Overview

- Packaging Overview

-

2020 Total Packaging Market Size (million units):

82,510

2015-20 Total Packaging Historic CAGR:

0.9%

2021-25 Total Packaging Forecast CAGR:

0.0%

Packaging Industry

2020 Market Size (million units)

Beverages Packaging

20,482

Food Packaging

53,960

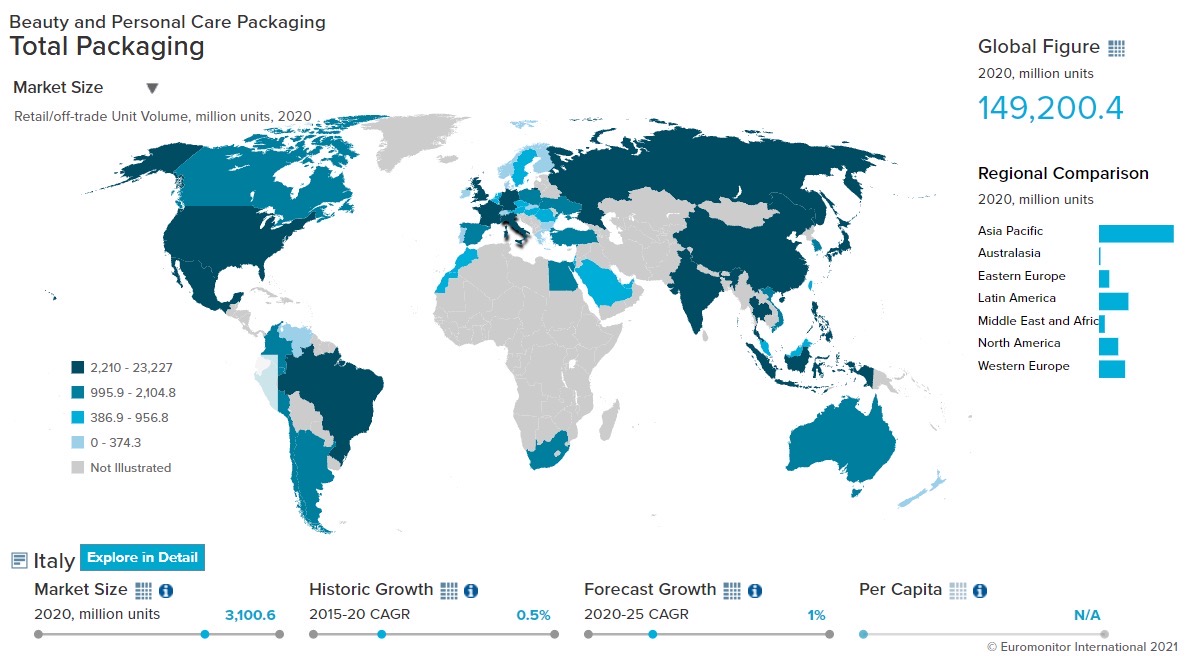

Beauty and Personal Care Packaging

3,099

Dog and Cat Food Packaging

2,456

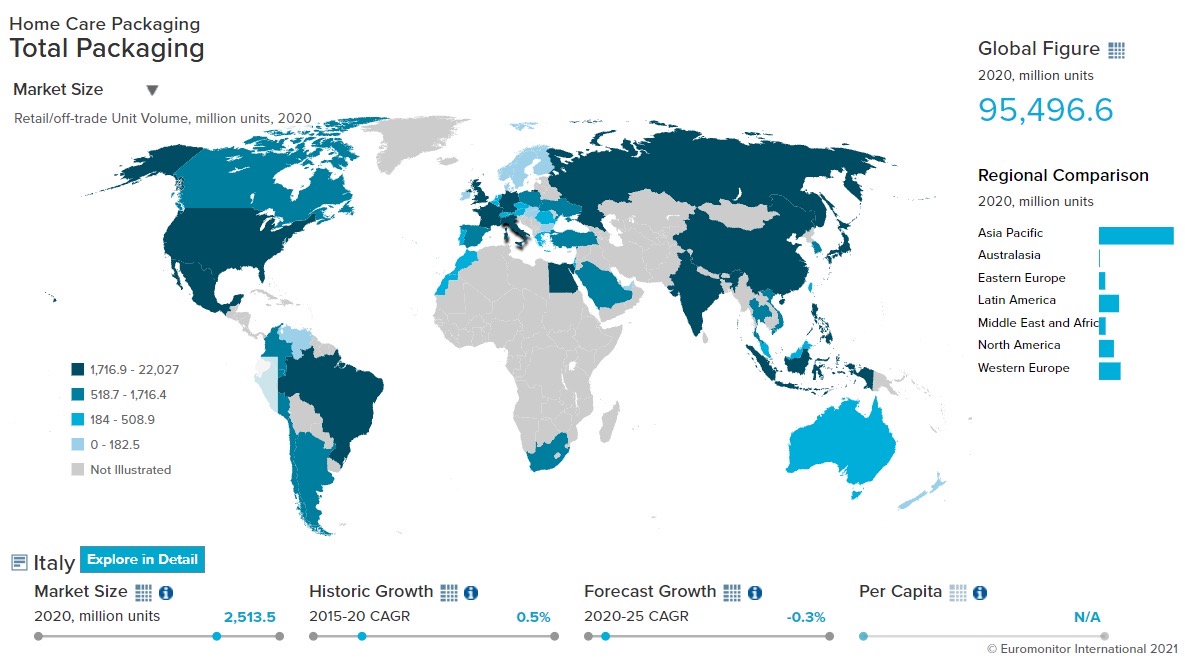

Home Care Packaging

2,514

Packaging Type

2020 Market Size (million units)

Rigid Plastic

27,069

Flexible Packaging

29,795

Metal

6,271

Paper-based Containers

7,762

Glass

8,136

Liquid Cartons

3,476

- Key Trends

-

The pandemic-induced restrictions, fear of contracting the virus, and fear of supply shortage of essential goods led consumers to stockpile products. As a result, large value-for-money packs and multipacks in all packaging industries benefited. On the other hand, home seclusion and travel restrictions affected impulse purchases resulting in low demand for small pack sizes and single-serve packs. The trend of more convenient and user-friendly packaging gained momentum in 2020. As the competition intensifies, players are expected to invest in packaging that is easy to open, handle, and helps keep the product’s freshness intact for longer periods.

Sustainable packaging is fast becoming an industry standard in beauty and personal care, home care, and beverages packaging. Beauty and personal care packaging are increasingly impacted by the trend towards natural and organic beauty in Italy. Consumers who are particularly sensitive to environmental issues are opting to reduce plastic in general, especially single-use plastic, and opt more frequently for glass and aluminum/steel packaging.

- Packaging Legislation

-

