Overview

- Packaging Overview

-

2020 Total Packaging Market Size (million units):

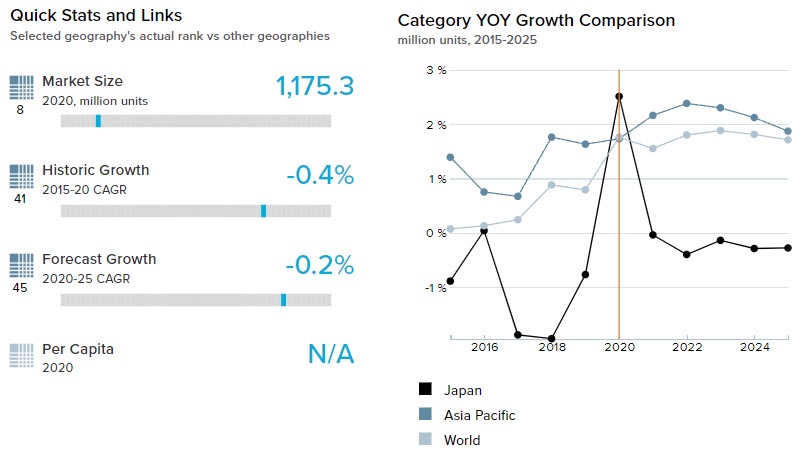

220,444

2015-20 Total Packaging Historic CAGR:

0.7%

2021-25 Total Packaging Forecast CAGR:

