Overview

- Packaging Overview

-

2020 Total Packaging Market Size (million units):

98,351

2015-20 Total Packaging Historic CAGR:

0.2%

2021-25 Total Packaging Forecast CAGR:

-2.0%

Packaging Industry

2020 Market Size (million units)

Beverages Packaging

24,127

Food Packaging

65,978

Beauty and Personal Care Packaging

3,190

Dog and Cat Food Packaging

2,847

Home Care Packaging

2,209

Packaging Type

2020 Market Size (million units)

Rigid Plastic

37,884

Flexible Packaging

29,143

Metal

8,124

Paper-based Containers

10,724

Glass

9,279

Liquid Cartons

2,850

- Key Trends

-

The impact of COVID-19 on alcoholic drinks packaging in France was most visible in terms of reduced demand for smaller and on-the-go formats across the board and a shift towards larger packs. The trend was in line with increased at-home consumption and shared family value packs. There was also a spike in sales of multipacks of beer, a highly seasonal drink in France, with the format gaining appeal through its lower unit prices than single servings. As a result, flexible packaging, paper-based containers, and PET bottles benefited from this trend.

The rise in beauty and personal packaging is caused by an initial spike in stockpiling and panic-buying of some products, and continued consumer focus on hygiene-related products to protect against contagion. Growth was largely driven by bath and shower packaging. PET bottles in liquid soap, plastic pouches in body wash/shower gel, flexible paper and flexible plastic in bar soap and collapsible metal tubes in hand care have all shown substantial growth in 2020.

- Packaging Legislation

-

In food and beverages packaging, the inner side of plastic and metal packs is coated with BPA (Bisphenol A) to protect from corrosion caused by acidic food and beverages. In 2015, France banned BPA in metal cans and tins whereas the EU followed suit in 2019. The EU regulation confirms the toxicity of BPA and bans its use on the inside covering of metal tins and metal beverage cans, with a transition period factored in. It also extends the ban of BPA in baby bottles to all plastic cups and packaging for babies.

- Recycling and the Environment

-

The rise of refillable packs and reusable packs is driven by start-ups and premium brands. Premium brands are shifting towards refillable packs especially in fragrance packaging. Refillable stations for shampoo, liquid soap, and personal care products at the point of sale are becoming common in France. Natural brand Panier des Sens has introduced such a system in three of its stores, dispensing its flagship Liquid Marseille Soap. In home care, liquid detergents, liquid surface cleaners, and toilet cleaners are available for a refill at the point of sale. In dog and cat food, the movement of refillable packs has yet to pick up, but a few start-ups and private label brands have started the movement by offering dry dog and cat food in retail stores.

- Packaging Design and Labelling

-

Consumer concerns over the safety of ingredients contributed to the demand for greater transparency and clean labels. A smartphone brand called Yuka enables customers to scan products’ labels and get product details such as the origin of a product, listed ingredients, cruelty-free and vegan-friendly nature, and certified sustainable materials in packaging.

Rising demand for ‘free-from” products continued, as consumers sought to avoid ingredients that are perceived as being potentially damaging to both health and the environment. Due to the often-misleading nature of free-from claims, EU regulations were updated in July 2019 to prohibit certain claims from appearing on beauty and personal care labels and packaging. For example, labels may also no longer carry “free from allergens” or “hypoallergenic” claims since there is no guarantee that ingredients will never cause an allergic reaction in some consumers.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Despite the economic slowdown caused by the pandemic, growth was seen in fruit/herbal tea packaging. The growth can be attributed to the perception of fruit/herbal tea as a healthier alternative to other drinks. In fruit/herbal tea packaging, 50g plastic pouches continued to account for the highest proportion of retail volume sales. As a result, flexible packaging grew by 3.8% by volume in the hot drinks segment in 2020.

- PET bottles and flexible packaging are gaining ground at the cost of glass bottles and brick liquid cartons. PET bottles and flexible packaging offer convenience in terms of portability and storability. The shift from glass bottles and brick liquid cartons to PET and flexible packaging is evident in juices. In 2019, the juice brand Innocent, which used to be only available in brick liquid cartons, was well-received in PET bottles and flexible packaging.