In March 2019, the EU approved a directive on single-use plastic. The objective of the directive is to ensure that all plastic packaging placed on the EU market is reusable or recyclable by 2030. Single-use plastic has been banned by this directive. This creates a strong push in Italy towards sustainability. Even though Italy already has a high plastic recycling rate, it has the highest number of consumertakeaway meals in the world. The packaging of those takeaway meals are one of the areas yet to be improved to meet the requirements of these EU directives.

- Recycling and the Environment

-

In the budget law of 2019, the Italian Parliament approved a tax credit for companies purchasing eco-friendly products and packaging. Companies that purchase/use rPET/aluminum/biodegradable material could get a tax credit of 36%, up to a maximum amount of EUR20,000 per beneficiary. The National Packaging Consortium (CONAI) predicts record levels of recycling in Italy in 2021, expecting around 11 million tons of recovered packaging, equal to around 83% of the amount released for consumption, of which just short of 10 million tons will be sent for recycling.

- Packaging Design and Labelling

-

Multi-colored laundry capsules gained popularity in many European countries in recent years, as they are easier to use than traditional laundry detergents. However, being colorful, they have the potential to attract the attention of children, who may swallow them after mistaking the capsules for toys or sweets, and subsequently be poisoned. To protect children from poisoning by laundry capsules, the EU introduced stronger safety measures for liquid detergents in soluble packaging. It is now compulsory that all manufacturers must ensure that the soluble packaging of capsules available in the EU contains an aversive agent that makes children spit the capsule out within six seconds. Since this rule has been implemented, poisoning from these substances has significantly decreased in the EU.

