Overview

- Packaging Overview

-

2020 Total Packaging Market Size (million units):

158,456

2015-20 Total Packaging Historic CAGR:

-0.3%

2021-25 Total Packaging Forecast CAGR:

0.1%

Packaging Industry

2020 Market Size (million units)

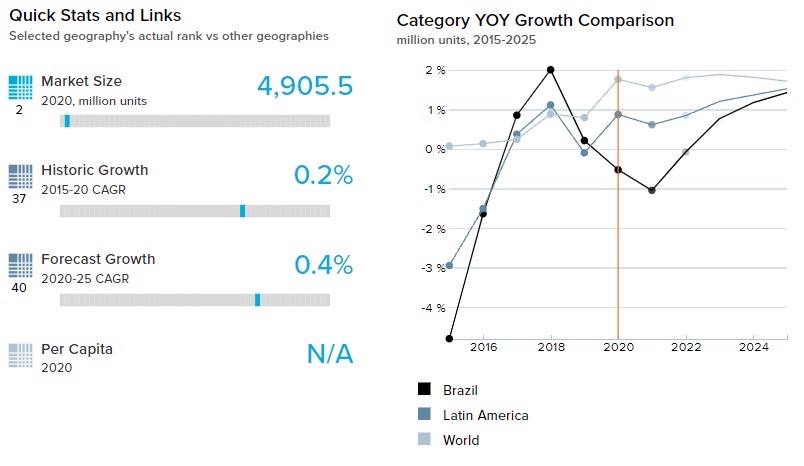

Beverages Packaging

47,373

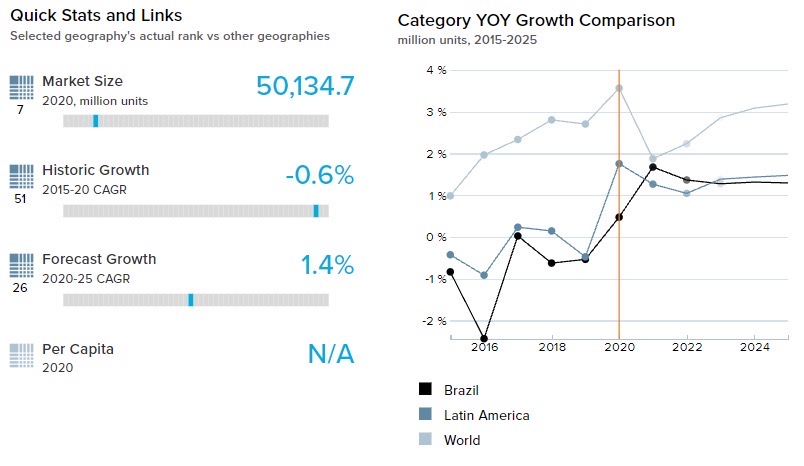

Food Packaging

87,614

Beauty and Personal Care Packaging

16,316

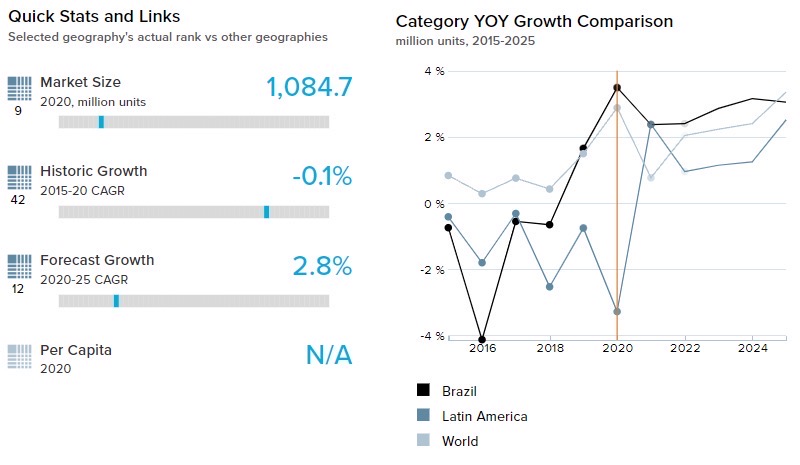

Dog and Cat Food Packaging

1,289

Home Care Packaging

5,864

Packaging Type

2020 Market Size (million units)

Rigid Plastic

45,233

Flexible Packaging

65,696

Metal

18,664

Paper-based Containers

10,866

Glass

6,768

Liquid Cartons

10,957

- Key Trends

-

Metal beverage cans have proved popular in alcoholic drinks. Metal beverage cans are less fragile than glass bottles which makes them suitable for transport and storage. They are also cost-effective. As a result, metal beverage cans are widely regarded as the most cost-effective solution for beer, wines, RTDs, and even spirits.

In dairy, premiumization gained momentum, with most innovation seen in yogurt. Yogurt enjoyed several new product releases including specialty, desert-shaped containers, upgraded bottle designs in terms of both aesthetics and ergonomics, and plastic caps containing chocolate sweet treats for mixing.

In beauty and personal care, large packs offering big value appeal to price-sensitive consumers in 2020. Several players announced the introduction of larger packaging types to target a broader consumer base. The trend was particularly significant in hair care. Standard shampoos and conditioners are often shared by entire families, allowing the purchase of large bottles to be used by everyone in the household.

- Packaging Legislation

-

ANVISA, Brazil’s national health surveillance agency, proposed a new system along the lines of color-coding seen in other countries, including neighboring regions such as Chile. ANVISA has repeatedly pointed out that simple warnings against sugar, sodium, and fat content on the packaging are insufficient, and has suggested the traffic light model with green, yellow, or red colors for low, medium, and high content, along with the standard nutritional data. However, the idea has been subject to severe backlash from the food and beverages industry out of fear of substantial drops in the consumption of certain products.

- Recycling and the Environment

-

Sustainability as a trend has led to Brazilian consumers showing greater concern for eco-friendly products. This further pushed the players to research and develop new alternatives and new types of plastics. Earth Renewable Technologies (ERT) produces plastics of plant origin, and already enjoys a strong presence in Europe and the U.S. The company claims that its plastics are fully biodegraded within six months. It is hoped that the biopolymer material will reduce dependence on environmentally harmful plastics and will encourage a zero-waste movement, as both producers and consumers shift away from non-degradable plastic waste.

Recyclability of packaging designs remains a challenge as packs are made of many layers and not all layers are suitable for the recycling process. Thus, separating all layers before recycling is a huge challenge. The industry is discussing the adoption of indexes of less than 5% of barrier materials to increase recyclability potential. Specialists highlight that this could be a risk for perishable products or goods, which need robust barriers during the distribution chain. Such a reduction could result in shorter shelf life for many products, which would be damaging to many companies. Resolving this issue is important as sustainability efforts receive pushback.

