Overview

- Packaging Overview

-

2020 Total Packaging Market Size (million units):

390,575

2015-20 Total Packaging Historic CAGR:

7.2%

2021-25 Total Packaging Forecast CAGR:

6.1%

Packaging Industry

2020 Market Size (million units)

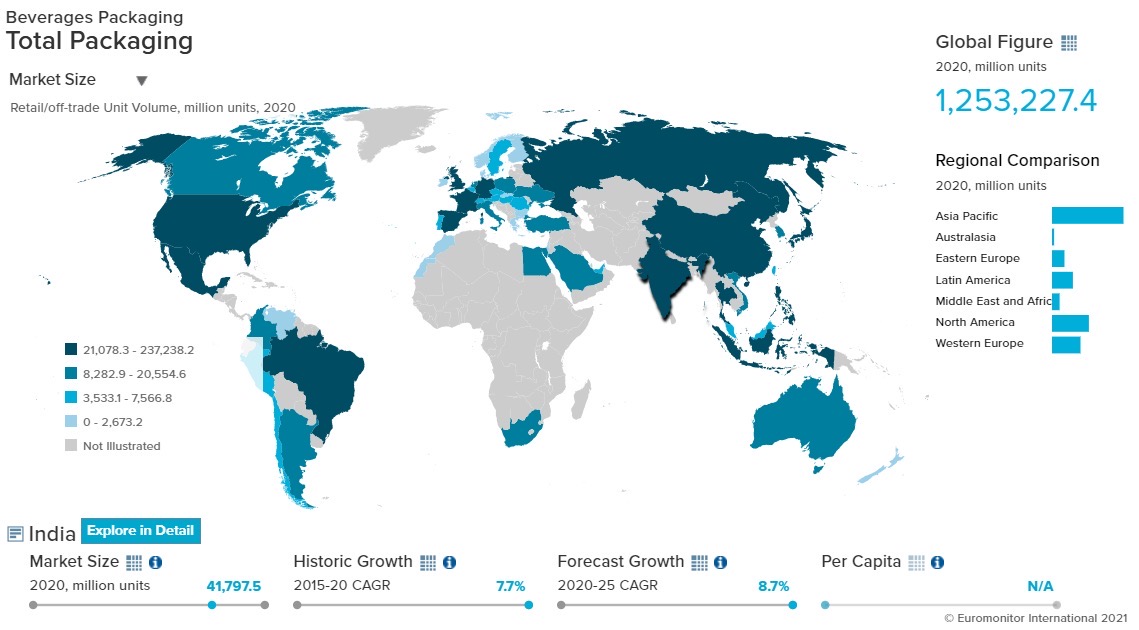

Beverages Packaging

41,654

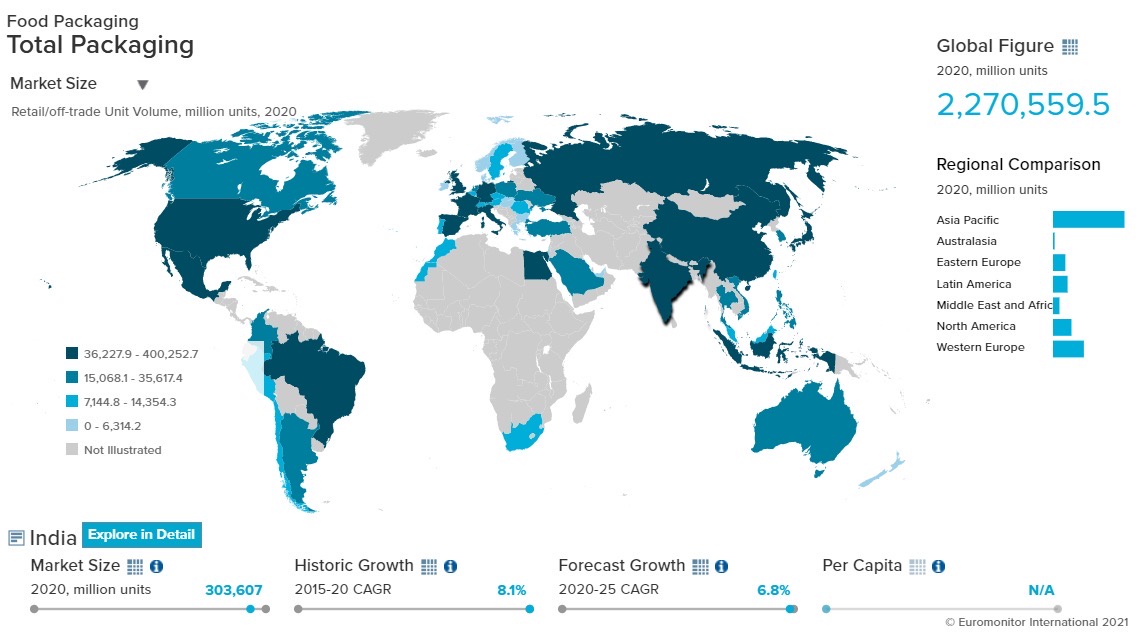

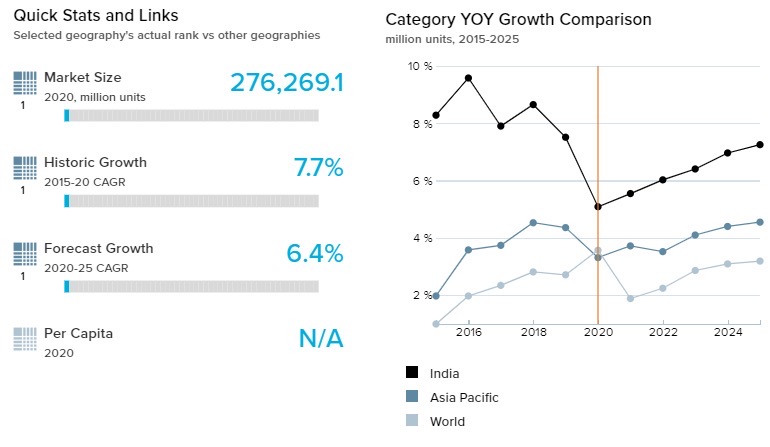

Food Packaging

303,607

Beauty and Personal Care Packaging

23,227

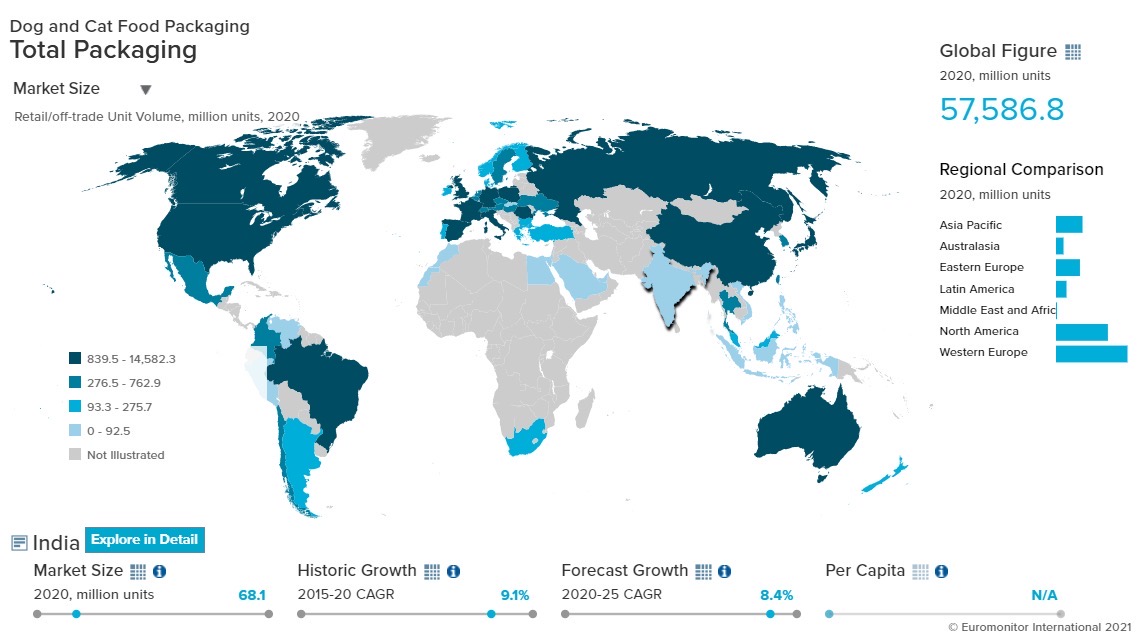

Dog and Cat Food Packaging

60

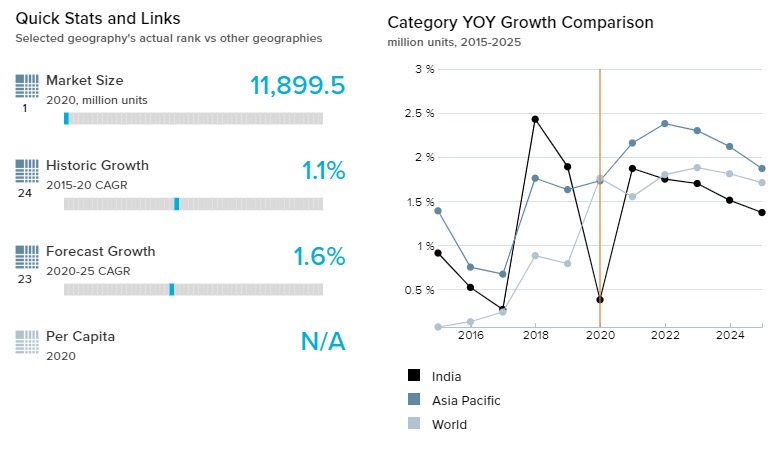

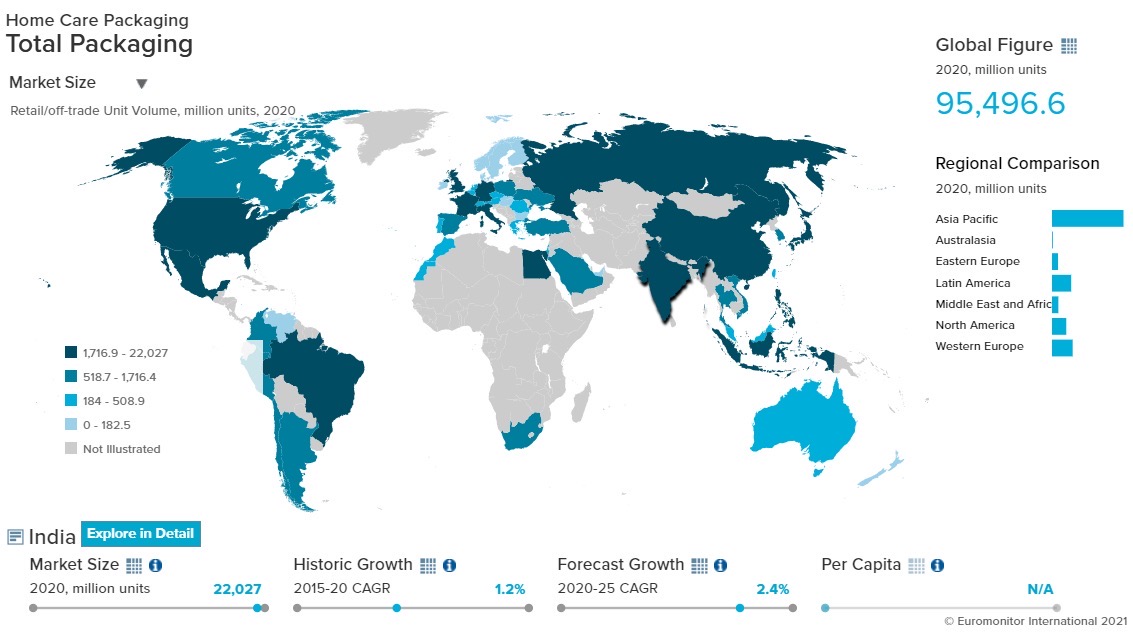

Home Care Packaging

22,027

Packaging Type

2020 Market Size (million units)

Rigid Plastic

41,451

Flexible Packaging

312,433

Metal

2,163

Paper-based Containers

11,359

Glass

11,462

Liquid Cartons

11,466

- Key Trends

-

Beauty and personal care have seen a rise in demand for smaller packs in some product areas. The trend, accelerated by COVID-19, was underway before the pandemic as consumers shifted to pocket-sized cosmetics and fragrances, as well as deodorants, for on-the-go application. Bottled water is consumed mainly by urban consumers, particularly those in first-tier cities, many of whom have been shifting away from the use of purified tap water and towards the purchase of water in 20-liter PET bottles. With Indian citizens more likely to switch houses more frequently during their lifetimes, bottled water in bulk has greater appeal than installed water purifiers, which must be serviced and have their filters changed regularly.

While glass remained the dominant pack type for alcoholic drinks due to its traditional use, demand is beginning to slowly shift away from the packaging material. The move has been spurred by industry players’ experimentation with different pack types as they sought to reach out to new consumer bases while expanding the range of consumption occasions across all alcoholic drinks categories. Metal beverage cans and brick liquid cartons are expected to grow at the cost of glass bottles in alcoholic drinks and they are likely to remain the most dynamic pack types over the 2021-2025 period.

- Packaging Legislation

-

In January 2019, India announced new regulations about food packaging. Key points centered around migration limits for certain contaminants in plastic packaging materials, pigments, and colorants used in packaging and printing ink and specific migration limits for metal containments in plastic materials to meet EU limits. Specifically, plastic migration limits have been set at 60mg/kg or 10mg/dm2 (1dm2 = 0.01m2), with no visible color migration; pigments or colorants for uses in plastic in contact with food particles and drinking water must conform to the new standards, as must printing inks used in food packaging.