Click here for further detailed macroeconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Flexible plastic is the dominant pack type in coffee, as it is cost-effective, which made it an ideal pack type during the economic slowdown caused by the pandemic. Another benefit of this pack type is that it allows the flexibility of vacuum packaging to retain the product's freshness. As a result, flexible plastic grew by 5.1% by volume in coffee packaging in 2020.

- In soft drinks, large packs received a strong boost as consumers preferred stockpiling products during the pandemic. This is mostly available in the larger pack sizes of 750g, 1,000g, and 1,500g and therefore benefitted from the trend of stockpiling among consumers during the pandemic. The rise of large packs was also supported by the strong growth of e-commerce as bulk buying is preferred through this channel. As large packs are mostly made of flexible plastic, flexible plastic benefited from this trend. As a result, flexible plastic grew by 0.4% by volume in soft drinks packaging in 2020.

- Trends

-

- Wine packaging, which is considered the most conservative, is witnessing a shift in preferences in closure types. Cork currently dominates wine closuresand is associated with the quality of the drink. Any other closure besides cork is perceived by Italian consumers to be an indication of poor-quality wine. However, metal screw closures arebecoming more popular and even being used for high-quality wines. The advantages of the metal screw closure type is that it is significantly less expensive than cork, suitable for wines that do not need to age, easier to export, and allows for more creative designs.

- Sales of soft drinks in glass bottles have taken a hit during the pandemic as HORECA (hotels, restaurants, cafes) establishments were closed down in 2020. Even in retail sales, this pack type suffered due to its premium pricing. On the other hand, PET bottles and liquid cartons fared better due to the convenience they offer in terms of storage. Also, the rise of multipacks boosted the growth of PET bottles as most multipacks are packaged in PET packaging.

- Outlook

-

- In a post-pandemic Italy, low-alcohol and non-alcoholic products are expected to show considerable growth. This will be driven by the health and wellness trend. Less expensive products are likely to see stable performances, as the post-pandemic Italian economy is likely to experience an elongated recovery period. This will be particularly evident in categories such as bourbon, single malt scotch, and champagne. This price-sensitive market is expected to boost flexible packaging as it is economical as compared to other packaging options.

- During the pandemic, soft drinks witnessed a trend towards the rise of large packs. However, with the decline of COVID-19 restrictions, smaller formats are expected to grow over 2021-25. The return of impulse buying, on-the-go purchases, rise of single-serve packs, are expected to cause the growth of smaller formats such as 90ml, 110ml, and 125ml. Moreover, increasingly busier lifestyles and demographic changes, with a growing number of smaller households, are expected to boost demand for single-serve packs.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Dog and cat food packaging continues to see a rising demand for smaller pack sizes such as 50g, 80g, 200g, and 375g. The population of smaller breeds of pets is increasing n Italy. Also, owners are preferring to buy single-serve packs as it is more convenient to use and dispose of. As smaller packs and single-serve units are mostly packed in flexible packaging, it grew by 5.9% by volume in dog and cat food packaging in 2020.

- Italian pet owners are more interested in a greater level of convenience when choosing pet food. As a result, they are opting for more innovative packaging formats such as stand-up pouches with closures that better preserve the product's freshness and provide a longer shelf life. They are favoring smaller pack sizes of stand-up pouches as this helps in controlling portion sizes and limits wastage. As a result, stand-up pouches grew by 6.6% by volume in dog and cat food packaging in 2020.

- Trends

-

- With more consumers viewing dogs and cats as family members, rather than simply as pets or animals, they are paying more attention and money for dog and cat food. This resulted in the growing demand for higher-quality offerings featuring natural ingredients such as mono protein and grain-free diets. This trend boosted premium packaging formats such as stand-up pouches, single-serve packs, and rigid containers.

