Overview

- Packaging Overview

-

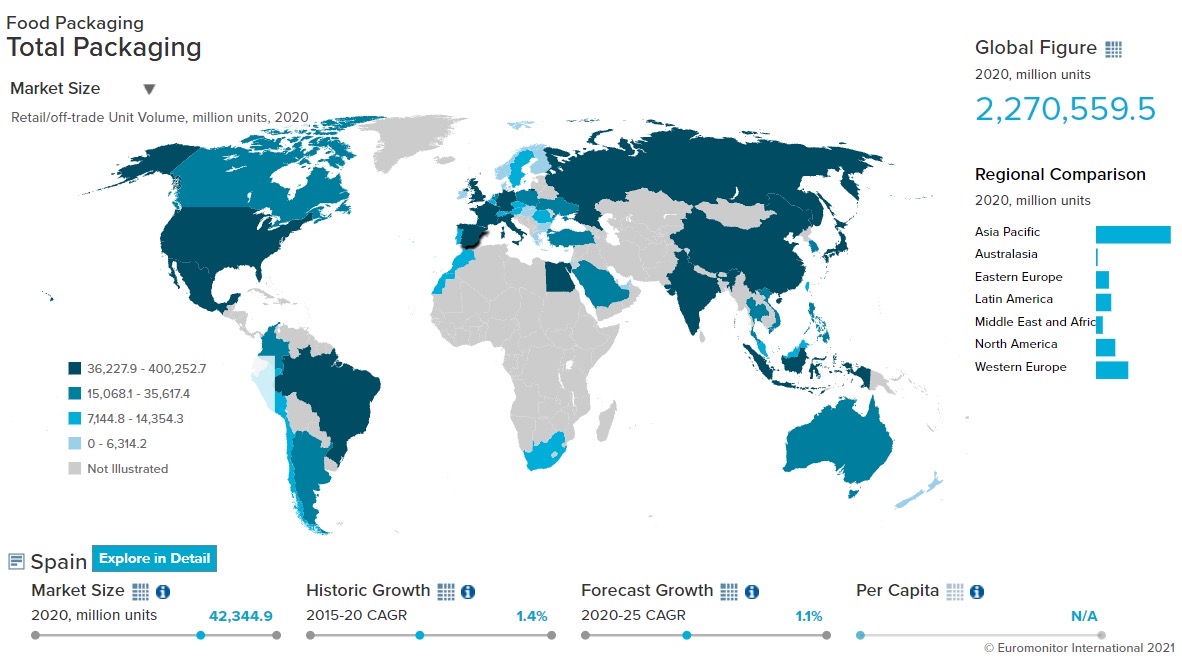

2020 Total Packaging Market Size (million units):

67,973

2015-20 Total Packaging Historic CAGR:

1.7%

2021-25 Total Packaging Forecast CAGR:

-0.8%

Packaging Industry

2020 Market Size (million units)

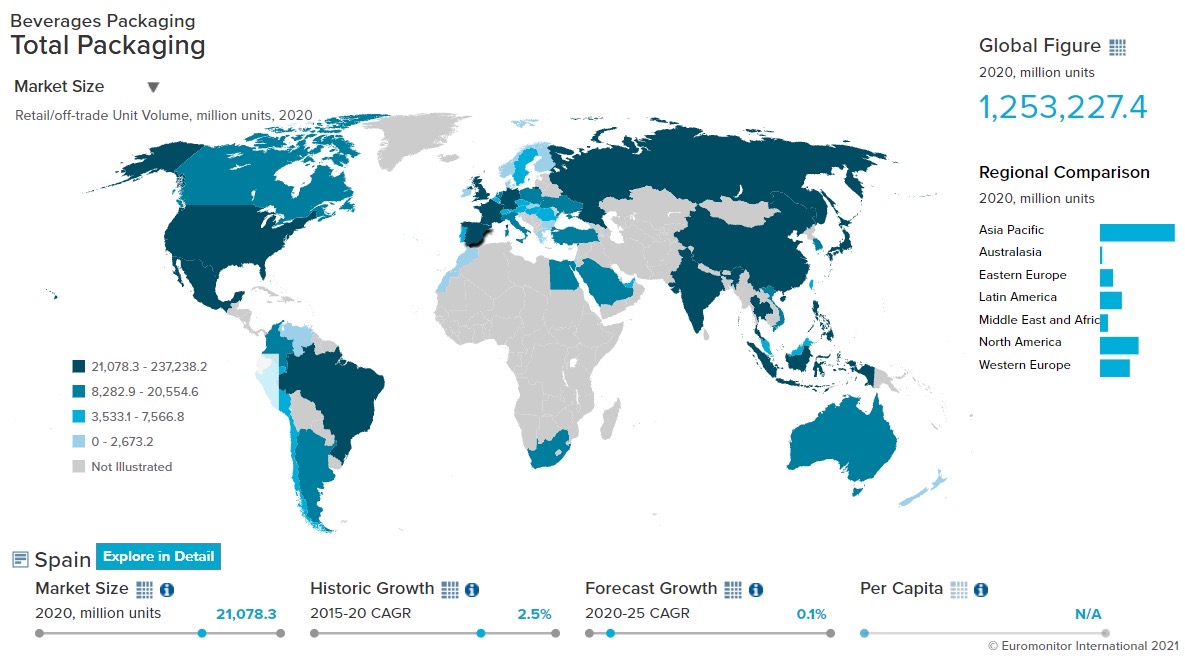

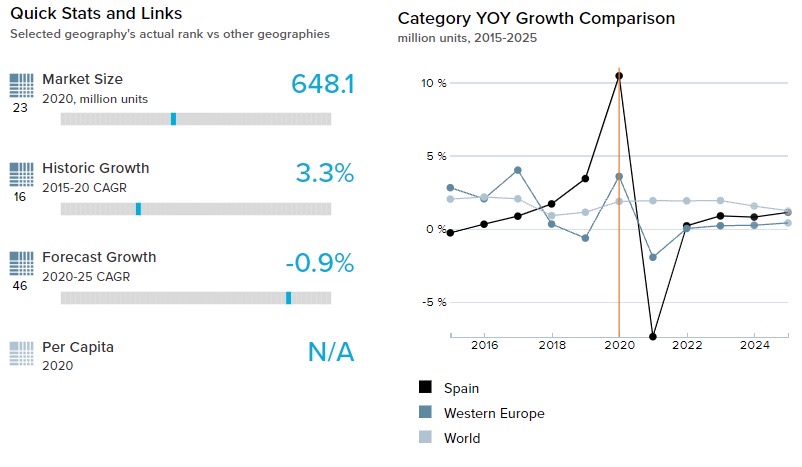

Beverages Packaging

21,020

Food Packaging

42,345

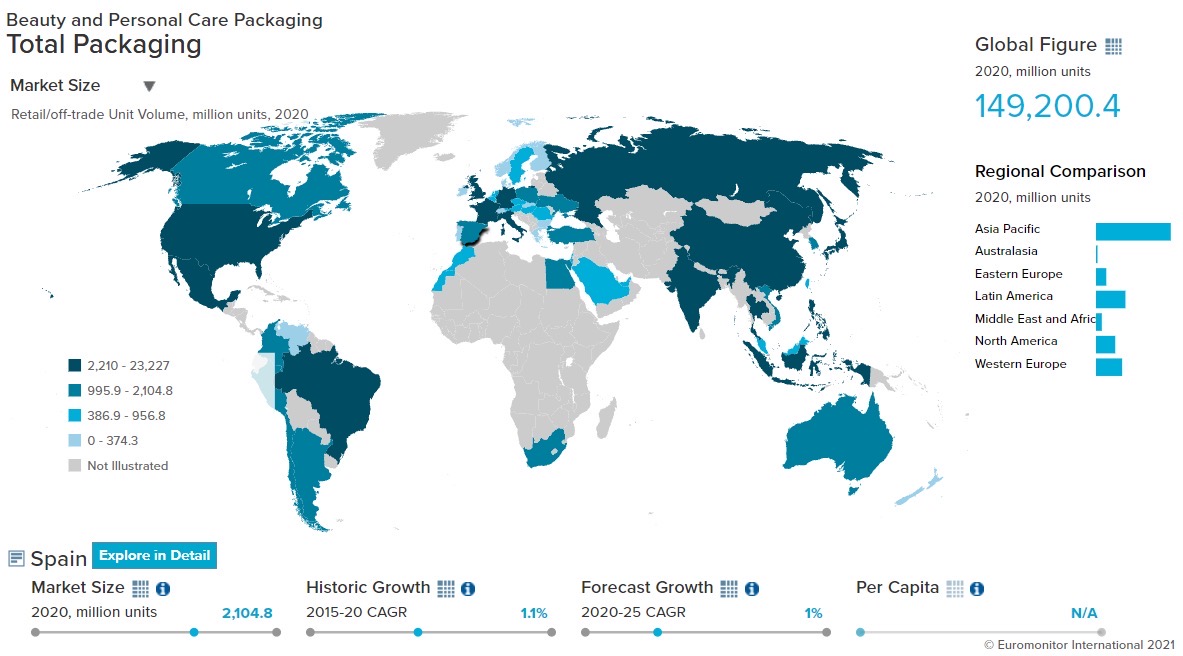

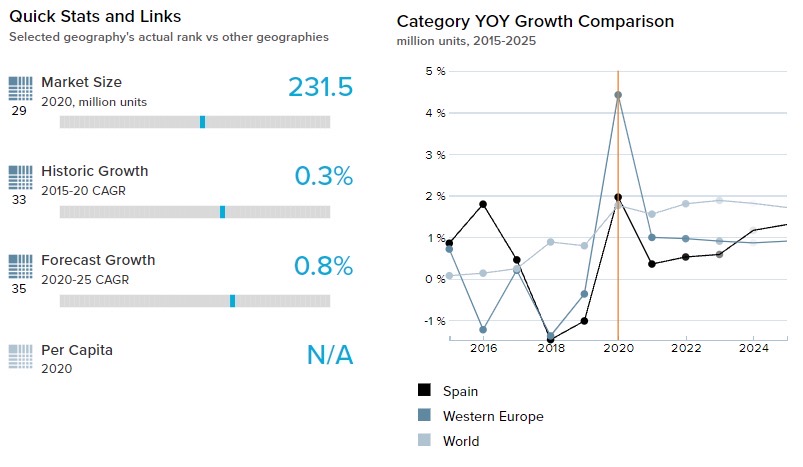

Beauty and Personal Care Packaging

2,105

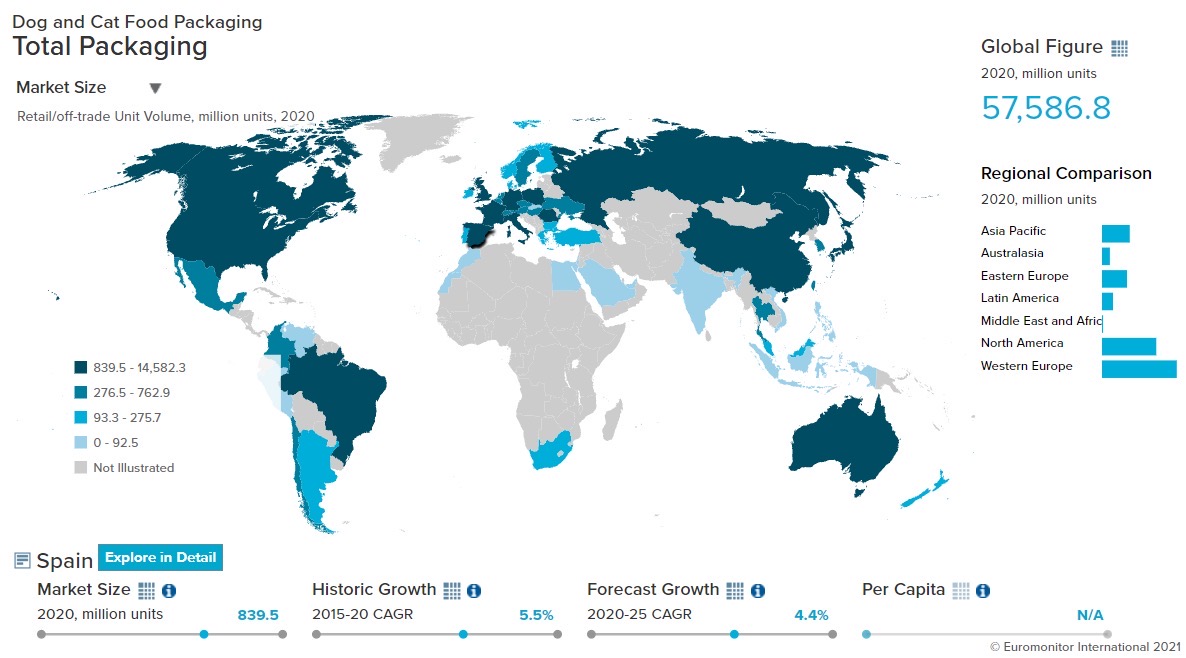

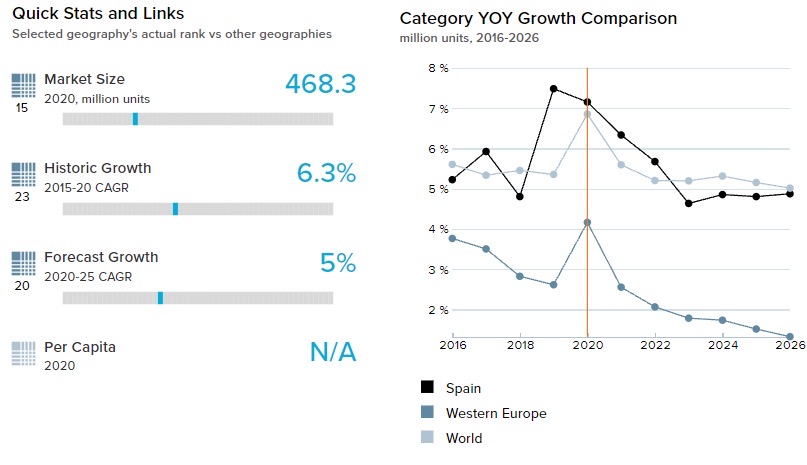

Dog and Cat Food Packaging

787

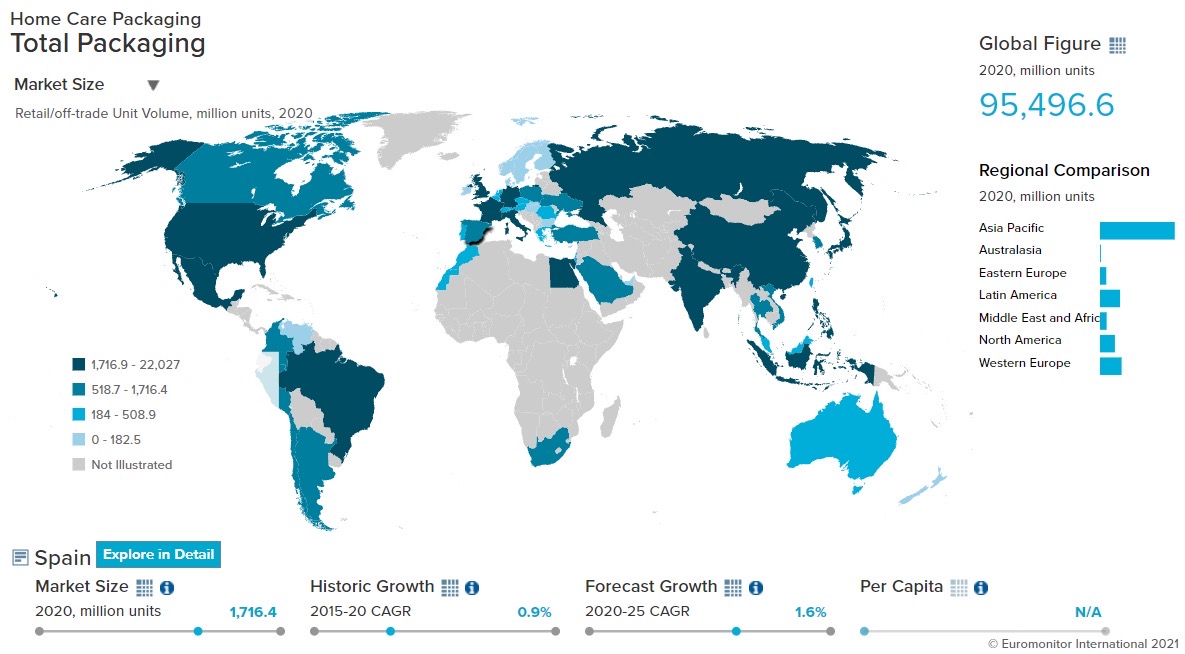

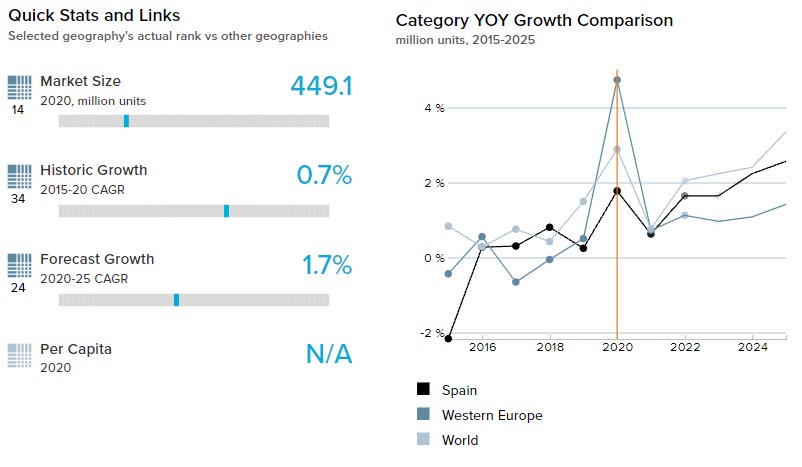

Home Care Packaging

1,716

Packaging Type

2020 Market Size (million units)

Rigid Plastic

24,006

Flexible Packaging

17,785

Metal

9,601

Paper-based Containers

4,723

Glass

6,894

Liquid Cartons

4,927

- Key Trends

-

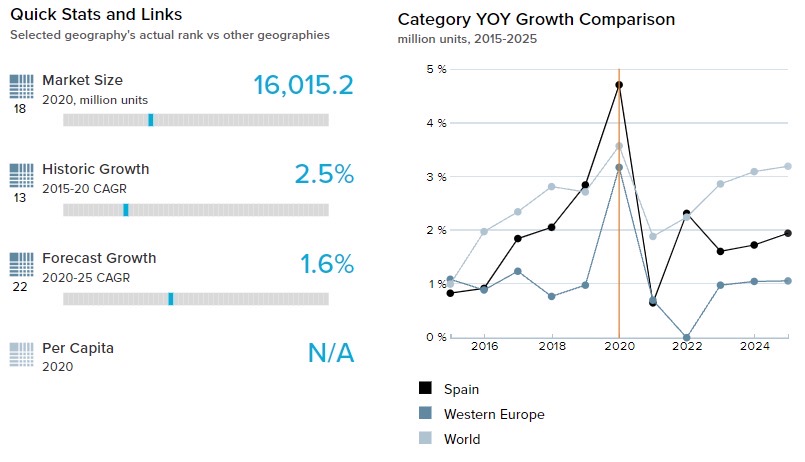

The advent of COVID-19 disrupted the tourism industry of Spain. This severely impacted the sale of small-sized packs that were suitable for on-the-go consumption in beverages, confectionery, and dairy. Furthermore, the popularity of e-commerce is helping the growth of larger packs as they can be delivered with ease at the doorstep. Flexible packaging is benefitting from these trends in chocolate confectionery and home care, while metal food cans gained share in dog and cat food and processed seafood.