- Recycling and the Environment

-

Consumer awareness of plastic waste and its pollutant effects is growing and a slow transition towards a more conscious consumption continues. In response, several companies have been swift to introduce products presented in sustainable packaging. Beauty and personal care player SoulTree is one of the first companies to introduce color cosmetics such as Kajal and lipstick in recyclable packaging instead of the commonly used specialty cosmetic containers. They have also introduced biodegradable packaging, which can decompose naturally. Similarly, Soapworks India now packages all of its products in tin or cardboard and parcels them in newspaper and duct tape in place of bubble-wrap and plastic tape, ensuring packaging is completely plastic-free.

- Packaging Design and Labelling

-

Alcohol packaging is prohibited from positive claims. The FSSAI regulates alcoholic drinks in India to help protect the health and safety of consumers. Under the Food Product Safety & Standards (Alcoholic Beverages Standard) Regulations 2018, the FSSAI looks to ensure that new rules are adhered to. The most recent regulation that specifies labeling requirements for beverages containing more than 0.5 percent alcohol by volume includes the declaration of the product’s alcohol content; that it does not contain any nutritional information; that there are no positive health claims; a restriction on the word “non-intoxicating” or words implying similar meaning; and an allergen and statutory warning.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

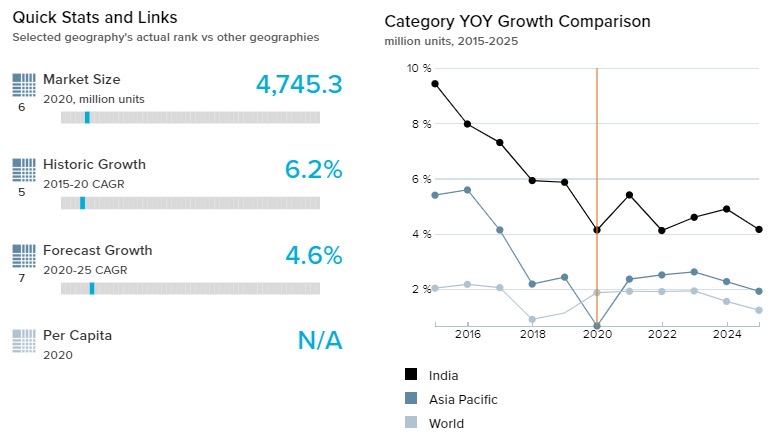

- In the soft drinks industry, consumers preferred flexible packaging and PET bottles over returnable glass bottles due to concerns in regard to the spread of the COVID-19 virus. Moreover, consumers also preferred to buy products online to reduce the frequency of their trips to supermarkets and their exposure to the virus. Flexible packaging, being easier to transport and store, benefited at the expense of glass 7.0% by volume in 2020.

- Flexible packaging remains dominant in hot drinks packaging due to the widespread use of flexible aluminum/plastic in both coffee and tea. The popularity of flexible aluminum/plastic is tied to its numerous advantages, including its lightweight nature, portability, low cost, and ability to preserve the freshness of products. The pack type remains extremely popular as a refill for reusable metal tins and glass jars. As a result, flexible packaging grew by 5.1% by volume in the hot drinks industry in 2020.

- Trends

-

- The change in alcohol consumption habits, driven by the health-consciousness of consumers and drinking occasions impacted pack sizes. Companies are making smaller pack sizes available to help control consumers’ alcohol intake. The impact is prominent in wine, with branded players and private labels alike, launching smaller bottle sizes for their wine offerings. In wine and many other alcoholic drinks, larger formats such as 1,500ml are in decline. For beer, cider, and RTDs, the craft movement is pushing canned formats and subsequently driving the growth of the 330ml format.

- Folding cartons are a major pack type that is gaining in popularity for hot drinks in larger sizes as consumers stock up on products such as fruit/herbal teas, green teas, etc. This growth can be attributed to the fact that the COVID-19 pandemic led to lockdowns, including forcing all food service establishments to remain completely closed for extended periods. Consumers were therefore entirely dependent on home caffeine consumption.

- Outlook

-

- Many single-serve pack sizes are expected to launch in response to the expected rise in on-the-go consumption once normalcy is achieved over 2021-25, post pandemic. This trend is likely to be visible in RTD coffee, RTD tea, and bottled water, but also in juice and carbonates, where bigger pack sizes tend to be more common. The rising demand for smaller pack sizes can be attributed to increasingly busy lifestyles and demographic changes and the number of smaller households in the country.

- Hot drinks packaging is expected to follow the trend of premiumization and value growth as the hot drinks market in India expands. The pack types that add a more luxurious feel to a product or have some sort of value-added benefit in the packaging itself, for example, biodegradable pack types, are expected to gain popularity over 2021-25. Consumers are expected to prefer environmentally sustainable pack types, but within a budget-friendly price range and with the same level of quality.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

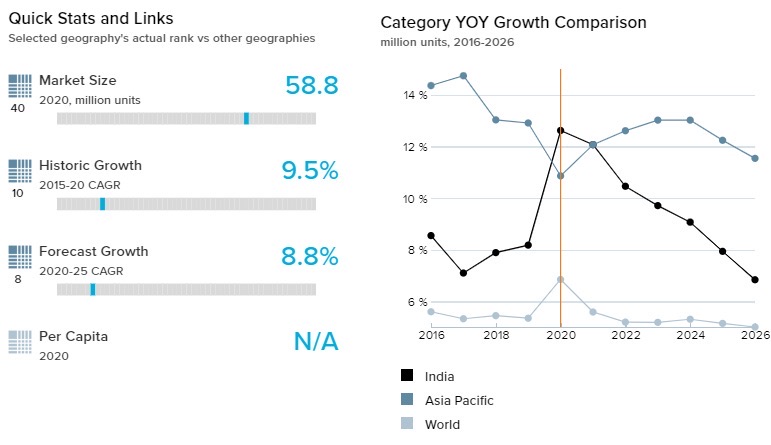

- The price-sensitive Indian consumer seeks out pack sizes that provide the best value for money. In response to that, companies are pricing their 5kg, 8kg, and 10kg packs more competitively than their smaller packs, leading to increased interest. Zip/press closures benefitted from this trend as consumers find this type of closure convenient when buying larger pack sizes, as it ensures freshness. This is also in line with the growing demand for flexible plastic packaging, which is proving best suited to maintaining product integrity. As a result, flexible packaging grew by 10.9% by volume in 2020.