- Cat treats are witnessing growth as owners are rewarding and pampering their cats by offering cat treats to create a bond with them. This is reflected in squeezable plastic tubes as it is one of the most dynamic pack types across cat treat packaging, which grew by 32.6% by volume in 2020. This can be attributed to the fact that this pack format provides an opportunity for cat owners to bond with their pets by hand feeding them from the tube.

- Outlook

-

- Pet humanization and premiumization trends are expected to continue in dog and cat food packaging over 2021-25. As a part of the premiumization trend, owners are expected to prefer smaller pack sizes as well as single-serve packs of premium/quality food as they are relatively affordable, minimize wastage of food, and keep the product fresh. Consumers are likely to pay more for mono-protein food, free from grain and gluten products, and options without additives and colorants. See-through packaging is also expected to gain ground as consumers are likely to prefer to be able to see their food.

- Sustainability is likely to gain momentum over 2021-25. Increasing awareness among consumers is likely to boost the importance of packaging as it is expected to help manufacturers stand out from the crowd. Pack design and labeling are likely to play an important role in conveying ingredients, origins, sustainability of pack type, etc. Pack labeling is expected to be used to provide transparency by emphasizing the sustainability of production, particularly in the case of premium products.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- As a result of the economic impact of COVID-19, demand for large value packs increased in 2020. Big formats such as stand-up pouches and plastic pouches gained as they offer not only lower unit prices but also the convenience of easy transportation. Plastic pouches are used to refill rigid plastic packaging formats such as HDPE bottles as they are lightweight, easily portable, and offer competitive prices. As a result, stand-up pouches grew by 28.8% by volume in 2020.

- Due to the closure of salons, haircare brands opted for pack formats that are suitable for the retail channel such as packs that can attract consumer attention at the retail store. Thus, brands launched flexible packs with attractive matte and gloss printing. Also, demand for refill packs increased that are also made from flexible plastic. As a result, flexible plastic grew by 21.7% by volume in hair care packaging in 2020.

- Trends

-

- Beauty and personal care packaging are increasingly being impacted by the sustainability trend. Italian consumers, as well as manufacturers, are putting extra effort into reducing unsorted/unseparated waste. Rising consumer awareness is appreciating sustainable packaging formats such as bioplastic, plastic/glass/paper produced from recycled materials, and other packaging that can be recycled. They are particularly avoiding single-use plastics and instead opting for glass and aluminum/steel packaging, formats that are more likely to be recycled and reused.

- Biodegradable plastic is seeing an upward trend as many brands are adopting this type of plastic. L’Oréal launched Ecologic bottles that biodegrade within two years. With the launch of Ecologic bottles, L’Oréal successfully replaced PET bottles with biodegradable plastic. Established brands are investing heavily in the development of biodegradable plastic to replace flexible plastic which is the main pack type in the beauty and personal care sector. Some beauty brands are exploring more creative solutions, using materials like mushrooms, wood pulp, or agar.

- Outlook

-

- Refill models are expected to grow across different beauty verticals. In-store refills are likely to gain momentum over 2021-25 as they are both affordable and sustainable. Many brands are expected to launch refill stations to allow consumers to refill shower gels, hand soaps, shampoos, and conditioners in stores. L’Oréal and Estée Lauder have announced goals to reach carbon neutrality by using reusable packaging and refillable business models.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- During the COVID-19 pandemic, consumers preferred the best value-for-money options like larger packs such as 800ml, 650ml, 500ml, and multipacks of 6/12 units. The use of plastic pouches as stand-up pouches and refill packs is witnessing dynamic growth in Italian home care packaging. Consumers prefer stand-up pouches as they are lightweight, can be opened and closed multiple times, and are easy to recycle. As a result, plastic pouches grew by 22.5% by volume in home care packaging in 2020.

- Growing consumer demand for sustainable and lightweight packaging has contributed to the 5.3% growth of flexible packaging formats within home care packaging in 2020 in terms of volume. For manufacturers, its production uses less energy andit reduces harmful greenhouse gas emissions. While retailers prefer it because it is lighter than rigid plastic bottles and improves logistics and distribution costs. It is also easy to transport from warehouse to store as well, as in the case of online orders that are shipped directly to consumers’ homes.