- Packaging Legislation

-

New legislation relating to packaging and packaging waste were proposed, but could not be achieved because Spain hasn’t had a stable government since April 2018. Due to this, regions and communities have taken the onus on themselves to bring in new guidelines to fight packaging waste. For example, in February 2020, the Balearic Islands introduced a new law related to contaminated waste and soil and the prohibition of selling products containing microplastics and nano-plastics from 2021.

- Recycling and the Environment

-

7,400 new recycling points were installed in crowded places like sports stadiums, hospitals, and airports during 2018-20, taking the total to 37,800 recycling points. These were made to make recycling more accessible. Apart from focusing on accessibility, the government and organizations are also working on developing innovative and eco-friendly packaging solutions. For example, Ecoembes, a Spanish non-profit environmental organization that promotes sustainably developed a new plastic, bio-bio. It is made from plant waste and can be used in the manufacture of bottles and trays for food and beverages. This material is completely biodegradable in a marine environment and has zero impact on the environment.

- Packaging Design and Labelling

-

Target-based packaging gained ground in packaged foods, especially in ready meals. Manufacturers embraced a more tailor-made approach towards customers by developing packaging aimed at older generations, children, active people, women, and consumers with larger disposable incomes. For example, Golden Foods introduced Mini Meals for children, which shows “funny” cartoony animals and has easy-to-access packaging. For high-income customers, manufacturers focused on communicating the health benefits of their organic and natural products using extensive graphic information printed on the packaging. The health and wellness trend due to COVID-19 further increased the use of such packaging.

Click here for further detailed macroconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- The closure of workplaces and institutions due to COVID-19 shifted coffee consumption from on-trade to retail channels. In Spain, at-home consumption of coffee was led by increased sales of coffee pods and instant coffee. These forms help consumers save time in its preparation and provides a similar taste to what they used to consume through on-trade channels. As a result, the main pack types of coffee, flexible plastic and folding cartons, showed a volume growth of 10.3% and 12.9% respectively in 2020.

- Spain was one of the worst-hit countries in terms of COVID-19 and therefore the government imposed very stringent measures and lockdown restrictions to curb the spread of the virus. Due to this, people feared stock-outs of essential products, such as hot drinks, as they could not go out frequently to the retail stores. As a result, customers bought more hot drinks in large packs like the 1kg flexible plastic packs and 800g composite containers, which showed a volume growth of 12.2% and 11.3% respectively in 2020.

- Trends

-

- Owing to the health benefits of juice over carbonates and increased focus on personal health due to the pandemic, Spaniards are shifting from carbonates to juice. This was reflected in packaging as well, as carbonates packaging showed a volume decline of 5.4%, while juice packaging showed a volume growth of 3.3% in 2020.

- Similar to the trends in other beverages, alcoholic drinks consumption also shifted from on-trade establishments such as bars and restaurants to homes. This increased the demand for those pack types that were convenient to carry and easy to stock. As a result, metal beverage cans, which are light in weight and come in multi-packs of 6, 12, and 24, showed a volume growth of 13.2% in 2020.

- Outlook

-

- A tax on plastic waste is expected to be introduced over 2021-25 and is likely to negatively impact plastic packaging like those used in plastic coffee pods. As a result, flexible aluminum/plastic and flexible plastic are expected to show a volume decline at a CAGR of 6.6% and 1.0% respectively over the same period. Responding to this, leading players such as Nespresso recently launched coffee pods using 80% recycled aluminum, a trend that is expected to be followed by other players also.

- Sustainability is expected to remain the central theme for innovations in soft drinks packaging where major companies look to increase the use of recycled material in their soft drink PET bottles. For example, Coca-Cola’s World Without Waste strategy has been applied in Spain in which 100% of the company’s packaging will be recyclable by 2021-22.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- The variety in terms of product offerings in dog and cat food increased during 2015-20. Products like dog and cat treats and mixers gained popularity showing a volume CAGR of 8.1% and 11.1% respectively over 2015-20. As these products are purchased, depending on the size and requirements of pets, manufacturers introduced their products in various sizes. For example, Alpha Spirit, a premium brand that launched dog treats in a 50g pack, is a new format in this category. Also, the new Rex dry dog food was launched in a flexible plastic pack of 14kg, which is also a new format in its category.

- Owing to their convenience in terms of storage and ability to keep contents fresh, stand-up pouches like aluminum/plastic pouches and metal packaging like aluminum trays continued to dominate the dog and cat food packaging with a volume share of 38.9% and 42.1% in 2020.

- Trends

-

- The popularity of using e-commerce websites for shopping increased further with the advent of the COVID-19 pandemic. Therefore, manufacturers demanded pack types such as thin-walled plastic containers, flexible aluminum/plastic, and metal food cans that are sturdy and able to withstand transportation risks. As a result, these pack types showed a volume growth of 23.1%, 8.6%, and 6.1% respectively in 2020.

- Plastic pouches recorded a strong growth of 12.8% in volume terms in 2020. This is because they come with zip/press closures that makes them resealable, keeping the contents fresh and moisture-free. Zip/press closures also showed a volume growth of 12.8% in 2020.

- Outlook

-

- According to a 2020 survey by IBM analytics, 43% of consumers consider the sustainability of the packaging before making a purchasing decision and believe that it adds value to the brands. Therefore, sustainability is expected to be an important purchase decision factor. As a result, metal packaging, which is eco-friendly as it can be easily recycled, is expected to show a volume CAGR of 3.2% over 2021-25.

- The growth of e-commerce is changing the packaging needs of both the consumers and the manufacturers. Now, packaging needs to be functional, safe, and efficient in terms of delivery and preservation of food. As people are expected to continue buying large pack types to reduce their trips outside, the most suitable and practical pack type, plastic pouches, are expected to grow at a CAGR of 8.7% in volume terms over 2021-25.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- The closure of salons due to the COVID-19 pandemic contributed to the growth in demand for beauty and personal care products for home consumption in 2020. For example, for depilatories, consumers adopted at-home hair removal solutions due to the movement restrictions. This resulted in an increase in its main packaging format, flexible packaging, such as blister and strip packs, and showed a volume growth of 4.6% and 1.6% respectively during the year.

- In haircare, the sales of flexible aluminum/plastic and plastic pouches increased showing volume growth of 8.3% and 13.3% respectively in 2020. These are commonly used as refill packs and have a lower price point in comparison to other packaging formats. As a result, they were in demand as the decrease in disposable income has made consumers look for economical options.

- Trends

-

- Bath and shower products showed a strong value growth of 23.5% in 2020 as COVID-19 increased the focus on personal health and hygiene, benefitting brands like Sanex and Dove. As a result, bath and shower packaging showed a strong volume growth of 24.7% in 2020.

- Spanish consumers sought hygienic products not just in bath and shower products but also in other segments like deodorants. In June 2021, Sanex launched products under their BiomeProtect range, including shower gel, bath foam, and deodorant, which used pre-and postbiotics to support the skin’s microbiome.

- Outlook

-

- Over 2021-25, for hygiene-related products like bath and shower, large pack sizes are expected to be in demand as these are expected to remain an essential item that people are likely to stock. For the perceived non-essential products like fragrances or make-up products like lips, eyes, and nail care, smaller packs/kits are expected to be in demand as smaller packs are suitable for trials and stay within the consumer’s budget.

- Sustainable and environmentally friendly packaging is expected to witness a rise in adoption over 2021-25, as consumers are becoming aware of the harmful effects of waste on the environment. Companies already started taking steps towards this direction, a trend that is expected to catch on. For example, in 2020, Instituto Español launched the first shower gel packaged in a plastic bottle made of recyclable plastic, meanwhile Head & Shoulders launched a range of products in Spain presented in bottles composed of recycled beach plastic.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- Plastic bottles continued to dominate laundry packaging with a volume share of 72.1% in 2020. However, plastic pouches are growing at a very strong rate, taking share from HDPE bottles because of the popularity of liquid tablet detergents. As a result, plastic pouches showed a volume CAGR of 11.8% while HDPE bottles showed a volume decline at a CAGR of -2.3% over 2015-20.

- COVID-19 helped increase the popularity of the e-commerce channel, due to the convenience in terms of home delivery and transportation. This benefits pack types that provide convenience in terms of storage and transportation. As a result, flexible plastic and PET bottles, that can be used to store products for a longer time and do not get damaged during delivery, showed a volume growth of 1.3% and 2.3% in 2020.

- Trends

-

- The World Health Organization (WHO) recommended regularly disinfecting households to eliminate the spread of the COVID-19 virus, which helped the sales for surface cleaners and home insecticides. This increase in consumer demand due to the rising need to keep the surroundings clean helped HDPE bottles grow by 4.4% in volume terms, and metal aerosol cans by 5.8% in 2020.

- The COVID-19 induced economic uncertainty resulted in a reduction in disposable income and a preference for home care products that have multiple uses or benefits. For example, brand owners like Henkel introduced Wipp Express Discs 4en1, the very first detergent on the market, that combines the power of four different functions in a single tab. This trend helped PET bottles, the main pack type of laundry care, show volume growth of 3.4% in 2020.

