Overview

- Packaging Overview

-

2020 Total Packaging Market Size (million units):

40,315

2015-20 Total Packaging Historic CAGR:

1.0%

2021-25 Total Packaging Forecast CAGR:

-2.3%

Packaging Industry

2020 Market Size (million units)

Beverages Packaging

16,370

Food Packaging

21,364

Beauty and Personal Care Packaging

1,262

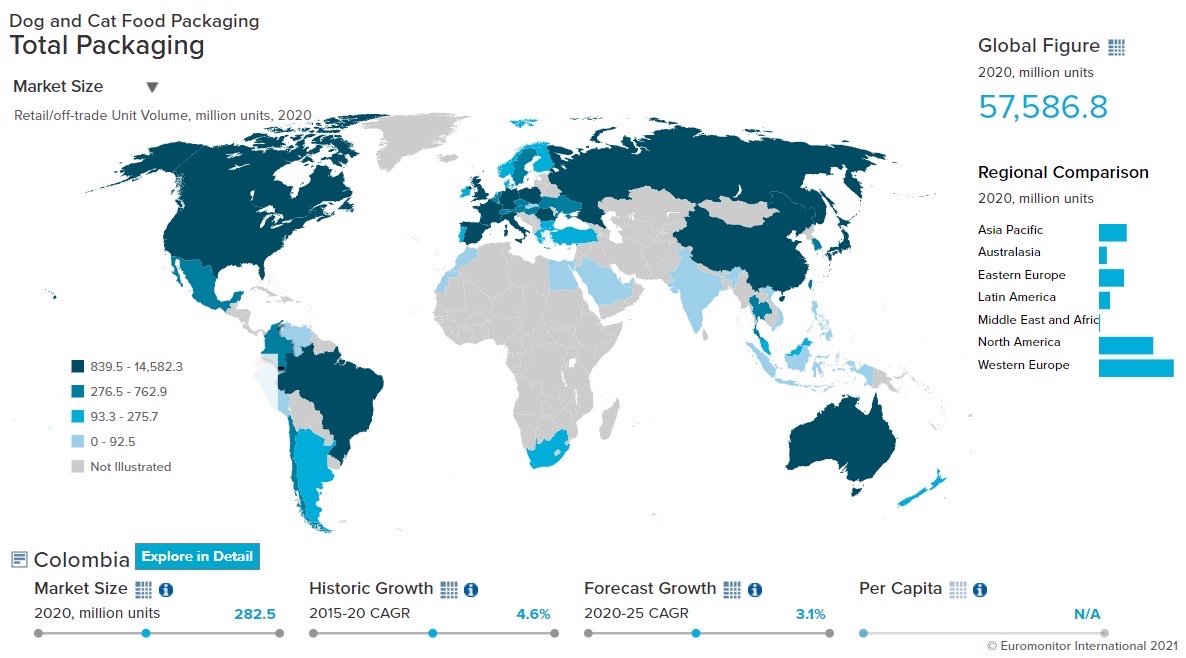

Dog and Cat Food Packaging

265

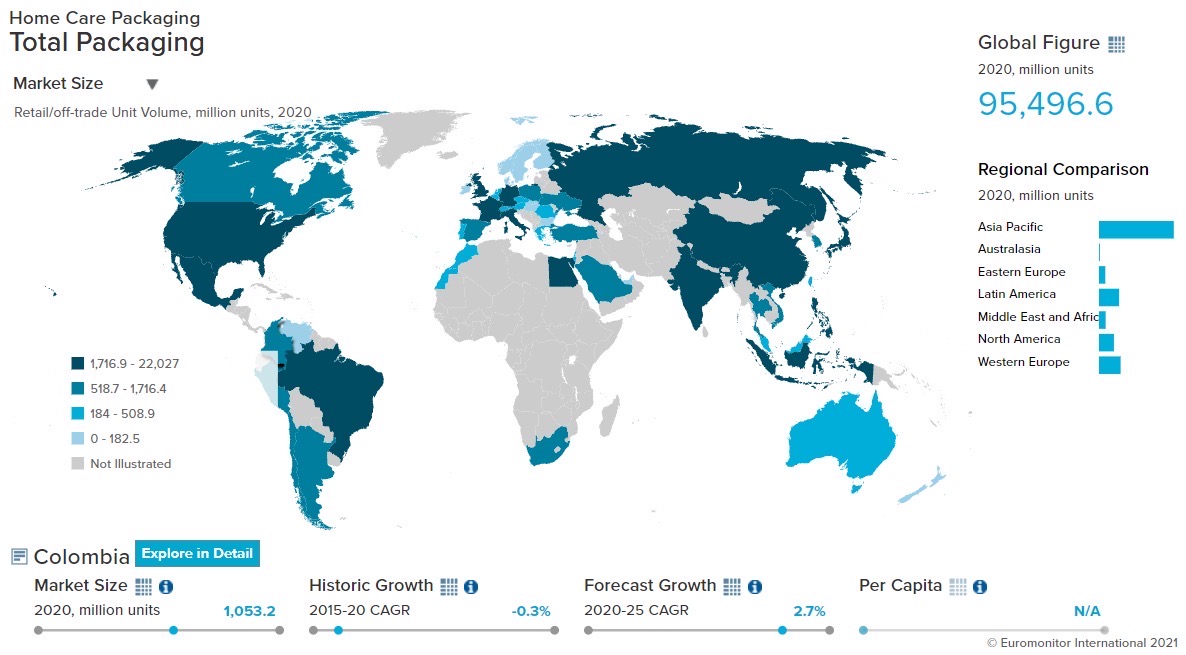

Home Care Packaging

1,053

Packaging Type

2020 Market Size (million units)

Rigid Plastic

7,650

Flexible Packaging

20,763

Metal

1,701

Paper-based Containers

1,289

Glass

7,710

Liquid Cartons

1,197

- Key Trends

-

A notable shift towards larger packs and family-value formats has been one of the main impacts of the 2020 pandemic in food and beverage packaging in Colombia. By contrast, smaller sizes that were previously gathering pace in line with the rising on-the-go snacking trend have suffered. Moreover, the closure of schools undermined demand for 200ml packs of flavored milk and drinks in Tetra Pak packaging, which are usually popular for lunchboxes. On the other hand, demand for 1-liter formats of milk and family-sized soft drink packs has risen, thus reducing the volume production of packaging to some degree.

