Overview

- Packaging Overview

-

2020 Total Packaging Market Size (million units):

151,454

2015-20 Total Packaging Historic CAGR:

0.9%

2021-25 Total Packaging Forecast CAGR:

-2.5%

Packaging Industry

2020 Market Size (million units)

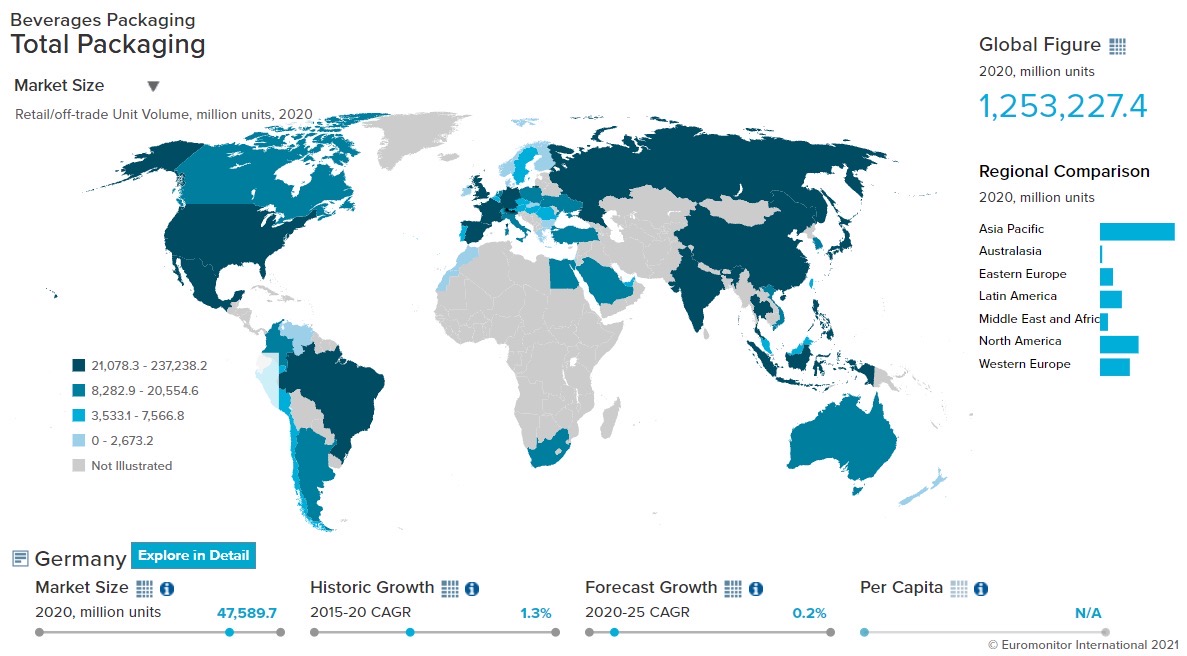

Beverages Packaging

47,127

Food Packaging

91,016

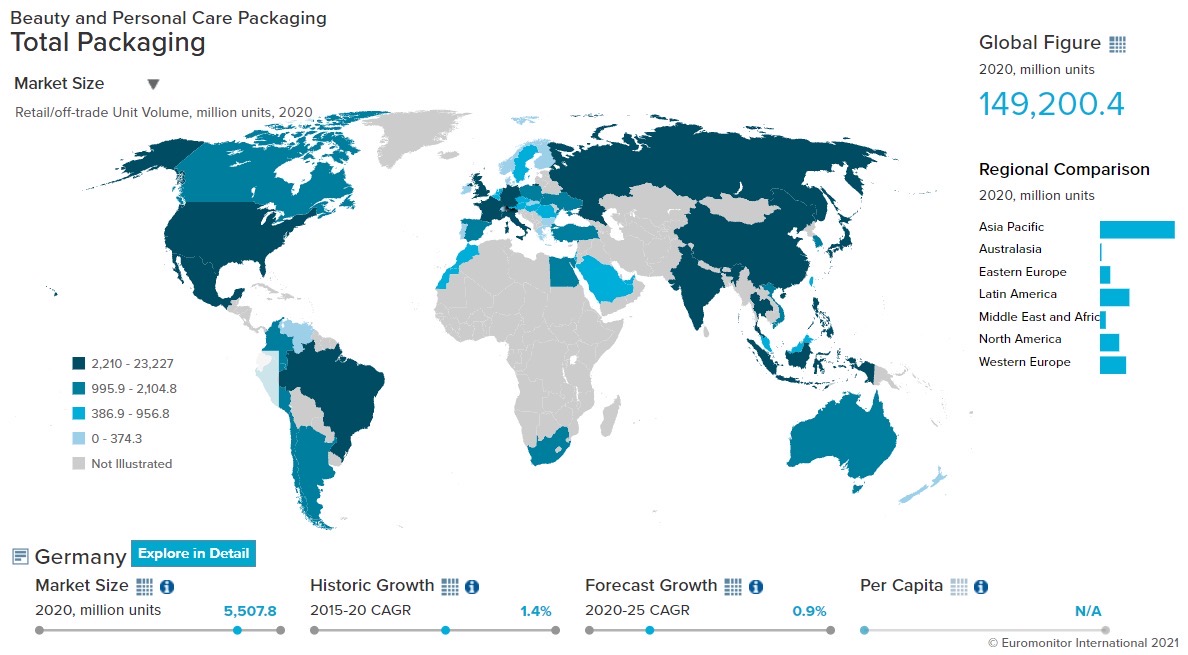

Beauty and Personal Care Packaging

5,508

Dog and Cat Food Packaging

5,224

Home Care Packaging

2,579

Packaging Type

2020 Market Size (million units)

Rigid Plastic

46,699

Flexible Packaging

50,923

Metal

9,482

Paper-based Containers

11,175

Glass

24,952

Liquid Cartons

8,013

- Key Trends

-

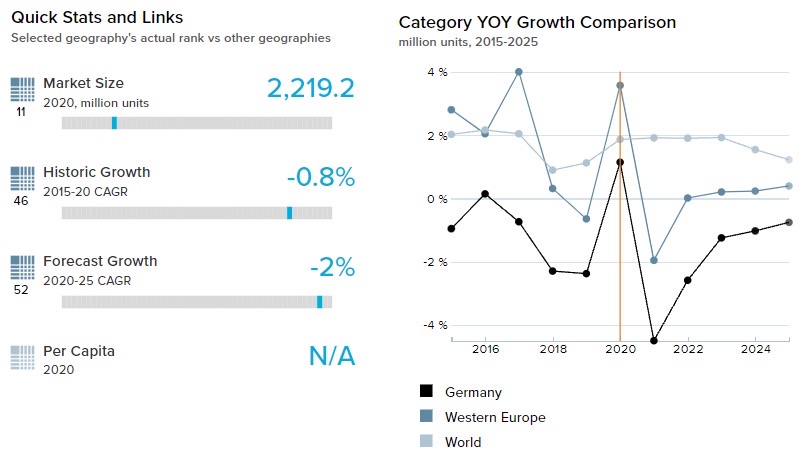

The war on sugar hit liquid cartons hard as consumers are increasingly concerned about the sugar content in soft drinks. Similarly, juices have also been struggling in recent years. As the majority of juice products are packaged in liquid cartons, the share of liquid cartons within the soft drinks market has been negatively affected. Within the juice category, the PET bottle is a popular choice for juices with a healthy and fresh image as consumers can see the product and can judge its freshness based on its appearance. However, there is growing resistance to plastic in general, and plastic bottles in particular.

The German home care industry witnessed robust growth in e-commerce during the pandemic. Packaging that offers more protection from damage or spillage became more appealing to manufacturers. In turn, plastic pouches saw a large increase in demand, not only due to the convenience aspect but also because of their flexibility and the ease of packaging them for shipping. These pouches have also been developed to a point where the exterior is extremely durable and difficult to puncture.

- Packaging Legislation

-

In November 2020, the German government approved the EU legislation banning a wide range of single-use plastic products alongside products made from oxo-degradable plastic. Since 2019, manufacturers have been required to register with a newly created national authority, the Zentrale Stelle, before launching any new packaging on the market. Packaging cannot be released without registration (filled packaging sold to consumers or distributors). The registered manufacturers will be published on the website of the Zentrale Stelle to ensure full transparency for all market participants. In addition to registering, manufacturers will also have to exchange packaging-related data to the Zentrale Stelle.

- Recycling and the Environment

-

Manufacturers are expected to invest heavily in the research and development of sustainable packaging, especially 100% recyclable plastic bottles. Belgian brewery Martens launched a new packaging with 100% recycled PET 500ml bottles.

Such initiatives are expected to increase the recycling rate from 55% at present to 75% by 2025. The demand for 100% recycled plastic bottles is set to increase as demand from the bottled water industry, carbonates, juices, and other beverages is expected to increase.

- Packaging Design and Labelling

-