-1.3%

Packaging Industry

2020 Market Size (million units)

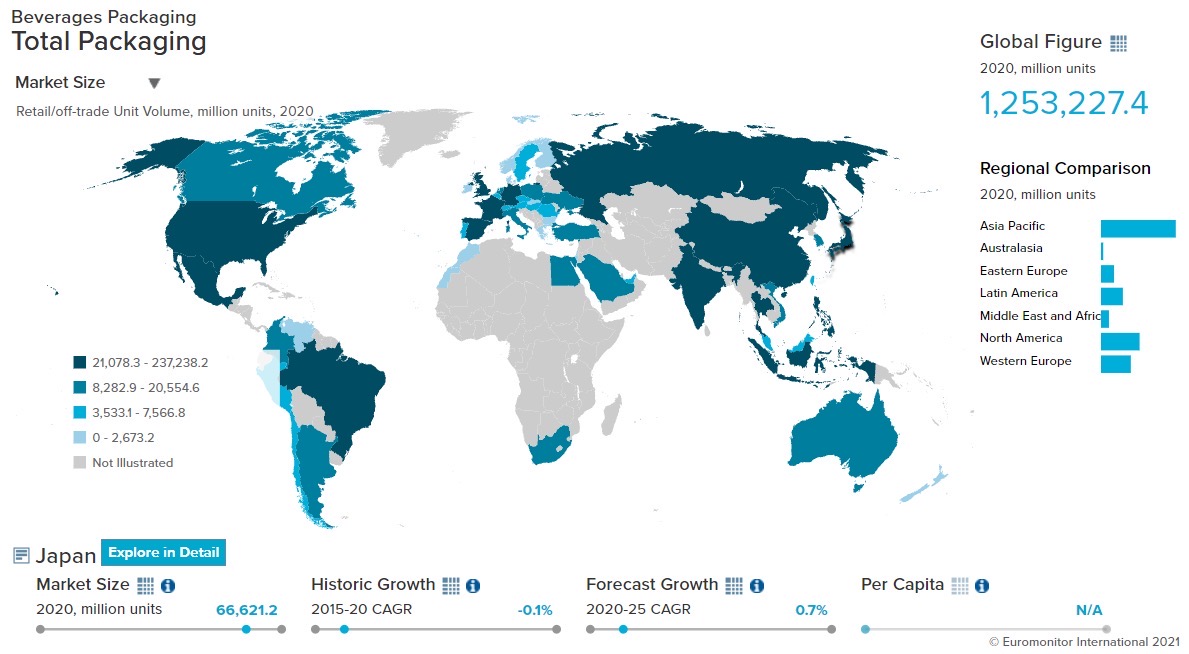

Beverages Packaging

66,408

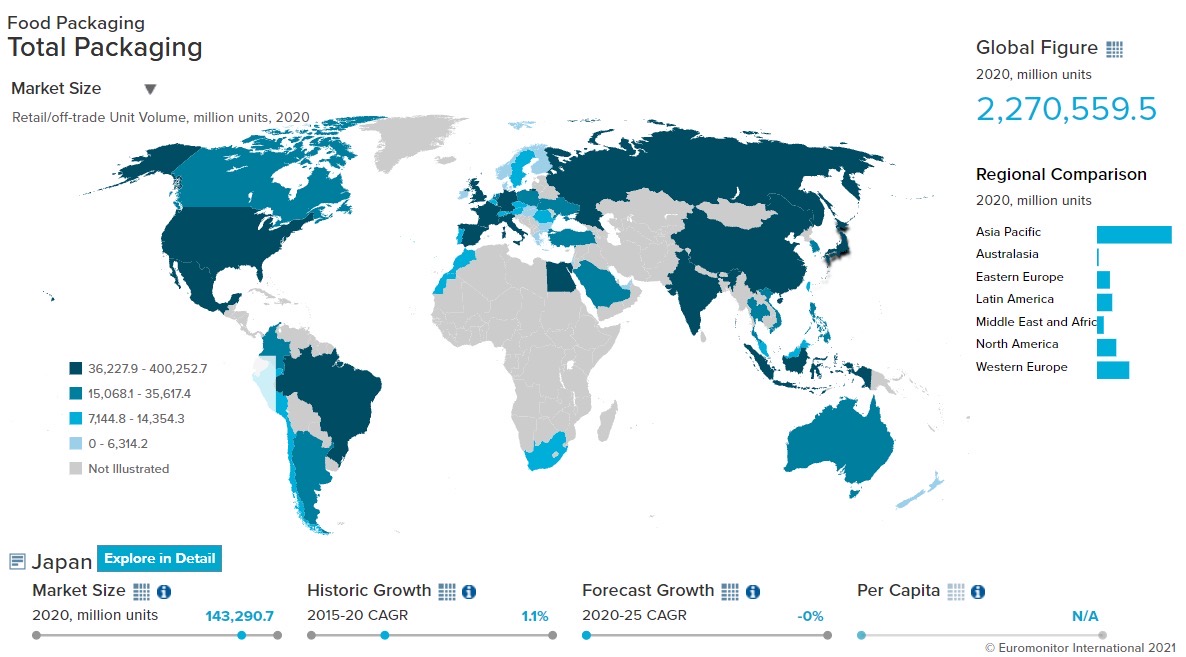

Food Packaging

143,291

Beauty and Personal Care Packaging

4,714

Dog and Cat Food Packaging

2,853

Home Care Packaging

3,179

Packaging Type

2020 Market Size (million units)

Rigid Plastic

62,843

Flexible Packaging

85,345

Metal

31,197

Paper-based Containers

20,315

Glass

8,773

Liquid Cartons

11,886

- Key Trends

-

Japan is one of the countries where the average age of the population is the highest in the world and with falling birth rates and increased longevity, this trend is expected to continue. As a result, smaller pack sizes are expected to grow as they provide convenience, portability, and are perfectly suitable for the busy lifestyles of the Japanese. Manufacturers are expected to continue to support this trend by adopting smaller pack sizes for both new product launches and established product lines. It is also expected that when faced with rising costs, many companies will choose to reduce pack sizes rather than increase unit prices to avoid alienating price-sensitive consumers.

- Packaging Legislation

-

The Containers and Packaging Recycling Act (Ordinance of the Ministry of the Environment) was enacted in June 1995 will continue to be reviewed every five years to help develop the best practices in terms of environmental behavior and choices. In 2019, the law was amended to make it compulsory for all retailers to charge for single-use plastic bags from July 2020, thereby creating awareness about single-use plastic and asking consumers to shift to other environmentally friendly pack types and opt for refill packs.

- Recycling and the Environment

-

Inspired by the concept of “3R + Renewable,” the Japanese Government came up with a “Resource Circulation Strategy for Plastics” in May 2019. As per this strategy, among many targets, they aim to reuse and recycle 60% of plastic containers and packaging by 2030. As a result, in September 2020, the two major home care manufacturers, Kao and Lion announced plans to collaborate on recycling flexible packaging. Even various confectionary players such as Mikakuto and Fujiya, decided to change the long-time selling sweets’ exterior packaging from plastic to paper.

- Packaging Design and Labelling

-

The Food Labelling Act that came into force in April 2015 introduced mandatory nutritional labelling for pre-packaged processed food sold in Japan, which was previously a voluntary requirement. The act gave a 5-year transitional period which ended in 2020. Now all products must display the energy, protein, fat, carbohydrate, and sodium levels on the packaging, allergy labelling (for packaged food), and the country of origin (for processed food).