- Manufacturers are increasingly introducing a variety of pack sizes to meet varying needs of different sizes and breeds of pets and the disposable incomes of pet owners. Higher socioeconomic households often have larger homes that can cater to bigger dogs or a greater number of dogs and/or cats. Thus, companies are offering dog and cat food in bulk, such as larger pack sizes in premium packaging such as stand-up pouches and zip/press pouches of 10kg, 12kg, or 20kg, as they can easily afford and store them. On the other hand, pet owners with smaller homes prefer to own smaller pets. These householders, therefore, look for smaller pack sizes as the daily food intake of small dogs is lower in comparison to large dogs. Thus, companies are offering small pack sizes in flexible plastic and folding cartons for such consumers.

- Trends

-

- The focus of brands has mainly been introducing different pack sizes rather than launching new pack types. But the trend is now changing as companies are investing in the development of new pack types. With consumers in India becoming more conscious about preserving the surrounding environment, sustainable packaging is another area that companies are exploring. For example, the launch of Nestlé Purina’s Beyond Simply range in flexible plastic packaging resembles recycled paper.

- Natural and premium ranges have also been on the rise as Indian pet owners in the upper or upper-middle-class segment focus on Due to the rising levels of health and wellness awareness and the burgeoning pet humanization trend, pet owners have become more conscious of the kind of products they buy. To capitalize on this, dog food manufacturers are offering premium products with organic, natural, and healthy ingredients along with premium packaging with features such as zip/press closures and handles for large packs, etc.

- Outlook

-

- E-commerce is expected to continue to see dynamic growth in sales of dog and cat food. As consumers lead increasingly busy lives, they are looking for more convenience, which has helped them offer benefits such as express delivery, customizable ordering options, and access to consumer product reviews. E-commerce platforms recorded strong growth in sales since introducing pet food online by offering a wider choice of products and pack sizes than what is available in the store. E-commerce is expected to see further development within dog and cat food over 2021-25.

Click here for more detailed information from Euromonitor on the dog and cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- The economic impact of COVID-19 forced many consumers to restrict their spending on non-essential products. This means that while categories like bath and shower, hair care, and skincare were relatively resilient, categories such as fragrances and sun care declined. The pandemic also had a direct impact on packaging, with consumers increasingly becoming more price-conscious, meaning sustainability was taking a backseat and less expensive pack types like flexible plastic were becoming much more popular than alternatives like folding cartons, rigid plastic, or glass. Major brand owners like L’Oréal focused on selling smaller-sized products packed in flexible plastic as these sizes were the only ones that many of the cash-strapped middle-income consumers could afford. As a result, flexible packaging grew by 0.4% by volume in 2020.

- Bath and shower packaging recorded strong growth in 2020, with consumers prioritizing spending on items that focus on health and hygiene over beauty as they attempted to protect themselves and their families from contracting the COVID-19 virus. In bath and shower packaging, strong growth was seen by 200ml stand-up pouches in bath additives and 500ml plastic pouch refill packs in liquid soap. As a result, flexible packaging grew by 3.3% by volume in 2020.

- Trends

-

- The trend among men to have a beard affected men’s pre-shave, post-shave, razors, and blades categories. This trend, coupled with lockdown restrictions, further negatively impacted the men’s shaving categories in 2020. This led to a decline of 3.1% by volume in these categories in 2020. On the contrary, larger packs of razors and blades saw an overall increase. This can be attributed to consumers who shave regularly spending on larger packs that provide lower costs per unit.

- Packaging formats in facial cleansing wipes, hand care, and both liquid and bar soaps saw sales boosted during the early stages of the pandemic due to panic-buying. These products were of central importance during the pandemic due to newly developed rigorous daily hygiene routines. Liquid and bar soaps retained their status as crucial to preventing the spread of COVID-19, with hand creams in demand to compensate for the drying effect of frequent handwashing. Fragrance packaging suffered due to consumers’ economic woes, with many Indians using less expensive body sprays. Moreover, home seclusion and working from home measures further undermined the demand for fragrances in 2020. The dramatic fall in travel and tourism contributed to a decline in sun care packaging during the year as well.

- Outlook

-

- Due to the economic impact of COVID-19, small-sized packs are expected to remain popular in the coming years. Price sensitivity is expected to continue to be seen even in the post-pandemic period, meaning that the demand for smaller-sized packs is expected to increase over 2021-25. Smaller-sized packs are expected to attract the populations in tier-2 and tier-3 cities, and they can also help brand owners to bring the population in rural India into the beauty product consumer cycle.

- Ayurvedic products in beauty and personal care previously involved less attractive packaging and primarily catered to older generations. However, the new entrants in the space are expected to invest heavily in developing new packaging formats to attract new generations with higher disposable incomes. Building stories or retail experiences around holistic living and sustainability are likely to connect better with the younger population and will go a long way to ensuring growth in the future. While the share of premium Ayurvedic products is comparatively small, it is expected to grow significantly over the 2021-2025 period.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- Against the backdrop of the COVID-19 pandemic, consumers were buying large volumes of disinfectants, floor cleaners, and surface cleaners to regularly sanitize their homes. As demand was rising for larger packs, players switched to flexible plastic as it is not only seen as safer but also more affordable and long-lasting. This trend was prevalent across various home care categories, including laundry aids, gel air fresheners, powder detergents, other home insecticides, metal polish, hand dishwashing, and shoe polish. As a result, flexible packaging grew 2.0% by volume in 2020.

- Flexible packaging is used across multiple home care categories, but the use of flexible plastic and paper in laundry care packaging, such as powder detergent and bar detergent, is its biggest contributor. Insecticides and dishwashing are other categories where flexible packaging is widely used. Refill packs available in pouch formats are also becoming common on retail shelves, as consumers who are regular users of certain brands buy these packs. Manufacturers are taking advantage of this trend by launching large value packs such as 1kg, 3kg, and 5kg.

- Trends

-

- People are buying daily-use items in bulk to avoid regular visits to the store. Categories such as powder detergents, other home insecticides, or laundry aidssaw a surge in demand for larger pack sizes. Due to the pandemic, given the decreased disposable income of the Indian population, smaller pack sizes were ubiquitous in the retail landscape.

- Sustainability and environmental concerns are driving change within the industry, as central and state governments in India have been regularly taking steps to ban single-use plastic. Manufacturers such as Hindustan Unilever, in collaboration with social entrepreneurs and partners in various Indian cities, initiated several projects to collect, segregate, and safely dispose of plastic waste. It is also taking steps through strategic partnerships to convert plastic waste into energy (electricity). The company is pledging to make 100% of plastic packaging reusable, recyclable, or compostable by 2025. They also pledge that 25% of all the plastic used will be from recycled sources by the same year.

- Outlook

-

- India currently lacks the infrastructure to process plastic waste. But the Indian Government, as well as local bodies, are expected to invest heavily in building infrastructure to process plastic waste. Awareness among consumers is expected to drive companies to shift from single-use plastic to sustainable packaging solutions. These triggers are expected to propel manufacturers into action, with most companies planning to make plastic packaging recyclable, reusable, or compostable.