Consumers are expected to become increasingly cautious regarding their diets and the food products they consume over 2021-25. The processed meat industry in Germany faced some scandals, such as the horsemeat scandal, which reduced consumer confidence in the processed meat industry. Now, to gain consumer confidence, processed meat manufacturers will have to reassure consumers with greater transparency. Companies need to be transparent about nutritional information and quality labels on large facings and with transparent plastic windows or plastic foil. Consumers are increasingly studying the labels on products before purchasing. This offers an opportunity for the packaging industry as the importance of transparent packaging and printing on the packaging has increased.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- In hot drinks, demand for larger pack sizes grew as consumers chose to stockpile products. Due to movement restrictions during the pandemic, consumers were almost entirely dependent on at-home caffeine consumption, which led to purchase larger pack sizes in folding cartons for their domestic consumption. Flexible plastic gained popularity as it is suitable for larger packs and is easy to carry, store, and deliver at the doorstep. As a result, flexible plastic grew at 2.0% by volume in hot drinks packaging in 2020.

- To avoid unnecessary travel outdoors, German consumers preferred to purchase bulk formats or multipacks of soft drink products in 2020. Consumers also moved towards non-returnable pack types as COVID-19 created hygiene concerns among consumers about returnable pack types, causing the volume of returnable to decline in 2020. As a result, PET bottles and flexible packaging grew by 3.5% and 0.8% by volume respectively during the year.

- Trends

-

- The new trend “drink less but drink better” and changes in consumption occasions has led to a preference for smaller pack sizes. Smaller pack sizes also help in controlling alcohol intake. This impact is prominent in wine, with branded players and private labels launching smaller bottle sizes such as 250ml and 330ml for their ranges. Smaller bottles also help consumers experiment with new wines without investing in a full bottle. As a result, in wine and many other alcoholic drinks categories, large formats such as 1,500ml declined in 2020.

- Composite containers are increasingly becoming popular as they offer the right mix of constituent materials that helps them remain resistant to corrosion. They can also withstand damage from weather and harsh chemicals. These containers are also lighter in weight, compared to most woods and metals, making them highly suitable for most hot drink categories, such as flavored powder drinks and instant coffee.

- Outlook

-

- Hot drinks packaging is expected to follow the trend of premiumization and value growth as the hot drinks market in Germany matures. The pack types that add a more luxurious feel to a product or has value-added benefit in the packaging itself, such as biodegradable pack types, are expected to gain popularity over 2021-25. Since consumers have increasingly started to prefer environmentally sustainable pack types, most players will struggle to offer sustainable options at an affordable price without major quality sacrifice going forward.