Click here for further detailed macroconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Due to the COVID-19 pandemic, off-trade sales of tea and coffee grew in 2020 as hotels, restaurants, and Cafés were closed and people were afraid to go out and drink. Pack types like flexible aluminum, plastic, and stand-up pouches, which provide high levels of protection and extended shelf life, saw a rise in sales within hot drinks, with a growth of 4.9% and 7.3% respectively in volume terms in 2020.

- With the increasing popularity of ienomi culture (i.e., consuming drinks at home), demand for portable and light in weight beers and RTDs has increased, especially for 350ml metal beverage cans. This resulted in the growth of metal beverage cans at 3.2% in 2020 in volume terms, which consequently decreased the demand for flexible packaging as it is not a preferred type of packaging for beers and RTDs. Therefore, flexible packaging grew at a mere 0.2% in volume terms in 2020.

- Trends

-

- The closure of gyms and other sports facilities and increasing trends of virtual meetings and parties decreased on-the-go consumption. As a result, smaller pack types such as 120ml and 240ml, which saw double-digit growth in 2019 due to convenience and portability suffered in 2020, with sales plummeting by 56.0% and 42.0% respectively in volume terms for Asian specialty drinks.

- Fresh ground coffee pods have seen a boost in sales as work from home arrangements persist and customers are looking for high-quality at-home solutions. In fresh coffee pods, 110g folding cartons remained the most popular pack type and 100g folding cartons showed the fastest growth, though from a small base, and this trend is expected to sustain over the short run as COVID-19 cases are on the rise.

- Outlook

-

- As vaccination rates are expected to rise, resulting in an easing of restrictions, more consumers will return to offices as part of their work routines. Due to this, the retail unit volume is expected to decline over 2021-25 as on-the-go consumption will increase. As a result, smaller pack types that are easy to store like the 150g folding carton will take the largest hit and are expected to decrease at a CAGR of 11.3% in volume terms in hot drinks over 2021-25.

- Despite the return of plastic packaging during the pandemic, sustainability and environmental issues will continue to impact consumer purchasing behavior. Therefore, brands in coffee and tea alike are anticipated to focus heavily on paper-based packaging formats and recyclable materials over 2021-25. Brands such as Nespresso and Dolce Gusto launched recycling initiatives for their coffee pods in 2019. In addition, these brands have also taken steps in the development of paper-based coffee pods in a bid to reduce the use of aluminum and plastic in their products. As a result, the paper-based composite container is expected to grow at a CAGR of 8.0% over 2021-25.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Pet humanization is creating demand for products that are perceived to be fresher and more nutritious and manufacturers are using packaging to attract customers. As a result, there is a shift from metal food cans to flexible packaging, as it displays high graphic images and contents and is suitable for transportation. Flexible packaging grew at 6.4% in volume terms in 2020.

- Trends

-

- Snack products are gaining popularity in the cat and dog food segment due to the pet humanization trend as people spent more time at home with their pets, resulting in a better bond between them. This led to the increase in the sales of individual packaging as this type of packaging is perfect for snacks that are consumed at one go. As a result, 30g and 50g packaging grew 22.1% and 29.0% respectively in volume terms in 2020 while larger packs like 400g grew by only 2.3%.

- The development of products containing natural ingredients represented an increasingly prominent trend in 2020. Unicharm launched a new line of wet dog foods, made from 100% domestically produced chicken and free from artificial additives, under the Grand Deli brand. Plastic pouches were used as they are believed to keep ingredients fresh and extend the product’s shelf-life. Plastic pouches grew 17.4% in volume terms in 2020.

- There is an increasing trend of keeping smaller dogs because of the smaller average house size and the convenience it offers in terms of maintenance as smaller breeds require less food and are easier to manage vis-à-vis their larger counterparts. Thus, many manufacturers are capitalizing on this trend; for instance, Nisshin Pet Food Ltd launched Petitinu Motto, a gourmet food for small-sized breeds.

- Outlook

-

- The trend of keeping larger dogs is on the decline and this trend is expected to continue over 2021-25. This is due to the hectic lifestyles of consumers and the aging population in Japan, both of which limit the time and energy people have to take care of larger dogs. As a result, the smaller packaging trend is set to become increasingly influential. The 25g and 50g packs are expected to grow at a CAGR of 10.1% and 8.7% respectively in volume terms while larger packs like 1kg and 2kg will decline at a CAGR of 0.8% and 4.6% respectively in volume terms over 2021-25.