Throughout the packaging industry in Columbia, brands will continue to focus on innovative formats to generate interest and boost demand across all areas over the forecast period, with further investment in sustainable solutions. Convenience is also likely to be a driver of development, with portable, on-the-go formats becoming more visible.

- Packaging Legislation

-

In 2018, the Ministry of Environment and Sustainable Development (MADS) issued a resolution to regulate the environmental management of packaging waste. The regulation covers all categories of packaging such as paper, cardboard, plastic, glass, and metal packaging. Public awareness of the environment has risen significantly as Columbia is facing acute drought and prolonged winters. According to the new law, companies that produce packaging must now formulate an environmental management plan for packaging and packaging waste. The plan must contain details of the operations, technical, and financial schemes of the project. According to the law, companies should maintain transparency about collection, transportation, storage, re-use, and final disposal of waste.

- Recycling and the Environment

-

Nearly a third of all solid waste emanates from Colombia’s capital city, Bogotá. It also has a lower recycling rate than the rest of the country. It is estimated that single-use plastic accounts for 54% of all plastic waste. It is also estimated that 78% of Colombian households do not separate plastic waste. Over 300 of Colombia’s landfills are likely to reach full capacity by 2025. This has prompted urgent calls for rapid action in waste management from consumers, manufacturers, and the government.

- Packaging Design and Labelling

-

The Colombian government approved front-of-pack warning labels legislation for food and beverages in 2020. According to the new law, it is mandatory to display information about the content levels of sugar, sodium, and saturated fats per 100g or 100 ml of product. The law has also changed the nutritional label requirements to make such labels clearer and simpler. The warning labels will be bold black circles that enclose pictorial representations of the targeted ingredients. In a response to this law, brands are anticipated to redesign packaging formats, especially in terms of size, to limit the warning labels’ negative impact.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Flexible packaging is a preferred packaging category in hot drinks among consumers, producers, and retailers. It dominates the segment as it is lightweight, low-cost, and has versatile characteristics in terms of pack size such as it is used for single-portion sachets as well as is used for family sizes of over 1kg. Most flexible packaging offers resealable zip/press closures, as well as affordable prices and a presence in almost all distribution channels. As a result, flexible packaging grew by 5.9% by volume in the hot drinks category in 2020.

- The economic impact of the pandemic has lowered the purchasing power of consumers, making smaller pack sizes within soft drinks packaging more lucrative. These smaller pack sizes are usually witnessed within PET bottles and stand-up pouches. As a result, they have registered a volume growth of 14.1%, and 1.6% by volume respectively for 2020. This shift in demand for smaller pack sizes can also be seen in bottled water where the once standard pack size of 600ml was replaced by 300/330ml. Increasing price sensitivity is expected to drive the soft drinks manufacturing shift towards stand-up pouches from glass bottles, as they are economical and easy to carry and store

- Trends

-

- The coffee culture is on the rise in Colombia, driving demand for upscale products and premium packaging. Premiumization started in fresh ground coffee, where innovation and expansion in the varieties offered can be observed. A busy lifestyle has led to more demand for instant coffee among consumers. Thus, manufacturers are increasingly introducing premium instant coffee in attractive and innovative pack types.

- Rising health consciousness amongt Colombians prompted manufacturers to offer healthier alternatives within hot drinks, often positioning them as a replacement for soft drinks. As a result, soft drink manufacturers are looking to compete in this space by offering natural products such as fruit/herbal tea. It led to the development of infusions that can be prepared in cold water in just a few minutes.

- Outlook

-

- PET bottles are expected to grow in bottled water, with brands increasingly transitioning to PET bottles from expensive and bulky glass bottles in other product areas, especially in nectars and juices. The use of PET bottles is anticipated to spread through the different categories of soft drinks, mainly at the expense of glass. Most brands would replace glass bottles with PET bottles, which are safer and easier in terms of portability and storage.

- Returnable packs in beer are expected to grow over 2021-2025 period due to the inauguration of the new Central Cervecera facility in 2019. This facility will enable brands to improve distribution channels for small grocery stores. Small grocery stores are the most popular channel for beer, in which returnable bottles dominate. Similar facilities are expected to be created, as returnable bottles are becoming popular among consumers, as well as manufacturers.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Flexible packaging in dog and cat food is on the rise due to the convenience and functionality of the packaging. Consumers expect practicality or functional packaging such as stand-up pouches, and zip/press closure pouches as these pack types help keep food fresh. The importance of packaging is increasing as consumers carefully pay attention to details such as ease of opening, closing, handling, and storage. This is in addition to the demand for food protection and conservation. Flexible packaging fits the bill perfectly as it is suitable for packaging with the above-mentioned qualities. As a result, flexible packaging grew by 4.5% by volume in 2020.

- Wet cat food saw a shift from metal food cans to stand-up pouches as stand-up pouches are more affordable and they are convenient in terms of storage and handling. There is also increasing usage of stand-up pouches and zip/press closures for premium and super-premium products. As a result, stand-up pouches in wet cat food grew by 10.0% in terms of volume in 2020.

- Trends

-

- Consumer purchases of dog and cat food packaging are highly influenced by the type of retailer that they visit to buy these products. Many pet shops are finding it more practical to stock repackageable products in rigid plastic. The retail channel is benefiting from this strategy as the country suffers an economic downturn in the wake of the COVID-19 pandemic.

- Meanwhile, in independent small grocers, a frequent concern is the fact that dog and cat food is bought in small quantities alongside food for human consumption. Thus, these outlets are focusing more on small pack sizes positioned as fit for daily consumption needs. As a response to this, hypermarkets are focusing more on bulk packs and multipacks of single-serve packs.

- Outlook

-

- Most dog and cat food products in Colombia are imported due to the high cost of local production. Thus, innovations and new developments targeted at Colombian consumers are limited. But there are some improvements expected in terms of pack closures and new pack types over 2021-25. Pack types that offer convenience and functionality such as stand-up pouches and pouches with zip/press closures are expected to grow at 16.0% CAGR by volume over 2021-2025.