- Metal beverage cans, already a popular pack type in energy drinks and carbonates, are also expected to be adopted by many bottled water players. Metal beverage cans helped manufacturers of bottled water meet their need for sustainable packaging by offering lightweight, durable packaging that fits in well with on-the-go consumption. Metal beverage cans are expected to grow at 2.5% CAGR by volume over 2021-25 and become more popular as the best medium for smaller pack sizes and on-the-go consumption.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Flexible packaging is dominating dog and cat food packaging in Germany. Due to increasing environmental concerns and sustainability issues, manufacturers stopped using two-layered pack types: primary packaging (one for outer packaging) and secondary packaging (one for inner packaging). Instead, pet food is packed in new and innovative pack formats such as packs with zipping/press closures, stand-up pouches, etc. These packs are mostly made from flexible packaging. Thus, flexible packaging grew by 3.3% by volume in 2020.

- Pet owners are closely monitoring portion size and dietary intake in the wake of rising obesity among pets. Thus, pet owners are preferring smaller pack sizes, particularly those under 100g in cat food and 150g in dog food. This phenomenon can also be attributed to the growing popularity of smaller dog breeds, as they are easy to handle and look after. The rise of smaller packs such as single-serve packs, stand-up pouches, and flexible pouches that are easy to transport, store, and convenient to use is a positive trend as they are usually made from flexible packaging

- Trends

-

- Products with natural ingredients and clean labels with no additives and preservatives are finding wider acceptance. As consumers become more aware of their pet’s health needs, they pay more attention to such details. Thus, grain-free products or those with a low proportion of grains are set to benefit from growing demand, alongside products with unmixed single meat sources, such as horses or deer. Players are launching new pack types such as transparent see-through packs that allow the customers to have a look at the food before purchasing it . As a result, pack types such as flexible plastic have benefitted from this trend.

- The rise of e-commerce is impacting pack sizes in the dog and cat food industry. Consumers who order pet food online may either choose to purchase a larger quantity of smaller portions or a single large pack. This trend reduced demand for mid-range pack sizes such as 400g and 800g which are common in retail outlets. The online channel also directly benefited from companies such as Zooplus, which gained a stronger presence in dog food and pet care overall, thanks to a focus on both competitively priced private label products and premium brands.

- Outlook

-

- Increasing environmental concerns are expected to boost paper-based containers that currently remain a niche when compared to other types of packaging. Awareness of paper-based containers has been driven by launches such as the dog food brand Good from Interquell, which is best known for its Happy Cat and Happy Dog brands. Good is marketed as a sustainable brand due to being carbon neutral and packaged in reusable cartons, which Interquell claims to be a first in dog food. To reduce waste, most manufacturers already refrained from using secondary packaging and this trend is expected to continue.

- Private labels such as Carry petfood and MERA pet food are expected to grow over 2021-25 as they offer a wide assortment of products across all price bands, including economy and premium ranges. Private labels are expected to offer more options in the organic food category. They are increasing their online presence. Thus, private labels are expected to give tough competition to existing brands.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

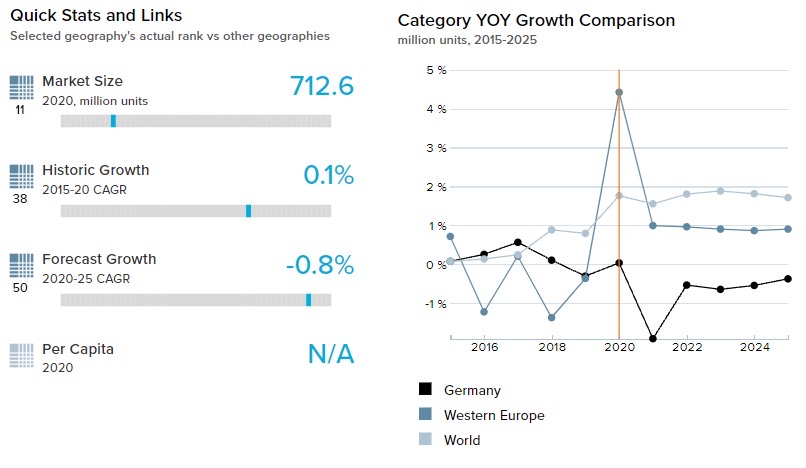

- As demand for environmentally-friendly packaging materials is rising, companies are focusing on the innovation and development of sustainable packaging. Concern for the environment is increasingly characterized by a shift towards lighter materials, recyclable packaging, refill packs, and solid color cosmetic products that require minimal packaging. The movement of refillable packs is gaining momentum in Germany wherein companies have installed dispensing machines at the point of sale to refill packs. Returnable refill packs are mostly made from stand-up pouches or PET bottles. As a result, stand-up pouches and PET bottles grew by 7.8% and 4.7% by volume respectively.

- Trends

-

- With consumers looking for detailed information on product ingredients and packaging, aspects such as sustainability, waste reduction, and recyclability are increasingly influencing purchasing decisions. The German packaging company FKuR produces “natural” plastic – that is, Bio-Flex and Bio grade, which are biodegradable plastics made from renewable raw materials that can be processed on standard production lines. The natural basis of Bio-Flex is either corn, castor oil, or sugar cane. Biograd is manufactured using cellulose. This type of packaging is mostly used in cosmetic products, and color cosmetics.

- The trends towards naturalness and organic products will continue, particularly in baby and child-specific products. Parents are seeking products that boast organic, cruelty-free, vegan-friendly, and natural ingredients. Brands that contribute to the progress of these trends include Sebamed, Eucerin, La Roche-Posay, Lavera, and Weleda.

- Outlook

-

- Germans are expected to become increasingly concerned about the environmental impact of packaging. In response, manufacturers and brand owners will invest more heavily in developing ecologically sound packaging solutions, with bioplastic expected to gain a lot of attention. Bioplastic is expected to replace flexible plastic such as plastic pouches and stand-up pouches. This trend is likely to be more visible in liquid soap, hand sanitizers, and shampoo packaging. A sharp rise is expected in lightweight packaging formats in bath and shower products. More retailers are likely to follow the example of Lush by encouraging consumers to bring bags to pack their purchases.