- Sustainable packaging and natural products are very likely to remain longer-term trends. Nippon Pet Food, a domestic player, is targeting the natural trend with its Combo Pure line of dry dog food, which helps them to have a natural positioning. Also, they are trying to react to rising environmental awareness by utilizing sustainable packaging solutions.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- COVID-19 has negatively affected all the subcategories of beauty and personal care like sun care and skincare among others with the exception of bath and shower products as consumers increased their focus on hygiene. As a result, the main pack types of bath and shower products are plastic pouches and HDPE bottles that showed strong growth of 64.1% and 29.8% in volume terms in 2020.

- Trends

-

- Consumers are reducing their spending on non-essential items, such as those in color cosmetics and fragrances as the country’s economy contracts due to measures taken to contain the COVID-19 virus. As a result, main pack types like rigid plastic in color cosmetics and glass bottles in fragrances showed a negative volume growth of 27.2% and 17.9% respectively in 2020. However, with the expected economic recovery over 2021-25, these pack types are expected to grow at a CAGR of 5.2% and 5.7% in terms of volume over the same period.

- The COVID-19 pandemic increased the focus on hygiene products along with a significant number of consumers working from home which led to the increased usage of bath and shower products. This led to an increase in sales of medium to large packs like 250ml and 450ml growing 33.3% and 52.6% respectively in volume terms in 2020.

- Outlook

-

- Sun care and skincare are expected to revert to their historical growth trajectories over 2021-25 as the restrictions due to the pandemic are expected to ease. Most of the increase will be seen in their main pack type, rigid plastic, which is expected to grow at a CAGR of 2.9% and 5.9% in skincare and sun care respectively in volume terms over 2021-25.

- The development in beauty and personal care packaging in Japan will increasingly focus on sustainability over the forecast period. Shiseido aims to promote and raise environmental awareness through technology and its continued collaborations outside of the company, and other players are likely to take note and follow suit.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- COVID-19 forced people to not only work but also spend more time at home. As a result, there has been an increase in the utilization of kitchens which has consequently driven up the requirement for more cleaning products such as surface cleaners. This led to a boost in sales of plastic pouches and HDPE bottles, the main pack types of surface care, which grew 15.1% and 12.7% respectively in volume terms in 2020.

- Trends

-

- As the threat of the pandemic persists, a large proportion of consumers have been prioritizing cost-saving measures in addition to looking to maintain high levels of personal hygiene. This trend is expected to gain ground as it encouraged leading players to start offering combo-packs or multipacks of refill pouches that allowed consumers to both stockpile and access products at a low per-unit cost. This trend is opposite to the one that prevailed before the pandemic when people preferred specific purpose products instead of multi-purpose ones.

- Rising environmental concerns among consumers in Japan have led to increasing demand for water-soluble packaging in the detergent segment of the Japanese market. Water-soluble packaging products, such as films, bags, and pouches are a type of packaging made from biodegradable materials that dissolve in water, leaving behind a harmless and non-toxic aqueous solution, which helps with effective waste management.

- Outlook

-

- The future demand for home care products in Japan is expected to revolve around the convenience of usage and transportation as it plays an important role in their lives. Refill pouches in liquid laundry detergents are expected to grow over 2020-25, with plastic pouches expected to grow at a CAGR of 5.4% in volume terms, both due to lower unit costs and demand for usage efficiency.

- Due to the pandemic and the concomitant rise in hygiene-consciousness, consumers have increased emphasis on keeping their homes clean and this trend is expected to continue over 2021-25. Flexible packaging formats like flexible plastic and stand-up pouches, which form the majority of pack types in this category, are expected to grow at a CAGR of 2.5% and 1.7% respectively in volume terms over 2021-25.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- Gum, which is mostly consumed on the go, saw a decline as people are confined to their homes. Therefore, demand for gum packaging – which accounts for the bulk of packaging units in confectionery – was hit particularly hard. This undermined the sales for flexible packaging which was the dominant type of packaging for gum. As a result, flexible packaging declined 6.2% in 2020. Therefore, demand for confectionery packaging declined for the first time in six years during 2020.

- As COVID-19 induced a compelling need to work from home, busy employees are looking for easy and convenient solutions to their meals which requires less time to prepare and yet gives them the required nutrition. This boosted sales of frozen ready meals and shelf-stable ready meals, which can be microwaved easily. Therefore, the main pack types, flexible plastic for the former and flexible aluminum/plastic for the latter, grew 27.8% and 15.5% respectively in volume terms in 2020.