- Outlook

-

- Glass packaging is expected to show modest growth over 2021-25 as it is considered to be a more premium packaging format compared to other pack types like plastic pouches, PET, and HDPE bottles. Also, with the lockdown restrictions expected to ease and lessen, the need for stockpiling will likely decrease and help glass bottles record a volume CAGR of 1.5% over 2021-25.

- Consumers are increasingly becoming aware of climate change and the ill effects of single-use plastics. As a result, there is a rise in demand for products that are packed in environmentally friendly or recycled materials, with this trend expected to continue to grow over 2021-25. This is prompting leading players to bring sustainable materials into mainstream packaging. For example, Procter & Gamble stated its plans for the reduction of plastic content in Ariel and Lenor packaging, using only 100% recyclable plastic by 2022.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- Over 2015-20, several companies in confectionery invested in stand-up pouches. This was due to a rising trend of sharing confectionery with a group of friends, for which plastic pouches were useful. For example, in 2018, Nestlé launched Kit Kat Bites in practical stand-up pouches, targeting millennials and the rising sharing trend. This shift to plastic pouches accelerated during COVID-19 in 2020 as demand for chocolate pouches was boosted because they were ideal for at-home consumption. Plastic pouches saw a volume growth at a CAGR of 14.9% over 2015-20.

- To supplement their daily meals with protein, Spaniards are buying processed meat as it is easy to store and prepare. Flexible plastic, which recorded a volume share of 49.8% in 2020, owing to its transparency which allows consumers to check the quality of meat before purchase. The format showed a volume growth of 8.8% in 2020.

- Trends

-

- The COVID-19 induced panic sales and fear of stock-outs increased the sales of shelf-stable ready meals as they keep for a long period. Also, the rising popularity of traditional Spanish dishessuch as cocido Madrileño (a chickpea-based stew) and fabada Asturiana (a white bean-based stew) in ready meals is helping the growth of this segment. This helped metal food cans, the main pack type of shelf-stable ready meals, to record a volume growth of 8.8% in 2020.

- The birth rates in Spain were on a declining trend over 2015-20. The main reasons for this were: high youth unemployment, low wages for young and inexperienced employees, and a rising preference to starting a family at an olderage. With the COVID-19 pandemic also adding further uncertainty to households in Spain in 2020, it resulted in the decline CAGR of -1.6% in baby food, and a consequent decline CAGR -1.5% in baby food packaging in volume terms over 2015-20.

- Outlook

-

- In dairy products, PET bottles are expected to take share from HDPE bottles, as PET bottles are expected to show a volume CAGR of 12.8% over 2021-25. This is due to two reasons. First, it is perceived to be modern packaging by Spaniards and is considered safe in terms of health risks. Second, private label products are gaining popularity in Spain and this trend is expected to continue over 2021-25, for which PET bottles are the main pack type.

- Players in confectionery products are moving towards sustainable and recyclable packaging as consumers are becoming more aware of climate change and packaging’s role in it. For example, Nestlé pledged to make all its packaging 100% reusable and recyclable by the end of 2025. Also, Mondelez, moving in line with its zero-waste policy, announced use of recyclable packaging by 2025.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Spain

-

Spain ends indoor face mask rules, however, retains COVID-19-related travel rules until June 2022

- According to the World Health Organization (WHO), Spain had 12,280,345 total COVID-19 cases, with 106,105 deaths and 259,448 cases per million inhabitants reported by May 2022.

- As of April 2022, the Spanish government approved the termination of the mandatory use of face masks in most indoor settings. Masks will no longer be required in the workplace, but will be required on public transit, as well as at health facilities, nursing homes, and pharmacies.

- Separately, the Spanish government stated that the existing COVID-19 entry criteria for all travelers will be extended until June 15, 2022. As a result, all travelers will be subject to COVID-19 entry rules when they arrive in Spain; meaning that COVID-19 evidence is necessary for all travelers over the age of 12 arriving from the European Union/European Economic Area.

- According to the WHO, on May 15, 2022, Spain’s total vaccinations reached 101,466,700. The percentage of the population that has been fully vaccinated is 78.8 per 100 people.