- Trends

-

- PET bottles are growing at a rapid pace in soft drinks packaging. Producers are investing to boost the manufacturing capacity of rPET, which is a more sustainable solution than PET. By the end of 2020, Danone launched a 100% rPET bottle for Evian and Volvic, whereas Nestlé Waters launched Valvert 1.5-liter rPET bottles in 2019. In 2020 Coca-Cola launched the Honest Tea. Glacéau Smartwater and Chaudfontaine bottled water brands in 100% rPET.

- The “drink less but drink better” trend is supporting the growth of small pack sizes. In spirits, 700ml glass bottles will continue to be a lead pack size. The popularity of small pack sizes can be seen in 200ml flasks, which are used for culinary aids, and in 350ml glass bottles, mainly used for adding ingredients to cocktails. In wine, 200ml PET bottle formats, made for individual consumption, are growing at a rapid pace. Brands are tackling the decline of cider in France by offering smaller 330ml long-neck bottles. Some local brands such as Sassy, Appie, Lefevre, or La Mordue as well as a few Irish brands have successfully launched these smaller pack sizes.

- Outlook

-

- The growth of plastic pouches in soft drinks packaging is anticipated to be 32.0% CAGR over 2021-25. 500g plastic pouches are expected to gain popularity over this period. PET bottles are expected to gain ground from glass bottles and brands are expected to invest in creating a new capacity for the supply of more sustainable rPET packaging. As a result, PET bottles are expected to grow at 1.7% CAGR over 2021-25.

- Alcoholic drink packaging is likely to witness a growing contrast between modern packaging formats and traditional/vintage packages. Companies within vodka and beer will look to attract consumers via modern and catchy packaging. On the other hand, wine producers are expected to focus on traditional packaging. This will open more opportunities for the packaging industry in terms of value growth.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Stand-up pouches performed well in 2020 owing to their stackable nature and low cost. Pet food companies are facing competition for shelf space at retail stores in France. Their stackable nature makes stand-up pouchessave up to three times more space compared to other packaging materials. Moreover, they are easier and cheaper to transport and store. As a result, stand-up pouches grew by 3.0% by volume in 2020.

- The pet humanization trend, where pets are treated as humans, is supporting the premiumization of dog and cat food. Pet owners are paying more attention to ingredients and nutrients in the food. The look and feel of packaging are becoming more premium as manufacturers adopt pack formats that can improve the visibility of their products on retail shelves and help them stand out. This can be seen in the rise of stand-up pouches, but also in the increasing usage of zip/press closures, which are perceived as more convenient in terms of resealable nature, and ease of transport and storage.

- Trends

-

- In wet dog food, smaller pack sizes in pet food are gaining popularity in France. The pet humanization trend increased the awareness of the benefits of grain-free/gluten-free and organic pet foods. This is leading to premiumization as these newer niche pet products are significantly more expensive for both manufacturers as well consumers. As a result, smaller attractive pack sizes are gaining popularity. On the other hand, in dry dog and cat food, which is considered as a staple food for cats and dogs, very large pack sizes, such as 15kg and 20kg, are growing in popularity as consumers are increasingly ordering their pet food online.

- As the number of pet stores and superstores continues to grow, specialist retailers have started introducing individual/single servings. These treats are made to look fresh and “home-made,” and so that they can be sold at premium prices. This is following the trend seen in organic grocery stores, where staples and pulses are available in individual/single servings.

- Outlook

-

- Innovations and new start-ups are expected to rise in dog and cat food with a focus on the need for sustainability. For example, the New Loop online store, one of the prominent dog and cat food brands in the country, delivers food in durable reusable packaging that can be returned to be filled up again, with repeated subsequent reuse. Many brands are expected to follow suit over 2021-25. Such initiatives are expected to create more awareness and are aimed at achieving a circular economy.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- Glass, being heavy and fragile, is losing ground to flexible packaging and rigid plastic packaging. Retailers and e-commerce players are avoiding glass packaging as they are cumbersome to transport and store. Flexible packaging, which is a dominating pack type in bath and shower, benefited as retailers and e-commerce players favored more convenient flexible packaging. As a result, flexible packaging grew by a robust 12.9% by volume in 2020.

