Overview

- Packaging Overview

-

2020 Total Packaging Market Size (million units):

653,504

2015-20 Total Packaging Historic CAGR:

1.1%

2021-25 Total Packaging Forecast CAGR:

0.9%

Packaging Industry

2020 Market Size (million units)

Beverages Packaging

221,721

Food Packaging

400,253

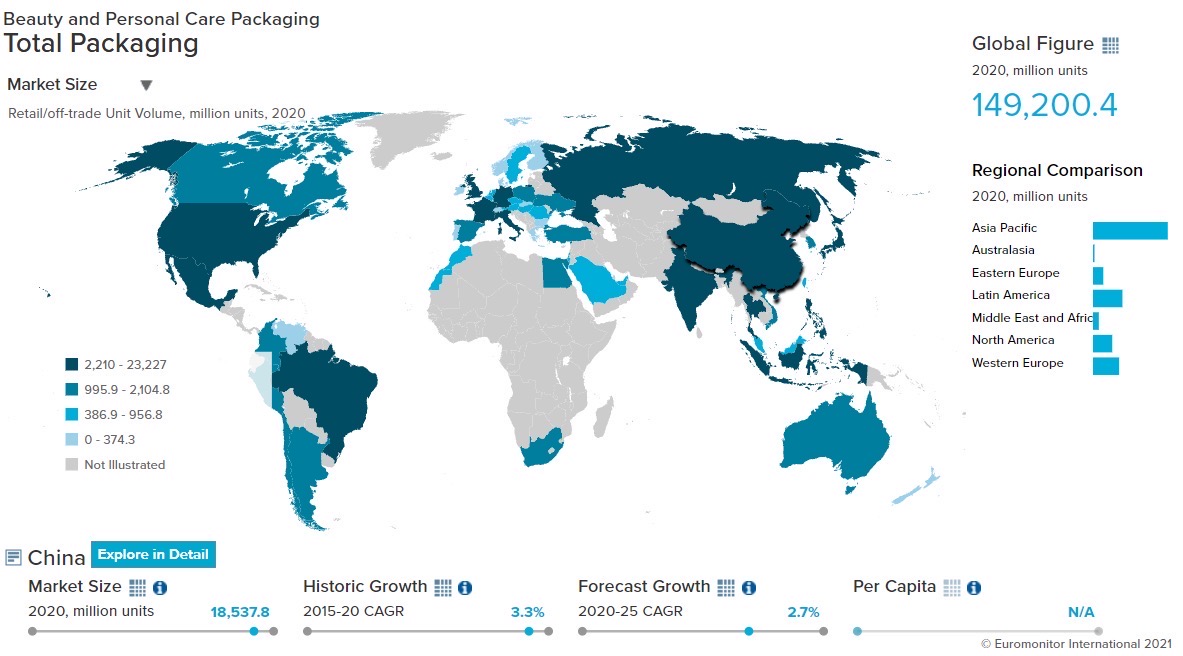

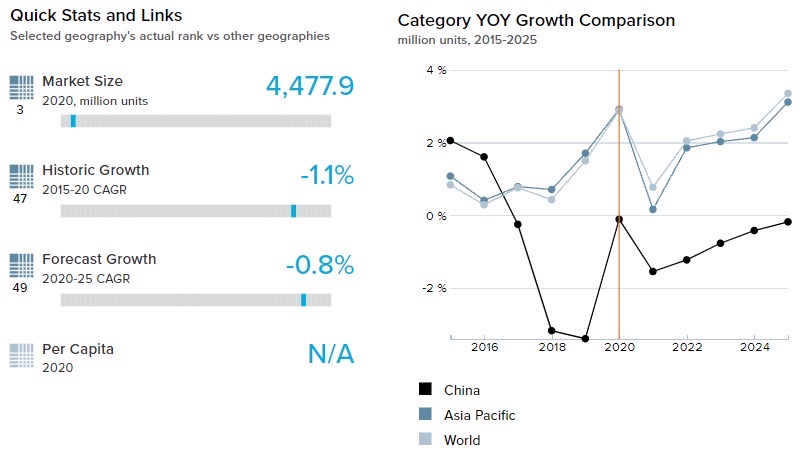

Beauty and Personal Care Packaging

18,377

Dog and Cat Food Packaging

2,710

Home Care Packaging

10,443

Packaging Type

2020 Market Size (million units)

Rigid Plastic

192,567

Flexible Packaging

234.100

Metal

45,848

Paper-based Containers

37,798

Glass

54,584

Liquid Cartons

86,809

- Key Trends

-

Demand for smaller pack sizes is rising as the average household size in China is decreasing. Products that have short expiration dates are mostly bought in smaller packages to avoid waste. Thus, manufacturers are introducing new and innovative smaller packaging formats. Hot drinks sold in metal are the fastest-growing type of packaging thanks to the increased demand for quality products. Airtight and waterproof, metal tins preserve freshness against oxygen and humidity. They also serve as a robust shell and save the content from being crushed during delivery. As hot drinks seem to be becoming more upmarket, manufacturers are employing more metal packaging, typically in specialty coffee and high-end tea.