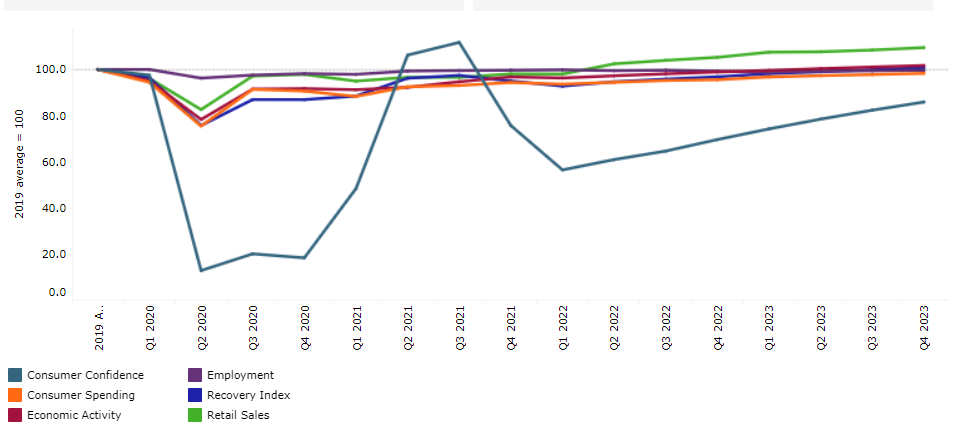

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Spain

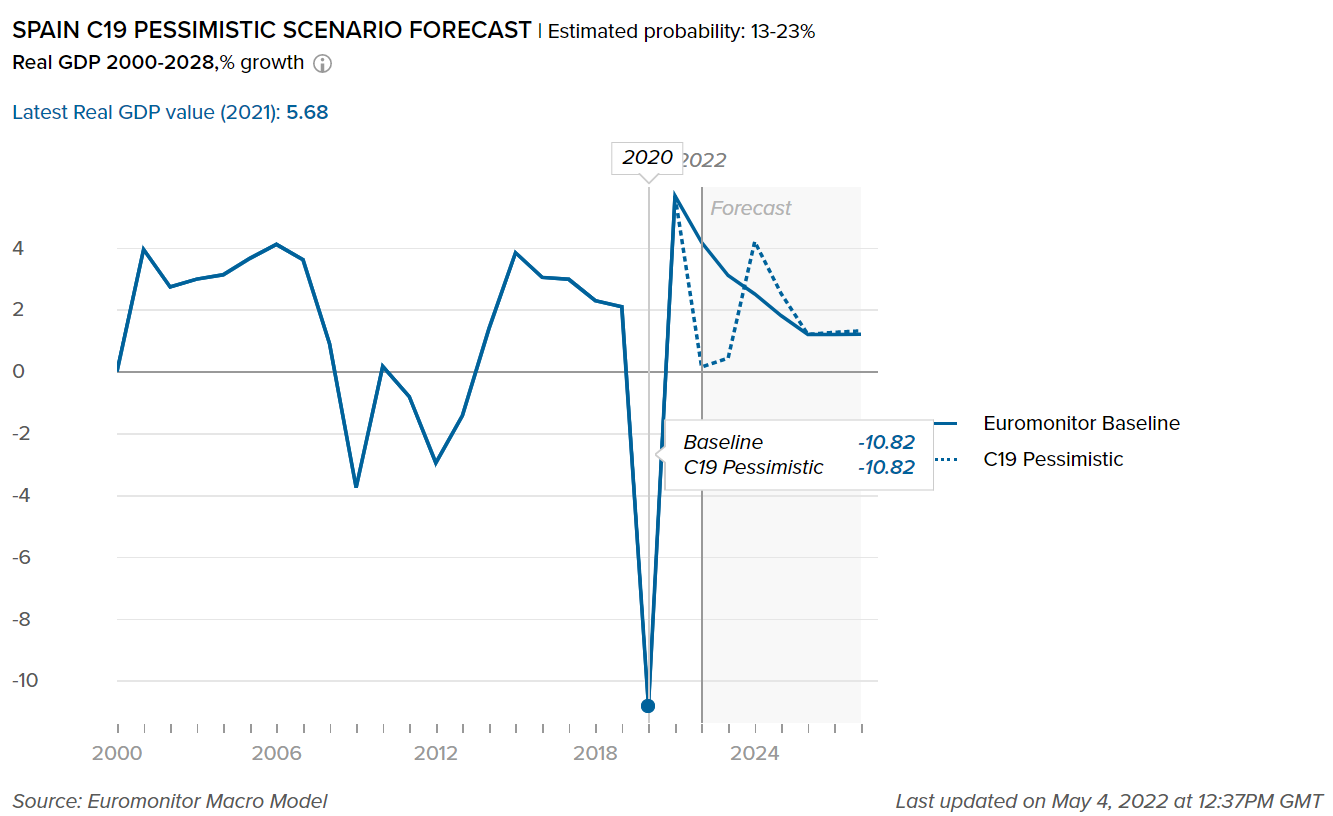

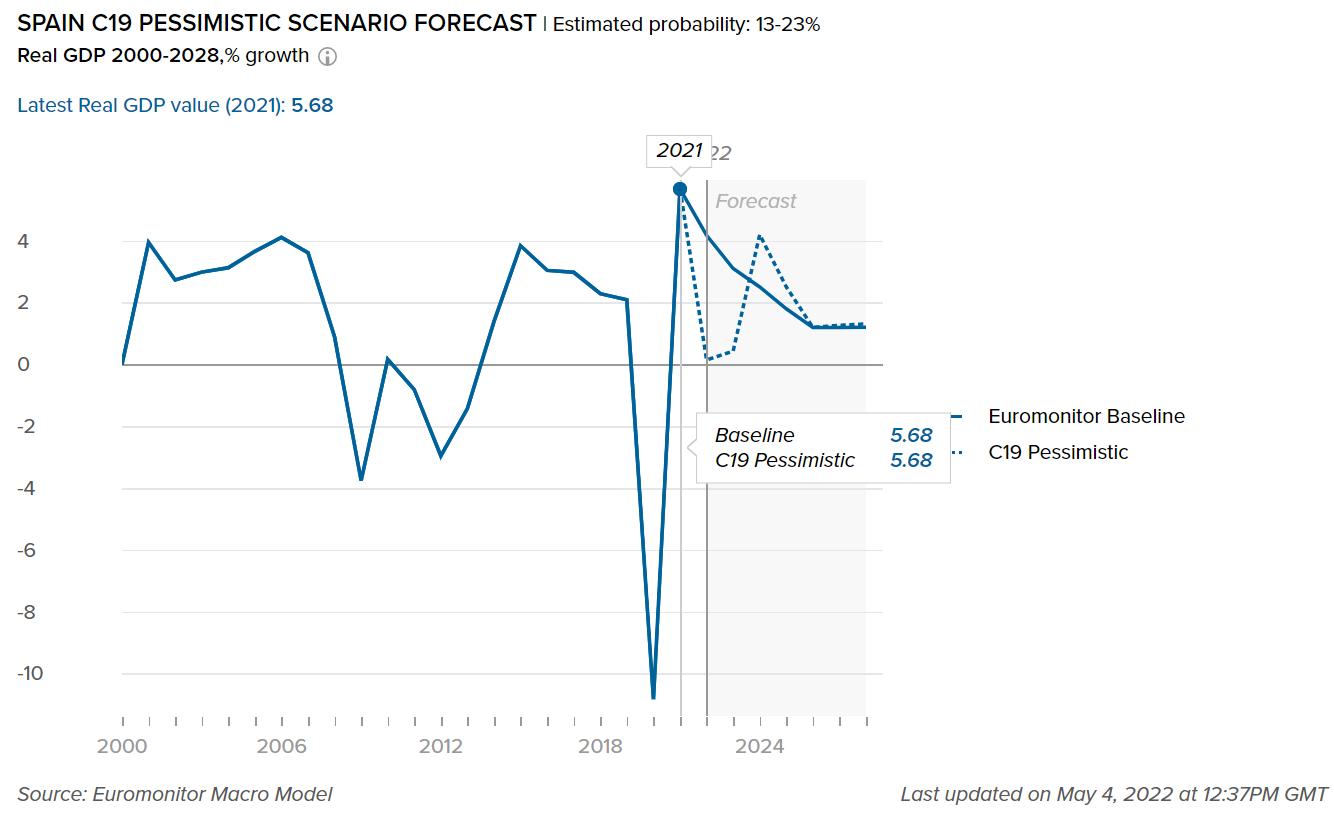

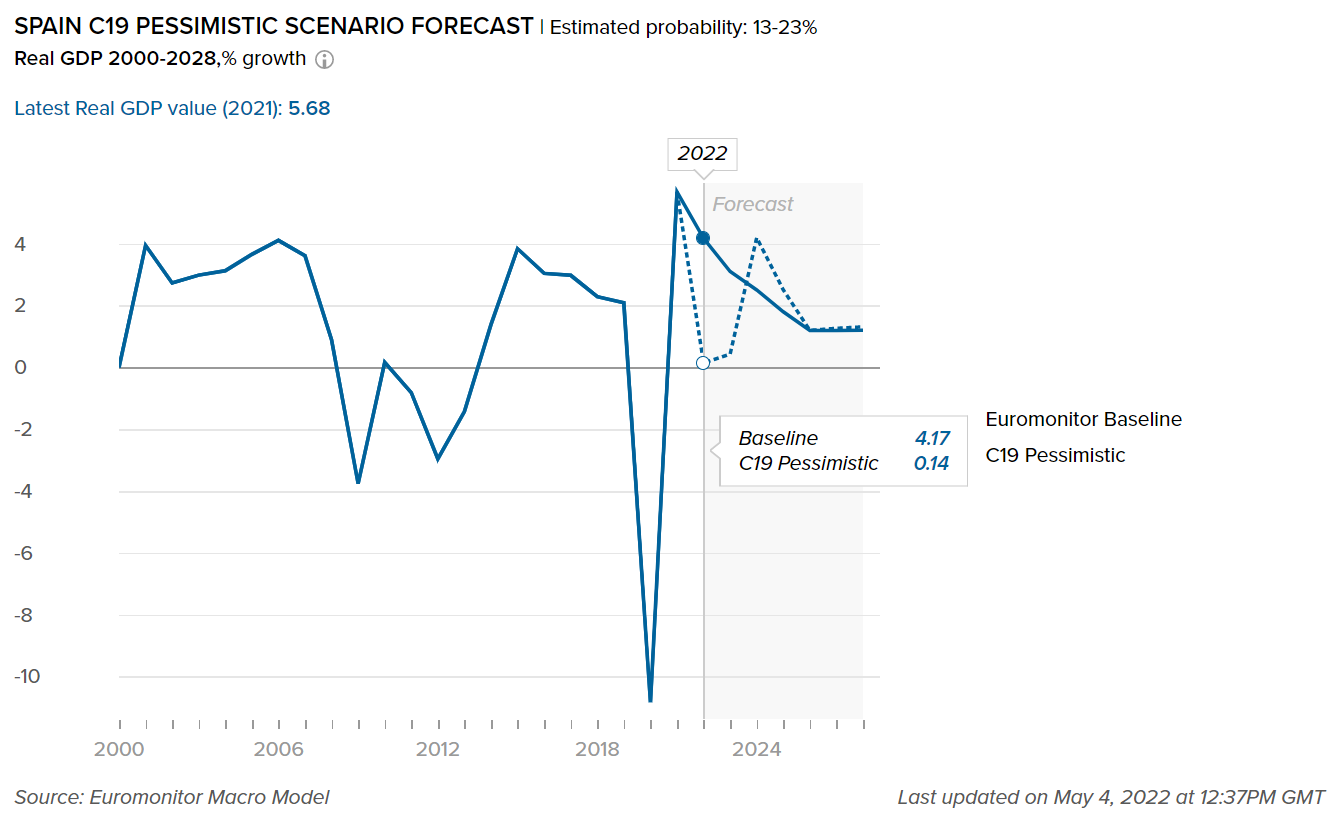

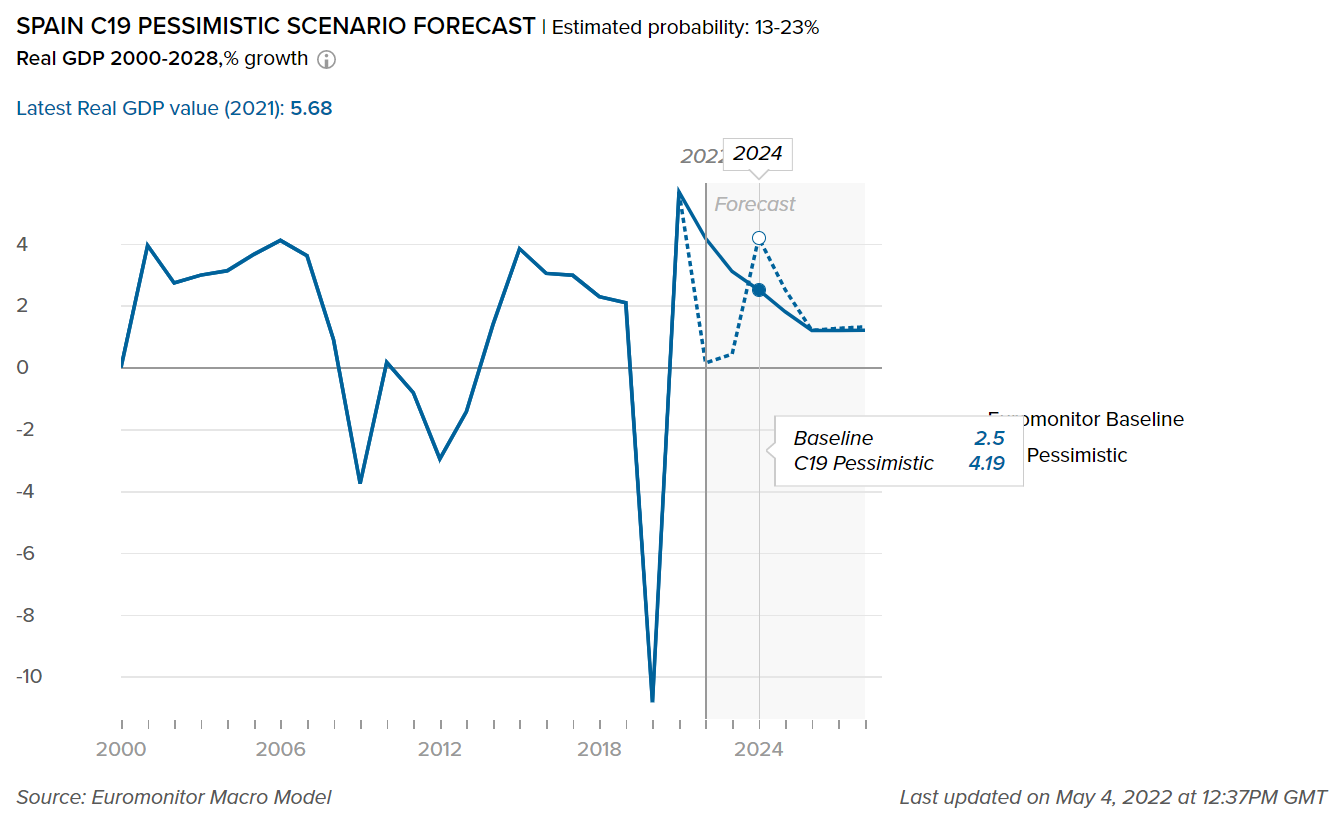

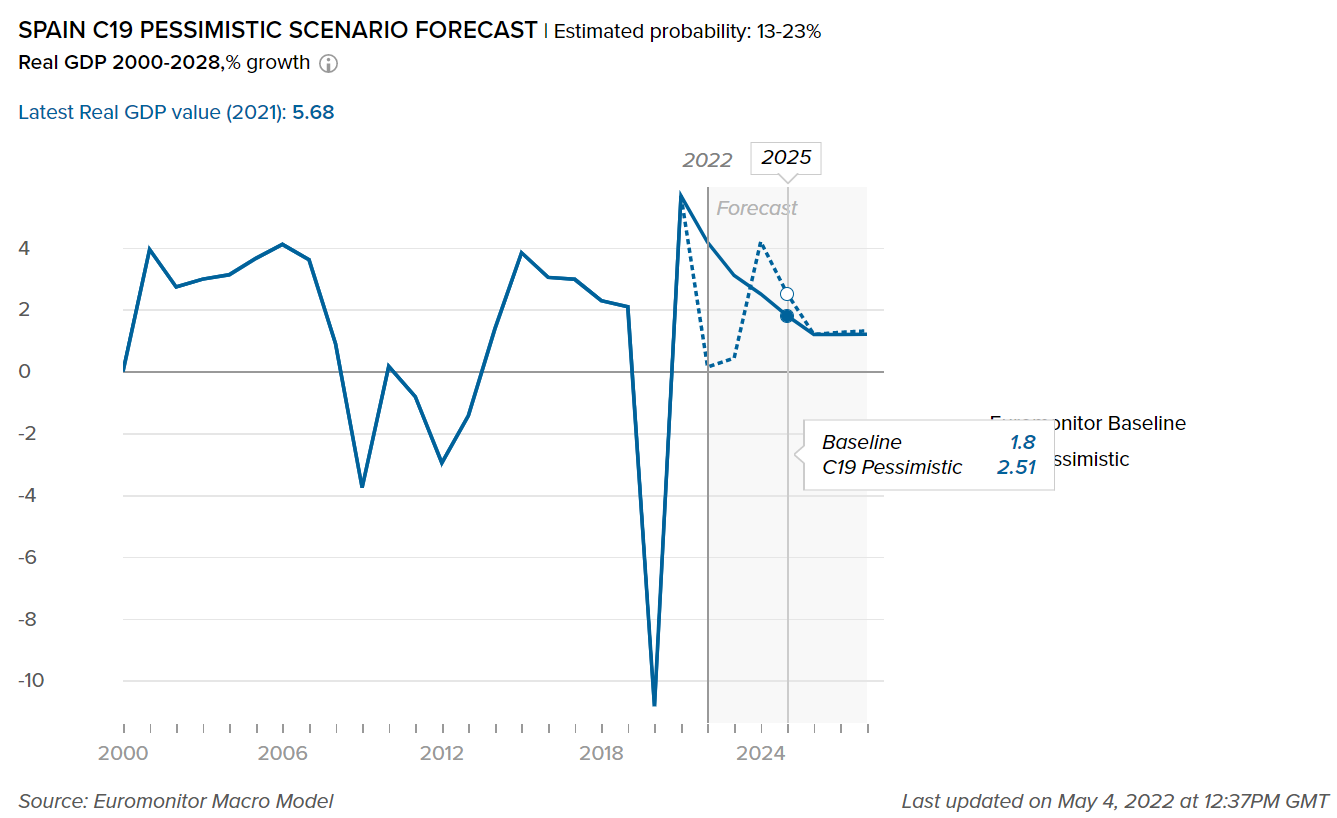

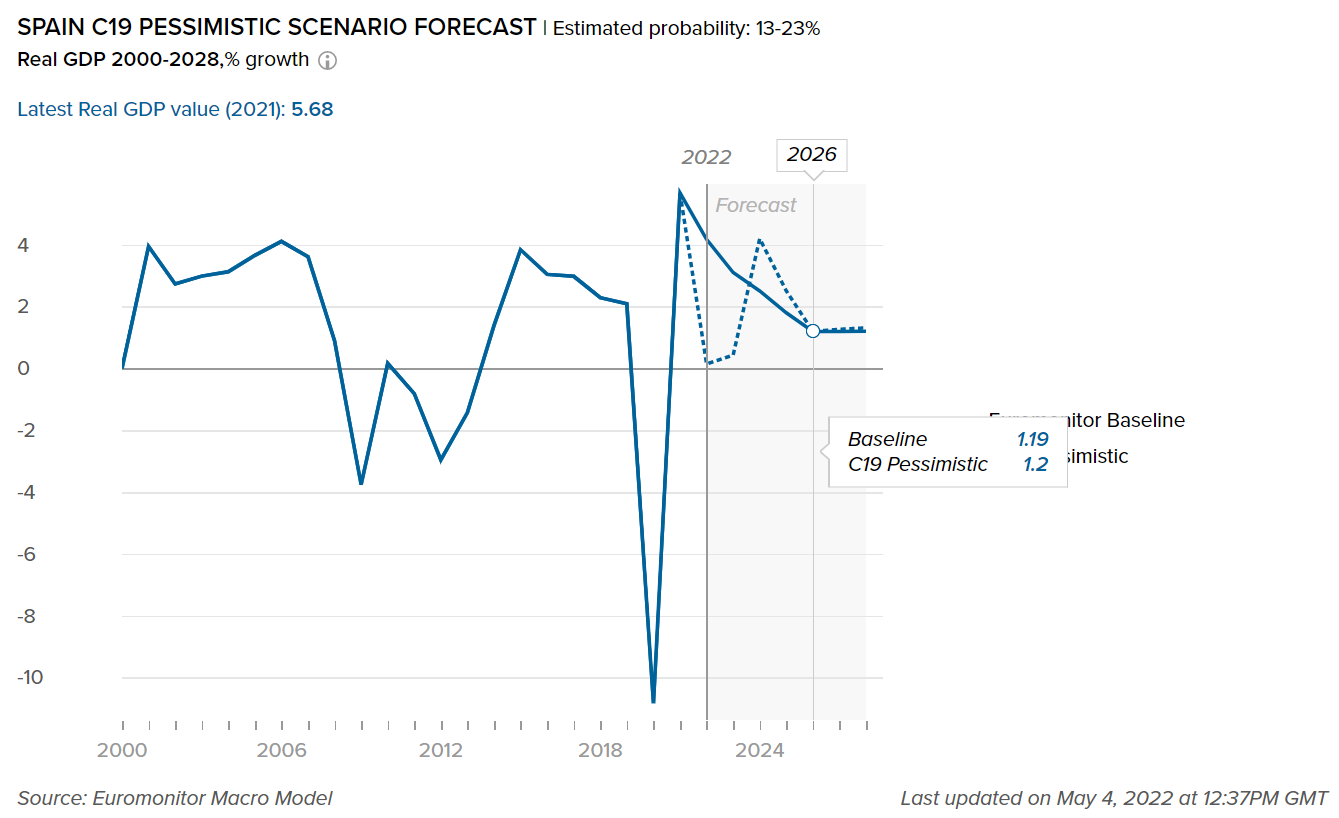

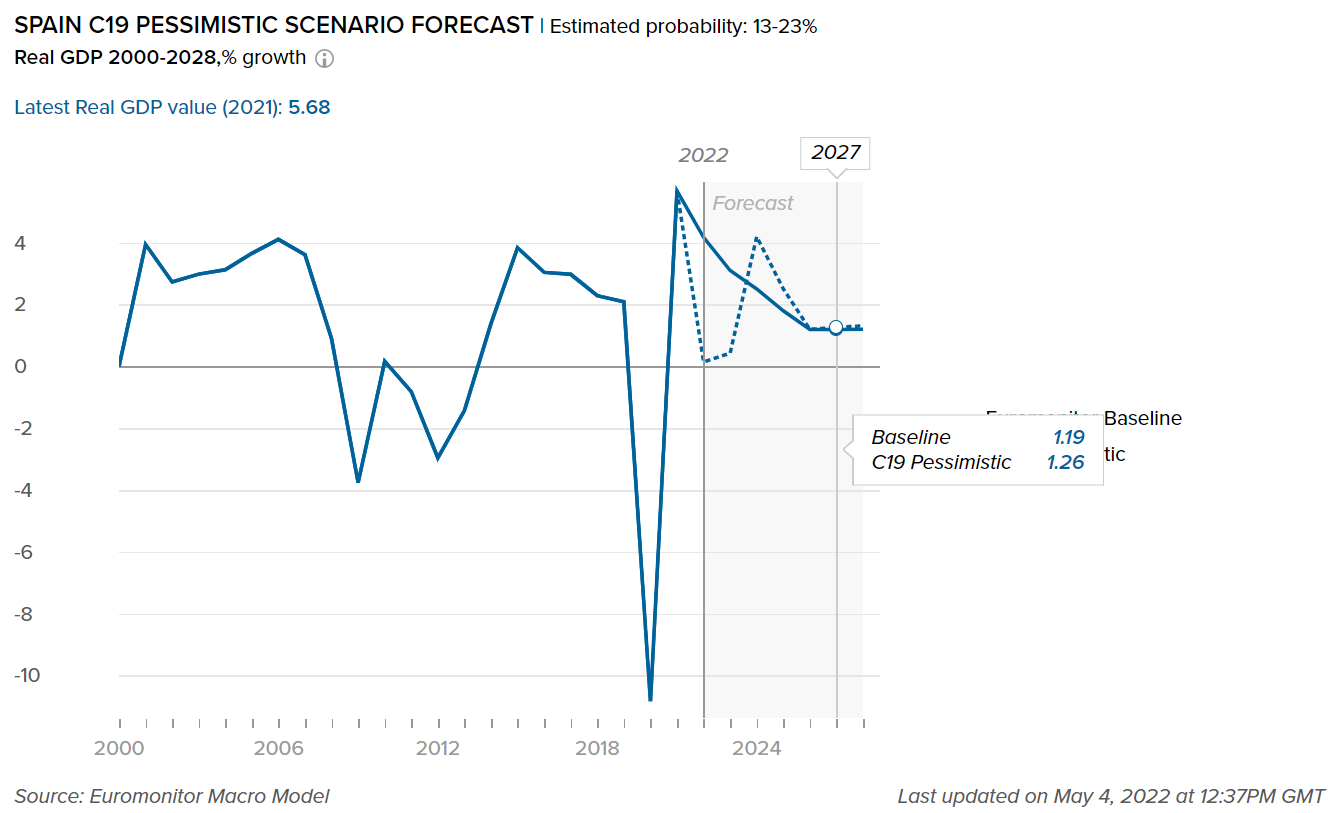

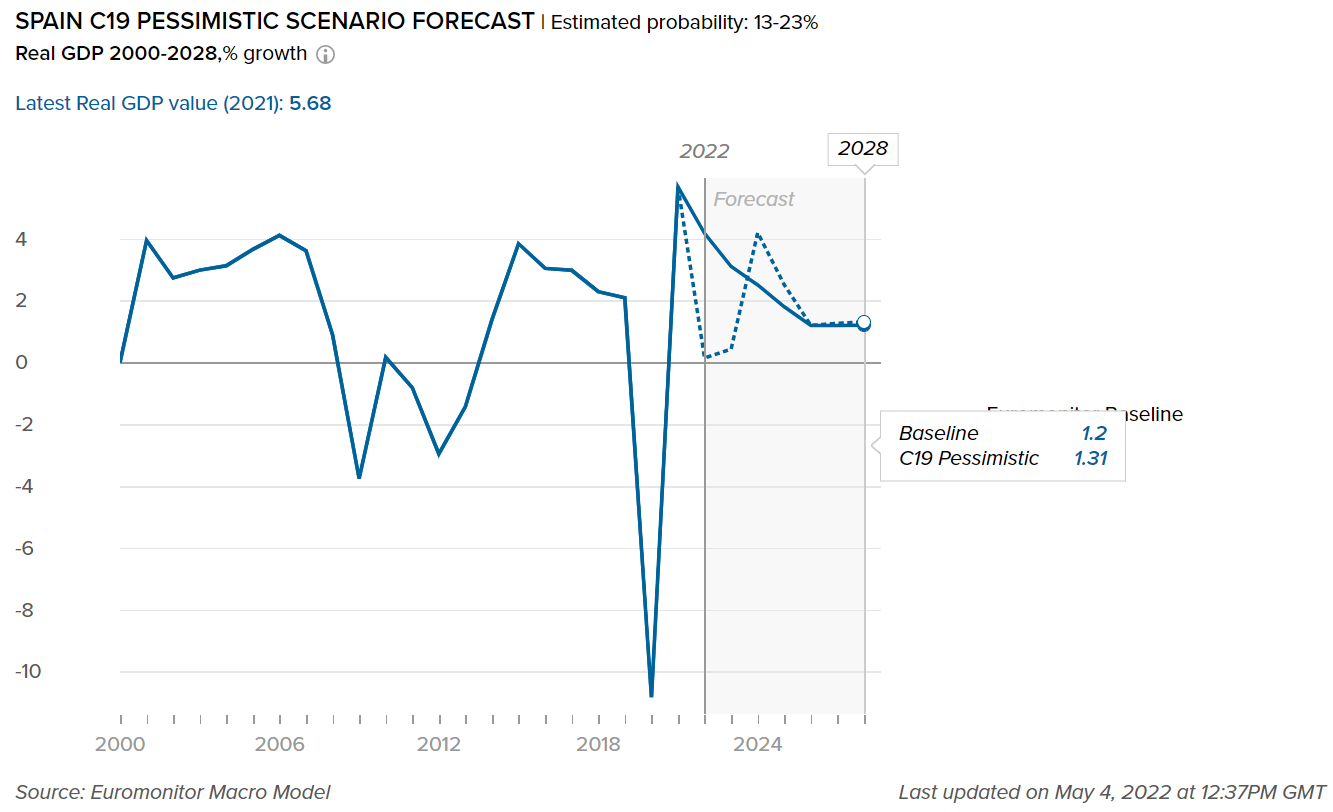

- Impact on GDP

-

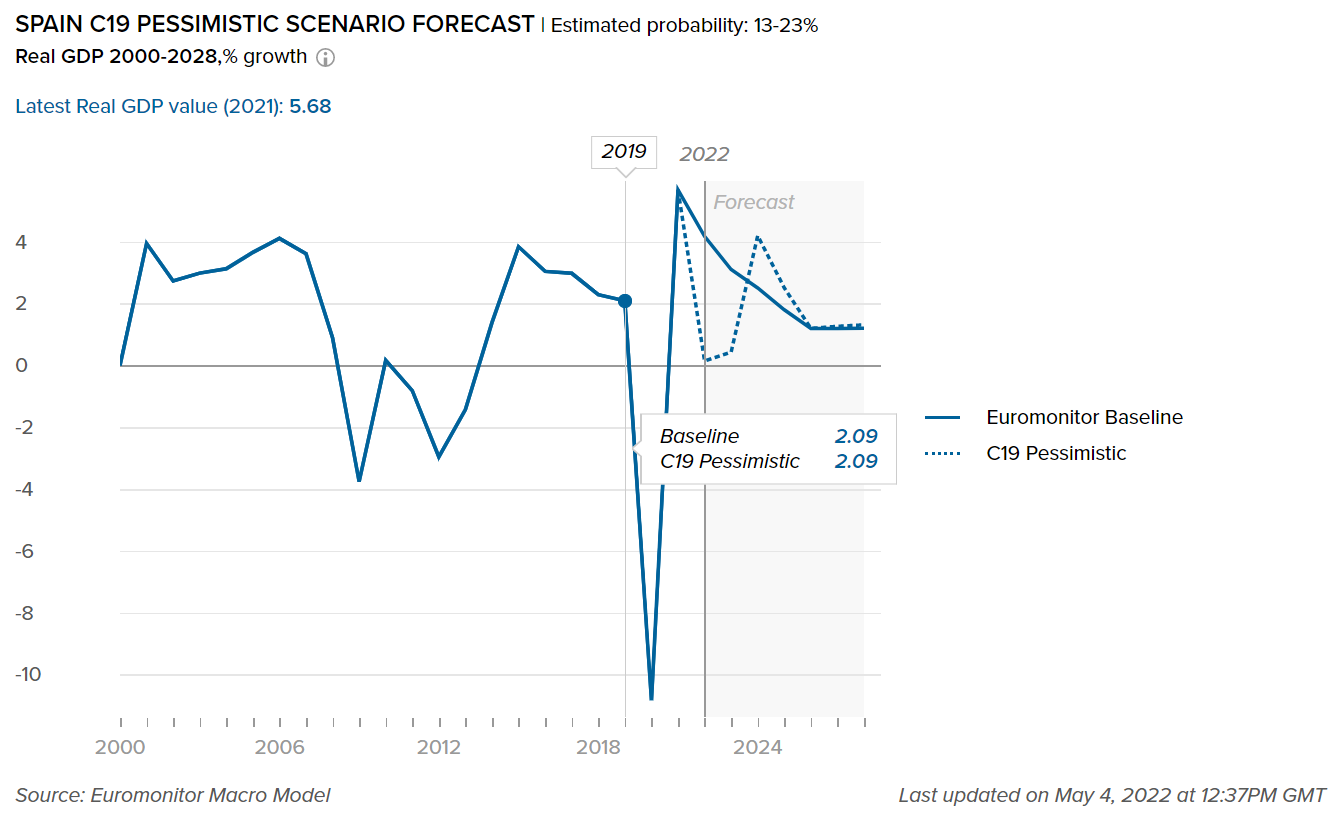

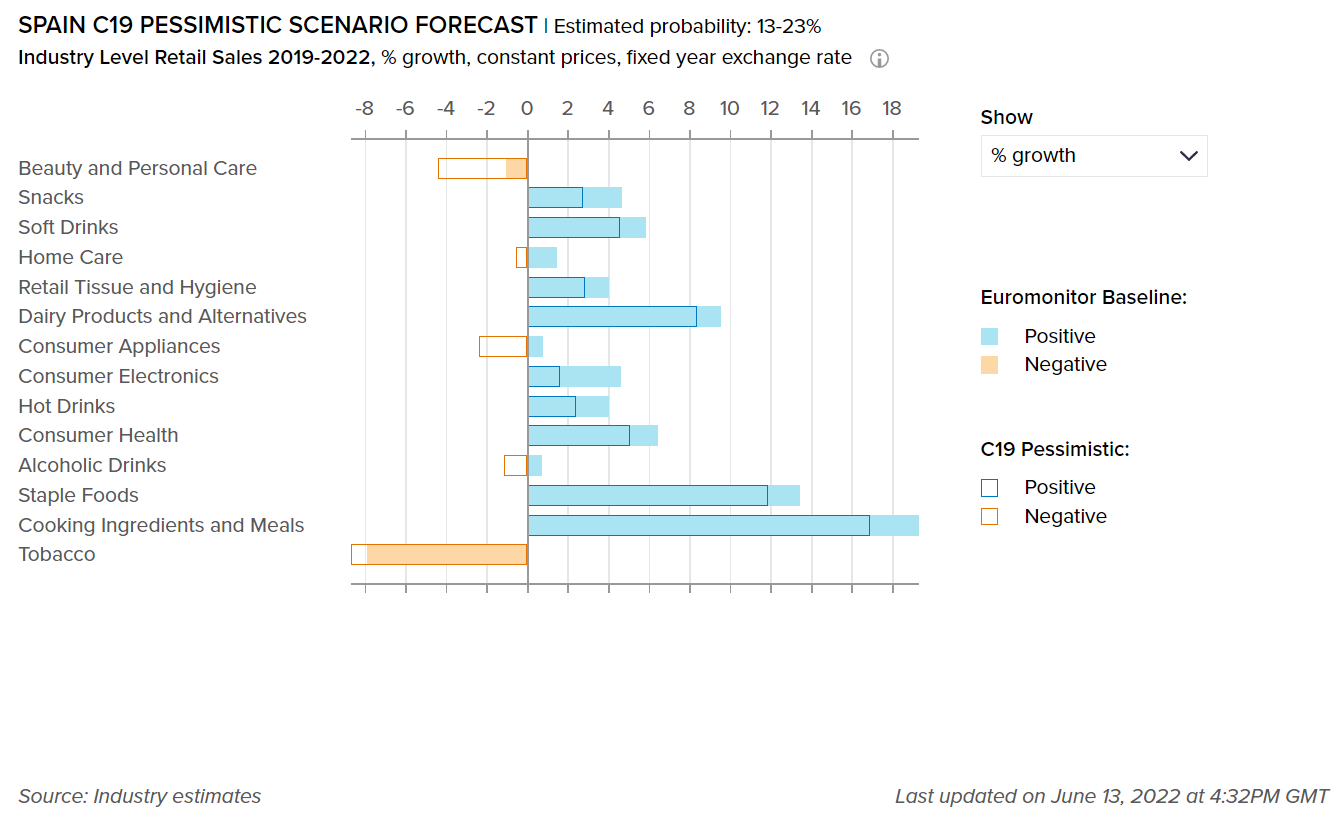

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in Spain. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Additional support packages to boost economic recovery

- Following a dramatic contraction of 10.8% in 2020 due to the coronavirus pandemic shock, Spain's real GDP increased by 5.6% in 2021, trailing Western Europe's average growth of 5.7%. As a result, Spain's GDP per capita in 2021 was USD29,788, compared to an average of USD40,083 in Western Europe.

- In 2021, the country’s economic performance was supported by improving domestic demand, due to elevated private spending, public consumption, and gross fixed capital formation (GFCF). Financial services, real estate, and business activities continued to be the leading contributors to the country's economy, accounting for 28% of total gross value added (GVA).