- The pandemic boosted the sale of home care products through the e-commerce channel. This is expected to lead various companies to redesign their product packaging to ensure minimal waste and lighter/quicker shipping. Procter & Gamble’s Eco-Box is one such product. According to the company, the Eco-Box, which contains a sealed bag of ultra-compacted liquid fabric care, requires less packaging, up to 60% less plastic, and does not need any secondary packaging or bubble wrap.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- In ready meals packaging, smaller packs of 240g are popular and are often packaged in flexible plastic packaging because it is sufficient for a single meal and is easy to carry and store leftovers. Unlike thin wall plastic containersthat are mostly used in frozen ready meals, flexible plastic can be used in the shelf-stable, dried, and the frozen categories. These pack types are cost-effective for manufacturers and convenient for consumers to dispose of. In 2020, however, 400g, 500g, and 1,000g pack sizes recorded particularly strong growth. The surge in demand for these larger formats during the COVID-19 pandemic can be linked to the greater demand for stockpiling. As a result, flexible packaging grew by 18.8% by volume in ready meals in 2020.

- Processed meat and seafood packaging was negatively affected by false rumors that spread across the country linking the consumption of chicken products with COVID-19 infection. However, the category benefited from the rising awareness of the safety of packaged meat and seafood products in the second half of 2020. This boosted sales of processed meat and seafood packaging, with flexible packaging continuing to represent the most popular pack type within the category. Sales were boosted by this trend in urban areas in 2020, where consumers are more likely to own personal freezers. As a result, flexible packaging grew by 1.7% by volume in processed meat and seafood packaging in 2020.

- Trends

-

- During the COVID-19 pandemic, at-home consumption of dairy products increased considerably. Consumers adapted their shopping habits to make less frequent shopping trips, thus reducing their potential exposure to the virus as much as possible. This shift in shopping habits benefited shelf-stable products, as consumers were able to stockpile products with longer expiration dates such as shelf-stable milk in 2020. The most popular pack size, however, was 1,000ml as many consumers preferred to stockpile larger pack sizes in the face of future uncertainty.

- Transparent flexible packaging is enjoying an uptick in processed fruit and vegetable packaging. Freshness is a key driver when buying fruits and vegetables with visual freshness playing a major role when consumers make purchasing decisions. Manufacturers are striving to ensure that the product is visible through the packaging and providing additional information consumers seek when buying such products. See-through packaging is most popular in pack types such as thin wall plastic containers and flexible plastic, the latter of which is by far the most common pack type in processed fruit and vegetable packaging.

- Outlook

-

- The growth of shelf-stable seafood is good news for metal food cans. Smoked tuna, pickled fish, dried meat, and other shelf-stable meat and seafood products are commonly sold in metal food cans. Although sales of these types of products remain low in India, mainly because consumers prefer fresh or frozen products over shelf-stable, they are increasingly consumed as delicacies and will continue to grow in popularity over 2021-25. International dishes have been influencing consumers in India for a long time and will continue to gain wider consumer interest in the coming years. Shelf-stable meat and seafood are expected to grow as a result of this.

- From 2021, aseptic packaging is expected to gain considerable traction in Indian dairy and will continue to gain popularity among manufacturers and consumers over 2021-25. Aseptic packaging is expected to gain from government food safety initiatives as well as efforts to reduce plastic packaging. Demand for aseptic dairy packaging is likely to rise due to demand for products with an extended shelf life, as well as its greater convenience, transportation, and recyclability benefits. India is seen as a market with great potential for the use of aseptic packaging, which is viewed as being eco-friendly and meets the government’s new regulations.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in India

-

The Ministry of Railways issues mandates to all passengers to wear masks on trains

- According to the World Health Organization (WHO), India had 43,144,820 COVID-19 cases as of May 2022, with 524,525 deaths and 32,082 cases per million inhabitants.

- Amid a rise in cases, the railways ministry is advising all passengers to wear masks while traveling in trains, and specifically at entry and exit points.

- Kerala and Delhi continue to report the maximum number of daily cases, with the city of Delhi reporting a positive rate of 30.6% on January 14, the highest during the third wave of the pandemic, due mostly to the highly transmissible Omicron strain of the coronavirus.

- According to the WHO, as of May 24, 2022, a total of 1,941,328,608 vaccines have been administered, representing 64.1 fully vaccinated persons, per 100 people.