- In the case of dog food, consumers still associate pouches with dog treats rather than wet dog food. Manufacturers are expected to invest in the development of clear design features to differentiate these product types. The brands are keen to drive sales of single-serve pouches in wet dog food due to the attractive margins offered by these products. So packaging designs are expected to become important in this area over the 2021-2025 period.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- In bath and shower packaging, flexible packs in personal hygiene and body wash/shower gel are leading in 2020. Panic buying at the beginning of the pandemic helped liquid soap sales as consumers sought to stock it up as an essential product to lower the risk of infection and prevent the spread of COVID-19. Formats in bar soap continue to grow in 2020, led by 90g folding cartons and 75g flexible paper. As a result, flexible packaging grew by 3.5% by volume in the bath shower category in 2020.

- Color cosmetic packaging is suffering from the fact that its products are used mainly for social occasions outside the home. In addition, ongoing mask-wearing has eroded the desire for most items in facial makeup. Leading the category’s decline in 2020 is flexible plastic in blusher/bronzer/highlighter, followed by blister and strip packs in powder cosmetics. As a result, flexible packaging declined by 27.3% in color cosmetics in 2020.

- Trends

-

- In Colombia, packaging in beauty and personal care has continued to evolve in line with rising environmental awareness. An increasing number of brands are using ecologically sound raw materials, naturally derived inks, and adapting their production facilities for sustainable manufacturing. As consumers lookout for products and packaging that are environmentally friendly, several brands are pursuing national and international certifications to assure consumers of their commitment to sustainability.

- After the successful introduction of a sales tax on plastic bags, the government has expanded its efforts towards promoting sustainability by considering a prohibition on items such as plastic bags, plastic drinking straws, cotton swabs, and plastic applicators. Brands in color cosmetics packaging are introducing alternatives to reduce their use of plastic in secondary packaging – for example, instead of plastic strips, stickers are now commonly used to secure powder, eye shadow, and foundation products.

- Outlook

-

- Overall growth in beauty and personal care packaging is expected to be stable at 3.6% CAGR by volume over 2021-25. Increased hygiene-consciousness is expected to persist in the wake of the pandemic. Color cosmetics packaging and fragrances packaging will decline till the end of 2022 and are expected to record positive growth post-2023. Sun-care packaging is expected to stagnate over the 2021-2022 period.

- Brands are expected to continue to focus on innovative packaging formats to generate interest and boost demand in beauty and personal care in Colombia. Convenience is also likely to be a driver of development with portable, on-the-go formats becoming more visible. Packaging as a tool of differentiation is predicted to gather momentum over 2021-25 as brands look for ways to differentiate their products and encourage loyalty among younger consumers, with millennials being the primary target for customizable products and packaging.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- Due to the rise in demand for household products during 2020, economical size formats such as larger packs of various types gained prevalence in Colombia. Even flexible plastic formats gained market share in categories such as liquid detergents since they are inexpensive and useful for refill packs as they give consumers the convenience of buying larger volumes at affordable prices. As a result, flexible packaging grew by 43.6% and 12.3% by volume in surface care and dishwashing respectively in 2020.

- Refill packs are also on the rise, with a growing number of brands offering the same. This trend is not only in response to demand for more eco-friendly and socially responsible products, but also caters to the needs of more price-sensitive consumers. The categories in which refill packs are strongest include laundry care products such as fabric softeners, liquid detergents, and color-safe laundry bleach, as well as dishwashing and surface care. As refill packs mostly come in flexible packaging, the format benefitted from this trend.

- Trends

-

- In terms of packaging, consumers are realizing that packaging is not necessarily the cause of higher prices for traditional brands. Discounters are using pack types used by leading brands, such as flexible plastic, but using HDPE and PET bottles. As a result, private labels such as D1, Ara, and Justo y Bueno are establishing a significant presence in categories like surface care, dishwashing, polishes, and laundry care.

- Despite the emphasis on value for money, home care companies are increasingly communicating their environmentally friendly business practices via the internet. Most manufacturers believe that Colombians are not willing to pay a premium for such packaging, even though their concerns regarding sustainability are growing. Unilever, under its FAB line, relaunched its liquid detergent using 100% PET recycled bottles to reaffirm its environmentally friendly credentials among consumers.

- Outlook

-

- Value-for-money packaging is expected to make its mark in Colombia. The pandemic served to strengthen this trend as consumers’ disposable incomes were negatively affected by the measures implemented to contain its spread. This made consumers focus more on affordable pack types when buying home care products. As a result, an increasing trend towards inexpensive pack types is expected to continue which is likely to benefit flexible packaging over 2021-25.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- There was strong growth in demand for flexible plastic in ready meals packaging during 2020, as this is the dominant pack type for refrigerated ready meals. The category grew during the year because consumers working from home preferred meals that required very little preparation due to their busy schedules. Since other plastic trays and flexible plastic are the dominant packaging types for such products. Flexible packaging grew by 6.4% by volume in the segment during

- Demand for dairy packaging declined marginally during 2020. During the initial stages of the pandemic-added lockdown, many consumers sought to stockpile shelf-stable milk. Flexible plastic is the dominant pack type for shelf-stable milk, but brick liquid cartons grew in popularity in 2020. Discounters like D1 offer shelf-stable milk in new aseptic liquid cartons, as it offers better shelf-life and freshness. As a result, flexible packaging declined by 2.0% by volume in 2020.

- Trends

-

- The pandemic is driving accelerated growth in demand for shelf-stable vegetable packaging. Metal food cans remain the leading pack type for these products, but glass jars are also rapidly gaining ground. Glass jars are particularly popular for premium offerings in shelf-stable vegetables but are also being increasingly used by manufacturers of mid-priced brands. Local consumers perceive glass jars as being better able to preserve vegetables than metal food cans. Moreover, glass jars are also perceived as being more environmentally friendly – an increasingly important factor for younger consumers. As a result, glass packaging is expected to grow at 3.3% CAGR by volume over 2021-25.

- Flexible packaging dominates sugar confectionery, with flexible plastic being particularly popular. Flexible plastic can be printed with attractive graphics/imagery and it is easy to transport, store, and it keeps the product freshness intact. These benefits make flexible plastic popular with both consumers and manufacturers. Strong growth is observed in the demand for flexible paper and flexible aluminum/paper packaging in sugar confectionery over 2021-25. Pack sizes of less than 20g dominate sugar confectionery, with the smallest 3g pack size particularly popular as a quick and affordable snack.