- In late 2020, Spain approved an indirect relief package for retailers and businesses in the tourism, food, and drink sectors which were significantly impacted by the COVID-19 restrictions. The package offered tax cuts, state-guaranteed loans, delayed social security contributions, and other forms of support, with the plan estimated at EUR4.2 billion. Furthermore, in February 2021, the Spanish government announced another direct financial support package worth EUR11 billion to help companies, small and medium-sized enterprises, and self-employed workers in the tourism and hospitality sectors that have been hit by the pandemic the hardest.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

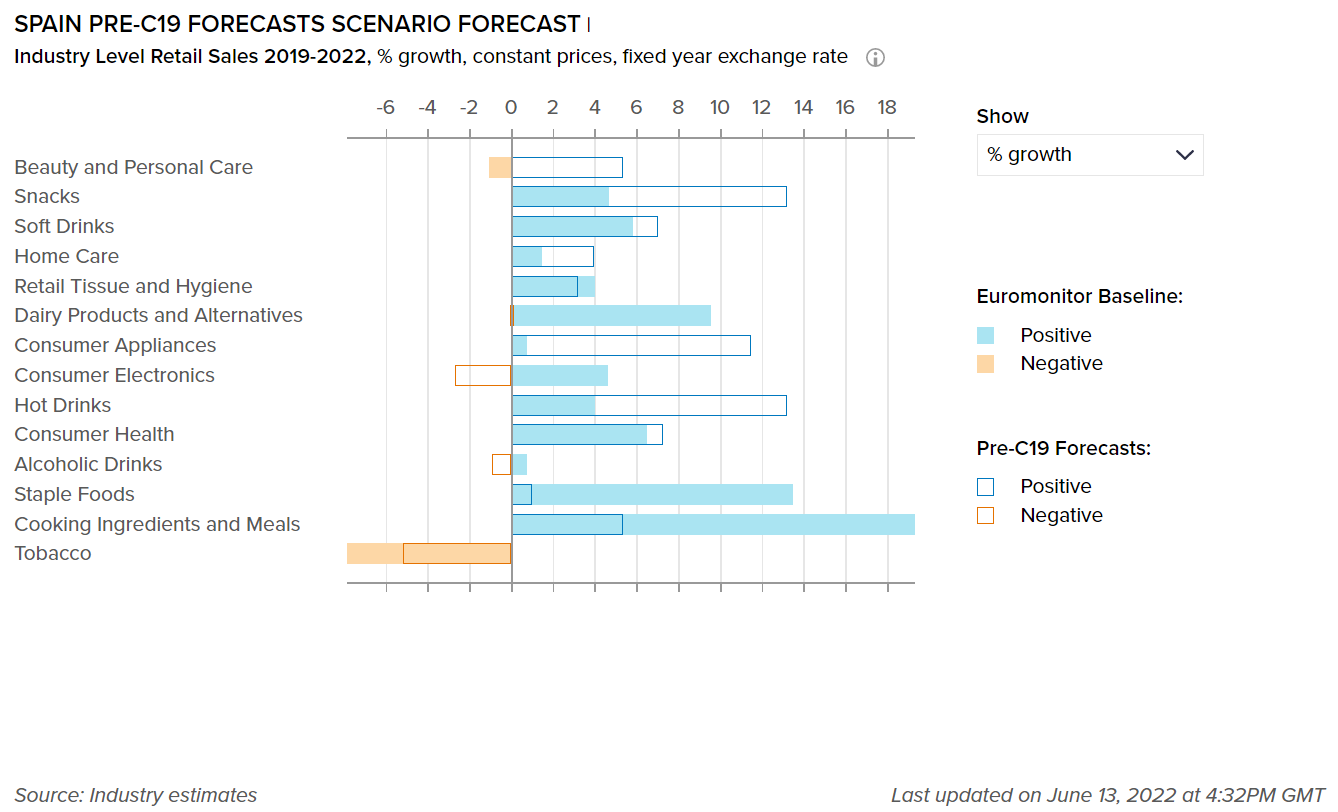

The graph below displays the adjusted forecasts of the percentage growth for the categories mentioned to highlight the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 65-75%.

Reduced household budgets put demand pressure on alcoholic drinks

- Alcoholic drinks were strongly affected by the COVID-19 pandemic, with the absence of tourists visiting due to travel restrictions and strict national lockdown measures, including the closure of horeca outlets, leading to a considerable overall decline in sales of alcoholic drinks. Furthermore, with prices dropping in all categories, alcoholic drinks also registered an even heavier decline in value sales, with a 1.6% decrease over 2019-2022, based on Euromonitor’s Baseline scenario forecast. Alcoholic drinks were also impacted by the reduced household budgets, leading to sharp reductions in consumer spending powers and ultimately prioritizing spending on essential products.