- Trends

-

- PET bottles continued to dominate liquid detergents and dishwashing due to the advantages it provides in terms of durability and sturdiness. PET bottles are a cost-effective option for manufacturers that became an important concern during the pandemic. PET can be easily recycled and reused, thus, PET bottles are favored by manufacturers as well as consumers for their versatility.

- Tablets remained a popular product type in laundry aids as it provides convenience for consumers and comes in an environmentally friendly pack type, folding cartons. With increasing awareness of the harmful effects of some packaging materials on the environment, consumers are consciously choosing more environmentally friendly pack types.

- Outlook

-

- Refill packs are expected to gain momentum over 2021-25 as they help ease the burden of expenditures on home care products and are seen as more environmentally friendly than buying a new PET or HDPE container. Refill stations or vending machines are expected to be launched by a few brands. Companies are expecting to invest in the research and development of refill packs and reusable packs. Along with that, recycling facilities are likely to see more investment by private players, as well as the government, as Italy lacks sites at which plastic can be collected for recycling.

- The post-pandemic period over 2021-25 is expected to see rising demand for smaller pack sizes that are convenient for quick usage and can be easily disposed of. As a result, the use of small plastic pouches of 15/24 tablets is expected to continue to see dynamic growth in home care packaging, and is likely to be favored by consumers, retailers, e-commerce players, and manufacturers.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- Flexible packaging dominates confectionery packaging as it is easier to handle, transport, and store for retailers, as well as manufacturers. The most popular pack type among flexible packaging is flexible plastic and accounts for almost half of the volume sales in confectionery packaging in 2020. As a result, flexible plastic grew by 4.0% by volume in confectionery packaging in 2020.

- In ready meals packaging, rigid and flexible plastic are growing whereas metal food cans are losing market share since consumers prefer transparent packaging options. Transparent pack types, such as plastic pouches or flexible plastic, reassure consumers of the quality of the product inside, as many consumers prefer to be able to see a product before purchasing it. As a result, plastic pouches grew 33.4% by volume in ready meals packaging in 2020.

- Trends

-

- The demand for single portion and snack-size packaging continued to rise in baby food. As manufacturers and consumers look for alternatives to more traditional glass jars, the number of new releases of baby food in plastic pouches continued to grow. Plastic pouches are perceived as a more convenient format than glass as it is non-breakable and can even be used with a single hand. Demand for single-serve packs as well as smaller packs such as 60g and 85g are rising which further helped plastic pouches. The steady shift away from glass jars towards rigid plastic and plastic pouches is expected to continue even after the pandemic is over.

- Many consumers preferresealable pack types for at-home consumption as they keep products fresh for longer. The resealable packs help consumers to manage their portions while using large packs. Biraghi, one of the main players in packaged hard cheese, is an early mover in resealable on-the-go packs. This innovation allows consumers to eat on-the-go, and also allows for convenient snacks for consumers working or studying at home. As consumer lifestyles are increasingly hectic, more dairy products are likely to be offered in small and resealable packs.

- Outlook

-

- Although the COVID-19 pandemic drove an increase in at-home consumption and stockpiling, normalcy in travel and movement is expected by mid-2022. As a result, on-the-go consumption is expected to return as an important consumer purchase factor. This will lead to a greater demand for smaller pack sizes such as 100g and 125g in the coming years, which are more convenient to carry for single-portion consumption. Plastic pouches, stand-up pouches, packs with zip/press closures, and resealable packs are expected to gain momentum over 2021-25 as convenience will be preferred by consumers.

- Premiumization is a trend that is expected to grow as health consciousness among consumers is on the rise. Consequently, packaging is expected to play a prominent role in distinguishing quality products from the crowd. Thus, glass jars with metal lug closures are expected to be used as premium packaging for products such as tuna fillets in extra virgin olive oil. As consumers continue to demand more sustainable packaging companies are expected to invest in their development.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Italy

-

Traveling with masks is still compulsory, while other travel limitations have been eliminated or adjusted.