- Bath and shower packaging will continue to see healthy growth rates in the next couple of years, as they are directly related to health and hygiene. In bath and shower packaging, 250ml and 500ml plastic pouches in body wash/shower gel dominated the segment. As a result, liquid soap in plastic pouches recorded 17.3% growth by volume in 2020 whereas flexible packaging recorded 52.9% by volume in 2020.

- Trends

-

- Premium brands in fragrances launched refillable packaging which is rare in the fragrance industry. Fragrance refills, which are not common, are gaining widespread popularity as brands, such as Guerlain, are introducing a refill station in its Champs Elyseés store. The station provides consumers with customizable, personalized perfume bottles. The success of Guerlain’s initiative prompted a rise in fragrance refill stations in France.

- L’Oréal’s La Roche-Posay brand launched a paper-based cosmetic tube for its new moisturizing Anthelios sunscreen body lotion in 2020. Overall, 45.0% of plastic is reduced using these cosmetic tubes. Nivea launched Naturally Good Body Lotion in a bottle that uses 50.0% less plastic. Companies are shifting towards packaging solutions that involve refilling and recycling as production aims to become more sustainable.

- Outlook

-

- Sustainability will continue to be a primary influencer in terms of packaging development. Sustainable packaging is expected to be perceived as premium and consumers, especially young consumers, are willing to pay a premium for products with such packaging. It will play an important role in categories with products of daily needs, such as bath and shower, deodorants, and baby and child-specific products Small players and new start-ups are expected to achieve growth by focusing on sustainable packaging. These companies can reasonably grab the attention of millennials and environmentally aware consumers.

- Returnable and refillable packaging will also gain popularity for economic reasons. With refill stations expanding across France, more recycling and washing centers are likely to open. New product launches, marketing initiatives, and advertising are expected to revolve around sustainability themes such as returnable and refillable packaging.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- The economic impact of the pandemic decreased the purchasing power of consumers. In home care categories such as laundry detergents, companies focused mainly on medium-to-large pack sizes as they provide better value for money in terms of cost-saving benefits for consumers. This trend benefited flexible packaging as most large packs come in flexible packaging. As a result, flexible packaging grew by 3.8% by volume in 2020.

- Trends

-

- Bulk unpackaged sales have attracted consumer attention owing to their economical price and no-waste model. Many retailers are at a trial stage with bulk sales. The Naked Shop was the first French shop specializing in bulk liquid personal care and home care products. The store features automated dispensers, with consumers using reusable packaging with deposits and seeing the price in real-time as they fill these containers.

- Consumers have become more hygiene conscious because of the presence of the virus and look to keep their household environments clean. Many people are spending more time than usual in their homes due to lockdowns and closures of foodservice establishments. Thus, at-home consumption of meals significantly increased and has contributed to the rise in cleaning and washing utensils at home. As a result, home care categories like surface care and dishwashing saw an 11.6% and 11.4% by volume growth in sales respectively in 2020, as a direct result of the COVID-19 pandemic.

- Outlook

-

- The French government introduced a law that imposes standards on industry players to minimize waste levels and enforce the reuse of materials. This law mandates lower consumption of non-renewable resources, the reuse of waste as a resource, products that have a longer useful life, the recycling of 100% of plastics, and producing less waste. More innovation is therefore expected in terms of the development and provision of sustainable packaging solutions. The law aims to achieve 100% plastic recycling by 2025 as well as an end to the usage of single-use plastic packaging by 2040. As a result, refill packs, concentrated formulas, thinner plastic pouches, and formats made from recyclable materials are expected to gain share in-home care packaging

- Smaller pack sizes are expected to witness strong new product development due to the launch of a widening range of products. Smaller pack sizes such as single-serve packs are expected to continue to proliferate on the grounds of the convenience of on-the-go consumption over 2021-25.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- During the lockdown, demand for confectionery declined considerably as consumers stayed at home more and were less likely to make impulse purchases. Rising health and wellness trends also contributed to its decline. The inability to purchase products impulsively on online e-commerce platforms is hampering the category’s growth, and movement restrictions also hindered impulse buying of confectionery in retail stores and hypermarkets. As a result, flexible packaging, which is widely used in confectionery packaging, declined by 3.7% by volume in 2020.