- Trends

-

- The demand for healthy products has increased due to changing customer behavior amidst the COVID-19 pandemic. Thus, products like yogurt and packed cheese have seen a boost in sales. As a result, PET bottles which is the main pack type for yogurt grew by 10.9% in 2020 and flexible plastic, which is the main pack type for packed cheese, grew 6.8% in volume terms in 2020.

- The increased emphasis on convenience is encouraging manufacturers of shelf-stable meat and seafood to switch from metal food cans to plastic pouches. But since plastic is generally inferior to metal in terms of preserving product quality, extending shelf-life for plastic packaging has become a priority for packaging manufacturers in Japan. For example, several players have introduced plastic formats featuring airtight EVOH (ethylene vinyl alcohol) barriers, which prevent oxidization and help in improving the preservation of quality and flavor.

- Outlook

-

- Liquid milk formula, which was first introduced in 2019 after the ordinance by the Japanese Government, is expected to see a boost in sales over 2021-25, as it provides a convenient solution for babies and busy parents. As a result, the main pack type – HDPE bottles – is expected to grow at a CAGR of 10.5% in volume terms over 2021-25. Although HDPE bottles will remain a dominant pack type, other alternatives such as glass bottles, liquid cartons, and metal cans are likely to emerge.

- There will be a decline in demand for ready meals as the threat posed by COVID-19 begins to diminish. As a result, more employees will return to their workplaces and will eat fewer ready meals at home. Frozen ready meals and shelf-stable ready meals packaging will bear the brunt, declining with a CAGR of 2.4% and 0.7% in volume terms over 2021-25.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Japan

-

Japan is expected to open borders for tourists in June 2022

- According to the World Health Organization, as of May 26, 2022, Japan had 8,587,421 COVID-19 cases, 30,292 deaths, and 34,957 new cases.

- As of May 2022, Japan’s total vaccinations reached 275,201,140. The percentage of fully vaccinated citizens is 4%, while the percentage of citizens who have received the first dose is 81.7%.

- On June 1, 2022, regulations including on-arrival tests, a self-quarantine period, and place of accommodation after entry were changed, based on country groupings depending on where entrants come from at least 14 days before entering Japan. The groups are categorized as “Red”- countries with most COVID cases, “Yellow”- countries with moderate COVID cases, and “Blue”- countries with the least COVID cases. Moreover, the entrants will have to show a valid COVID-19 vaccination completion certificate, in addition to a negative RT-PCR test result, taken within 72 hours of departure.

- Although the Japanese government allowed the entry of foreign residents, businessmen, and students from March 1, 2022, it did not allow the entry of tourists. The Japanese government reopened its borders to foreign tourists on June 10, 2022.