Alcoholic drinks manufacturers increasingly promoted multipacks as the closure of foodservice/restaurants boosted at-home consumption of alcohol. Multipacks are suitable for at-home consumption as they can be stockpiled. As a result, packaging used in multipacks such as flexible packaging, PET bottles, and metal tin cans gained momentum. Glass bottles continued to gain ground within skincare, color cosmetics, and fragrances packaging. Consumers are showing an increased interest in glass as a material that offers more durable product protection than most other materials, due to its non-toxic nature. Moreover, the appearance of glass conveys an image of purity and elegance favored by premium brands and trusted by consumers.

- Packaging Legislation

-

“Green Packaging Evaluation Methods and Guidelines” a new proposed law, was recommended by the State Administration for Market Regulation to create a new standard for the packaging industry. The release of the new national standard will potentially accelerate the transformation of the packaging industry into a more environmentally friendly one. The regulation stipulates the requirements for low-carbon emissions, environmental protection by green packaging products. Green packaging refers to environmentally friendly packaging that consumes fewer resources such as energy and is less harmful to human health.

- Recycling and the Environment

-

In response to the need to protect the environment, manufacturers are introducing recyclable materials across various industries. For example, Coca-Cola introduced clear plastic bottles for their brand Sprite by replacing green bottles. It’s a tedious job to recycle when waste contains both green bottles and clear plastic. Thus, most recycling units avoid green bottles.

With China’s manufacturing boom, waste recycling and processing units are on the rise. Thus, there is a growing demand for plastic waste. Previously, waste recycling was mainly carried out by individual rubbish collectors and rarely by private companies. However, with the rise of more recycling and processing units, waste plastic is being collected and processed by new technologies which are helping the industry grow at a rapid pace.

- Packaging Design and Labelling

-

The National Health Commission and the State Administration for Market Regulation announced the release of regulation GB 2716-2018 National Food Safety Standard for edible oil, to replace the previous GB2716-2005. The new regulation makes it mandatory for companies to disclose the proportion of different types of ingredients and nutritional value as per the set standards. This regulation was urgently needed as a few manufacturers adopted cheap low-value oil as the main ingredient in their blended oils but claimed a high content of high-value oil. The new regulation aims at weeding out manufacturers who falsify the information, making room for big, branded manufacturers.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Hot drinks saw strong growth in 2020, thanks to the widespread perception among Chinese consumers that specific types of tea and plant-based hot drinks deliver immune system support and other health-boosting benefits. These benefits may lessen susceptibility to virus infection. Thus, Chinese consumers preferred to stockpile hot drinks by purchasing larger packs such as 500g, 600g, and 680g flexible plastic packs. As a result, flexible packaging witnessed 2.5% growth by volume in 2020.

- The pandemic accelerated the rapid rise of e-commerce and innovation in terms of packaging. Pack sizes, especially in the case of coffee, saw a rise in large sizes of over 1kg in instant coffee. For example, Nescafé’s value pack is among the best sellers in instant coffee on e-commerce platforms. The pack contains 100 sticks, compared to the usual 40-stick packs found on store-based retailers’ shelves. As a result, flexible packaging recorded 5.7% growth by volume in the coffee category in 2020.

- Trends

-

- Toward the end of 2021, Nespresso partnered with JD.com to provide nationwide doorstep recycling of Nespresso coffee pods. Free recycle bags are available to consumers who purchased from the company’s official sales network. By scanning the code on the bag, they can schedule a pickup via WeChat mini program. JD delivers the used pods to the nearest recycling plant where the coffee and aluminum are separated. The coffee is composted and the aluminum is melted down and recycled.

- The growing interest in metal beverage cans and metal bottles also posed a great threat to glass packaging in beverages in general. Metal packaging not only offers effective performance as glass in terms of insulating from air and sunlight, but it is also less fragile and is lighter in weight than glass packaging, making it easier to transport. Riding on these advantages, metal packaging continued to be gradually adopted by beer manufacturers at the end of 2020.

- Outlook

-

- Premiumization is expected to impact development despite increased price sensitivity among many Chinese consumers. The hot drinks market in China is highly saturated and brands have been focused on the creation of a distinct image, with several players targeting China’s higher-income earners through premium-like packaging in metal formats. While flexible packaging will see 1.4% CAGR growth over the 2021-2025 period, metal, the third-largest area, will see 4.2% CAGR growth over 2021-2025.

- Returnable packaging is likely to see continued investment as efforts to reduce plastic waste accelerate. Brands and companies seek to boost their images in terms of environmental and social responsibility. Recyclable metal tins and folding cartons can thus expect more growth. Metal is expected to grow in fresh ground coffee pods, standard fresh ground coffee, black tea, and specialty high-end teas.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Stand-up pouches continue to be a strong performer in unit volume sales growth recording a growth of 24.0% in dog and cat food packaging in 2020. This type of packaging enjoys premium positioning as they are convenient to use, keeps the product fresh, and is widely used in dry and wet food products and treats. This packaging type also enjoys cost advantages over metal food cans and aluminum trays for manufacturers of wet dog and cat food.

- Flexible plastic is popular in dog and cat food packaging because of convenience and it is lightweight, particularly in terms of large packs. It is also benefiting from the boom in internet retailing, with more owners purchasing pet food in large packs online for cost savings and convenience reasons. Price-sensitive consumers are less interested in the look and feel of the packaging, preferring to remain with their regular brand or product in the simplest presentation. This supports the ongoing acceptance of flexible plastic, as these consumers tend to make repeat purchases of large packs.