- For much of 2020, consumer foodservice outlets in France were closed, as consumers switched to working and studying remotely. Moreover, stress and boredom caused by home seclusion made consumers choose comfort foods, such as frozen pizza, to treat themselves. Frozen pizza is quick and easy to prepare while working or studying from home. As such, demand for the product increased considerably in 2020. Flexible packaging, which is frozen pizza’s main pack type, grew by 1.3% during the year.

- Trends

-

- France is gradually shifting towards smaller households that prefer to shop frequently but purchase fewer items, especially consumers in urban areas. This trend continues to boost innovation in smaller pack sizes. It is also seen in multipacks of smaller yogurts and dairy desserts. Multipacks of two and four units and even single-serve portions witnessed strong growth in 2020. Manufacturers adopted stand-up pouches, as seen in many packaged food categories. Pouches have the advantage of being convenient for consumers and highly protective against air and sunlight. En Direct des Eleveurs launched a plastic stand-up pouch that is microwaveable and resealable. In addition, it has a QR code that consumers can scan to track the product origin which supports the growing demand for sustainable local products.

- Chocolates with toys recorded a much slower rate of volume growth compared to previous years. The category suffered from the drop in impulse purchases, whereas consumers were more likely to purchase larger packs of confectionery products to dole out to children in the home. This benefited products more suited to sharing, such as chocolate pouches and bags in 175g pack sizes. This format was also boosted by bulk buying as flexible plastic (the most popular pack type for 175g chocolate pouches and bags) helps in keeping the products fresh for longer periods.

- Outlook

-

- Over 021-25, processed fruit and vegetables are expected to see the negative effects of health and wellness trends as consumers increasingly avoid processed food products in favor of fresh and single-ingredient products. During the COVID-19 pandemic, interest in horticulture and gardening also increased in France, stimulating the home growing trend. As more consumers turn to grow their own fruit and vegetables, demand for processed fruit and vegetables will continue to fall. As a result, glass and metal packaging, which are the main packaging types used for shelf-stable processed food and vegetables, are expected to take a hit over 021-25.

- Over 021-25, consumer interest is expected to decline within dried baby food due to the rising perception that it contains too many preservatives. However, metal tins are expected to gain share from folding cartons in the coming years, as they are considered easy to store and benefit from a more premium image. The poor performance of dried baby food will harm folding cartons in baby food packaging, as folding cartons is an important pack type in this product area.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in France

-

France decides to lift the requirements for wearing masks on public transport

- According to the World Health Organization (WHO), France had 28,540,945 COVID-19 cases, with 144,781 deaths, and 438,257 cases per million inhabitants as of May 2022.

- The French government declared that due to the changing epidemiological situation, wearing a mask will no longer be required on subways, buses, or trains starting May 16. However, according to the government, wearing a mask will remain necessary for caregivers, patients, and visitors to health and care facilities, including hospitals, pharmacies, and medical biology laboratories.

- According to the WHO, the total number of vaccines as of May 15, 2022, stood at 147,595,541, which translates to 3 fully vaccinated persons per 100 people.