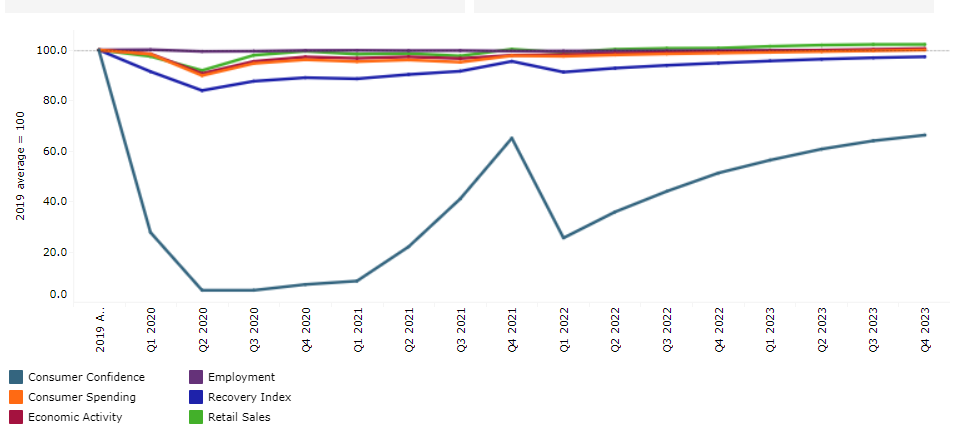

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Japan

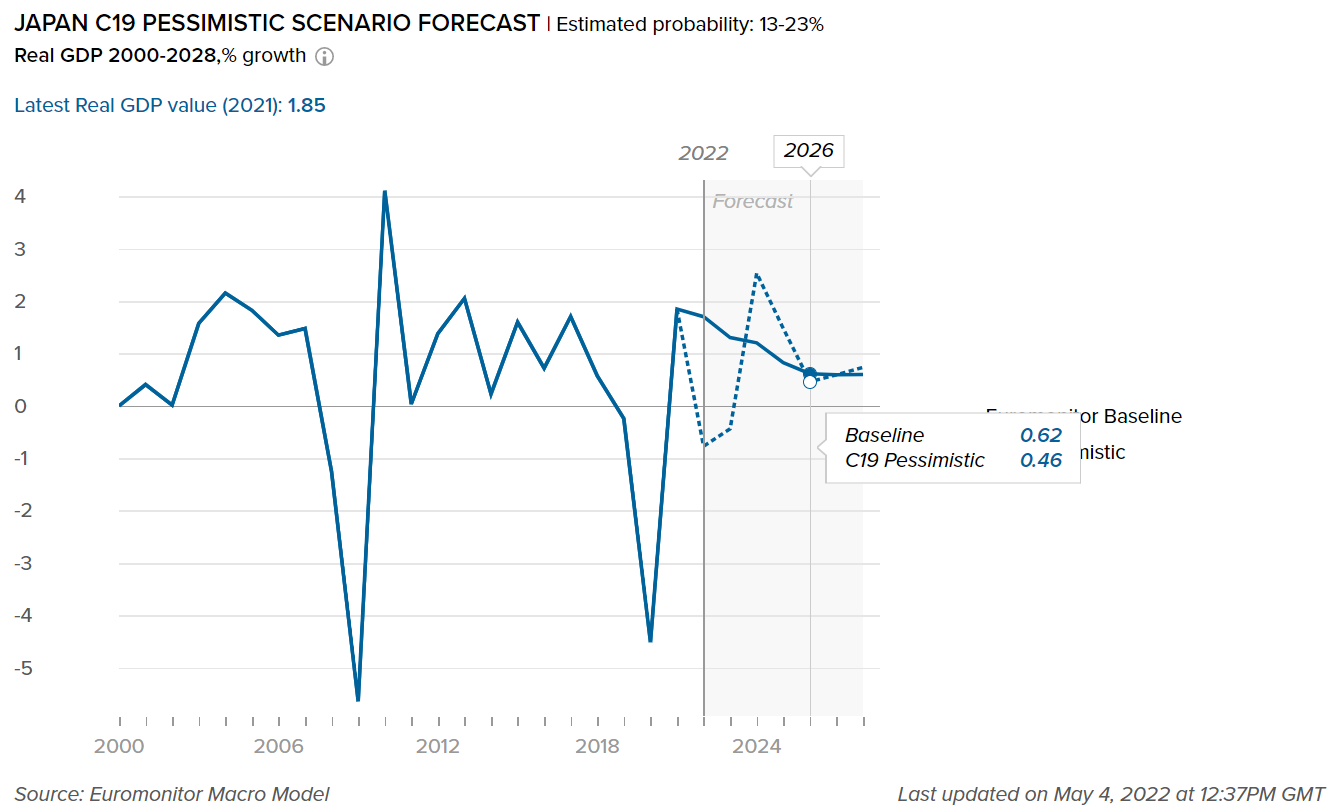

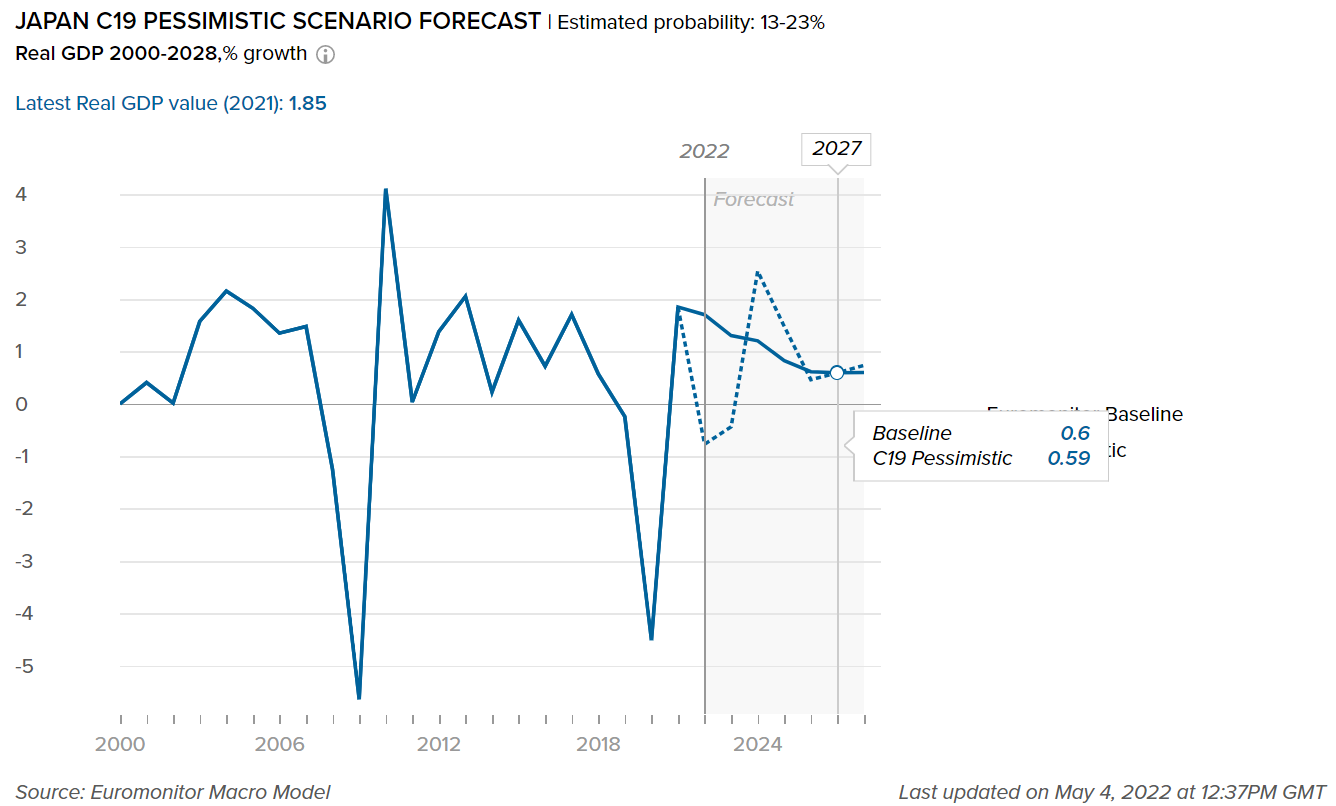

- Impact on GDP

-

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in Japan. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the "best case" COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the "worst case" COVID-19 scenario forecast that has an estimated probability of 13-23%.

Japan’s GDP is expected to remain strong owing to better monetary policies over the forecast period

- Japan’s GDP increased by 1.8% in 2021, following a pandemic-induced contraction of 4.6% in 2020, driven by strong policy support, robust exports, and a recovery in industrial production. In addition, rapid vaccination roll-out in Japan also loosened the prevailing COVID-19 restrictions in the country, aiding the economic rebound in the fourth quarter of 2021. In 2022, Japan’s GDP is expected to remain strongly driven by household consumption, rising capital spending, and accommodative fiscal and monetary policies. However, factors such as global supply chain disruptions, increasing oil prices, and rising fiscal sustainability risks pose concerns for Japan’s economy over the latter part of 2022-2026. Over 2022-2028, Japan’s economy is forecast to expand at a CAGR of 0.6%, in comparison to the average of 4.2% in the Asia Pacific.

- In 2021, government revenues increased by 2.3%. Moreover, in December 2021, the Japanese government approved an additional budget worth JPY36 trillion, which included the coronavirus pandemic relief fund, a cash handout program for families with children, and funds to promote tourism. These measures pushed the country’s public debt-to-GDP ratio to 262% in 2021, compared to the regional average of 94.7%. For 2022, the Japanese government approved a record-high budget of nearly JPY108 trillion, as the country aims to revive the pandemic-hit economy.