- Trends

-

- Growth in cat treats and mixers is supported by the use of small flexible plastic packs and plastic pouches that facilitate single-serve consumption and portability. Some of the products feature secondary packaging and a “window” to allow consumers to see the content before purchasing. Cat purée strips are likely to offer growth opportunities to product manufacturers and packagers.

- The use of easy dispensing closures is attractive to time-pressed consumers, while the addition of high-quality ingredients with health claims is seen as another important way of adding value. In 2020, Yantai China Pet Foods Co Ltd launched a new product – a wet cat food that is claimed to be able to replace dry cat food and fulfill a cat’s dietary needs. Targeting younger Chinese consumers, the product comes in convenient packaging and claims to have a higher meat content with human-grade ingredients.

- Brick liquid cartons are emerging as a new type of packaging in wet dog and cat food. The pioneer of this pack type in China is Shanghai Bridge, which has taken its inspiration from the brick liquid carton pack type used for milk. The products are easy to carry and transport because of their lightweight.

- Outlook

-

- Pack sizes smaller than 1.5kg are often used with freshness in mind or as a format ideal for offering consumers the opportunity to trial a new brand or product. Meanwhile, sizes of 10kg and over are more likely to be used by loyal customers to a particular brand or product who are looking to make cost savings by purchasing larger packs. It is possible that sales of larger packs, particularly available for home delivery via e-commerce, may see a short-term boost to sales because of the COVID-19 pandemic, with some consumers still keen to avoid frequent trips to physical stores.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- Due to lockdowns during the pandemic, consumers were unable to go out for extended periods, so the demand for make-up products such as lip gloss, lipstick, and nail polish as well as deodorant roll-ons, deodorant sprays, and similar categories went into decline. At the same time, demand for baby and child-specific products, bar soap, shower gel, and facial cleansing wipes grew as consumers stockpiled essential hygiene-related goods to restrict their unnecessary movement outdoors and safeguard against the virus.

- In bath and shower packaging, stand-up pouches of 400ml and 500ml sizes in liquid soap recorded 11.1% and 14.7% growth by volume in 2020. Again, in other bath and shower products, stand-up pouches performed well. As a result, stand-up pouches grew by 22.7% by volume in the beauty and personal care category in 2020.

- Trends

-

- Skincare packaging witnessed 8% growth by volume in 2020 as consumers prioritized purchases of hygiene-related products to protect themselves and their families from the risk of infection with COVID-19. Sales in baby and child-specific products grew 6.5% supported by stockpiling and panic-buying during the early lockdown period. Skincare saw continued growth due to salon closures boosting at-home treatments, and a rise in purchases of products that promote health and wellbeing. As a result of stockpiling and at-home consumption, larger packs that are mostly packed in flexible packaging benefited. Thus, flexible packaging grew at 7.5% and 4.7% by volume in baby and child-specific products and skincare packaging respectively.

- The lotion pump closure, already widely used, was boosted by the pandemic as it helps consumers to maintain hygiene as it can be used with minimal or no human touch. Lotion pump closures were becoming more visible throughout the beauty and personal care packaging, including in-hand care, toothpaste, and, in particular, liquid soap.

- Outlook

-

- The widespread trend towards smaller pack sizes is expected to gain pace. Producers can tempt consumers to try new products with lower-cost small-sized formats – a strategy growing fast in the premium segment, where high unit prices resulted in the decline of consumer demand. Beauty and personal care products offering sun protection and defense against pollution are popular in pocket sizes, as are fragrances. In color cosmetics, brands are increasingly launching mini variants of core products to encourage consumers to experiment with a broader range of colors and styles.

- Larger value-for-money pack sizes are expected to attract price-sensitive consumers. This will boost e-commerce as the channel is well-positioned to deliver large packs at doorsteps. This distribution channel encourages bulk purchases in beauty and personal care through the convenience of home delivery. Moreover, the emergence of third-party online delivery platforms such as Ele and Meituan, enable consumers to purchase beauty and personal care products in bulk from local grocery retailer outlets. Consumers can use an app to arrange delivery to their homes within 30 minutes. This trend is further expected to boost larger pack types.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- Due to lockdowns, home seclusion led to greater usage of household toilets. This increased the sales of toilet cleaners as consumers were conscious about health and hygiene and stockpiled these products to help contain the possible spread of the virus via their bathrooms. Flexible pack type dominates this category in packaging hence it recorded 10.7% growth by volume in toilet care in 2020.

- Within liquid detergents in laundry care, even though HDPE bottles are still the leading pack type, plastic pouches are on the rise due to the ease it provides in terms of transport, storage, and larger-sized refill packs. The proportion of plastic screw closures in plastic pouches, as well as HDPE bottles, is also growing as this design enables consumers to refill their detergent bottles more efficiently without spillage.

- Trends

-

- Movement restrictionsed to an increase in cooking which boosted sales of essential daily items such as kitchen cleaners and dishwashing products. These products were widely available across retail and e-commerce platforms at attractive unit prices. Hand dishwashing and kitchen cleaners are generally sold in HDPE and PET bottles. Medium-sized and large packs are preferred by consumers as kitchen cleaners have a long shelf life and offer better value for money in such sizes. Larger pack sizes also helped shoppers as they reduced the frequency of visits to physical stores.