- Outlook

-

- Demand for dairy packaging will continue to decline in 2021. However, it will begin to expand again during 2022 as the threat posed by the pandemic is expected to fade and consumer confidence is likely to revive. It is expected that new pack types such as aseptic liquid cartons and stand-up pouches may gain over 2021-25. However, the total demand for packaging units in dairy is not likely to exceed its pre-pandemic (2019) peak until 2023.

- The post-pandemic recovery in demand will be slow, with packaging units in confectionery unlikely to exceed their pre-pandemic (2019) peak until 2023. Growth in demand for confectionery packaging will remain lackluster throughout the entire forecast period. Heightened consumer concern regarding health and wellness – particularly weight management – is likely to be a long-term effect of COVID-19, and this will weigh on growth in demand for confectionery packaging.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Colombia

-

Colombia witnessed fewer cases in May 2022 than in the past two months

- According to the World Health Organization (WHO), Colombia reported 6,099,111 COVID-19 cases and 139,833 deaths as of May 26, 2022.

- In late April, the president of Colombia, Ivan Duque, announced plans to lift the mandatory use of face masks in closed spaces starting May 1, 2020. As per a leading trade press source, this restriction will only be removed in municipalities where the fully vaccinated rate is 70% or higher and at least 40% of the population has had a booster shot.

- Crisis24, a portal that provides news alerts about threats from all over the world, reported that in late April, Colombian officials issued orders to loosen COVID-19 restrictions on travel from May 1, 2022. International travelers are now allowed to visit Colombia without proof of vaccination, provided they carry a negative PCR or antigen test result.

- As of May 2022, 35,778,117 people have been fully vaccinated, equaling 70.3 per 100 persons, and 12,068,192 people have received a booster dose.