- Packaging Design and Labelling

-

In a case related to CNI (Confederação Nacional das Industrias), the high court denied their claim that the mandatory labeling of genetically modified food is unconstitutional on a federal level and that the decision should therefore be left to state and city authorities. The law in Brazil stipulates that any food or beverage made for human consumption, and which contains over 1% of any modified organism, must be labeled as genetically modified. The vote was tied in the Supreme Federal Court and the judgment was suspended.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Foodservice closures due to the pandemic resulted in a major decline in consumption through the channel, helping to give a strong boost – estimated by 35% by volume – to at-home consumption of coffee in Brazil. This helped drive volume sales of larger pack sizes such as 500g in flexible aluminum for products like fresh ground coffee.

- As there have been movement restrictions due to the COVID-19 pandemic, consumer travel declined to a great extent. As a result, impulse buying of soft drink beverages in pack sizes such as 250ml, 330ml, 355ml was reduced. As these small pack types are mostly sold in flexible plastics, volume was reduced by 18.3% in 2020.

- Trends

-

- In Brazil, larger pack sizes of fresh ground coffee such as 500g pack types are most popular as the average household size is 4 members per family. In recent times, however, the average household size has been decreasing due to the rising trend of people preferring to live alone and getting married later in life. This trend has posed a challenge against the dominance of larger pack sizes. Hence, to overcome this challenge, some brands are upgrading their traditional flexible packaging, introducing resealable closures such as zip/press closures that provide a barrier to air and light and maintain product quality. This move is aimed at making larger pack sizes of fresh ground coffee suitable for both large as well as small households.

- Growing health consciousness among consumers has boosted demand for smaller pack sizes of soft drinks. By consuming smaller pack sizes of soft drinks, less sugar will be consumed without compromising on taste or experience. This leads to more demand for smaller metal beverage cans as they remain chilled during consumption and are perceived to be eco-friendly.

- Outlook

-

- Traditionally, the usage of PET bottles in alcoholic drinks is not common. But PET bottles are now being introduced increasingly for beers and spirits. Smirnoff vodka brand is now offered in PET bottles. Other companies are following suit as PET bottles are cost-effective, easy to transport, and convenient to deliver at the doorstep.

- As the trend of “drink less, but drink better” is expected to grow, metal beverage cans are expected to benefit from this trend as metal beverage cans are usually associated with higher quality products. Metal beverage cans are easy to consume on the go, easy to store and transport. Along with this, glass supply issues and safety issues are pushing the manufacturers to switch from glass bottles to metal beverage cans. Metal beverage cans are expected to emerge in the wine and spirit category as well.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Presentation at the point of sale is becoming extremely significant since capturing impulsive buyers and buyers who lack brand knowledge is important. Stand-up pouches with zip/press closures are convenient to use as well as This is especially true for smaller packages ranging from 500g to 2.5kg. Bigger packs are still sold in flexible plastic, but brands are innovating with design and graphic print on the packaging. As a result, flexible packaging grew by 15.5% by volume in the dog and cat food industry in 2020.

- Metal food cans are predominantly used in wet dog and cat food, but with the rise of smaller pack sizes, flexible plastic has emerged as a new favorite. Another usage of flexible pack types is fractionated packs, such as 10 500gm plastic packs put together in a plastic bag to form a 10kg pack size. This allows the consumer to buy a higher volume of food (e.g., 7.7kg/10kg at a time) while maintaining quality and freshness.

- Trends

-

- The premiumization of brands is driving value growth in the dog and cat food packaging industry. Consumers are striving for better quality foods for their pets and prefer healthy alternatives such as organic, gluten-free, and additive-free. As a response to this trend, brands are looking at packaging types and design as a tool of differentiation. Pack types with zip/press closures, fractionated packaging, transparent packaging, etc. are perceived as premium by the customers. Thus, companies are focusing on better technology to produce high-quality packaging, as well as using new packaging formats and materials.

- Pet humanization is another trend that is influencing the dog and cat food packaging industry as consumers, especially young consumers, treat their pets like family members. Hence, owners tend to prefer pet food that is more like human food such as vegetables, rice, meat, etc. Companies are focusing on preparing food that looks and feels like fresh human food and has a better shelf life. This trend is pushing the players to develop pack types that will keep the food fresh for a long time. A few brands are introducing transparent packaging as it will help the customers see what the food looks like.

- Outlook

-

- COVID-19 accelerated the shift from retail stores/outlets to e-commerce. Online shopping has led to the emergence of bulk buying. Pet superstore websites such as Petz and Cobasi and online-exclusive shops such as PetLove are expected to focus on larger pack sizes. These sizes will mostly come in flexible packaging formats as they are easy to transport and easy to deliver to the doorstep.

- Brazilian consumers, particularly those with lower incomes, were already focused on buying dog and cat food pre-COVID-19. Pet owners will continue to buy bigger pack sizes and products that offer better value for money. It is anticipated that this trend will boost demand for affordable and convenient packaging materials such as flexible packaging

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- E-commerce grew exponentially against the backdrop of COVID-19. Beauty and personal care products that are packaged in flexible pack types were preferred by the e-commerce companies as they are convenient and easy to deliver to the doorstep. Hence stand-up pouches and flexible plastic pack types witnessed robust growth of 35.6% and 21.2% by volume in the beauty and personal care category in 2020.

- The impact of COVID-19 was especially strong on men’s grooming and color cosmetics categories. With many businesses, retail, and leisure outlets closed during the COVID-19 pandemic, consumers staying at home, and tourists largely absent, products used when going to work or for social occasions saw falling demand. As a result, flexible packaging in the men’s grooming category saw a 21.0% decline in 2020.

- Trends

-

- The pandemic had a significant negative impact on Brazil’s economy. Most Brazilians focused on purchasing essential products, with an emphasis on “value” when shopping. As a result, large pack sizes and combo offers were key drivers of sales in beauty and personal care in Brazil. For example, in skincare, 500ml, 575ml, and 1,000ml pack sizes performed especially well. As a result, flexible packaging in the skincare category grew by 21.3% by volume in 2020.

- Despite COVID-19 related restrictions, fragrances performed well in 2020. Fragrance packaging, surprisingly, grew by 5.3% by volume in 2020. Brazilians are looking for more sophisticated products in fragrances. Heavier and more intricate glass packaging types help manufacturers to deliver an impression of sophistication and a higher-quality product. Consumers expect such attributes to be incorporated into the items they purchase to make them look premium, leading to more investment in packaging by manufacturers to introduce such attributes to their offerings.

- Outlook

-

- It is expected that the consumers’ focus on value for money will become even more prominent over 2021- 25. This will further contribute to the growth of warehouse club sales. With economic uncertainty likely to continue, consumers will turn to distribution channels that are perceived to offer better value, with exclusive bulk packaging sizes likely to prove particularly successful. Packaging material such as flexible packaging is expected to gain from this trend. It is estimated that flexible packaging will grow at 1.8% CAGR by volume over 2021-25.