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, India

- Impact on GDP

-

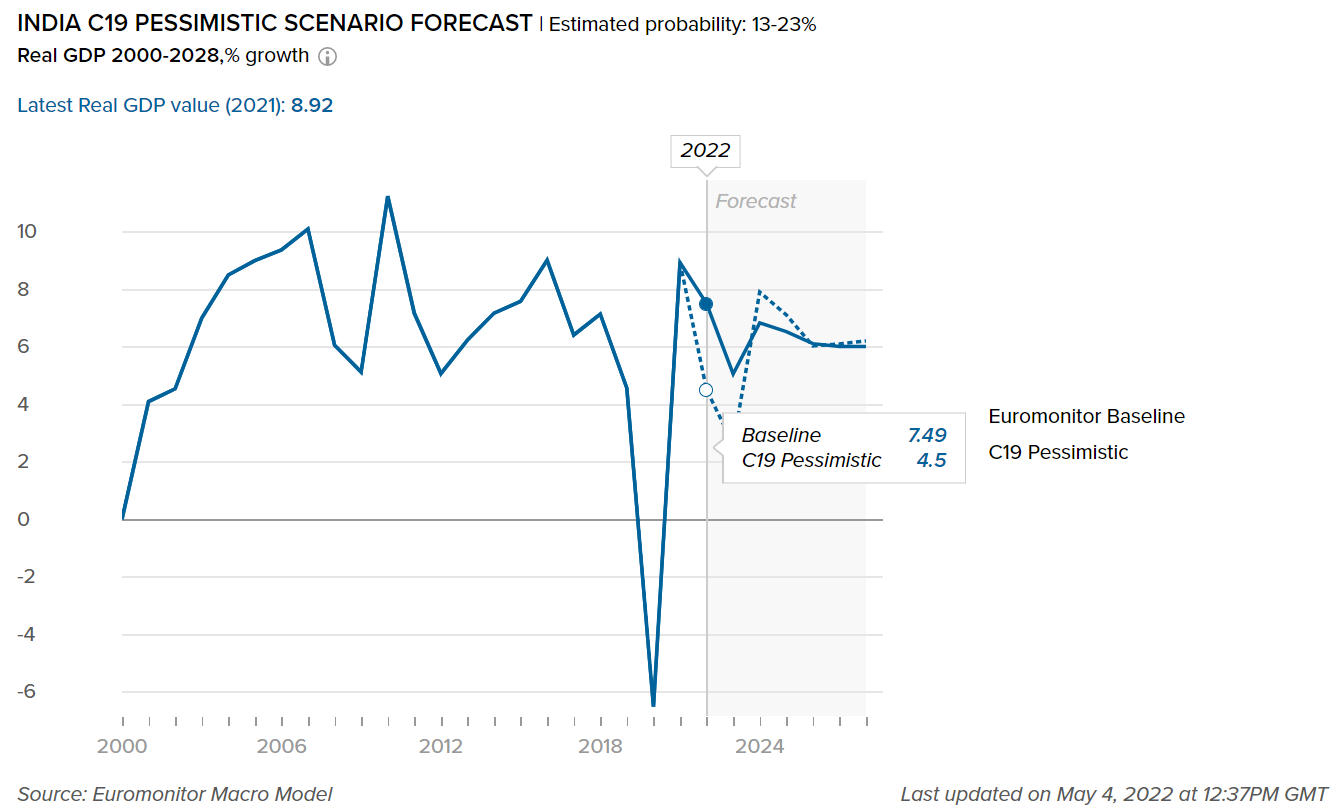

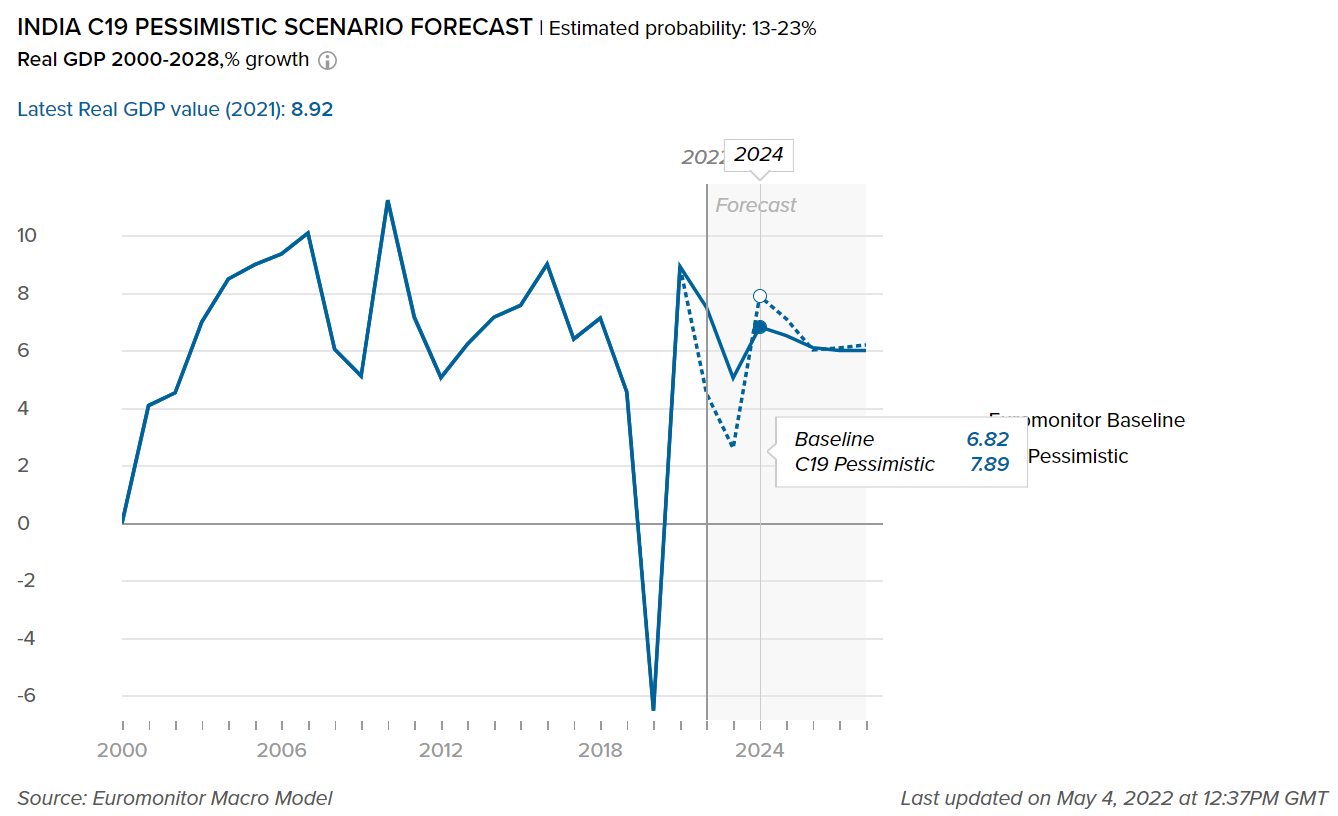

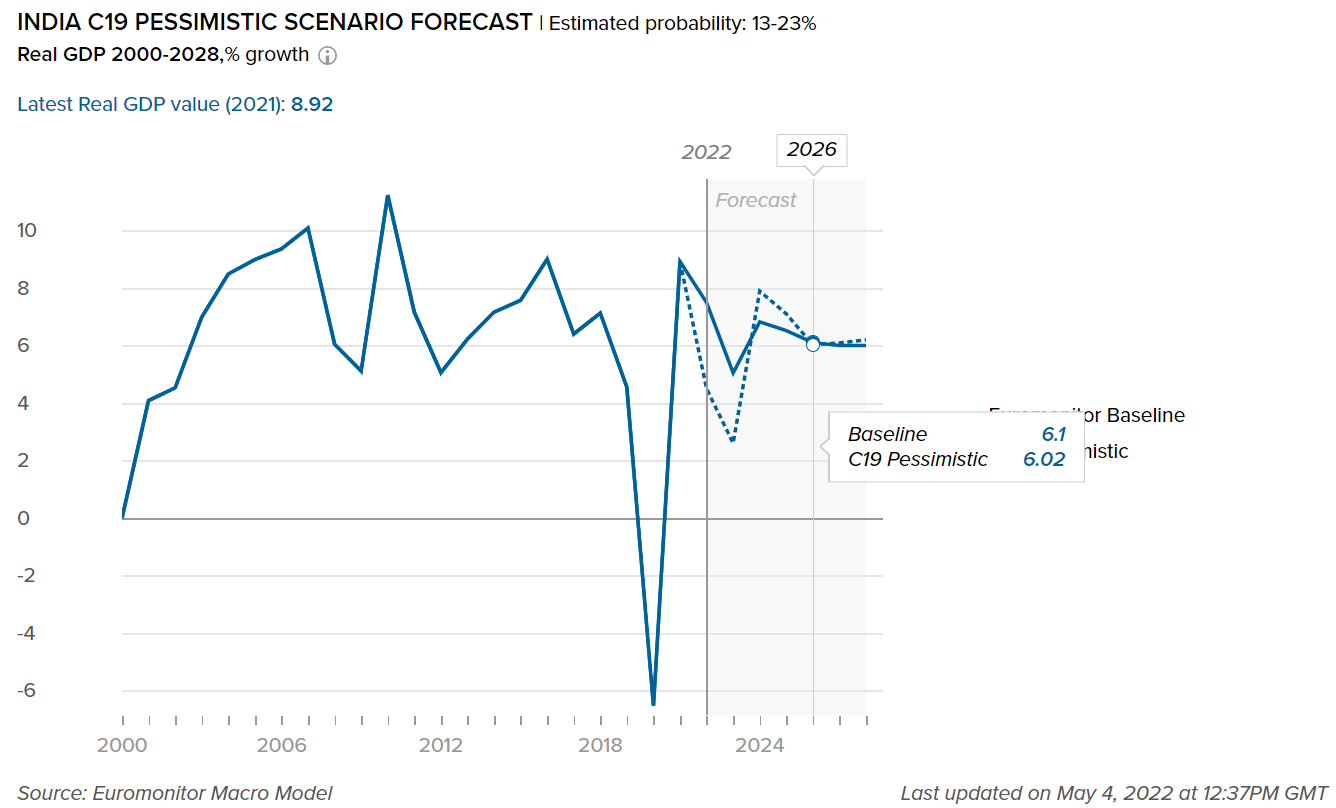

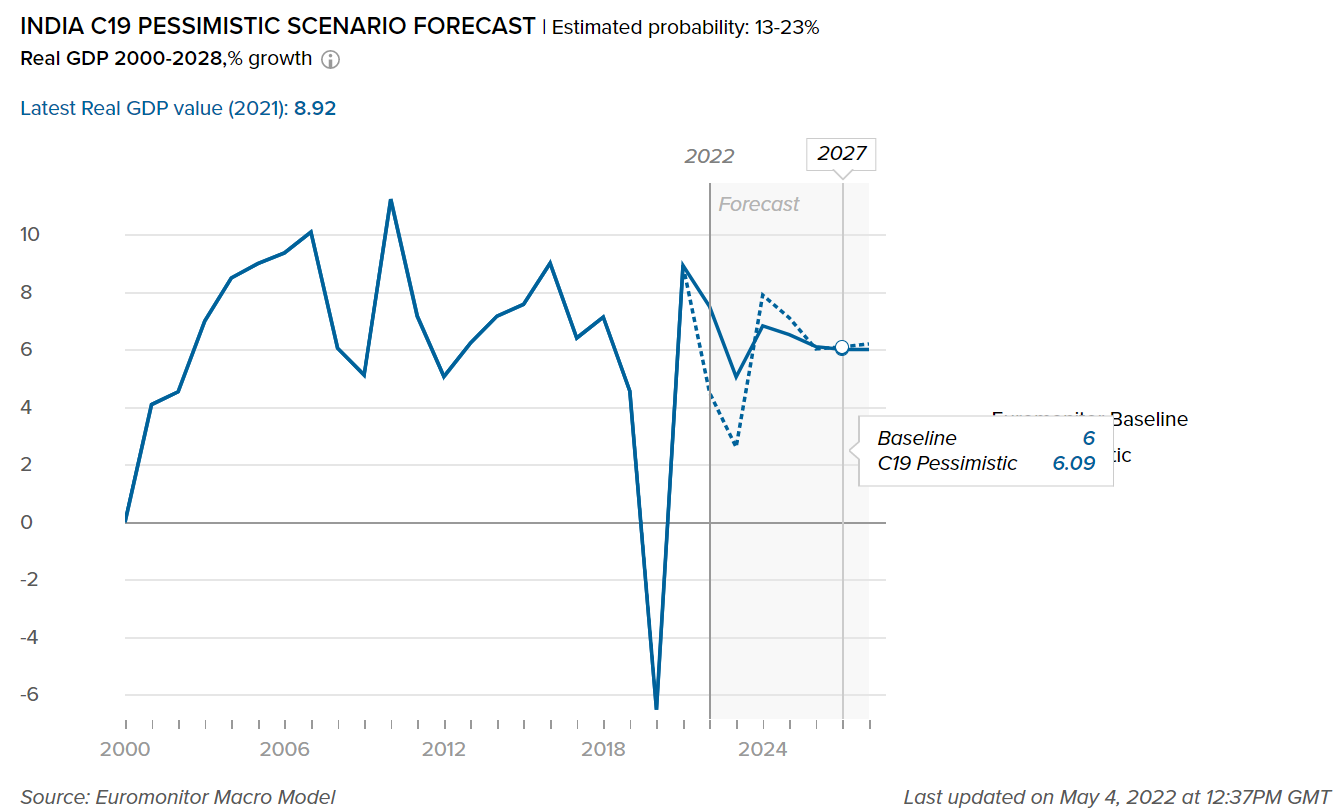

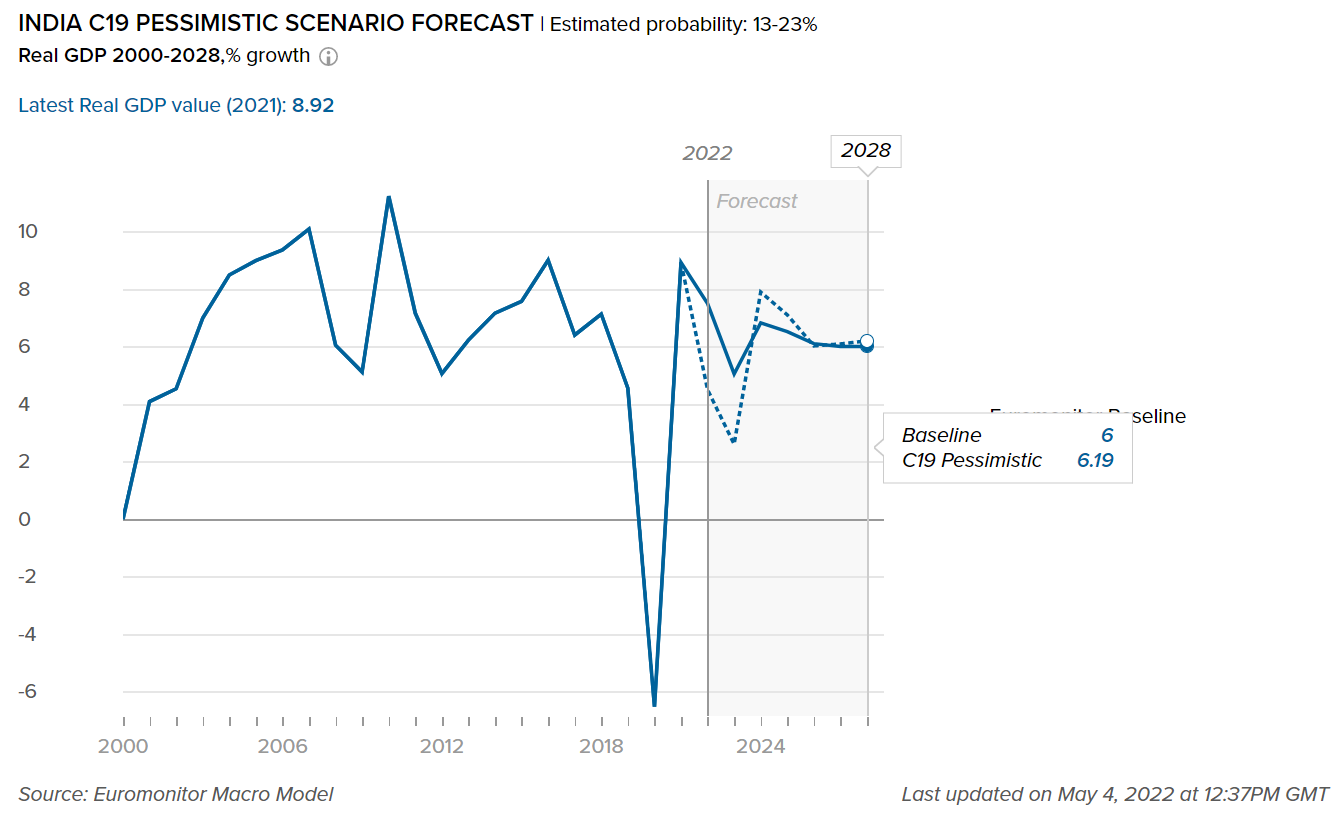

This graph shows our “most probable” and “worst case” scenarios of how COVID-19 will impact real GDP value in India. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Inflation pressures are mounting in India

- India's economy rebounded strongly in 2021, with annual real GDP growing by 8.9%. Although the International Monetary Fund (IMF) has reduced India's GDP prediction due to geopolitical uncertainties induced by the war in Ukraine, annual real GDP growth is likely to exceed the Asia Pacific average in 2022 and is forecast at 7.4%. Growth is predicted to be supported by an increase in private consumption as well as increased government spending, particularly on infrastructure upgrades.

- India demonstrates that foreign direct investment (FDI) is a driver of economic progress, with inflows of 2.4% of GDP in 2020 (latest statistics available), well above the Asia Pacific average of 1.8%. Given the growing importance of the Indian economy in the global perspective, India was the world's fifth largest beneficiary of FDI in US dollars in 2020. M&A activity is a major source of foreign direct investment (FDI) in India, with recent agreements involving US, Canadian, and Singaporean corporations buying Indian properties. The FDI landscape in India is improving, as the government has relaxed the regulatory environment around foreign investments by reducing the number of permits necessary by the central bank.

- India's inflation rate is projected to grow significantly in the short term as a result of Russia's invasion of Ukraine, which has led global food and oil prices to surge. Higher global oil prices will be one of the key reasons for higher inflation, as the country is a net energy importer. Food prices are rising as well, especially for vegetables, poultry, and edible oils, leading to increased inflation. The inflation rate reached about 7.0% in March 2022, above the Reserve Bank of India's (RBI) upper ceiling of 2.0-6.0%. As a result, the RBI has raised benchmark interest rates ahead of schedule to keep inflation under control.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below shows the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