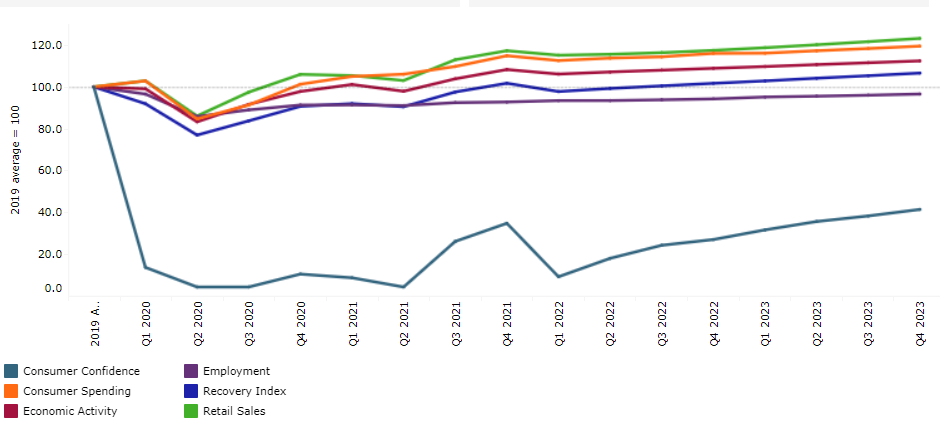

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Colombia

- Impact on GDP

-

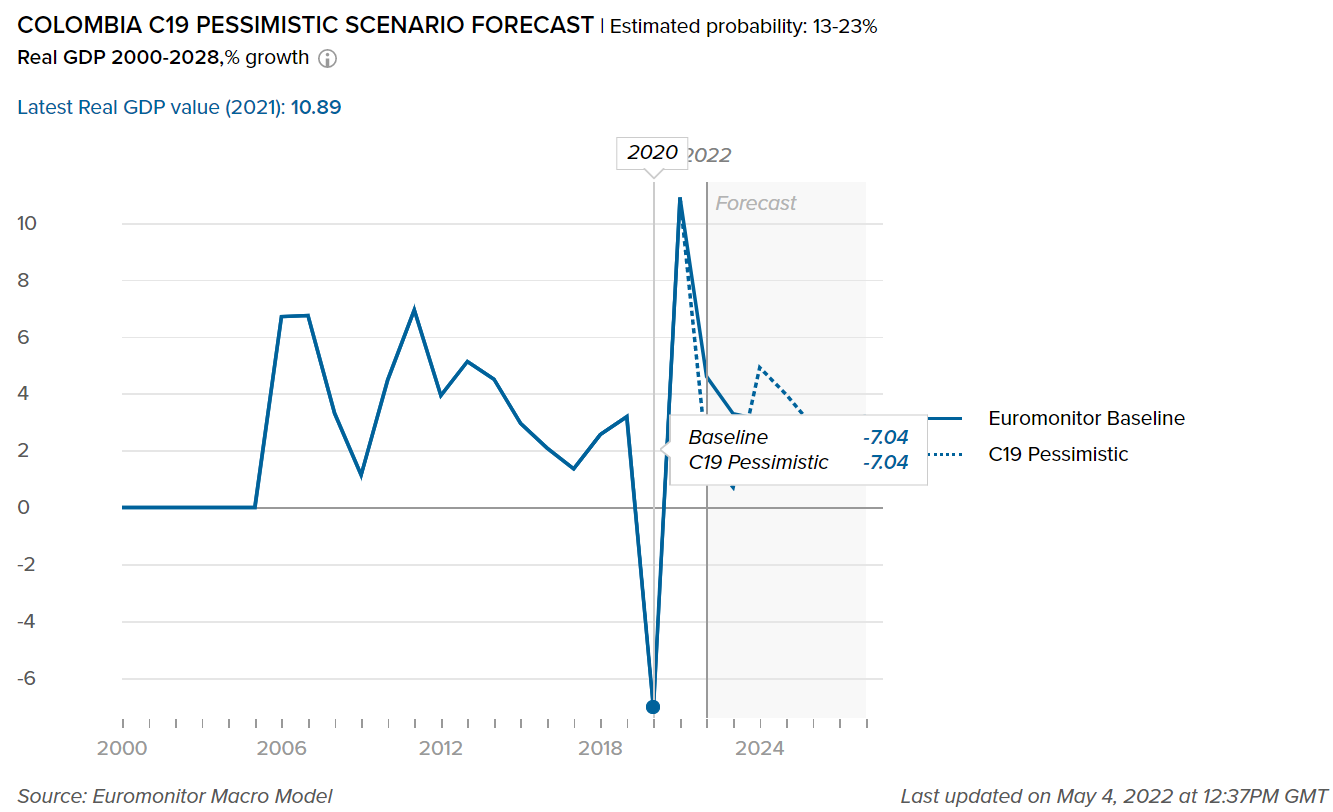

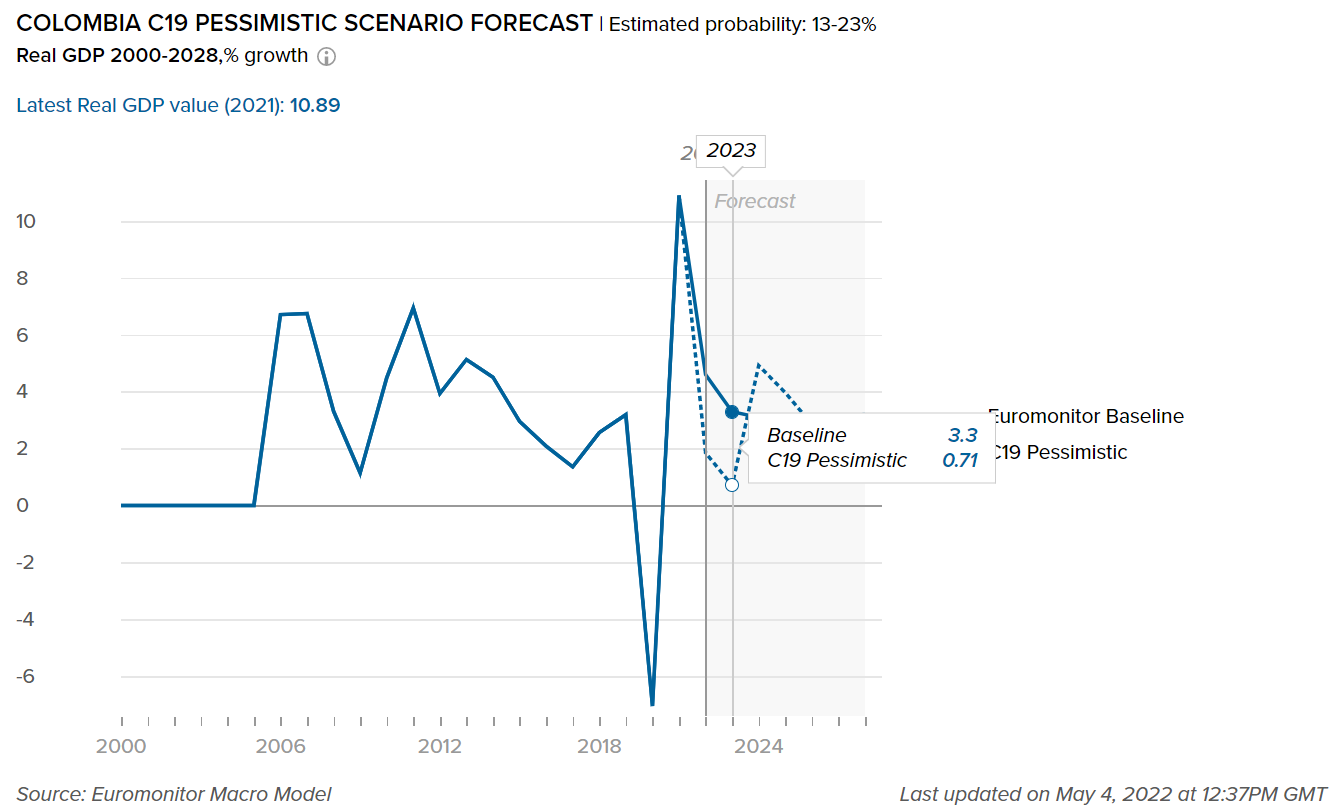

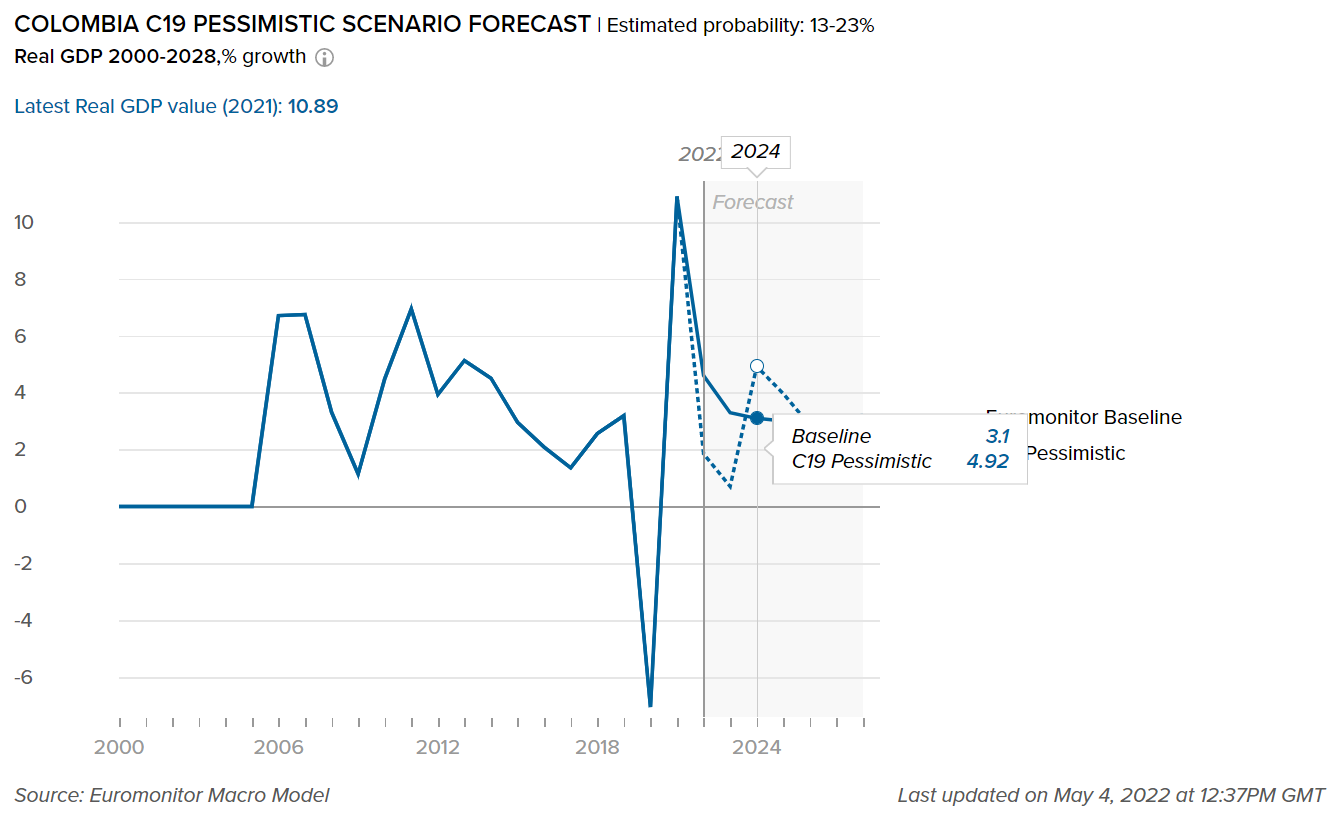

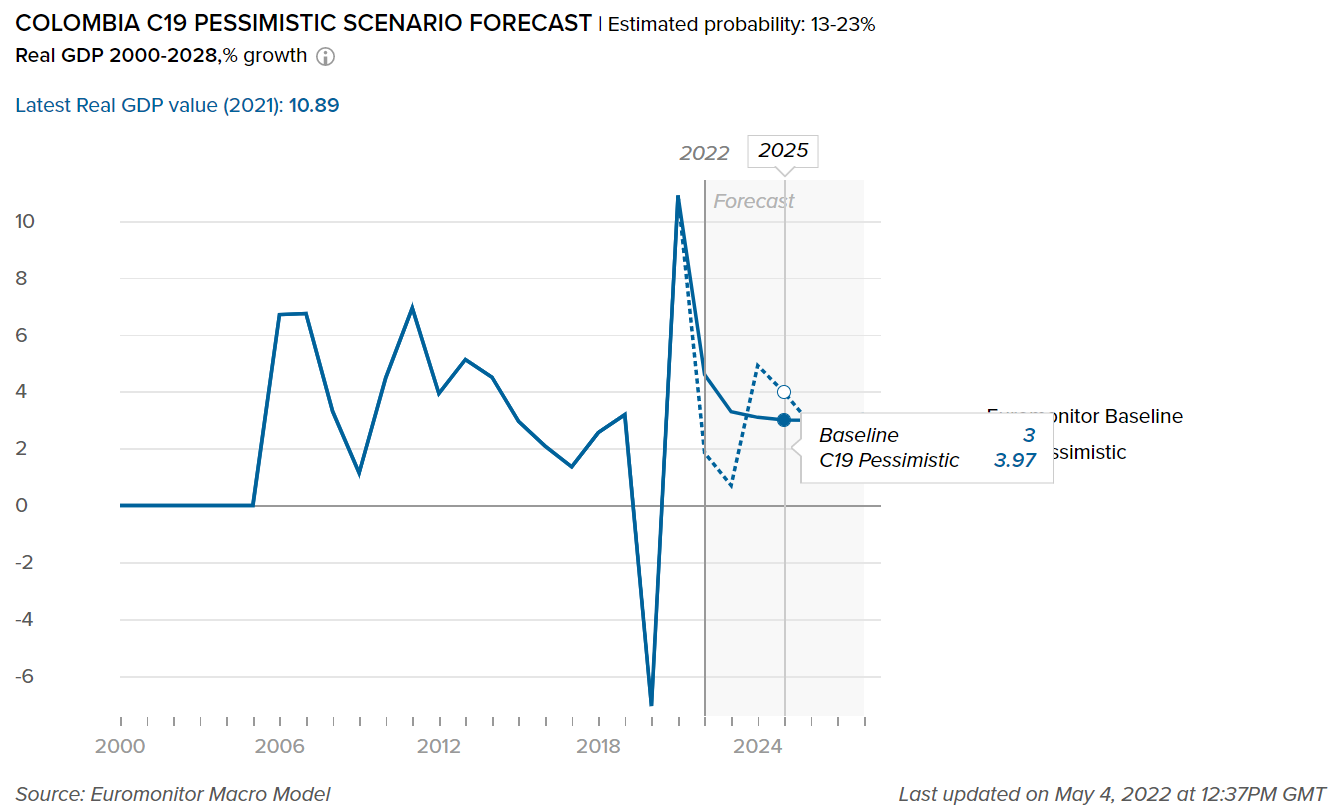

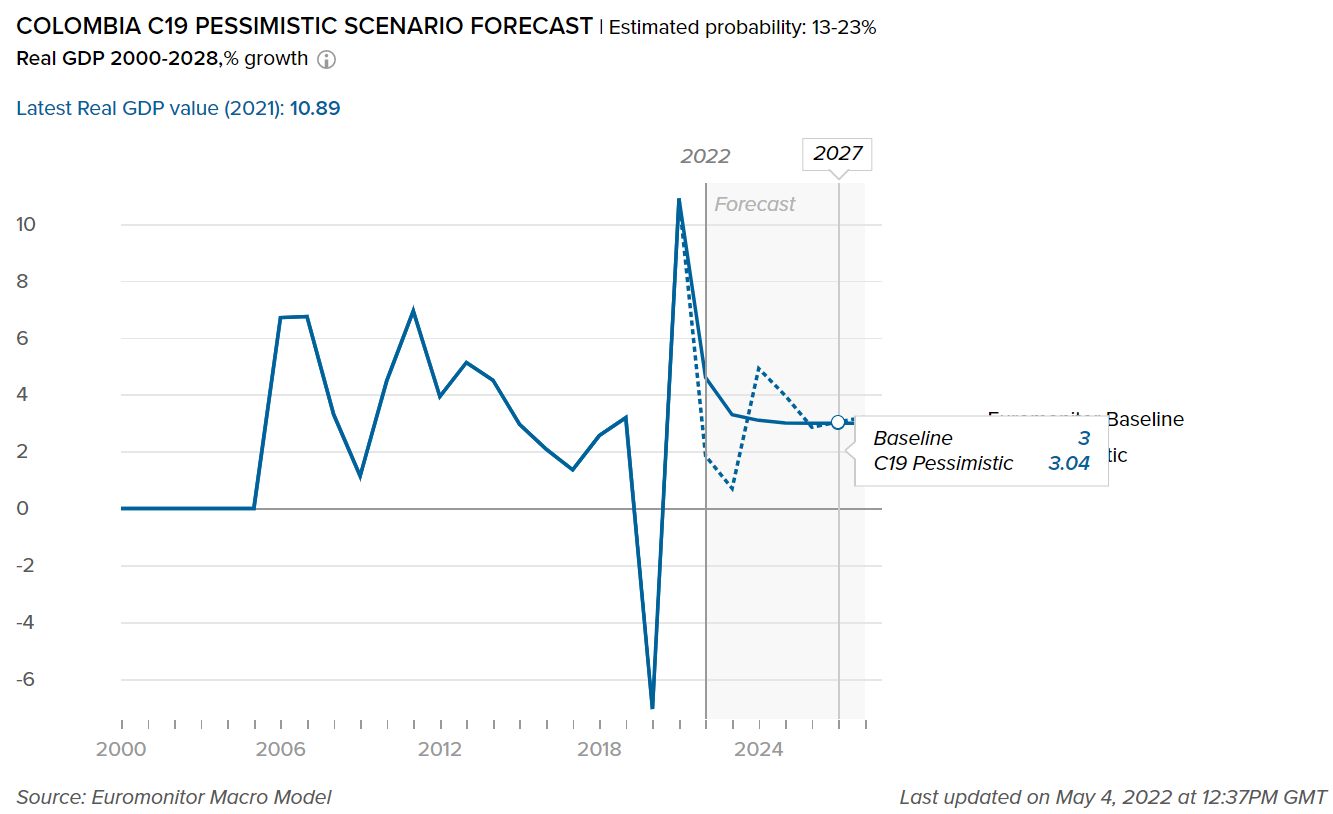

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in Colombia. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

The unemployment rate in Colombia is likely to remain above the Latin American average in the short term

- Following a contraction of 7.0% in 2020, the annual real GDP in Colombia witnessed robust growth of 10.6% in 2021, with the figure being one of the best in the Latin American region. Argentina and Brazil, for example, recorded lower annual real GDP in 2021 than Colombia, with the former at 9.0% and the latter at 4.7%. Higher consumer expenditure was one of the pivotal factors responsible for the economic recovery, as accelerated demand following the opening of the economy led to greater consumption, higher remittance inflows, an increase in exports, and higher investment. The average annual real GDP growth in Colombia is expected to be 3.4% over 2022-2026, outperforming the Latin American average of 2.2%.