- If a more infectious and vaccine-resistant COVID-19 variant spreads in 2022, Japan may need to reimpose lockdowns and strict social distancing, which would lead to large drops in consumption, business revenues, employment, and wages. The economic outlook would resemble the C19 Pessimistic scenario. In this scenario, the economy would contract by 0.8% annually in real terms in 2022 but grow by 1.2% over 2023.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below displays the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the "best case" COVID-19 scenario forecast that has an estimated probability of 45-60%.

Reusable snacks packaging is expected to improve over 2022-2026 as businesses and consumers focus on sustainability

- In 2019, Nestlé Japan became the first major snack manufacturer to replace plastic packaging with paper packaging to become sustainable. Over 2020-2021, owing to the economic turmoil created by the pandemic, sustainability became a prime factor for Japanese snack manufacturers, and following Nestle’s decision, many players improved their business strategies and ventured into new packaging development. In 2021, Meiji invested JPY30 billion in ESG (environment, social, governance). The investment was used for activities including reducing the use of plastic in the production of its products, alongside the development and use of biomass materials. In the same year, Japan’s largest retailer, AEON partnered with packaging company, Loop and launched products with reusable packaging across 19 stores in Japan. Loop is expected to expand its services in Japan over 2022-2026 as more consumers, retailers, and manufacturers become informed and attracted to the benefits of reusable packaging.