- Travel pack sizes are likely to benefit from a return to normalcy by the end of 2021. After getting vaccinated, German consumers are expected to resume traveling for business and personal purposes. This is expected to boost travel pack sizes in categories such as body wash/shower gel, standard shampoos, conditioners and treatments, deodorants, toothpaste, face masks, and adult sun care over 2021-25.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- Home care sales in Germany grew sharply in 2020 as a result of increased home seclusion during the pandemic. This is because the pandemic led to an increase in usage of daily essential items such as kitchen cleaners and dishwashing products. Furthermore, consumers preferred larger pack sizes to avoid multiple ordering via e-commerce or frequent shopping trips during the pandemic. Large pack sizes of home care products mostly come in flexible packaging. As a result, flexible packaging grew at 4.5% by volume in 2020.

- Trends

-

- Due to increased awareness of hygiene, surface care saw dynamic growth due to the greater frequency of usage of these products. Categories such as multipurpose cleaners gained traction in 2020 as consumers preferred using a single product rather than purchasing various cleaners to keep their surroundings clean. HDPE and PET bottles are attractive pack types for multipurpose and surface cleaners. The relatively sturdier packaging and high levels of recyclability make these ideal pack types for brands to achieve their sustainability targets.

- Consumer apprehension about the spread of the virus from different surfaces, including clothes, led to washing clothes more regularly than usual. Larger pack sizes were preferred by consumers for liquid detergents and liquid fabric softeners during the pandemic so they would not run out of stock. However, folding cartons and HDPE bottles are the dominant pack types for laundry aids, with consumers preferring compact pack sizes as they are more concentrated, with 500g the main pack size. Folding cartons usually come with secondary flexible packaging for better protection of the products and are often used as refill packs for other containers in the case of powder detergents.

- There are innovations in packaging materials within home care with increasing usage of recycled plastics or biodegradable material instead of non-recyclable plastics. Seventh Generation is a prime example of a home care manufacturer focusing on this aspect, with its new caps being made from 100% recycled plastic.

- Outlook

-

- German consumers tend to be environmentally conscious and have a strong habit of recycling. This is forcing producers to shift towards sustainable packaging and come up with innovations in terms of recyclable packaging. Henkel, for example, aims to use 100% recyclable or reusable packaging by 2025 and reduce fossil-based virgin plastic by 50%. Procter & Gamble also aims to use 100% recyclable plastic by 2030. Moreover, German consumers are increasingly seeking more detailed information on the ingredients of a product on their packaging. Aspects such as waste reduction and recyclability will be increasingly influencing purchasing decisions over 2021-25.

- The desire to maintain high levels of health and hygiene will remain strong among consumers. This trend will boost the volume growth of categories such as laundry care, toilet care, and dishwashing over 2021-25. This will, in turn, boost the volume of HDPE bottles, PET bottles, and folding carton, which are the main pack types for these categories.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- Aluminum/plastic pouches are gaining traction in categories such as prepared baby food while giving tough competition to glass jars and thin wall plastic containers. Stand-up pouches offer increased convenience to parents with their easy to reseal options, as they come with a plastic screw closure. Stand-up pouches take up less shelf space than rigid containers or other packaging options while also being visually appealing and cost-effective. Some start-ups have launched new products in aluminum/plastic pouches, which, in turn, led more established manufacturers of baby food to follow suit.

- Flexible plastic is the most used pack type for sugar confectionery followed by flexible paper and flexible aluminum/paper. Flexible plastic also remains the most popular pack type for boiled sweets, licorice, pastilles, gums, jellies, and chews. Major brands sell smaller units of sugar confectionery in secondary flexible packaging. Flexible plastic will remain dominant in confectionery being widely used in gum, sugar confectionery, and chocolate confectionery. Flexible plastic will benefit from being used for bite-sized products that are appealing to health-conscious consumers with a focus on portion control.

- Trends

-

- Folding cartons are gaining market share owing to recyclability whereas metal food cans are to gain market share owing to affordability. Folding cartons, which is the leading primary pack type in ready meals, continued to gain in 2020. This pack type is commonly used in refrigerated ready meals and frozen ready meals. A shift away from plastic packaging among manufacturers is expected to further benefit folding cartons. Shelf-stable ready meals will continue to face competition from other types in the category that are perceived as healthier and more convenient, including prepared salads, frozen pizza, and refrigerated ready meals. These are mostly packaged in rigid plastic, flexible plastic, or folding cartons.

- Aluminum/plastic pouches are gaining traction in categories such as prepared baby food while giving tough competition to glass jars and thin wall plastic containers. Stand-up pouches offer increased convenience to parents with their easy reseal options, as they come with a plastic screw closure. Aluminum/plastic pouches are expected to grow strongly at 3.4% CAGR by volume over 2021-25, benefiting from being a practical alternative that is easy to carry and is not fragile like glass. This is especially true in the case of on-the-go consumption, where parents tend to favor grab-and-go options that allow them to feed their babies quickly and with minimal mess.

- Outlook

-

- Increasing health awareness around the consumption of confectionery will impact sales over 2021-25. Brands are expected to invest in research and development to understand the changing consumer landscape and innovate in terms of healthier offerings and attractive packaging to appeal to different consumer segments. As German consumers are generally highly concerned about the environmental impact of packaging waste, confectionery players are expected to offer recyclable packaging. This trend is likely to be prominent in chocolate confectionery areas such as tablets, chocolate pouches, and bags and boxed assortments. The plastic content used in packaging will also continue to decrease, with plastic typically being replaced with paper pack types such as folding cartons or flexible paper.