- In the short term, the unemployment rate in Colombia is likely to remain above the Latin American average. One of the factors that is expected to add to the elevated unemployment rate in the country is the unstructured labor market, where skill mismatches are ubiquitous. The pandemic further acted as a driving force for mass job losses, a situation from which the employment market is yet to recover. Lower female employment participation is also responsible for the heightened unemployment rate in Colombia. The closure of schools, which resulted in increased household responsibilities, has been a factor that prevented women from joining the workforce.

- Although Colombia is a recipient of higher global oil prices, given that the country is one of the leading oil producers in Latin America, the war in Ukraine is a looming threat to the country’s economy, as it is placing inflationary pressures globally. In March 2022, Colombia observed 8.0% inflation, the highest level recorded since July 2016. The International Monetary Fund (IMF) anticipates inflation falling to 6.75% at the end of 2022.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below shows the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

Health trends strengthen as virus concerns and awareness rise

- The consumption of hot drinks, particularly coffee, as an everyday drink is strongly favored in Colombian culture. Tea consumption, on the other hand, is not as common as Colombians regard tea as a beverage that should only be consumed when one is ill. The sales across this category thus benefited from the pandemic as consumers drank tea to improve their general health and alleviate the symptoms of the virus, while also consuming chocolate-based flavored powder drinks as an indulgence in 2021.

- In 2022, rising health consciousness among Colombian consumers is likely to have an impact on the consumption of hot drinks, particularly high-sugar chocolate-based flavored powder drinks. The introduction of new labeling laws that make it mandatory for brands to clearly mention the sugar content in their products on the packaging will likely lower the demand for high-calorie hot drinks. Parents, in particular, will avoid purchasing such drinks to maintain and improve the physical well-being of their children and themselves.