- The pandemic accelerated the penetration of e-commerce within the beauty and personal care segment. E-commerce offers benefits such as convenience and lower prices. This trend is expected to boost demand for packaging types such as flexible plastic rigid plastic, whereas it will hamper the growth of pack types such as glass. and metal.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- COVID-19 increased the focus on personal hygiene, leading to more sales of hygiene-related home care products. However, the pandemic-related restrictions created many supply-chain issues. So, to tackle these hurdles, companies switched to flexible plastic, as it is easy to transport and store in automated warehouses. As a result, flexible packaging grew by 3.6% by volume in home care packaging category in 2020.

- Heightened awareness about cleanliness among consumers boosted sales of homecare products such as surface cleaners, toilet care, and dishwashing. These products are mostly sold in flexible pack types, and these packaging segments grew 13.1%, 8.8%, and 18.4% respectively, by volume in 2020.

- Trends

-

- Manufacturers, such as Amcor-Bemis, are increasing usage of PET bottles, and flexible pack types for their products in the home care category. This trend is logistics-driven and is efficiently reducing operational costs. Some brands are using PET bottles for economy refills rather than the stand-up pouches commonly used for this purpose. From an operational standpoint, PET bottles as refills lead to lower packaging costs in comparison to multi-layered stand-up pouches and result in more affordable home care products in retail outlets.

- Companies are consistently innovating with eco-friendly and sustainable pack types. Brands like Bio Wash are creating greater awareness of their refillable and recyclable products. This has led to a greater shift towards more sustainable and environmentally friendly packaging, with such options gaining increasing popularity.

- Outlook

-

- Environmental, social, and governance (ESG) norms and regulations are far from ideal in Brazil. In recent times, companies as well as consumers, especially young consumers, are advocating for effective and empowered ESG guidelines. Water consumption during product usage is carefully observed and improved upon by the companies. With product launches such as concentrated products, packaging companies are anticipated to invest heavily in sustainability, which is expected to reflect in their pack types.

- Recyclability and sustainability are being focused upon by the companies, consumers, and the local government bodies as well. Sustainability is proving particularly important in laundry care packaging. Laundry care has been affected by acute water shortages. Thus, companies launched products that will consume less water such as concentrated liquid detergent in PET bottles. In addition, laundry care is one of the most significant categories for innovation and value-added products. This makes differentiation a key selling point for many products, such as detergents and fabric softeners.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- Metal packaging, which includes metal food cans and aluminum trays, lost ground to flexible pack types in 2020. The flexible variety is more convenient in terms of transport, storage, and usage for consumers, as well as for retailers. Pack sizes 430g and 830g remain popular in Brazil. but 170g and 300g packs gained popularity in 2020. The smaller sizes are mostly packaged in flexible pack types. Owing to this trend, flexible packaging grew by 3.6% by volume in the ready meals packaging category in 2020.

- A plastic pouch is the most popular pack type for shelf-stable meals. Plastic pouches continued to demonstrate strong volume growth in 2020. In shelf-stable ready meals, plastic pouches were introduced to help manufacturers reduce their production costs by switching from metal food cans. Plastic pouches are more cost-efficient and ensure the shelf life of the product.

- Trends

-

- Smaller players in the market are innovating by launching newer, more sustainable pack types. Food start-up LivUp, founded in 2016, has introduced ready meals sold in vacuum-sealed green packaging. This pack type can be conveniently reheated in microwave ovens and occupies significantly less storage space, an important feature for single-person households with smaller refrigerators. This appeals to the company’s customer base, which is largely comprised of millennials, a generation that is more informed and concerned about convenience and sustainability.

- In 2020, the most popular packaging format was 100g flexible plastic, which beat 500g flexible plastic to lead the category. Sales of the leading, smaller pack size remained relatively stable in 2020. However, sales of 500g packs registered a considerable decline in volume sales as consumers struggled to afford the higher unit prices of larger packs during the COVID-19 pandemic. As demand for 500g packs fell in 2020, other pack sizes increased in popularity smaller pack sizes such as 200g and 300g flexible plastic are more affordable to consumers and offer more flexibility when it comes to managing food waste, especially for smaller households.

- Outlook

-

- In the second half of 2021, yogurt is projected to return to robust growth as consumers are expected to return to work and school as the threat of COVID-19 infection subsides and local restrictions come to an end. The rapid recovery of yogurt will benefit thin wall plastic containers and HDPE bottles, which are their dominant pack types.

- Milk alternatives are expected to suffer over the 2021-2025 forecast period. Milk alternatives, which are costlier than milk products, will mainly be hampered by the reduced purchasing power of the Brazilian population. This will hamper overall demand for brick liquid cartons in the forecast period, which is the leading pack type in milk alternatives.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Brazil

-

Insights released by the recent advisory bulletin indicates cause for concern

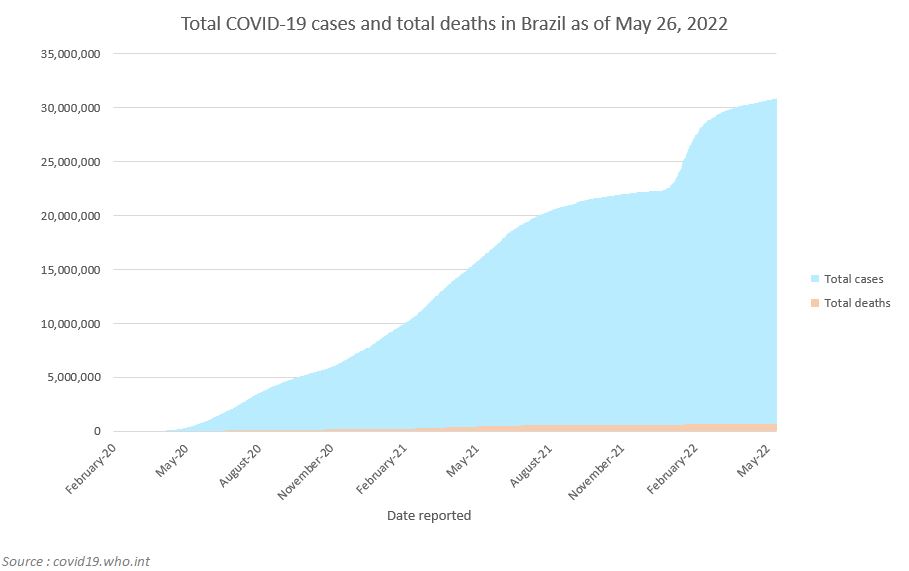

- According to the World Health Organization (WHO), on May 26, 2022, Brazil had 30,836,815 COVID-19 cases, and 665,905 deaths. The country’s total cases per million inhabitants on the day reached 145,624.

- The recent increase in the number of cases in the country has prompted some municipalities to recommend the usage of masks, with schools also asking students to wear protective items. Newer variants of the virus are currently in circulation which has increased the number of COVID-19 cases and hospitalizations, and has led to researchers speculating if the country is in its fourth wave of the pandemic. The country recorded more than 59,000 new cases on Saturday, May 28, 2022.