Cooking ingredients and staple foods set for high growth as consumers move toward packaged products

- Sauces, dressings, and condiments are expected to enjoy high demand in India, with strong growth projected through 2022, due to dry sauces, herbs, and spices being an important ingredient of many traditional Indian meals. COVID-19 has lowered demand for unpackaged items, and this trend is projected to continue during the forecast period, as people become increasingly concerned about how clean and safe the food they consume is. As a result, demand for packaged cooking items should benefit. Companies are also likely to launch new spice blends to make cooking more convenient for consumers, particularly those who are not as experienced or skilled in the kitchen.

- Rice is a staple meal in India, consumed on a daily basis, with the category of rice, pasta, and noodles remaining by far the largest in 2021/2022. Although most rice is still purchased unpackaged, there has been a significant shift toward packaged products over the review period, which has been hastened by the advent of COVID-19. The move from unpackaged to packaged rice products is expected to accelerate, due to the hygiene benefits of packaged products.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors covered in India. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst-case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Alcoholic drinks continue to suffer the effects of COVID-19’s breakout

- Alcoholic beverages were one of COVID-19's hardest-hit industries in 2019/2022, with revenues falling. This was largely due to the government's decision to put a statewide ban on the manufacture and sale of alcohol during the 41-day lockdown (March 25-May 3), deeming these products non-essential. During the ban, there was an increase in illegal alcoholic beverage sales. The government decided to prohibit alcoholic beverages due to a World Health Organization (WHO) mandate claiming that alcoholic beverages decrease immunity, as well as the product's potential to exacerbate the already high number of domestic violence cases. Due to the ban, no sales were registered in both the off-trade and on-trade channels throughout the period, and the industry continues to see declining demand, down 19.2% over 2019-2022, based on the Euromonitor Baseline scenario forecast.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

23,899

24,554

0.1%

Home Care Packaging

21,580

22,448

2.1%

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

38,245

42,108

0.00%