- Bigger pack sizes were becoming more common in powder detergents, liquid detergents, home disinfectants, etc. before the pandemic. This is due to a lower price per liter/kg, promotional campaigns, the rising penetration of e-commerce, and improvements in last-mile logistics. For example, in the bi-annual online shopping festivals run by JD.com and Tmall.com, consumers were often purchasing products in large sizes for household use in laundry care (e.g., 2,000-3,000ml) and home care disinfectants (e.g., 1,000-1,200ml).

- Outlook

-

- Consumers are expected to prefer pack types that offer convenience such as stand-up pouches and packs with zip/press closures. Stand-up pouches are convenient because they are easy to transport, store, and use. Packs with zip/press closures keep the product away from oxygen and the atmosphere. As a result, stand-up pouches are estimated to grow at 10.6% CAGR by volume over the 2021-2025 period.

- Consumers are expected to shift to larger pack sizes, especially in laundry care and toilet care, owing to the long shelf life of the products and lower price per liter/kg offered by such sizes. Within liquid detergents in laundry care, plastic pouches are expected to rise due to their convenience and the growing use of refill packs. The proportion of plastic screw closures is also expected to grow as this design enables consumers to refill their detergent bottles more efficiently without spillage.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- Confectionary products derive their demand from impulse purchases, get-togethers, and other social and corporate gatherings. The pandemic-induced restrictions on movement affected these activities to a great extent. Thus, confectionary packaging declined by 0.1% by volume in 2020. The pandemic boosted health awareness among the consumers which affected the demand for confectionary.

- The economic impact of the pandemic made consumers' price sensitive. As a result, companies chose flexible plastic over metal food cans and rigid plastic as it is an affordable option. As a result, flexible packaging recorded 1.9% growth by volume despite an overall decline of 1.1% by volume in total packaging in 2020.

- Trends

-

- The trend towards giving chocolate confectionery as a gift has been on the rise and has become an important source of sales. The key target audience for products such as boxed assortments is the young population, with this influencing their design. Soft materials and attractive packaging are common.

- Processed fruit and vegetables witnessed growth as consumers look for healthy snack This drove growth in the packaging solutions required for such products. Before the outbreak of COVID-19, the erosion of more formal eating habits and ever-busier consumer lifestyles drove the increasing demand for healthy snack options. In combination with the health and wellness trend, this trend led the consumers to prefer products such as shelf-stable food. Shelf-stable food mostly comes in metal and glass jars. As a result, these forms witnessed an uptick in demand.

- Outlook

-

- Dairy packaging is seeing a growing consumer awareness of the environmental impact of pack types – in terms of the process of production, sustainability, transportation, and waste. Consumers are expected to pay a premium for sustainable packaging and packaging using recyclable materials, as they become more aware of the environmental effects and carbon footprints of their waste. Increased eco-consciousness is expected to open new opportunities for the packaging industry to grow in terms of packaging volume as well as packaging value.

- Confectionery is expected to struggle during the 2021-2025 period, leading to stagnation in confectionery packaging volumes. The primary constraint on growth in confectionery packaging will be the health and wellness trend. Increasing obesity is likely to be an important feature of public health policy during the forecast period, encouraging consumers to pay greater attention to the consumption of sugar. This will hamper the growth of packaging materials such as flexible plastic and rigid plastic as they are estimated to decline at 2.2% and 0.3% CAGR by volume over 2021-25 in the confectionery industry.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in China

-

Beijing and Shanghai continue lockdown measures as fears of the virus mount

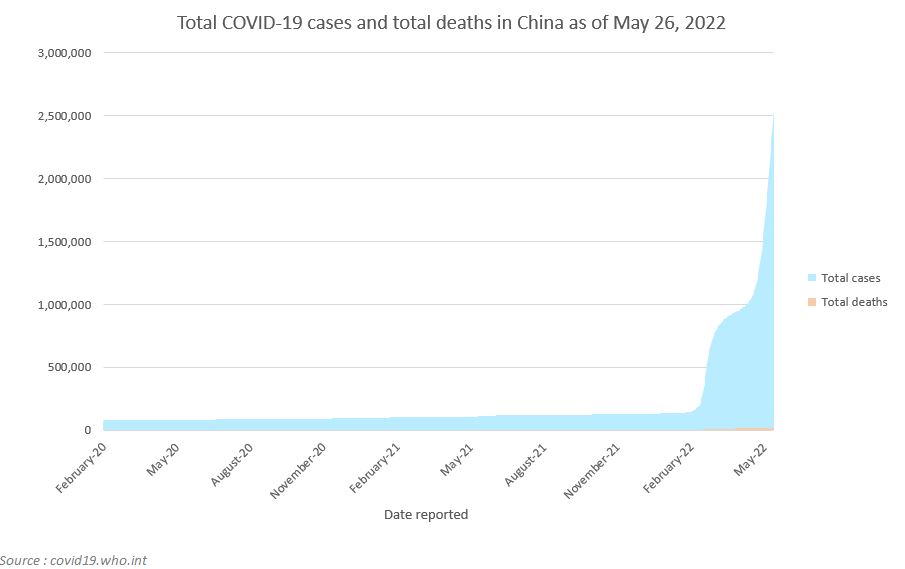

- According to the World Health Organization (WHO), as of May 2022, China had 2,543,706 COVID-19 cases, with 16,151 deaths and 1,809 cases per million inhabitants.

- With concerns about rising infections across the country, authorities in Shanghai aim to maintain most restrictions in place in May before lifting the two-month-old lockdown completely on June 1. Even then, public venues will have to limit crowds to 75% of their capacity.