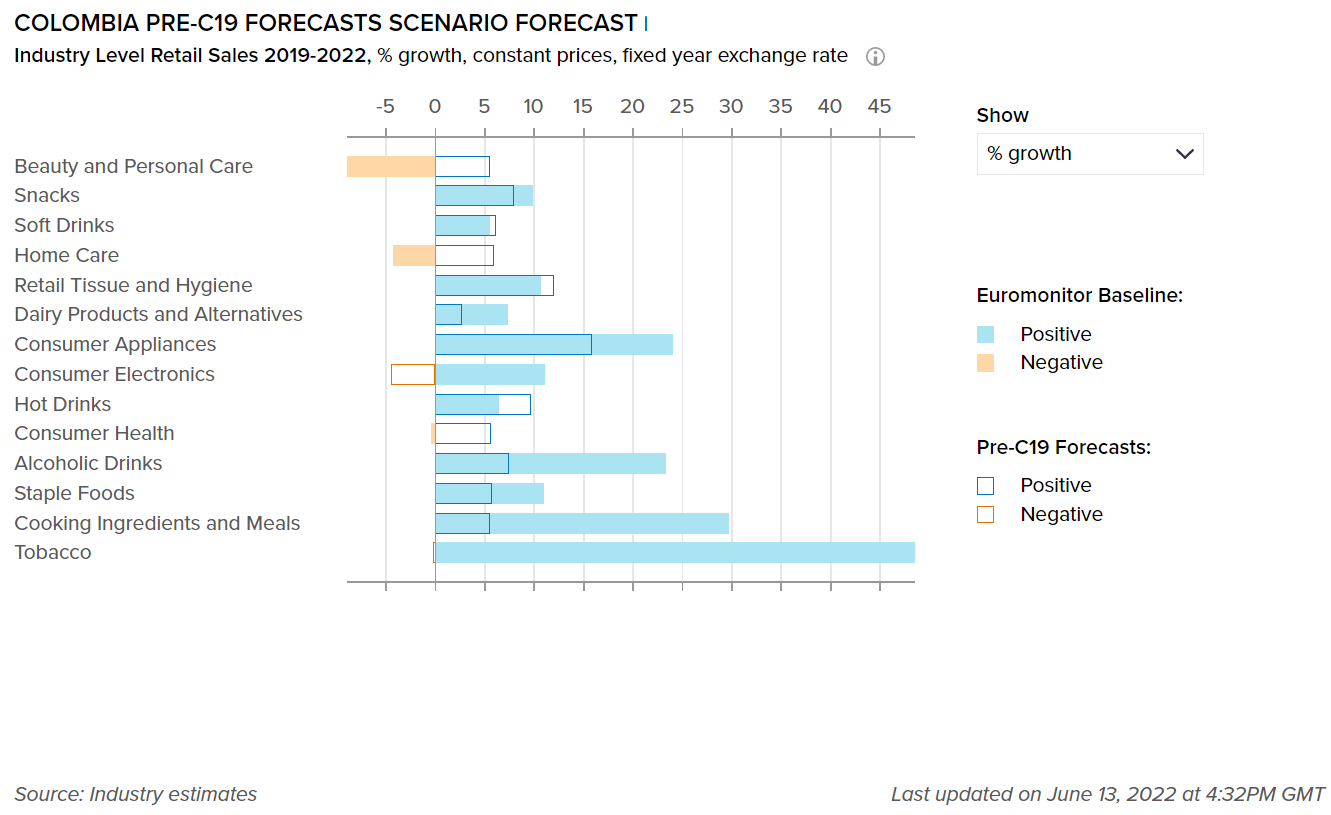

- In 2021, the sauces, dressings, and condiments category witnessed an upsurge in demand. As a result of the spread of the virus, many consumers experienced job or income losses, which limited consumers’ ability and willingness to visit restaurants, reinforcing the habit of home-cooking. Chili sauces witnessed increased demand as consumers explored new recipes to diversify their meals. Local brands such as AyMaría! and Codi experimented with the category of chili sauces by coming up with a variety of different flavors, which further elevated the demand for the category. Expectations are that the retail sales of cooking ingredients and meals will increase by more than 25% over 2019-2022.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors covered in Colombia. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Dairy products and alternatives are expected to witness slow retail volume growth in 2022

- Staple foods witnessed steady growth in 2021. The best-performing categories within staple foods were baked goods, frozen processed fruits and vegetables, and breakfast cereals. Consumers purchased foods that offer convenience. Dessert mixes (for cakes and cookies) continued to record positive retail volume growth in 2021, albeit at a slower pace than in 2020. It is anticipated that retail sales of staple foods will increase by approximately 9% over 2019-2022.

- Dairy products and alternatives are expected to witness slow retail volume growth in 2022. 2021 witnessed 5.6% year-on-year retail value RSP growth, while 2022 is likely to record 4.1% year-on-year retail value RSP growth. The demand for many products will decrease as consumers become less likely to stay and cook at home, owing to the easing of the COVID-19 restrictions and the return to normalcy. This, on the other hand, will boost the retail sales of some products such as yogurt, that are suitable for on-the-go consumption.

- The implementation of a new food labeling system that comes into effect in late 2022 will likely be influential in this regard. This system will empower consumers and make them aware of the sugar, fat, and salt content in the products they intend to purchase. It could also present opportunities for companies selling yogurt and cheese to position their products as healthy substitutes for indulgent snacks, such as confectionery, sweet biscuits, etc.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

1,271

1,302

-7.5

Home Care Packaging

1,148

1,156

5.8

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 21 and Feb 22 data for 2022

Rigid Plastic

7,921

8,176

-0.06

Flexible Packaging

19,105

19,427

-0.14

Metal

1,760

1,879

-0.03

Paper-based Containers

1,211

1,277

-0.87

Glass

7,765

8,256

0.02

Liquid Cartons

1,343

1,320

0.00

Flexible plastic dominates table sauces packaging

- Ketchup and mayonnaise are the most popular table sauces in Colombia. Plastic pouches are one of the significant packaging types for table sauces packaging. The use of flexible packaging for sauces, dressings, and condiments is popular among Colombian manufacturers as this pack type is easy to store. Most of the plastic pouches have plastic screw cap closures, making them convenient to use. Leading players in table sauces, such as Fruco and La Constancia, use plastic pouches, particularly for the 200g pack size.

- Flexible packaging dominates hot drinks packaging in Colombia as this pack type is lightweight, low-cost, and can come in numerous sizes, ranging from single-portion sachets to family sizes of over 1kg. Flexible packaging also provides the convenience of resealable closures and is available in almost all distribution channels. A leading Colombian coffee manufacturer, San Camilo, introduced a new packaging format using sustainable paper pouches to develop a classic premium coffee packaging.

- Flexible aluminum/plastic with plastic screw closures have been introduced in prepared baby food packaging, but the demand for this pack type is very limited as most purchasers prefer glass jar packaging. Brands such as Mah! and Luki, which mainly target older children rather than infants, use this pack type.

- The government of Colombia announced its National Plan for the Sustainable Management of Single-Use Plastics on June 3, 2021. One of the objectives of the plan is to strengthen the development of a circular economy in the country. Sustainable packaging, thus, is expected to become pivotal for industry players over 2022. This will likely boost the use of reusable and recyclable glass bottles in foodservice channels. There is a possibility that Coca-Cola, along with other key players, will carry out such a strategy in Colombia as well in 2022. Another packaging format that is likely to attract players is the use of 100% recycled PET, which was introduced by Postobón, a bottled water player, in late 2020. Taking into consideration the popularity of PET bottles in the soft drinks packaging industry, a gradual switch toward recycled PET is highly expected.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies

The spread of a more infectious and highly vaccine-resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe diseases from new coronavirus variants, with moderate vaccine modifications

Vaccination campaigns progress in developing economies is slower than expected

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and releasing pent-up demand

Longer-lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment, and wages relative to the baseline forecast in 2022-2023

- Recovery Index

-

Recovery Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.