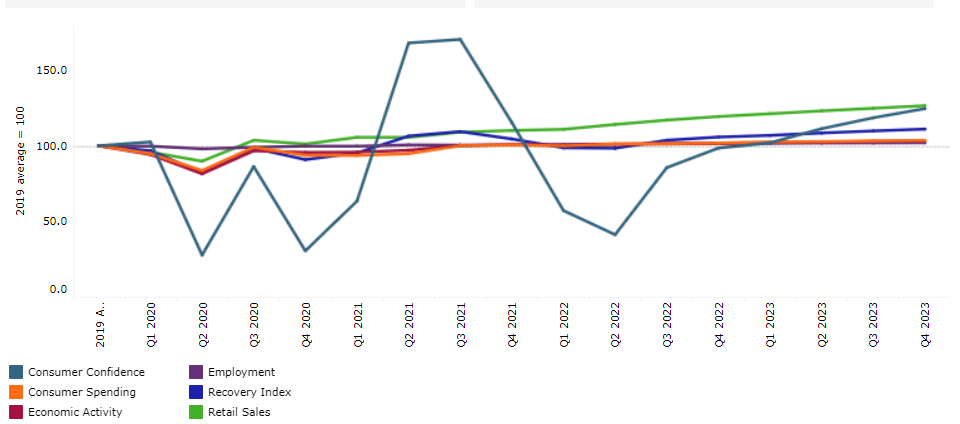

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, France

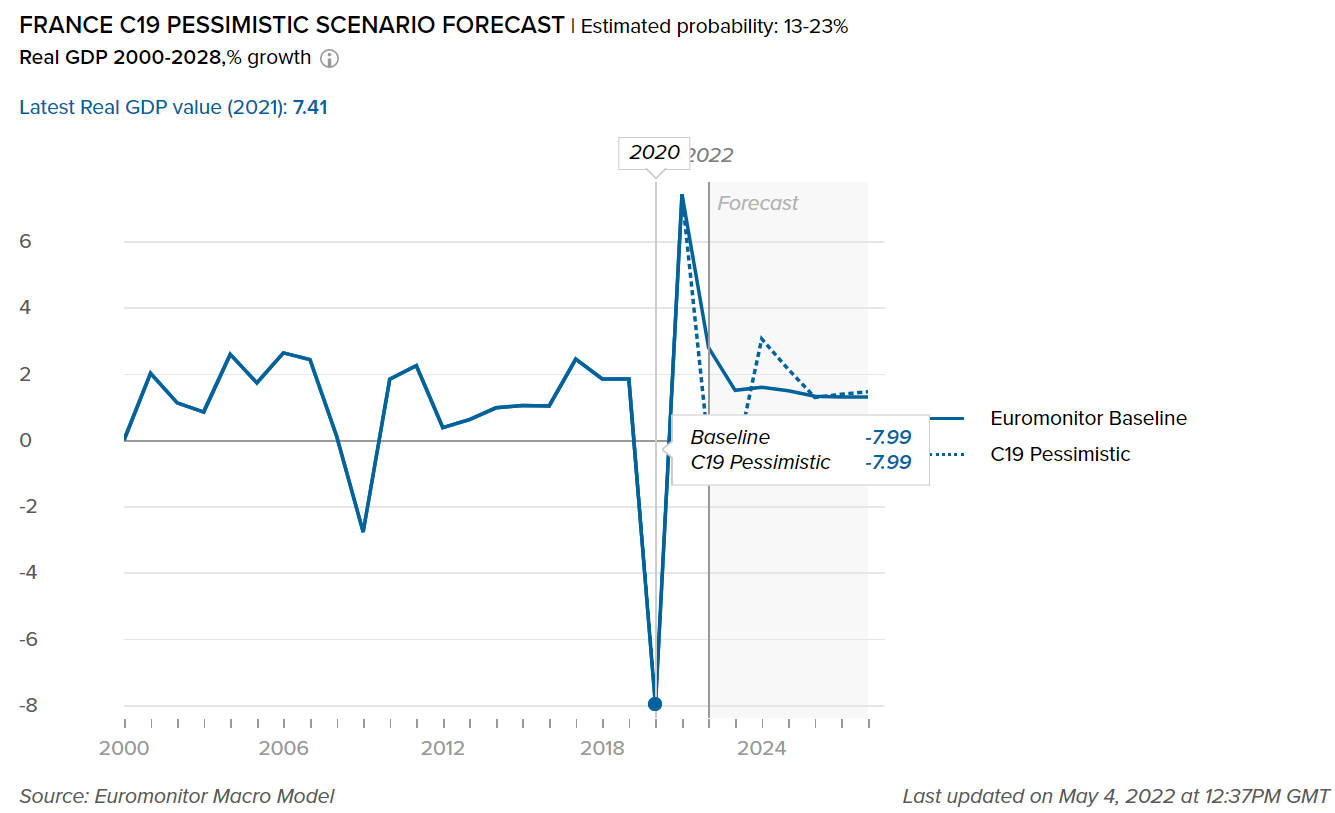

- Impact on GDP

-

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in France. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Improving private consumption is set to facilitate further recovery in France

- France's real GDP increased by 7.4% in 2021, outpacing Western Europe's average growth of 5.7%. Household consumer spending, buoyed by a successful vaccine rollout and reducing restrictions, as well as a solid increase in investment, drove the recovery. The government's EUR100 billion "France Relance" long-term recovery plan, announced in September 2020 and mostly funded by the EU, aided in cushioning the economic shock and facilitating recovery.