- Dairy products and alternatives are expected to grow over 2022-2026. The health and wellness trend is expected to be a key driver, with consumers becoming increasingly aware of how nutrition affects immunity and general well-being as a result of the COVID-19 pandemic. In addition, as sustainability concerns gradually grow among Japanese consumers, albeit to a lesser extent than in other countries, it is expected that sustainably produced products, especially free-from-dairy products, will attract growing attention.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors mentioned in Japan. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the "best case" COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the "worst case" COVID-19 scenario forecast that has an estimated probability of 13-23%.

.

Travel restrictions and store closures are set to decrease beauty and personal care sales over the forecast period

- Limitations on tourism, travel, and the closure of beauty salons, parlors, perfumeries, and spas led to the decline of beauty and personal care in 2020. Moreover, trends such as working from home, going natural, and casualization also reduced consumer demand. In addition, the lack of interaction and closure of public places such as bars, restaurants, and hotels limited the prospects of the category. Subcategories such as color cosmetics, fragrances, sun care, deodorants, and hair care were severely hit owing to similar reasons. However, bath and shower and skincare were the two categories that saw increased demand owing to health concerns among Japanese consumers. Despite the surge of these subcategories, overall beauty and personal care had a massive decline in 2020, continuing into 2021. Although limitations were lifted in 2021, many consumers continued to work from home and avoided public places and unnecessary spending on products such as fragrances, color cosmetics, depilatories, and sun care. The category is not expected to recover in 2022 as these trends are likely to continue in Japan.

- As a third wave of infections hit Japan in November 2020 and continued into early 2021, bars and pubs were kept closed. This impacted on-trade sales of alcoholic drinks in 2021. Although the on-trade is expected to return to growth in 2022, foodservice volumes are not expected to return to pre-pandemic levels by 2026. The fear of infection and price consciousness is set to continue to affect consumer behavior over 2022-2026.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2021 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

4,645

4,702

-3.1

Home Care Packaging

3,204

3,153

-0.2

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 21 and Feb 22 data for 2022

Rigid Plastic

63,307

64,352

-0.23

Flexible Packaging

90,034

90,210

-0.10

Metal

30,786

30,610

-0.09

Paper-based Containers

20,039

19,838

0.57

Glass

8,618

8,234

0.03

Liquid Cartons

11,565

11,691

0.00

Economic uncertainty aided flexible packaging in Japan over 2020-2021

- As the pandemic increased economic uncertainty and health concerns in Japan, consumers prioritized cost-saving measures in addition to looking to maintain high levels of personal hygiene over 2020-21. Hence, if they previously purchased home care products in HDPE bottles over 2020-2021, they opted for comparatively cheaper refill packs in the form of plastic pouches for bathroom cleaners, kitchen cleaners, and multi-purpose cleaners. This trend is expected to gain ground over 2022-2026 as it encouraged leading players to start offering combo-packs or multipacks of refill pouches that allow consumers to access products at a lower price, thus, helping them to stockpile.

- In addition to plastic pouches, rising environmental concerns among consumers in Japan also led to increasing demand for water-soluble packaging for home care products such as detergents and dishwashers. Since water-soluble packaging, such as films, bags, and pouches are made from biodegradable materials that dissolve in water, they do not leave a harmful or toxic solution, which helps with effective waste management and improved environmental protection. Since this packaging is more economical and customizable, it is growing in popularity in Japan.

- Glass jars, which were traditionally used to store tea and coffee, recorded declines in 2021. They were replaced by folding cartons and composite containers, which were cheaper and more convenient for the user, as these pack types were more flexible and customizable. In fresh ground coffee pods, 110g folding cartons and 110g other metal were the most popular pack types. Growth in metal packaging formats in coffee products was supported by rising demand for high-quality at-home solutions to replace foodservice consumption during the pandemic.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies

The spread of a more infectious and highly vaccine-resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe diseases from new coronavirus variants, with moderate vaccine modifications

Vaccination campaigns progress in developing economies is slower than expected

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and releasing pent-up demand

Longer-lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment, and wages relative to the baseline forecast in 2022-2023

- Recovery Index

-

Recover Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.