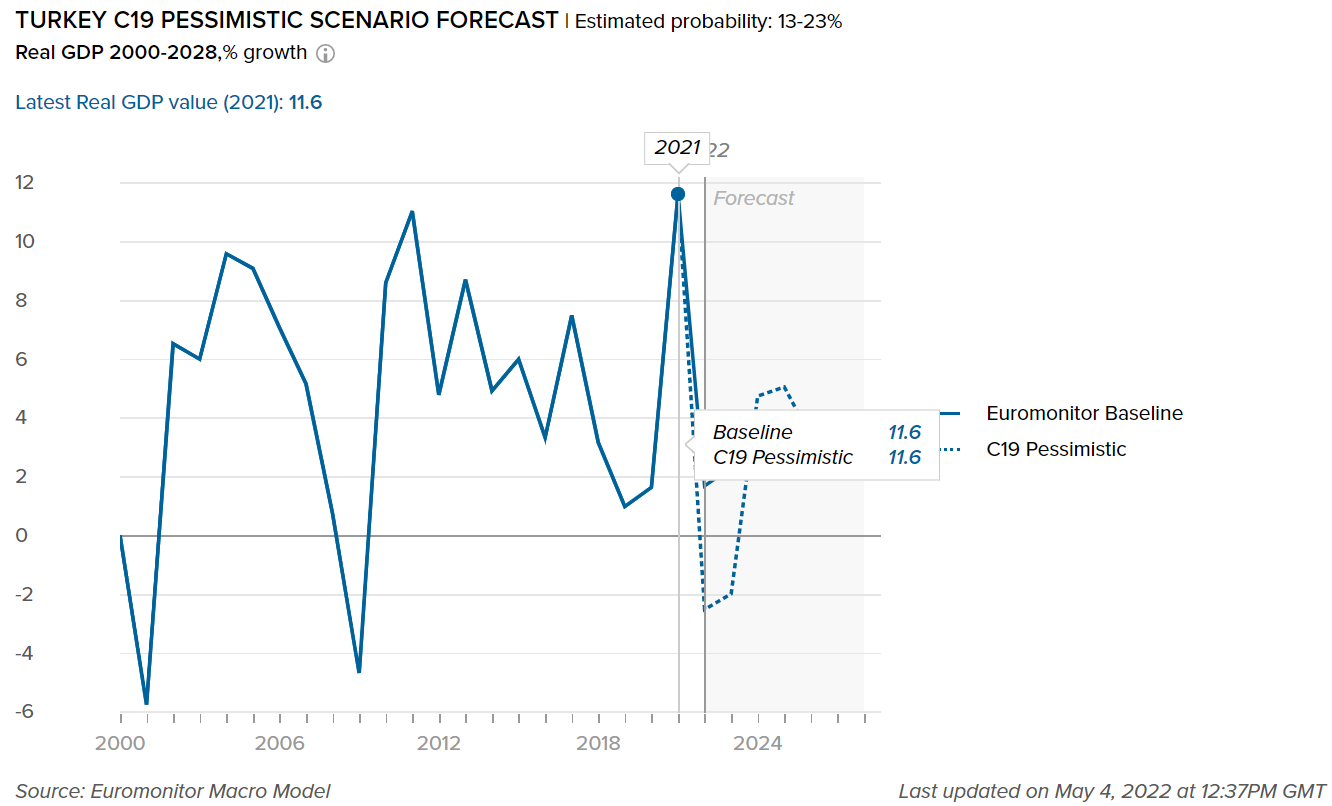

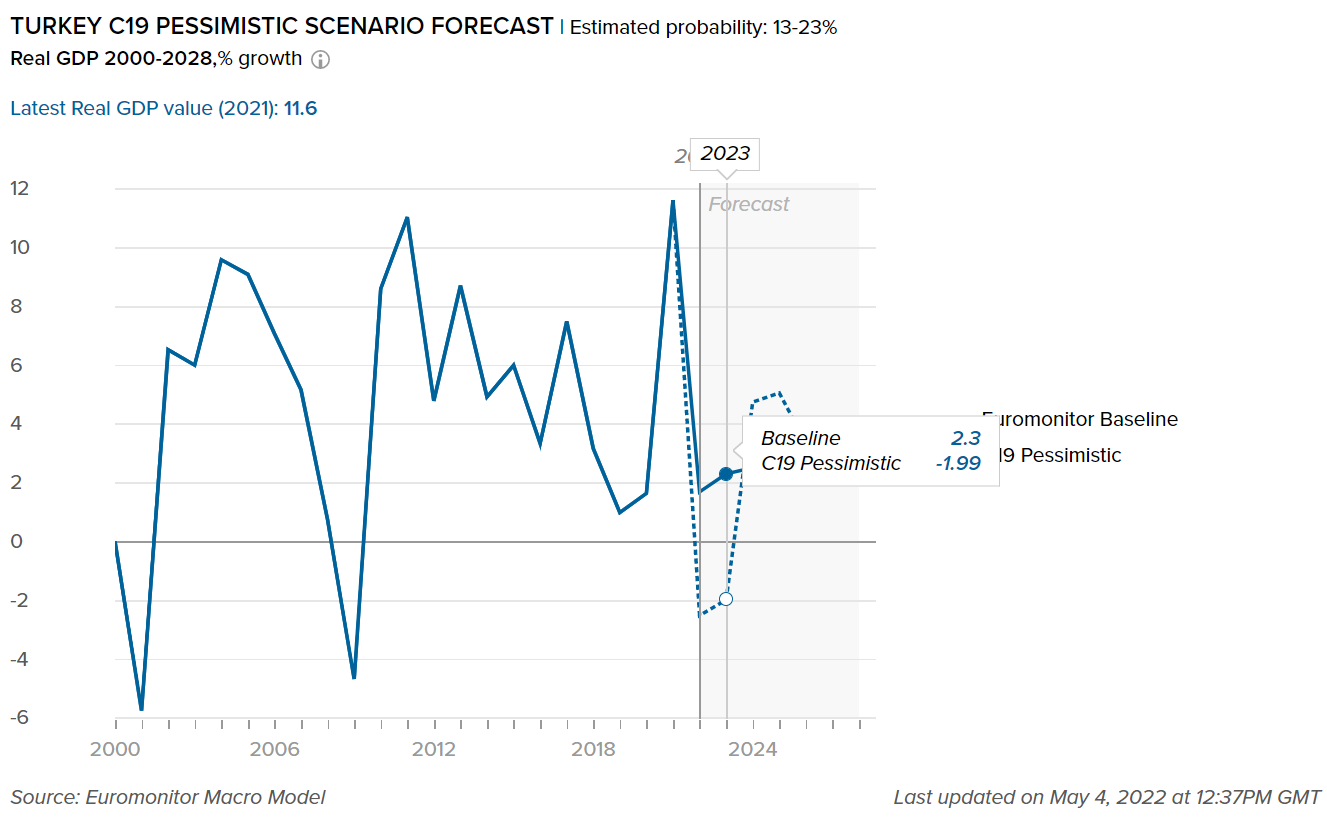

- Impact on GDP

-

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in Turkey. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

After strong growth in 2021, the Turkish economy is forecast to slow sharply in 2022

- Thanks to solid economic policy support, the Turkish economy recovered quickly from the health crisis. Turkey's real GDP expanded by 11.6% in 2021, above Western Europe's average growth of 5.7%. The country's economic performance was primarily driven by strong industrial production growth, soaring exports, and healthy private consumption during the year. Furthermore, the introduction of coronavirus vaccinations and the relaxation of COVID-19 restrictions aided the recovery of the country's services industry.

- According to the Turkish Statistical Institute, tourism revenues in the country will double to USD25 billion by 2021, thanks to a rebound in foreign arrivals. However, due to a worsening currency crisis and rising inflation, the economy lost pace in Q4 2021, and consumer confidence fell to its lowest level on record. Real GDP is anticipated to slow down in 2022 recording 1.6% growth.

- The services sector, which accounted for 63.3% of Turkey's total gross value added (GVA) in 2021, will be a major driver of future economic growth. In absolute terms, construction and real estate, transportation and storage, and technology and communication services will drive the sector until 2030.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below displays the adjusted forecasts of the percentage growth for the categories mentioned to highlight the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

Spirits are anticipated to boost further dynamic growth over the forecast period

- The alcoholic drinks industry in Turkey is witnessing dynamic growth with a positive performance recorded for both off-trade and on-trade channels, supported mainly by the diminishing effects of COVID-19. This performance is set to continue throughout the forecast period, with stronger growth on-trade than off-trade due to the continued recovery of this channel, partly due to the return of tourists to the country. According to Euromonitor’s Baseline scenario forecast, the alcoholic drinks industry in Turkey recorded 60.0% growth over 2019-2022.

- Spirits are set to maintain the most dynamic total volume CAGR over the forecast period, with premium products expected to become increasingly popular. Wealthier individuals will undoubtedly recover their spending confidence more rapidly, helping boost the growth of such products.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors mentioned in Turkey. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

The more premium categories in beauty and personal care such as fragrances and color cosmetics received the most severe hit