- In February 2022, the travel ban imposed on travelers arriving from South Africa, Eswatini, Botswana, Zimbabwe, and Namibia was removed. On the other hand, the requirements to present a negative PCR test before entering the country have not been altered.

- According to the WHO, Brazil administered a total of 428,405,492 vaccines as of May 20, 2022, with 76.4% of the people being fully vaccinated, while 85.0% of people have received at least one vaccine dose.

- The newest edition of the COVID-19 advisory bulletin released on May 19, 2022 states that the current vaccine coverage against COVID-19 in the adult population is concerning due to stagnated growth rates. Increasing hospitalizations and the emergence of new variants is likely to further aggravate the situation and further warrants the need for protection measures including compulsory wearing of masks.

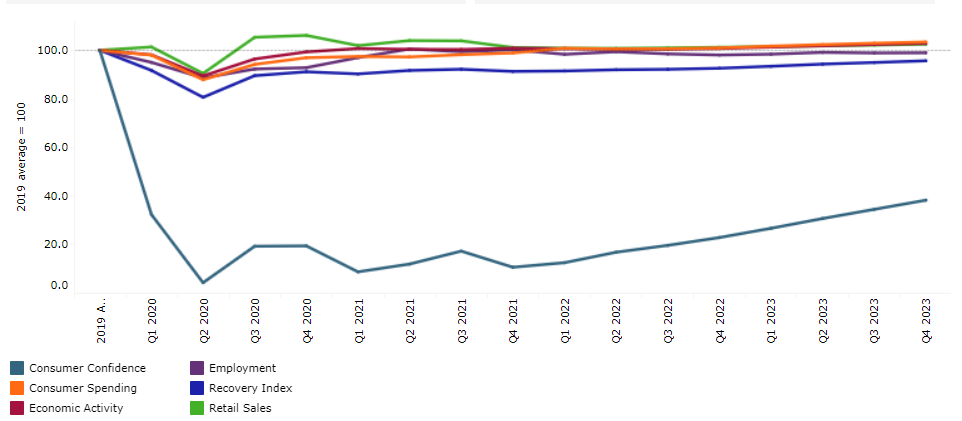

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Brazil

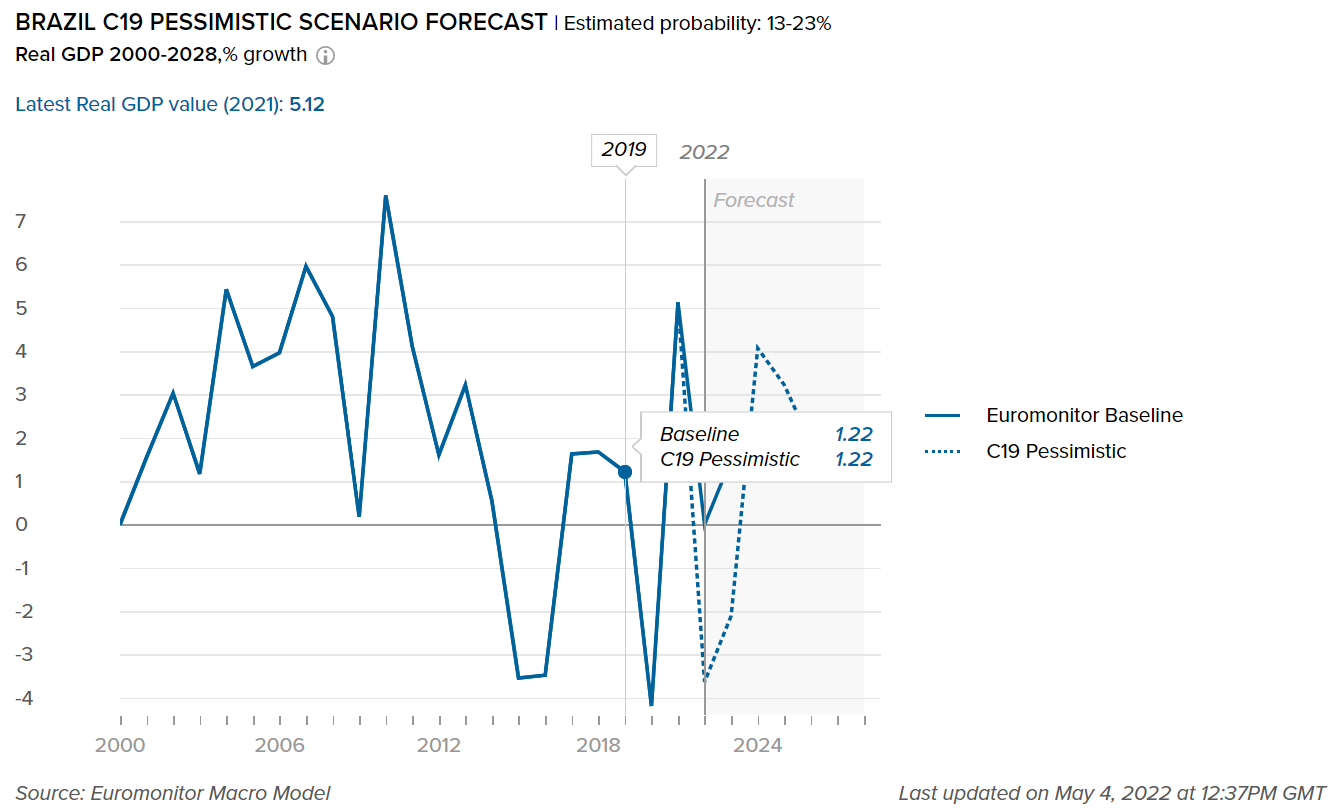

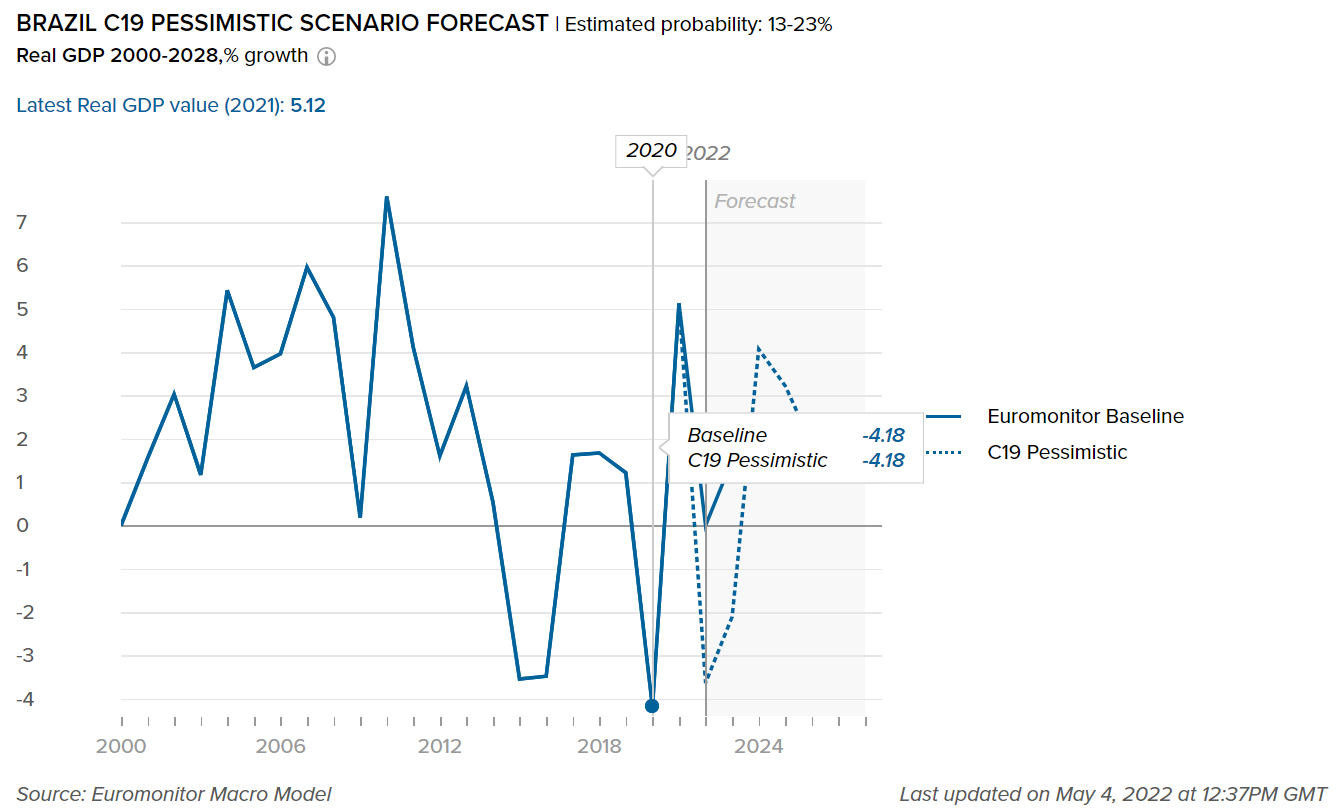