- In Beijing, instructions for citizens in six of the capital's 16 districts to work from home remain in force, while three more districts encouraged workers to do so, with each district responsible for enforcing its own set of rules. Beijing has already reduced public transportation services, ordering the closure of several shopping malls and other places, as well as the sealing of buildings where new cases have been discovered.

- According to the WHO, total vaccines as of May 20, 2022 stood at 3,442,312,826, corresponding to 87.0 fully vaccinated persons, per 100 people.

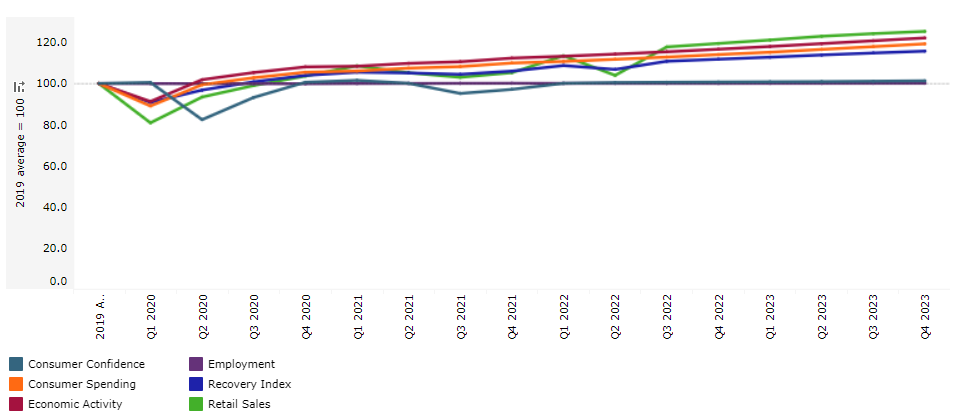

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, China