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors mentioned in Spain. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Beauty and personal care still suffer the impact of pandemic-related falling demand

- After a dramatic decline in 2020, the major theme in Spanish beauty and personal care in 2021 was one of slow recovery. Sun care and fragrances did particularly poorly in 2020, as local consumers spent significantly more time at home (many of whom worked or studied from home) and socialized far less. Furthermore, during 2021, with hair and beauty salons largely operating normally again, retail value sales of both hair and depilatories declined. Moreover, the fact that face masks were still required for much of the year in 2021 (for indoor public venues such as retail outlets) meant that demand for color cosmetics was particularly weak. According to Euromonitor International’s Baseline scenario forecast, beauty and personal care recorded a decline of 1.0% over 2019-2022.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

2,158

2,142

0.6

Home Care Packaging

1,754

1,775

-1.8

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

24,170

24,362

-0.25

Flexible Packaging

18,384

18,768

0.01

Metal

9,977

10,092

0.05

Paper-based Containers

4,812

4,905

0.30

Glass

6,875

6,992

0.26

Liquid Cartons

5,025

4,919

0.00

Sustainability trends should continue moving further into the mainstream

- As ecologically-friendly packaging becomes more mainstream, brand owners in the home care industry are likely to continue to invest in sustainable packaging, attempting to limit the use of single-use plastic containers in favor of reusable and recyclable alternatives. Various brand owners are now opening refill centers so that customers can return old containers of personal care goods and avoid creating new packaging waste.

- Procter & Gamble, for example, announced intentions to reduce plastic content in Ariel and Lenor packaging, with the company aiming to use only 100% recyclable plastic by 2022, while Reckitt Benckiser debuted its Finish 0% product range in dishwashing, which includes an ecolabel and recyclable packaging.

- Further, Flopp started using compostable packaging and bio capsules in laundry care, and Stanhome introduced a new line of environmentally-friendly kitchen cleaning products with new lighter packaging, containing less plastic to reduce the environmental impact. The company also offers recycled, recyclable, and reusable aerosols and PET bottles, with 100% responsible and sustainable packaging.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recover Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is officially the best measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.