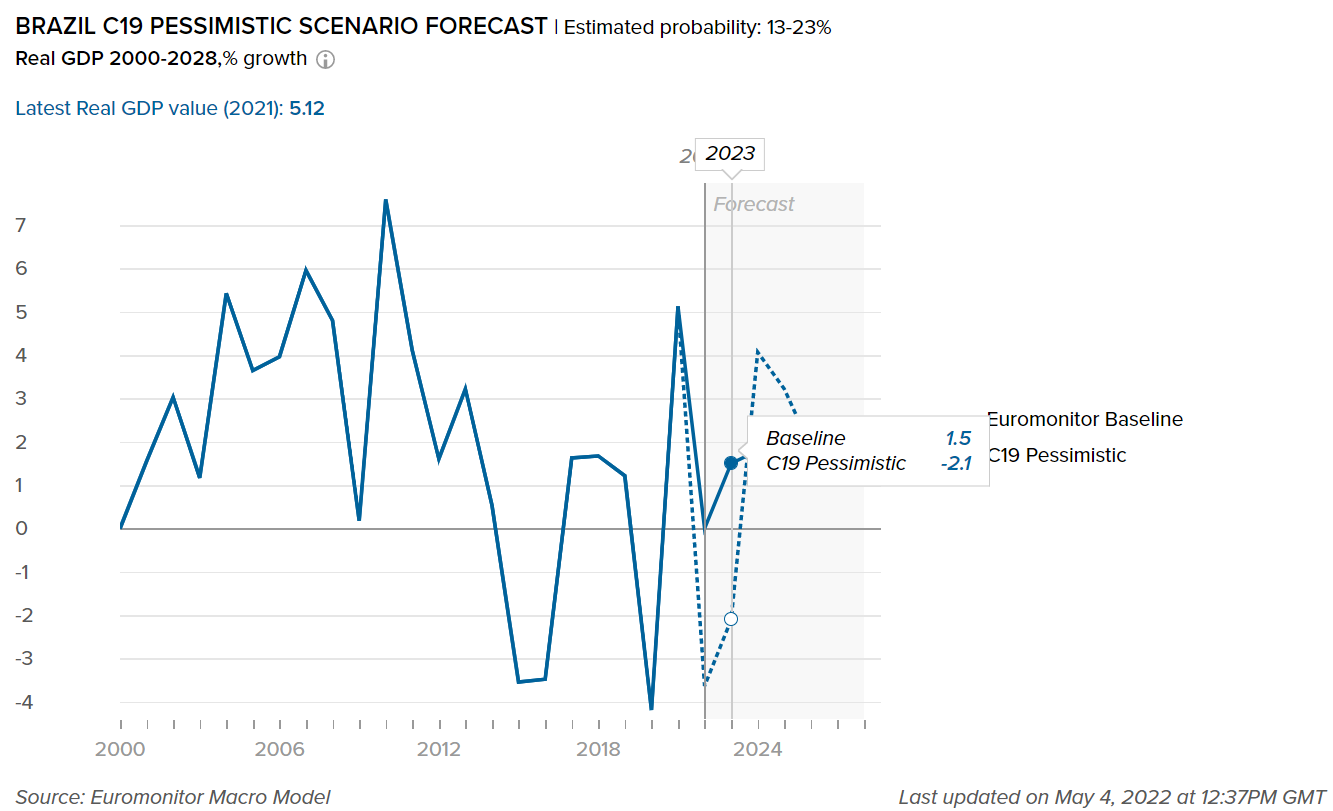

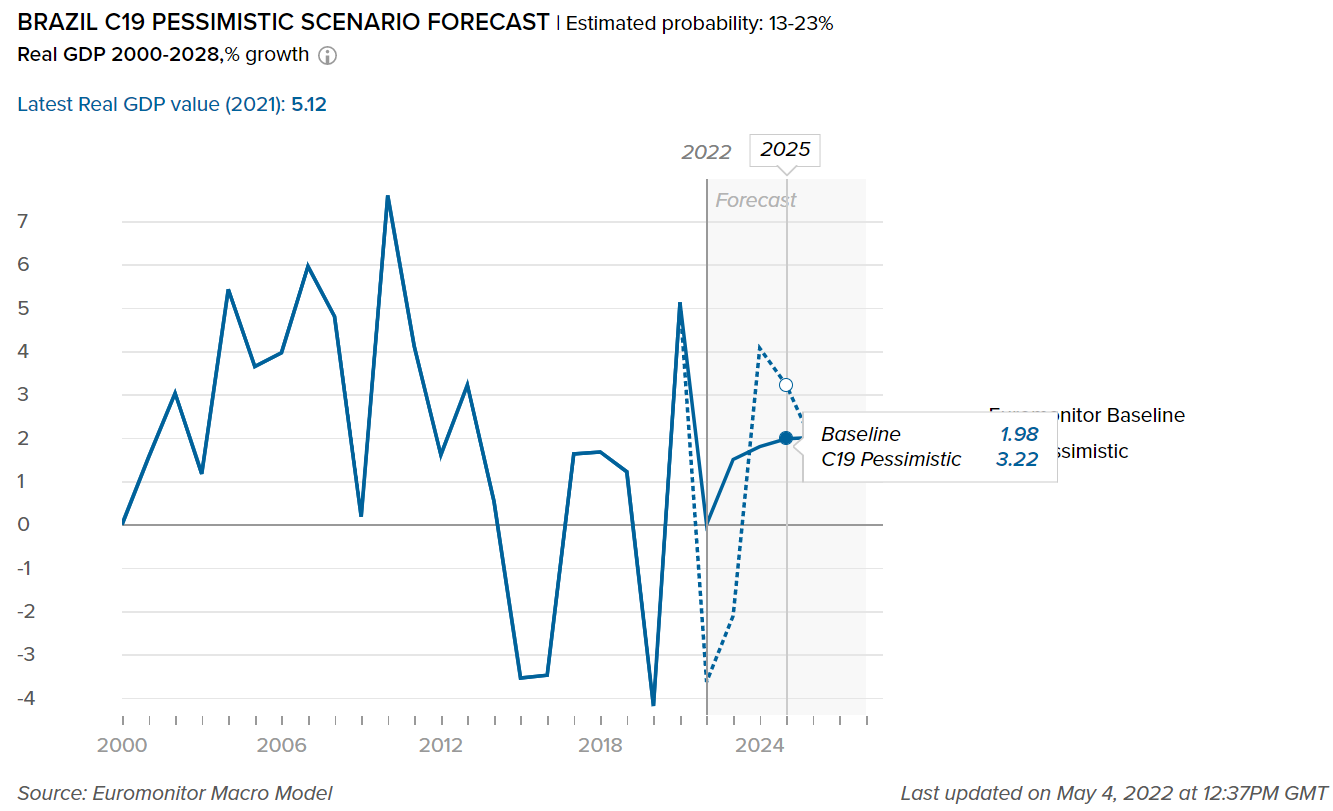

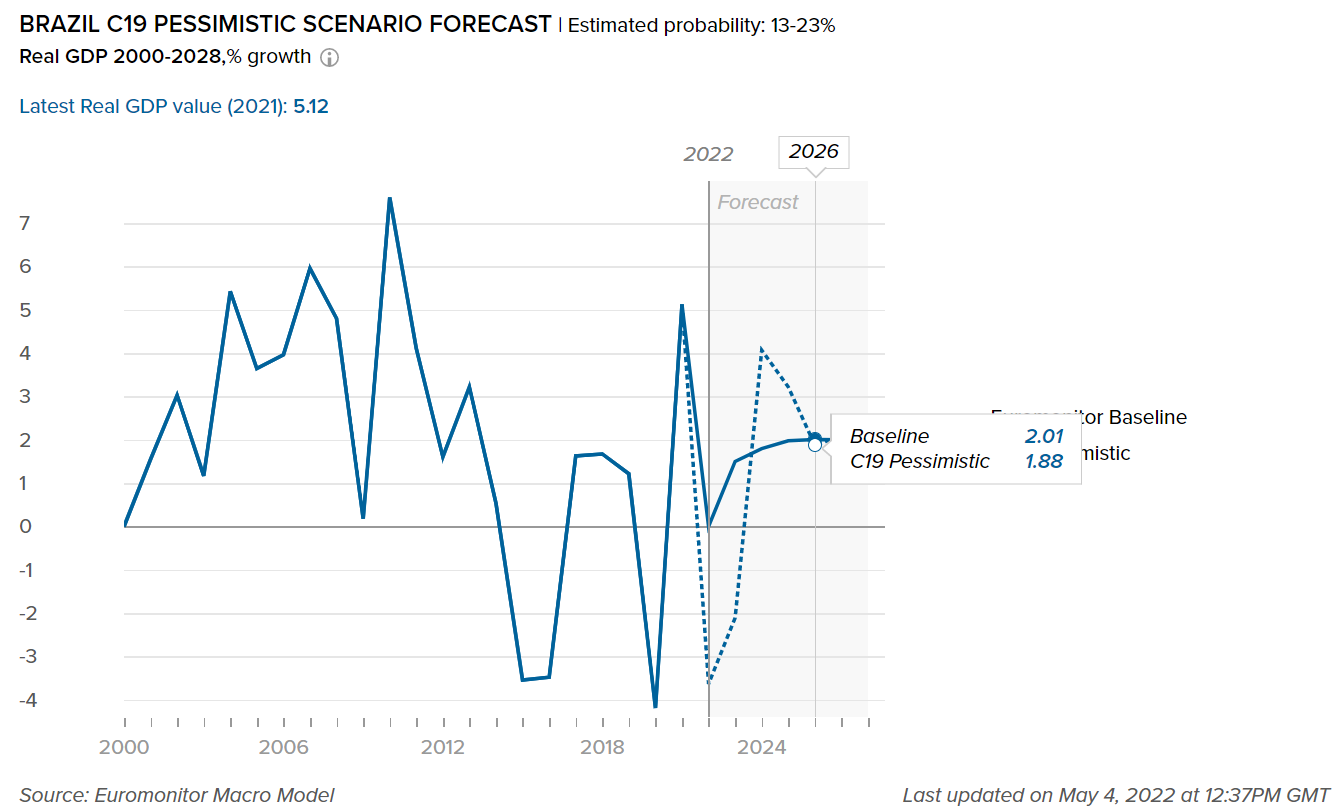

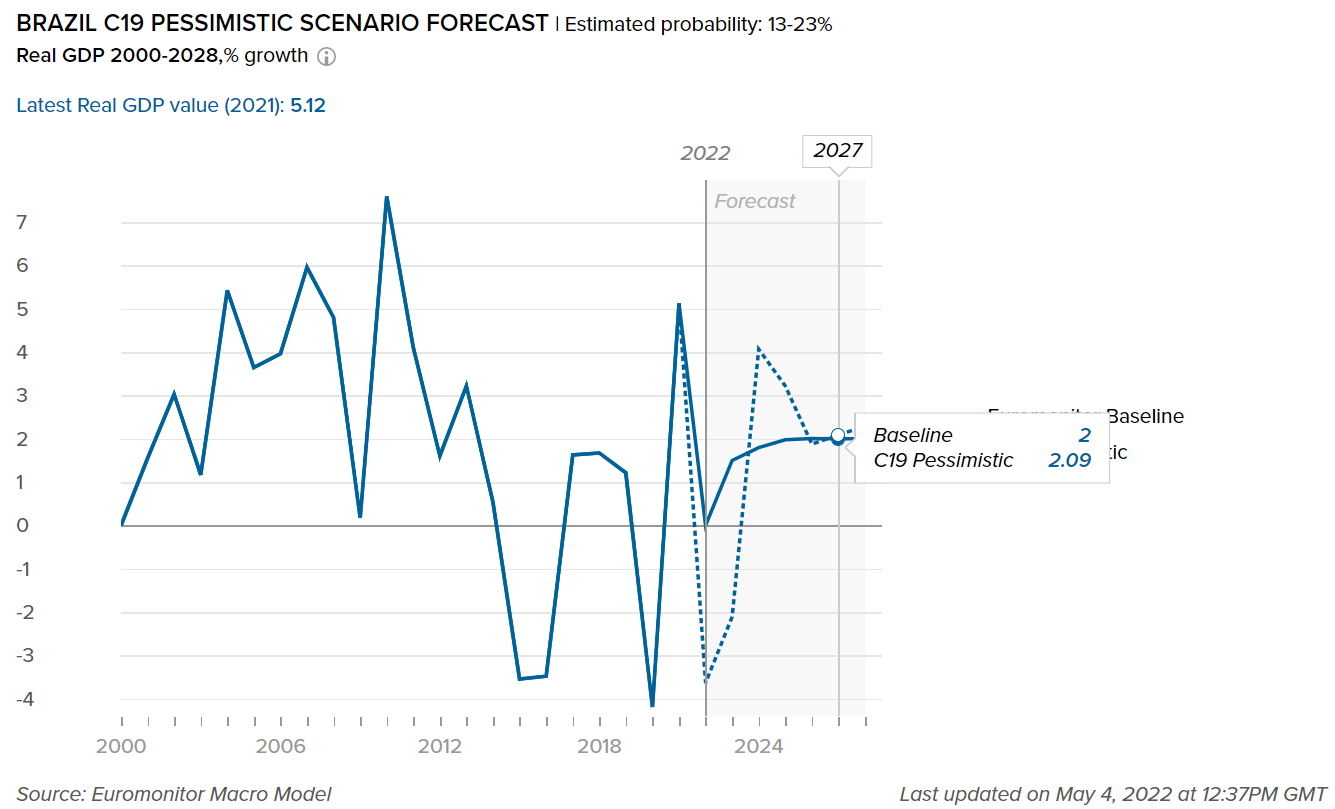

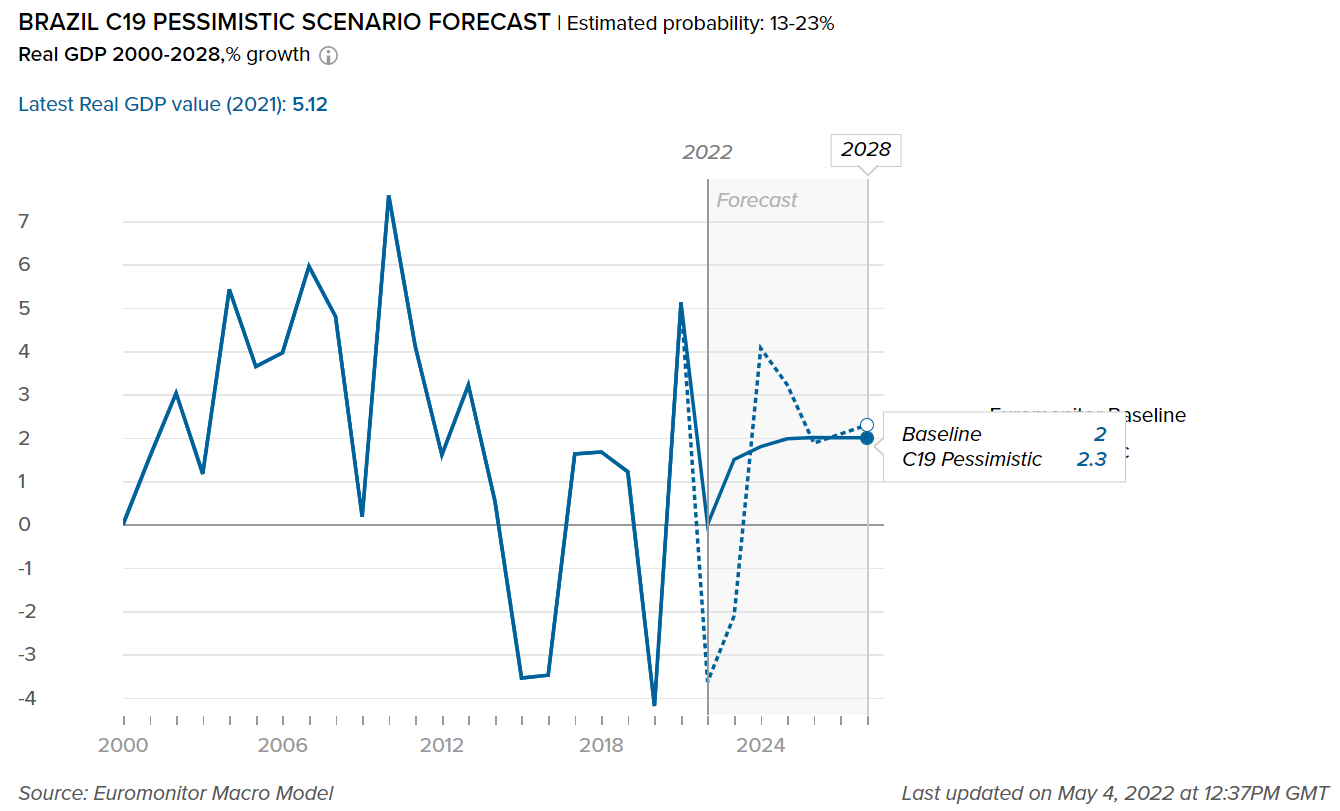

- Impact on GDP

-

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact real GDP value in Brazil. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Brazil is expected to witness slow economic growth in the medium term

- Over 2019-2020, commodity prices in Brazil surged as a result of global supply chain disruptions resulting in inflation. The ongoing effect of the pandemic on global commodity prices in 2021 further elevated the inflation rate in the country. Over 2021, inflation in Brazil increased to 8.3% from 3.2% in the previous year. It is anticipated that the general election in 2022 will heighten government spending and cause an inflationary spiral in the country.

- Expectations are that the inflation rate in Brazil will fall to 3.5% by 2026, although this will depend greatly upon the war in Ukraine and its repercussions on global commodity prices.