Flexible Packaging

285,959

299,788

0.11%

Metal

2,315

2,477

0.06%

Paper-based Containers

12,057

12,790

1.20%

Glass

11,885

12,339

0.03%

Liquid Cartons

12,717

13,898

0.00%

HDPE expected to perform well in home care packaging

- Due to the irregular opening of offices and schools/universities throughout 2021, many home care categories saw an increase in demand. Furthermore, in 2021, there was still increased interest in cleanliness and sanitization, which benefited important categories such as surface care, toilet care, and household insecticides. As a result, key pack types in these categories, such as HDPE bottles for toilet care, HDPE bottles and PET bottles for surface care, and flexible plastic and folding cartons for household insecticides, benefited.

- As a large number of Indians adopted hybrid working methods during the pandemic, and this tendency is expected to continue, convenience will play a big part in future purchase decisions. Demand for home appliances such as automatic washing machines and dishwashers is likely to rise, and as a result, home care categories in India, such as liquid detergents and dishwasher tablets, are projected to benefit. As a result of their widespread use in this category, HDPE bottles are projected to perform well in liquid detergents, while alternative pack types, including folding cartons and plastic pouches, are expected to gain appeal as dishwasher tablets become more common in the country.

- Sustainability and environmental concerns have already influenced industrial change, with India's national and state governments taking moves to prohibit single-use plastic. In accordance with global objectives, one of the important developments projected in home care over the forecast period is a growing focus on sustainability and developing clean, green labels. A growing number of businesses are emphasizing their efforts on having a lower environmental impact, whether through modifications in packaging or product formulation. Hindustan Unilever is stepping up its sustainability initiatives; it designed an in-store vending machine for popular brands including Surf Excel, Vim, and Comfort, where customers can fill their own bottles and obtain a discount. Surf Excel also pushed the use of 100% biodegradable active ingredients in the formulation of the product and shifted to recyclable bottles produced from 50% recycled plastic.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recovery Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.