- In 2021, France's GDP per capita was USD44,884, which was higher than the regional average. Despite the risks of new infection waves and global supply chain disruptions, the recovery in private consumption is likely to continue in 2022, with favorable financing conditions and funds from the "France Relance" program supporting public and private investment. In October 2021, the government also unveiled a new EUR30 billion 5-year investment plan dubbed "France 2030." The strategy intends to boost French industrial activity in the automotive, aerospace, digital technology, biotechnology, and healthcare sectors by facilitating a green transition.

- Inflation in France surged to 2.0% in 2021, up from 0.5% the previous year due to rising energy and raw material prices, as well as supply bottlenecks. In 2021, the most significant price increases were seen in alcoholic drinks and tobacco products, food and non-alcoholic beverages, and hospitality services.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

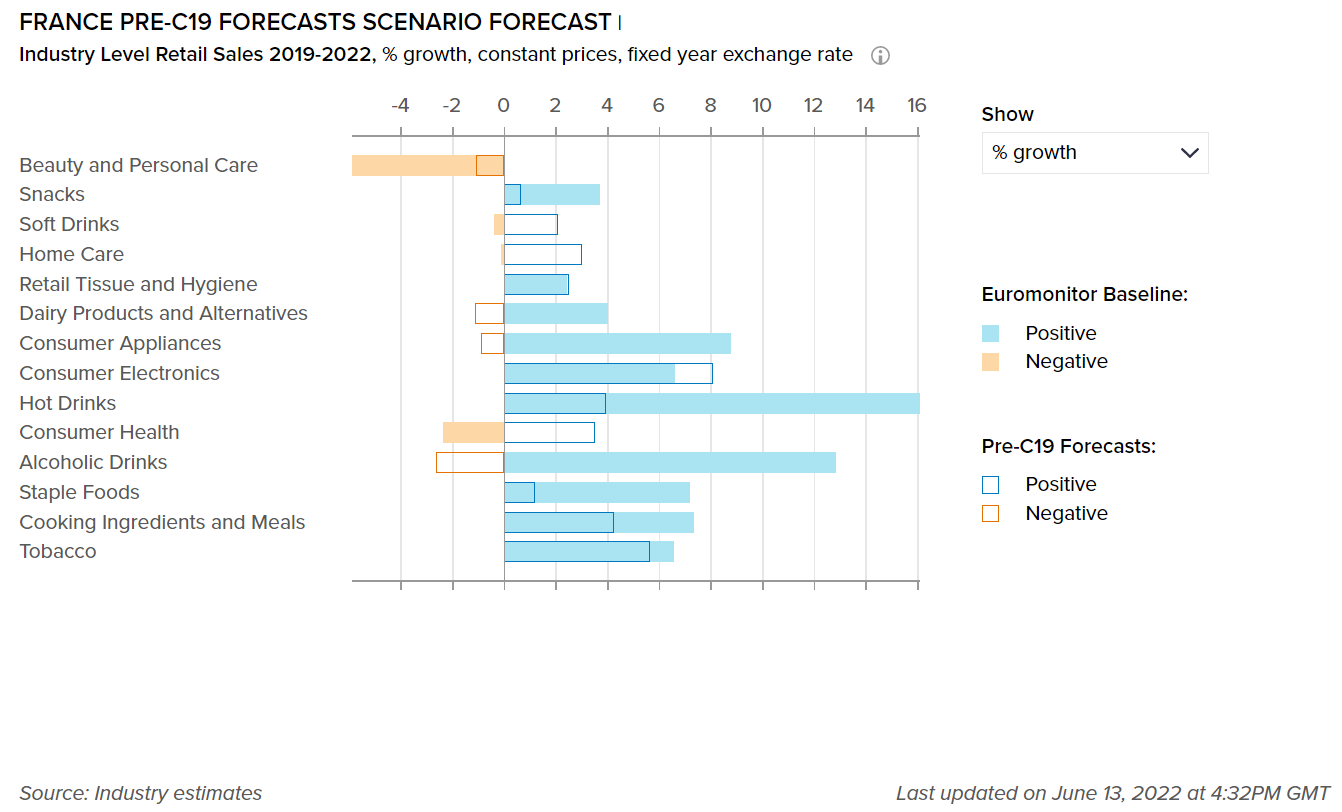

The graph below shows the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

Soft drinks and beauty and personal care continue to suffer from the pandemic’s impact on demand