- In the medium term, Brazil’s economy is expected to perform worse than the rest of Latin America with forecast average annual real GDP growth of 1.6% over 2022-2026. In comparison, average annual real GDP growth for Argentina and Colombia is expected to be 2% and 3.5%, respectively. Higher inflation and drought-related disruptions in the Brazilian agricultural sector, among other factors, are predicted to limit the country’s medium-term economic growth.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below shows the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

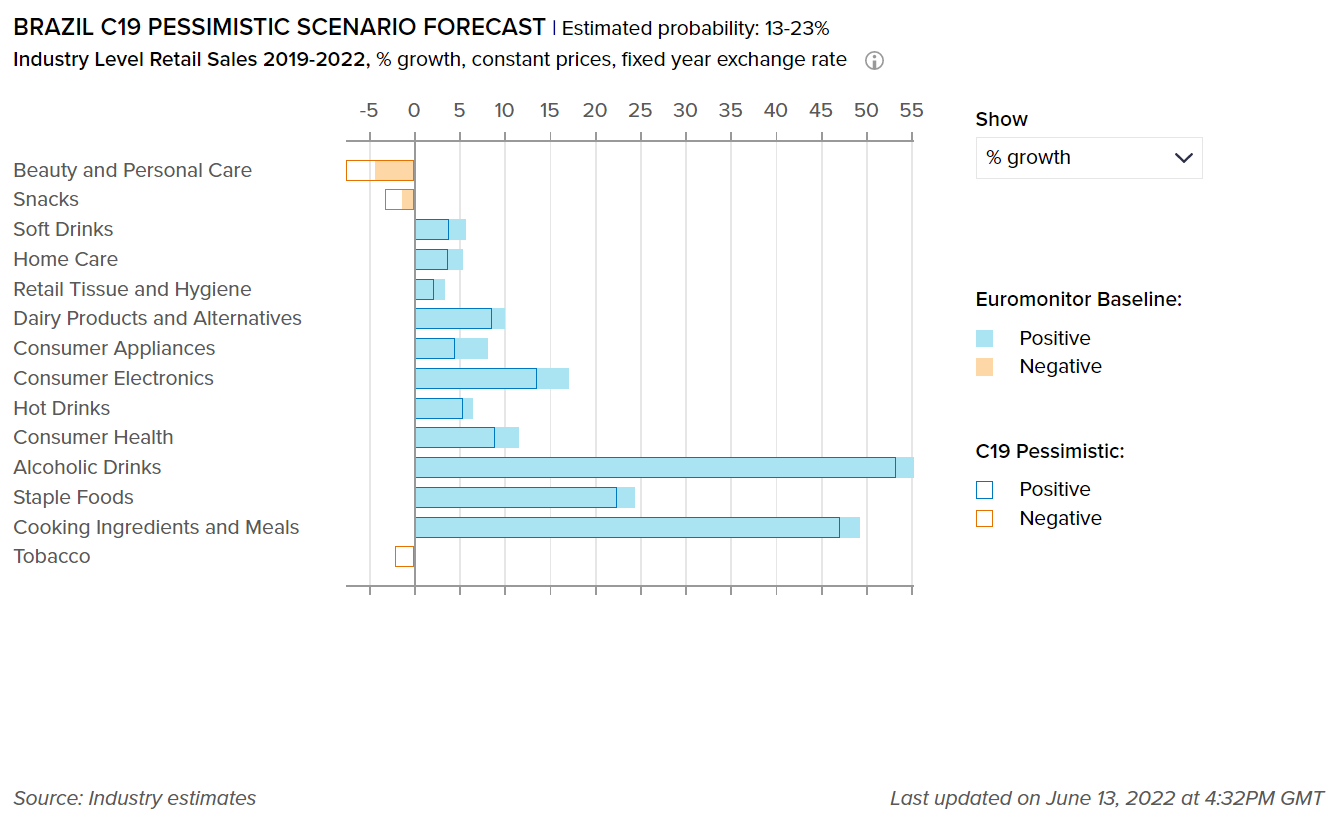

Demand for cooking ingredients and meals, alcoholic drinks, and home care products is expected to surge over the forecast period

- The rising popularity of the health and wellness trend during the initial stages of the pandemic encouraged Brazilians to cook fresh, nutritious meals at home. Over 2021, most consumers realized that preparing meals at home was cheaper than ordering food online. This elevated the consumption of cooking ingredients (sauces, dry herbs, and spices) and meals over 2019-2021. These factors are expected to influence consumers’ purchasing decisions in 2022 as well. It is anticipated that retail sales of cooking ingredients and meals will increase by 45% over 2019-2022.

- The pandemic might have had a devastating effect on certain industries, such as tobacco, but it managed to boost sales of alcoholic drinks in the country. Over 2019-2021, alcoholic beverages enjoyed stable demand among Brazilian consumers. One factor that increased retail sales of alcoholic drinks over the aforementioned years was consumers engaging in stockpiling during the initial stages of the pandemic. Another pivotal factor was using wine as a cooking ingredient. As the number of COVID-19 cases is subsiding and normalcy is returning in 2022, it is expected that the consumption of alcoholic drinks will increase over the year as Brazilians are back to celebrating special occasions and socializing with friends. It is anticipated that retail sales of alcoholic drinks will increase by 55% over 2019-2022.

- Over 2019-2021, Brazil witnessed three waves of the pandemic. This created a surge in demand for household disinfectants as people took conscious efforts to keep their homes clean to remain protected from the virus. There was also increased consumer desire to create a soothing and pleasant environment at home. These factors expanded retail sales of home care products, such as air freshners and scented candles, over the aforementioned period. It is anticipated that retail sales of home care products will increase by 5% over 2019-2022.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors covered in Brazil. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Rising health-consciousness among consumers bolsters demand for consumer health products over 2019-2022

- The onset of the pandemic brought a pivotal shift in the mindset of Brazilian consumers. Over 2019-2021, Brazilians paid greater attention to the foods they were consuming. As a result, demand for foods that boost immunity, such as vitamins and dietary supplements, increased over 2019-2021.

- The increased prevalence of stress and anxiety among consumers resulting from factors such as financial hardships, social isolation, etc., elevated the demand for analgesics and sleep aids over 2019-2021. It is anticipated that retail sales of consumer health products will increase by more than 10% over 2019-2022.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

16,652

16,865

1.7%

Home Care Packaging

6,215

6,443

0.2%

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

46,116

47,549

-0.41%

Flexible Packaging

66,381

67,637

0.36%

Metal

24,090

26,913

0.34%

Paper-based Containers

11,321

11,644

1.29%

Glass

7,940

8,450

0.13%

Liquid Cartons

11,336

11,552

0.00%

Increased demand for home care products and sauces benefits flexible packaging

- Brazil faced the third wave of COVID-19 in 2021. This influenced Brazilian consumers to keep purchasing home care products such as disinfectants to keep their homes clean and stay safe from the virus. In 2021, demand for multi-purpose cleaners and all-purpose cleaning wipes soared, as these products provided convenience to buyers. As a result, key pack types, such as plastic pouches in multi-purpose cleaners and flexible plastic in all-purpose cleaning wipes, witnessed booming demand in 2021, and are expected to perform well in 2022.

- With most Brazilian consumers turning to home cooking, demand for tomato pastes and purées soared in 2020. This benefited aluminum/plastic pouch packaging, which is the primary pack type for these products.

- While stand-up aluminum/plastic pouches packaging has been prevalent in the country for a long time, innovative releases were made, for example in Predilecta’s Sacciali line. The stand-up pouch is in the shape of a glass jar, and the pack comes with a different texture that resembles the texture of glass.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recovery Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.