- Impact on GDP

-

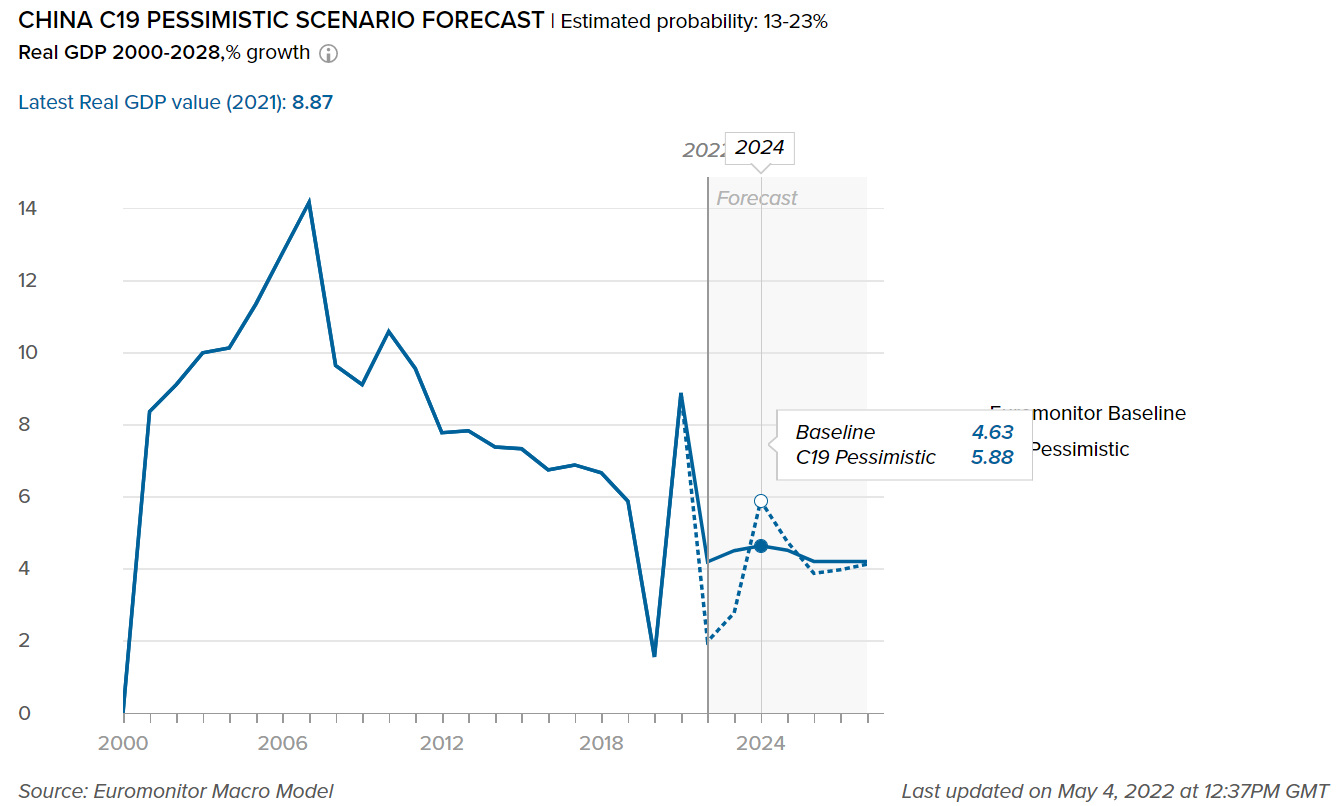

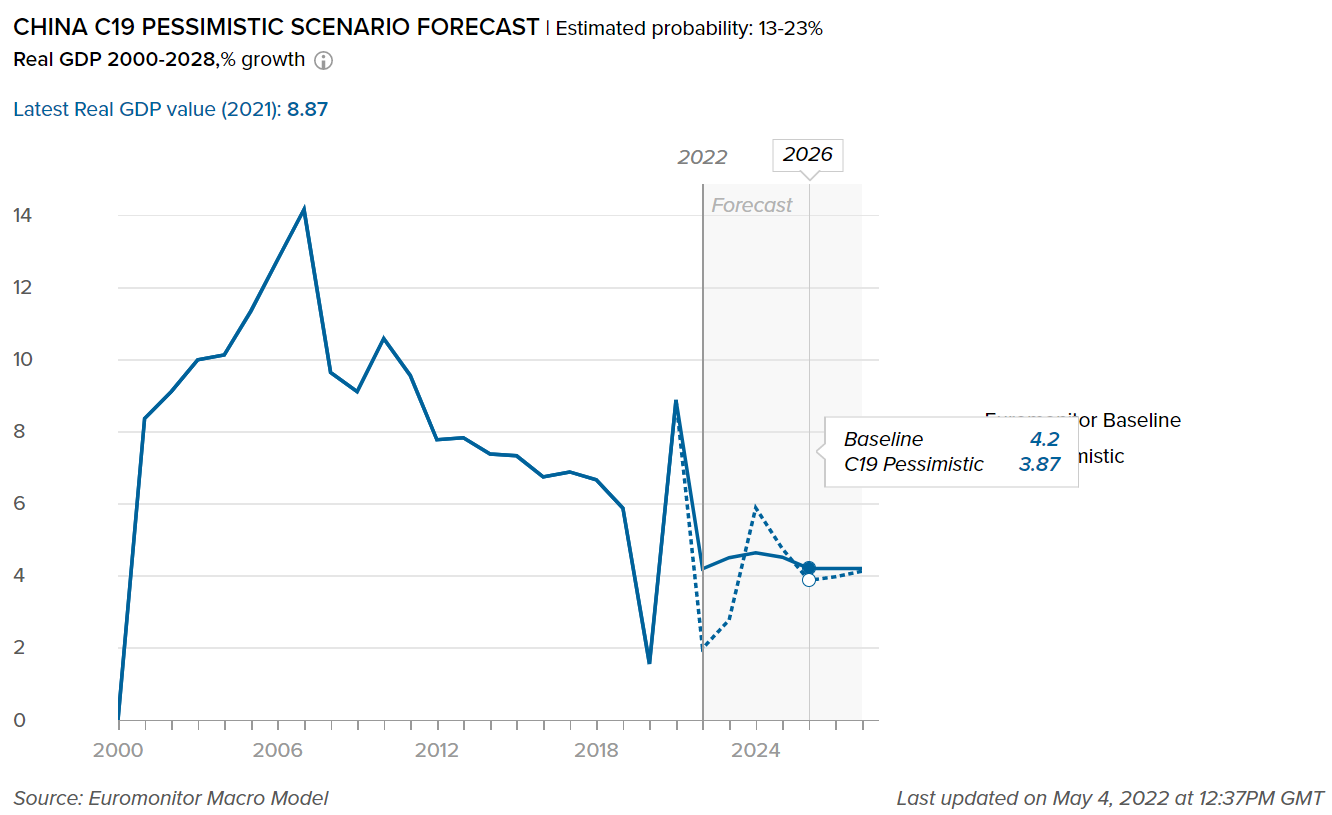

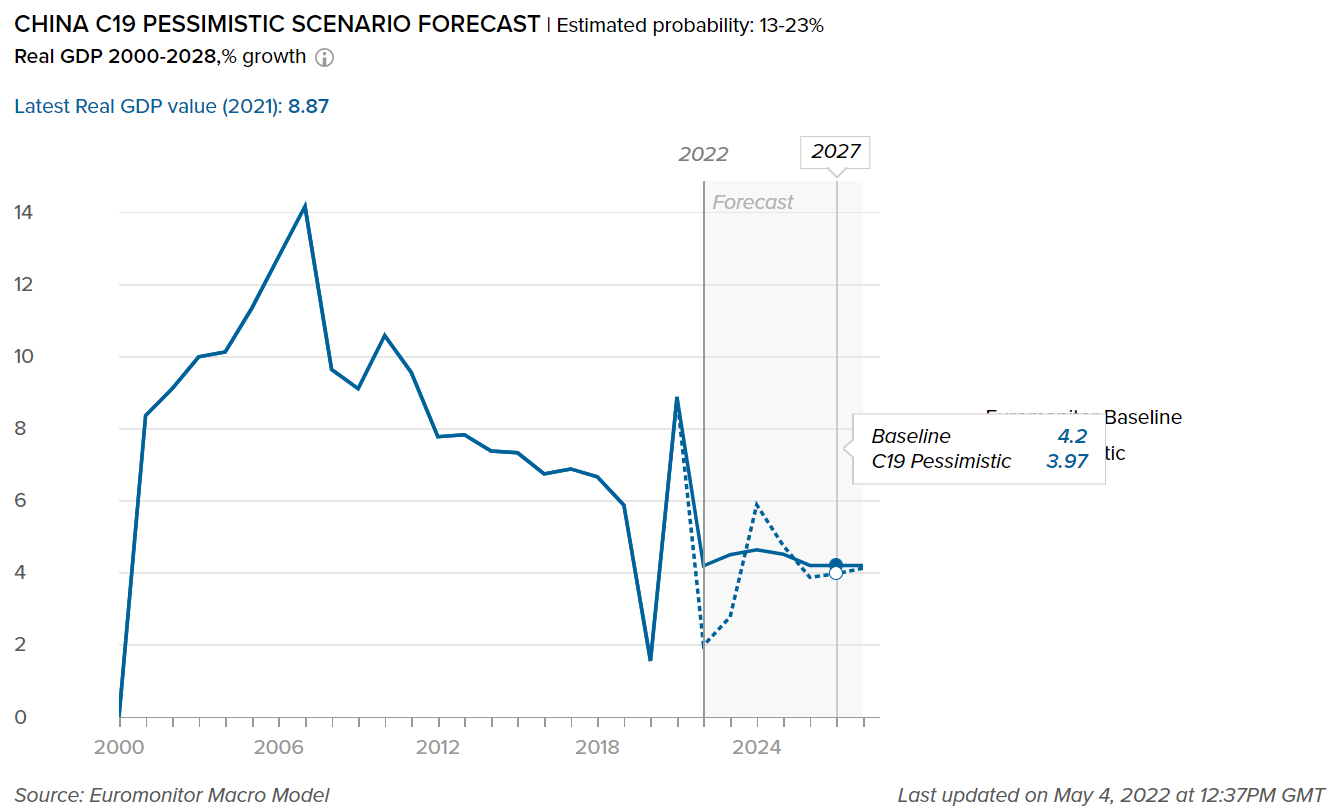

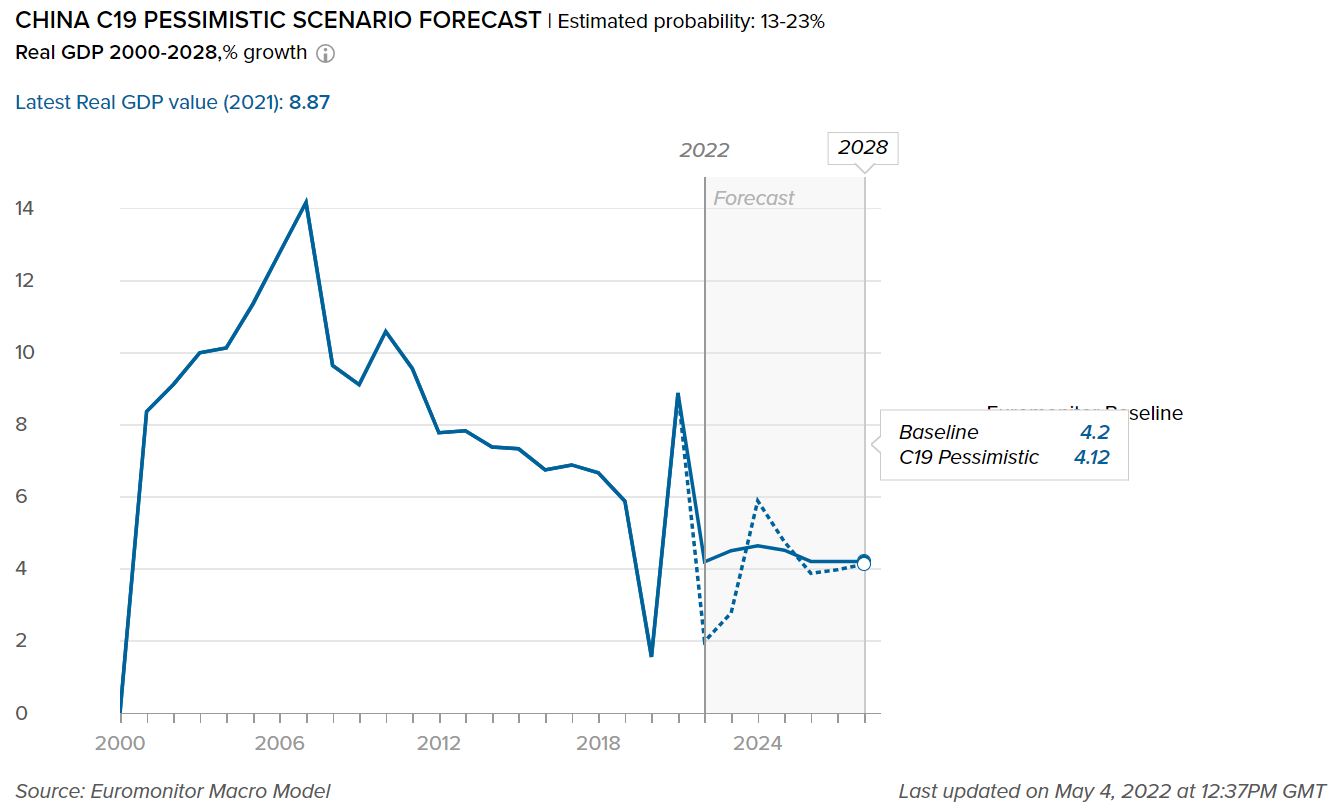

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in China. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

.