- Following the outbreak of COVID-19, many areas that saw a volume increase in 2020, including milk alternatives, shelf-stable milk, yogurt, and cow’s milk, will see stifled growth in 2021 as home seclusion ended. However, changes in consumer behavior will lead to on-the-go consumption becoming popular once more, aiding sales of smaller pack sizes. With health-conscious behavior still in place following the pandemic, smaller pack sizes are also ideal for consumers looking at limited consumption and regulate their sugar intake. In addition, the popularity of smaller pack sizes will also be driven by the ongoing decline of household sizes in Germany, as well as the aging population.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Germany

-

Proof of vaccination status is required upon entry to the country

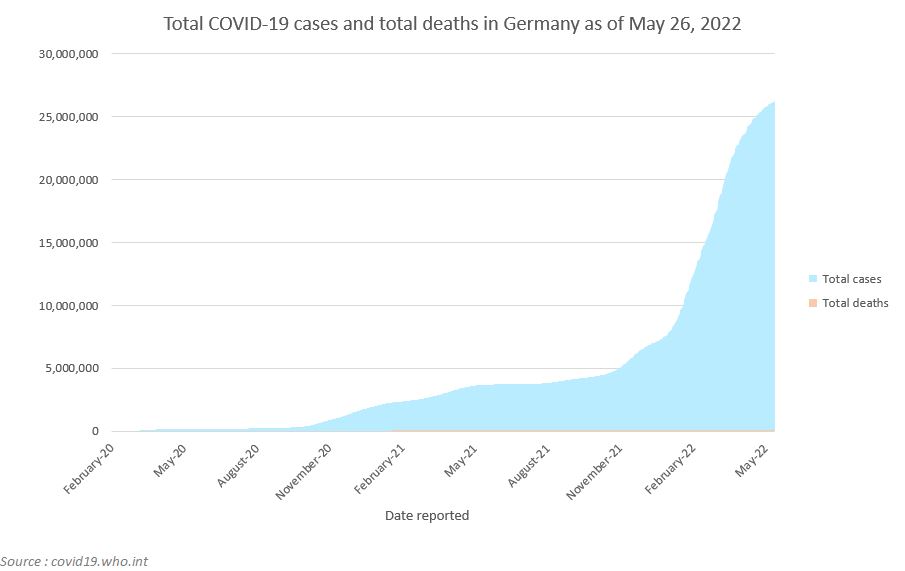

- According to the World Health Organization (WHO), Germany had 26,198,811 COVID-19 cases, with 138,779 deaths and 315,016 cases per million inhabitants as of May 2022.

- EU-wide restrictions remain in place in Germany. Only fully vaccinated people are allowed to enter from any other country for any reason (including visits and tourism). The vaccination must include at least two doses of one of the vaccinations authorized by the European Union.

- Every person above the age of 12 who enters Germany after March 3, 2022, will be required to show documentation of their COVID-19 status, including a negative test result, proof of recovery, or vaccination.

- According to the WHO, as of May 15, 179,411,634 total vaccines have been administered in the country, corresponding to 77.5 fully vaccinated persons per 100 people.