- Having plunged dramatically in 2020, retail value sales of beauty and personal care products continued to fall in 2021, albeit at a considerably slower pace, with a 5.8% decline over 2019-2022, according to Euromonitor’s Baseline scenario forecast. COVID-19 dominated the first quarter of 2021 once more, with curfews imposed from 6 pm from January 1 to March 30, forcing non-essential retail enterprises to close. Even after these restrictions were removed, demand remained low; the fact that many people continued to wear face masks, as well as the extensive work-from-home measures, contributed significantly to this.

- Soft drinks suffer from a poor image associated with excessive sugar content. According to Euromonitor International's Voice of the Consumer: Health and Nutrition 2021 Survey, there are a variety of health reasons behind the sugar reduction trend, which had a negative influence on soft drinks consumption. 50% of customers say they are reducing sugar consumption for weight loss or management, 45% believe it is healthier for them to avoid certain ingredients, and 38% say they have read or heard it is harmful to consume. As a result, the health and wellness trend had a negative influence on the demand for various soft drinks categories, resulting in an overall decrease of 0.3% over 2019-2022.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors covered in France. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Retail sales continue to benefit as consumers are still focused on home consumption

- The unavailability of cafés, specialty coffee and tea shops, and other on-trade outlets as a result of the COVID-19 pandemic in 2020 and part of 2021, boosted off-trade demand for coffee, with retail growth rates in the category for 2020 and 2021 being the most dynamic. In this context, it is worth noting that many consumers preferred to focus on premium coffee options to recreate the café coffee experience in the comfort of their own homes. This is in line with consumers’ need to indulge themselves in response to the harsh and challenging situations that emerged from the COVID-19 pandemic.

- Retail sales of some alcoholic drinks benefited from the negative impact of on-trade sales, with consumers forced to drink at home rather than in cafés/bars, nightclubs, or full-service restaurants. Craft beer, ales, Anglo-Saxon beer, and non/low alcohol beer, in particular, showed substantial off-trade increases due to growing interest and demand. Bitter spirits (such as Aperol and English gin) and sweet spirits (such as flavored and/or “finished” black rum) were also popular in 2020/2021, benefiting from the popularity of alcoholic cocktails and a brief trend of sipping drinks while talking with friends via video conference applications such as Zoom.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

3,104

3,108

-4.7%

Home Care Packaging

2,232

2,243

-2.5%

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

38,811

38,594

-0.49%

Flexible Packaging

29,751

29,698

-0.12%

Metal

8,461

8,619

0.03%

Paper-based Containers

10,968

11,003

-0.08%

Glass

9,770

9,893

0.16%

Liquid Cartons

2,813

2,780

0.00%

Innovation and improvements in home care appliances and products could influence packaging developments

- As a direct result of the emergence of COVID-19 in France, sales of a variety of home care categories, such as surface care and dishwashing, increased in 2020/2021. As a result of the virus, consumers became more hygiene conscious and sought to keep their homes clean, especially given that many people were spending more time than usual in their homes, and at-home meal consumption increased significantly as a result of lockdowns and foodservice establishment closures, implying more cooking and cleaning in a domestic setting.

- Another important category that experienced high growth during the pandemic was home care disinfectants, which saw a major sales rise in 2020, followed by further dynamic growth in 2021, due to increased health and hygiene awareness. As a result, during the pandemic, packaging unit volumes of HDPE bottles used in home care disinfectants increased significantly. In 2022, the performance of home care disinfectants and HDPE bottles is projected to remain high.

- Over the forecast period, French customers are likely to become more environmentally conscious, prompting manufacturers to develop new and inventive packaging. For example, new product introductions in laundry care and dishwashing could be sparked by improvements in home laundry appliances and dishwashers that cater to the increased demand for time savings, sustainability, and energy efficiency. This is expected to benefit the packaging unit volumes of key pack types such as plastic pouches in dishwashing and laundry care over the forecast period.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recovery Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.