Improving business confidence supports recovery, while Inflation is forecast to pick up over 2022 amid easing monetary policy

- In 2021, China's economy performed well, particularly in the first half of the year. China's real GDP expanded by 8.8% in 2021, above Asia Pacific's average growth rate of 6.4%. Strong industrial output, increasing exports, and improving business confidence drove the country's economic growth in 2021.

- After the COVID-19 outbreak, China's labor market recovered quickly. The unemployment rate dropped from 4.2% in 2020 to 3.9% in 2021, well below the pre-pandemic level and far below the Asia Pacific average of 5.2%.

- Inflation in China increased by 1% in 2021, significantly below the government's objective of 3%, due to a delayed rebound in private spending and a slowdown in the highly indebted property industry. Furthermore, government measures to ensure the supply of products contributed to price stability. To help reduce commodity price spikes, China's state reserves authority released coal and several metals, including copper and aluminum, from the national reserves this year. However, due to a more accommodating monetary policy, supply chain bottlenecks, and rising commodity prices, inflation is likely to go up in 2022, and remain around 2.3% in the medium term.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below shows the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

A focus on healthy living boosted the growth of beauty and personal care in China

- Following a downturn in growth in 2020 due to COVID-19, the beauty and personal care industry witnessed a swift return in 2021, with 21.2% growth between 2019-2021, as per the Baseline scenario forecast. Consumer interest in healthy living has grown, propelling the growth of associated products such as dermocosmetics, functional skin care, and clean beauty. Several categories of skin care showed great resilience and growth potential in 2021, as promotions and discounts got more aggressive. Anti-aging products, for example, continued to perform well as customer demand grew and diversified into increasingly segmented demands. Dermocosmetics also grew at a strong rate in 2021, owing to consumers' rising interest in skin health and the increasing prevalence of sensitive skin conditions.

- According to Euromonitor’s Baseline scenario forecast, home care saw 1.2% increase during 2019-2021. COVID-19 increased consumer hygiene awareness, which benefited antibacterial products that saw sales surge in a variety of home care categories, including laundry, dishwashing, and surface care. Natural and green items were widely welcomed by customers in 2021, alongside antibacterial products, albeit being somewhat niche, as people sought to make a beneficial impact on the environment while also saving money on utilities and ensuring safety and health.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors covered in China. Our “most probable” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Post-lockdown conditions provide potential for products such as cooking sauces and dairy alternatives

- The return to normal social and economic activities following the easing of stringent limitations established to contain COVID-19, created significant prospects for the growth of cooking ingredients and meals. As customers return to their hectic modern lifestyles and have little time to prepare and cook meals from scratch, retail sales are experiencing favorable conditions for increased demand for convenient products such as cooking sauces. Furthermore, such products appeal to many younger consumers who, unlike their parents, do not have a basic understanding of cooking. To benefit from this growth, players such as Totole have launched cooking sauces of popular Chinese dishes such as mapo tofu and sweet and sour ribs.

- With healthy eating forming part of the government’s health strategy, milk products and alternatives enjoyed growth in China aided by the government's push to increase dairy consumption, resulting in 1.7% growth over 2019-2021, based on Euromonitor’s Baseline scenario forecast. With a growing number of consumers buying more dairy products, fresh milk performed well supported by the recent entry of three domestic dairy giants, Yili, Jiabao, and Mengniu. On the other hand, yogurt also witnessed dynamic growth due to its healthy and protein-rich image.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

21,174

21,724

9.9%

Home Care Packaging

11,670

11,637

0.1%

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

199,149

206,161

0.08%

Flexible Packaging

319,964

330,191

-0.02%

Metal

47,772

49,971

0.02%

Paper-based Containers

42,792

44,913

4.34%

Glass

55,751

55,267

-0.08%

Liquid Cartons

87,007

86,252

0.00%

Sustainable packaging will be a development focus for product launches in the future

- The continued demand for surface care products in 2021 as a result of the heightened hygiene and cleanliness levels saw the main pack type of HDPE bottles used in bathroom cleaners, floor cleaners, and kitchen cleaners continuing to grow in 2021, with further growth expected in 2022. HDPE bottles are widely used in surface care products due to their sturdiness and resistance to chemicals.

- Numerous partnerships have taken place among organizations since the COVID-19 pandemic lockdown began in order to present society with creative solutions. Dow has signed a strategic 3-way Memorandum of Understanding with Liby, a leading Chinese laundry care brand, and LOVERE, an internet environmental tech company. According to a statement from the company, the signing of the Memorandum of Understanding advances Dow's new sustainability goal of collecting, reusing, or recycling one million tonnes of plastic through direct actions and partnerships by 2030, and 100% of its packaging applications being reusable or recyclable by 2035.

- On the other hand, leading beauty and personal care players in China are continually updating their packaging to keep up with current sustainability trends, with brand owners being more conscious of the carbon footprint they leave in their sourcing and manufacturing operations. Leading companies are investing in environmentally- friendly solutions such as lighter packaging and a greater use of 100% recyclable and recycled materials. At least 80% of Herborist's outside packaging is now recyclable and biodegradable, while the local brand's folding carton packaging is made entirely of recycled paper. Origins-branded items are packaged in Forest Stewardship Council-certified recyclable paper-based packaging, which contains about 50% recycled fiber. Origins recently started a bottle recycling campaign, rewarding customers with free product samples in exchange for returned bottles of any brand.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recovery Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.