- Sales of some categories within beauty and personal care, such as color cosmetics, continue to suffer the economic fallout as a result of the virus outbreak. As many Turkish women have become accustomed to their natural hair color or not wearing nail polish during quarantine, for example, they continued focusing on how they feel rather than how they look through 2020/2021, causing a 7.0% decline in the industry over 2019-2022, based on Euromonitor's Baseline scenario forecast.

- Premium perfumes, which were driving value sales before COVID-19, fell sharply, with double-digit value and volume decreases, as many fragrance customers moved to mass products to save on less essential items during a time of heightened economic hardship.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

1,639

1,707

29.2

Home Care Packaging

1,236

1,289

6.7

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

14,602

15,208

2.59

Flexible Packaging

28,678

29,802

-0.16

Metal

4,329

4,574

1.49

Paper-based Containers

2,680

2,827

0.02

Glass

7,577

8,167

0.80

Liquid Cartons

3,397

3,581

0.00

Inflationary pressures push demand for added-value products and packaging

- Living costs will continue to rise due to inflationary pressures, ensuring that value for money is a crucial factor in purchase decisions. As a result, Turkish consumers are likely to gravitate toward products with increased efficacy, adaptability, and other added-value characteristics. Market innovation will be shaped by this, as well as the growing demand for more eco-friendly alternatives produced with natural ingredients.

- In response to consumers' rising demand for added value, Henkel partnered with Mondi, a global leader in packaging and paper, to launch a fully recyclable refill pouch for Pril. The two companies also collaborated on a packaging solution for Henkel's hand dishwashing products that allowed flexible pouches to be used to refill plastic bottles. The pack type is convenient and lighter to carry home. The pouch also completely empties thanks to its shape, leaving no residue.

- Furthermore, an expanding population, increasing urbanization, and growth in the number of households in the country, as well as increased consumer hygiene awareness in the aftermath of the COVID-19 pandemic, will all help the overall home care industry grow. As a result, HDPE bottle packing volumes are predicted to increase over the forecast period, with HDPE bottles being the most common pack type in both laundry and surface care. HDPE bottles offer high levels of chemical resistance, which prevents reactions with the pack type, as well as ensures a longer shelf life period for its contents without spoilage.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recover Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.