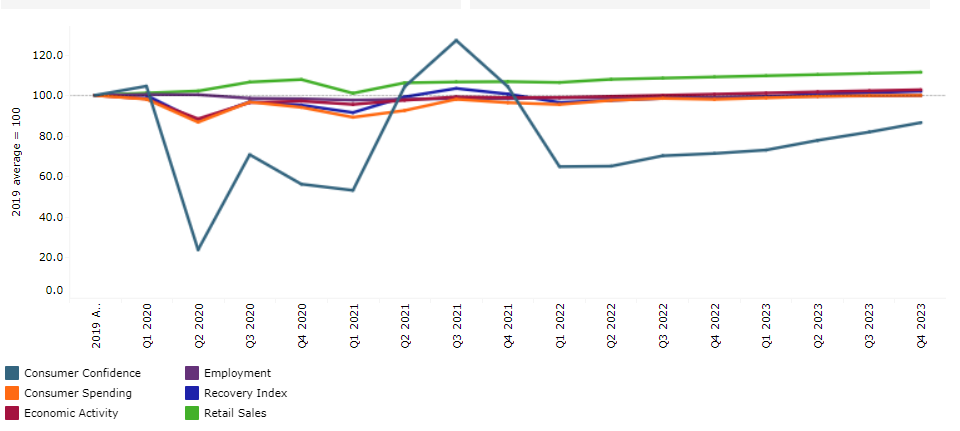

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Germany

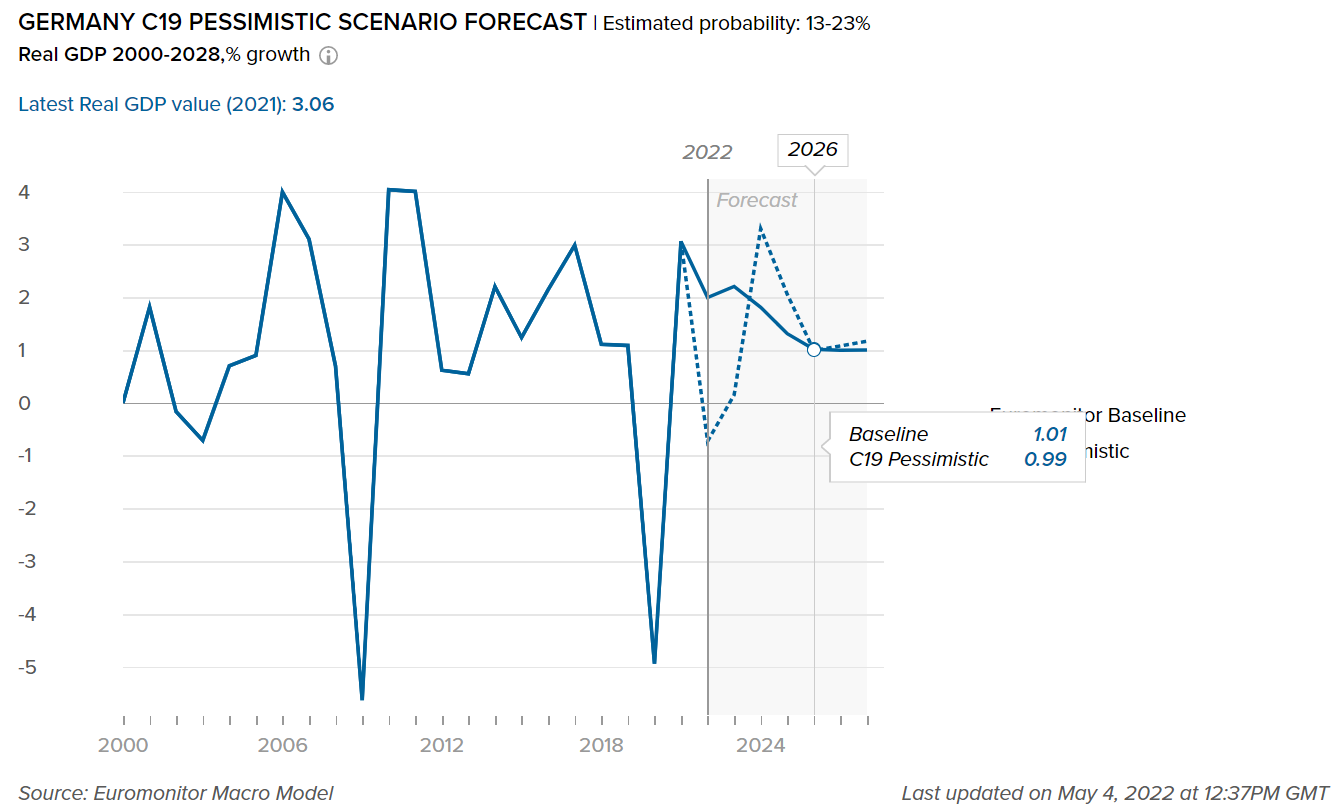

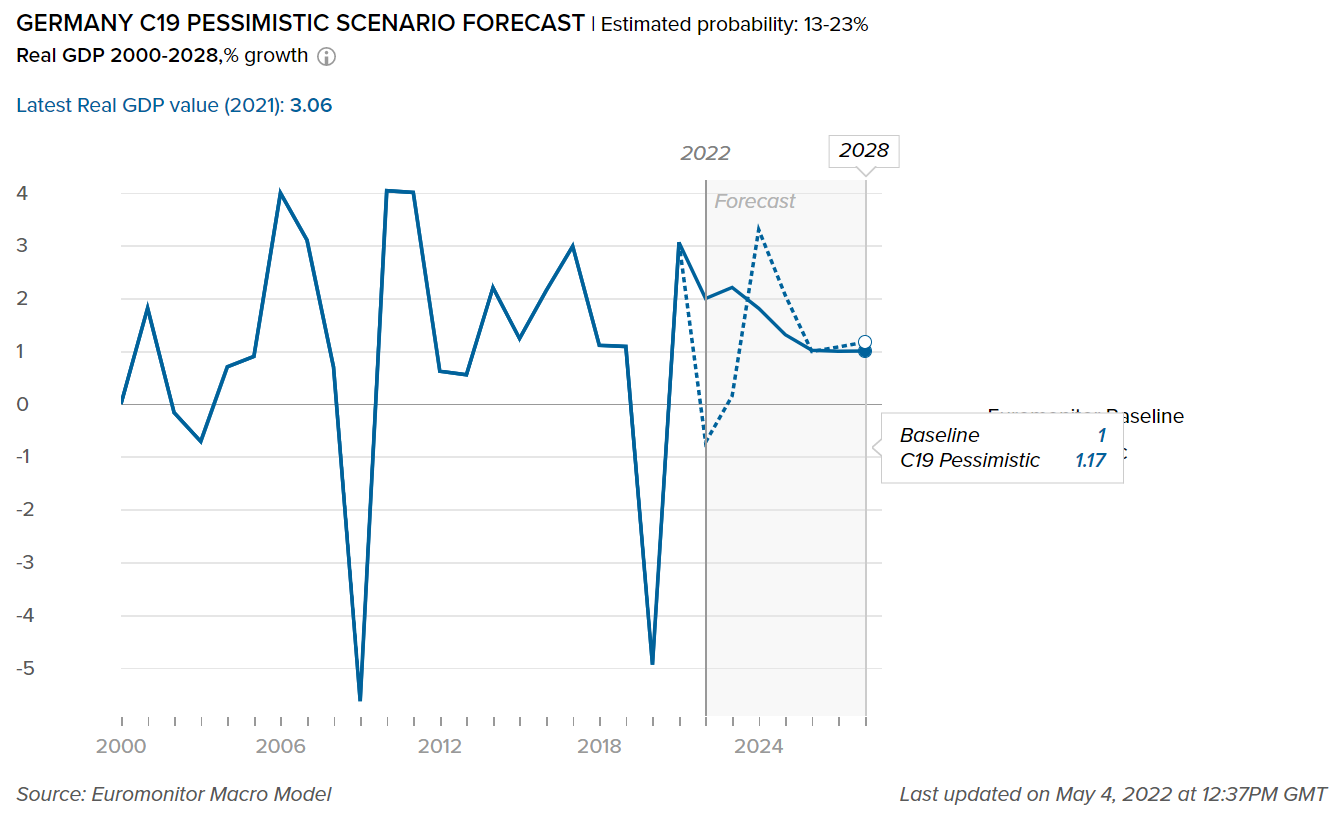

- Impact on GDP

-

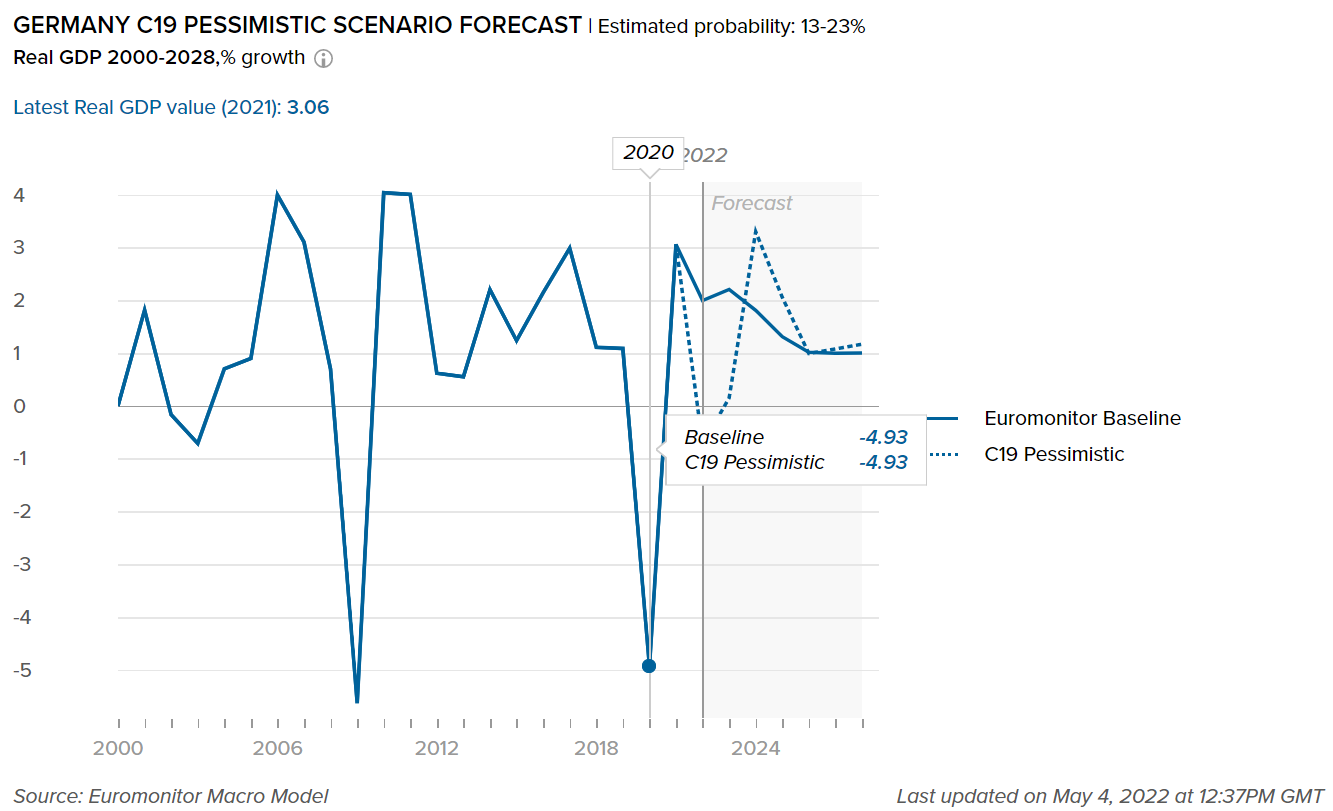

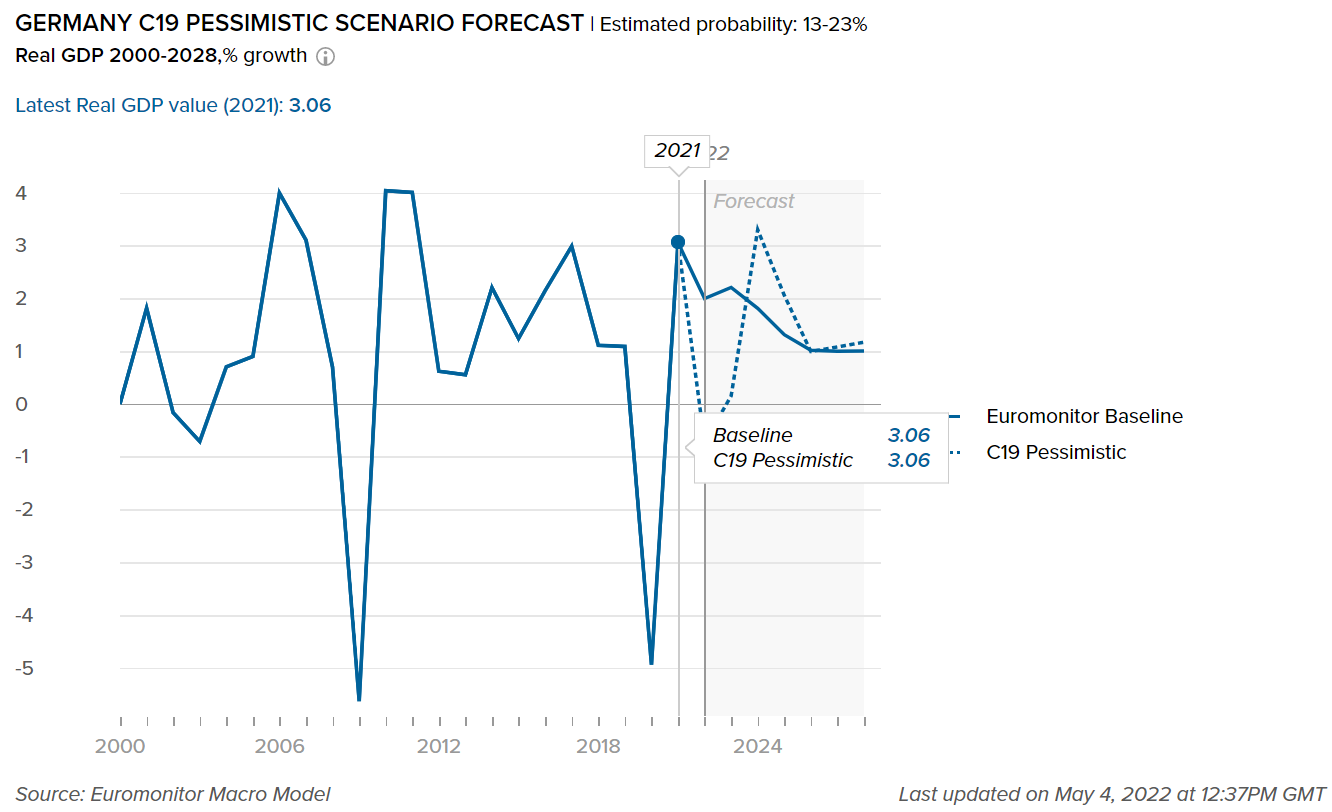

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in Germany. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Reviving exports and rising investment to spur near-term economic growth

- Following a 4.9% contraction in 2020 due to the COVID-19 pandemic shock, Germany's real GDP increased by 3.0% in 2021. The recovery was fueled by strong economic performance in practically every sector, including business services, trade, transportation, and manufacturing. The government's record fiscal support, which included a EUR130 billion economic stimulus plan and a EUR1.7 trillion financial assistance package for enterprises, helped cushion the economic shock and speed up recovery.

- The impact of the pandemic on the labor market was relatively low due to an effective short-time working plan. In 2021, Germany's unemployment rate was 3.5%, less than half of the regional average in Western Europe.

- Given the manufacturing and construction sectors' significant backlogs, the predicted easing of supply bottlenecks in the second half of 2022 is expected to translate into solid growth in exports and investment during the year. The Recovery and Resilience Plan's execution is also expected to boost investment in green transition and digital transformation, as well as assist future economic growth.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below shows the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

Beauty and personal care products are anticipated to see a much slower recovery

- Over 2019-2022, one of the industries in Germany that was negatively affected by the pandemic was beauty and personal care, which saw overall single-digit reductions of 3.7%, based on Euromonitor’s Baseline scenario forecast. COVID-19 had a significant negative impact on color cosmetics, fragrances, and sun care, with all three categories experiencing the greatest decline in value sales; struck predominantly by lockdowns, store closures, home seclusion, and social isolation.

- Furthermore, general apprehension will persist in terms of discretionary purchases of products such as fragrances and color cosmetics, meaning value sales are unlikely to fully recover to pre-pandemic levels by the end of the forecast period.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors covered in Germany. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Essential categories outperformed growth potential supported by growing health awareness

- The COVID-19 pandemic benefited home care, as consumers focused more on intense cleaning routines in the house as part of the preventive health movement. Even before 2020, German consumers prioritized hygiene, and this trend accelerated since the outbreak. The increased use of many cleaning products resulted in sales increases in several categories, including surface care (home care disinfectants, multi-purpose cleaners, and kitchen cleaners), dishwashing, and toilet rim blocks. Home care outperformed its growth potential over 2019-2022 recording 8.1% growth based on Euromonitor’s Baseline scenario forecast, as opposed to a projected 6.7% based on the C-19 Pessimistic scenario forecast.

- As a result of the COVID-19 crisis, the rising popularity of plant-based and vegan goods such as milk alternatives and meat substitutes intensified between 2019 and 2022. Consumers have been experimenting with cooking at home during the COVID-19 shutdown, focusing on sustainable alternatives to meat and dairy. Veganism's rising popularity coincides with the rise of health and wellness trends fueled by the COVID-19 outbreak, which focused attention on health and immunity. The pandemic increased consumer awareness of the importance of nutrition in maintaining a healthy body and immune system.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

5,525

5,613

0.3%

Home Care Packaging

2,965

3,020

12.8%

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

47,543

47,255

0.13%

Flexible Packaging

53,828

52,883

0.53%

Metal

9,998

10,083

0.02%

Paper-based Containers

11,929

11,772

0.16%

Glass

25,023

24,896

-0.01%

Liquid Cartons

8,263

8,053

0.00%

Sustainability and health awareness are key trends impacting the packaging landscape in Germany

- As a result of the public health emergency caused by the COVID-19 pandemic, consumer awareness of cleanliness and sanitization issues increased. Consequently, packing unit volumes of the major pack type, HDPE bottles, used in most home care categories such as kitchen cleaners or multi-purpose cleaners increased significantly in 2020 and 2021, with further dynamic performances expected in 2022.

- German consumers are known for being environmentally conscious and recycling enthusiasts. Plastic waste recycling is becoming more popular in the country, with consumers eager to use recyclable plastic. This is prompting manufacturers to change to sustainable packaging and develop new recyclable packaging ideas. Henkel, for example, announced ambitions to utilize 100% recyclable or reusable packaging by 2025, as well as a 50% reduction in fossil-based virgin plastic. By 2030, Procter & Gamble intends to use 100% recyclable plastic.

- As in other categories across packaged food, ready meals manufacturers are increasingly seeking to reduce their use of plastic-based packaging as a primary pack type and replacing plastic with other packaging materials. Folding cartons, by far the leading primary pack type in ready meals, continued to benefit in 2020/2021, with this pack type commonly being used in chilled ready meals and frozen ready meals. In addition to being easily recyclable, folding cartons also offer cost-effective packaging for manufacturers.

- Similarly, retailer Schwarz Gruppe, operator of the Kaufland and Lidl chains, set a target of cutting its use of plastic packaging by 20% by 2025 through the Reset Plastic program, while also aiming to use 100% recyclable plastic packaging. Discounter chain Aldi also plans to reduce the use of all packaging materials by 30% by 2025.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery index

-

Recovery Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.