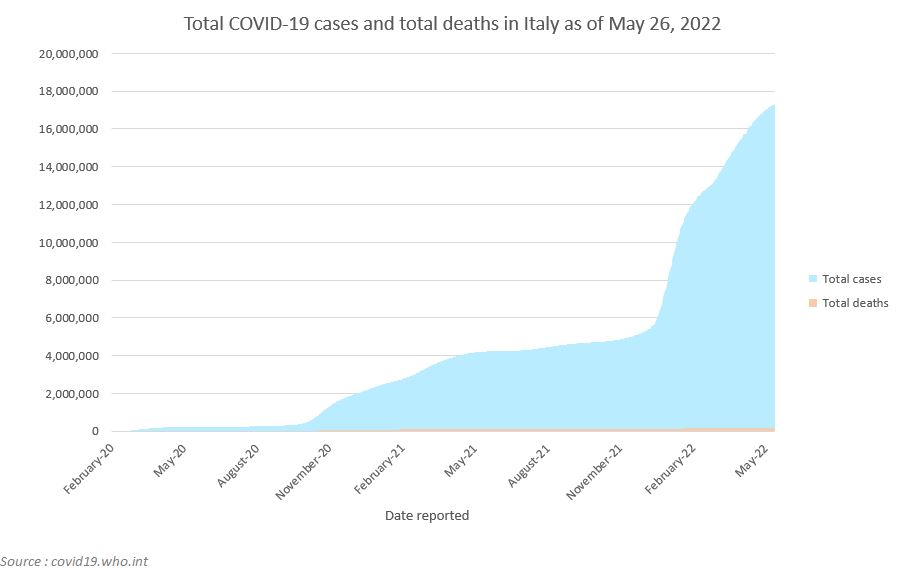

- According to the World Health Organization (WHO), Italy’s total cases amount with 166,264 deaths and 290,275 cases per million inhabitants as of May 2022.

- On March 1, 2022, Italy's border regulations were greatly eased. Instead of being ranked by risk level, countries are now ranked based on an individual's vaccination status. This means that anyone can enter Italy without quarantining for any purpose if they are fully vaccinated or have recovered from COVID-19 lately. This includes visitors from nations previously on List E, who were only permitted to travel for necessary purposes.

- FFP2 masks must still be worn by everyone flying to or from Italy. Passengers must also show proof of completing a first vaccine round within the last nine months, or a complete cycle with booster, which can be older than nine months. Alternatively, individuals can show a certificate of recovery from COVID-19 issued within the last six months, or a negative test result, taken within 48 hours (antigen) or 72 hours (PCR) of departure.

- According to the WHO, as of May 15, 2022, a total of 136,206,350 vaccines have been administered in Italy, representing 79.5 fully vaccinated people, out of 100 in the country.

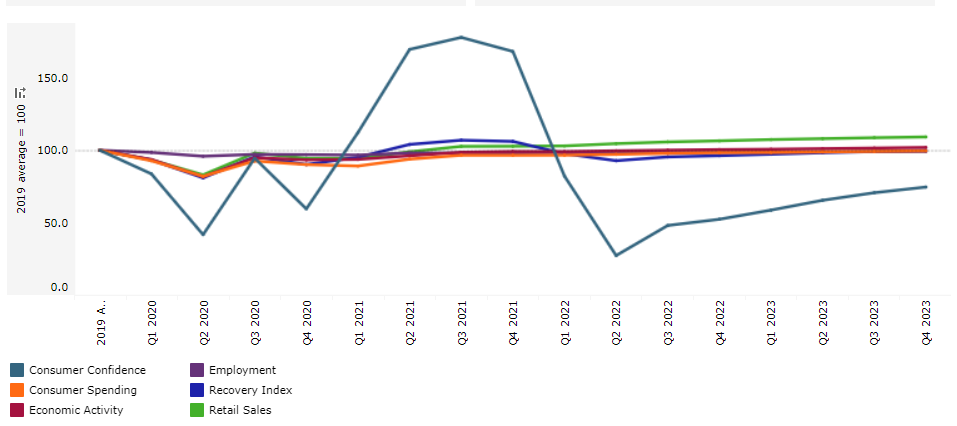

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Italy

- Impact on GDP

-

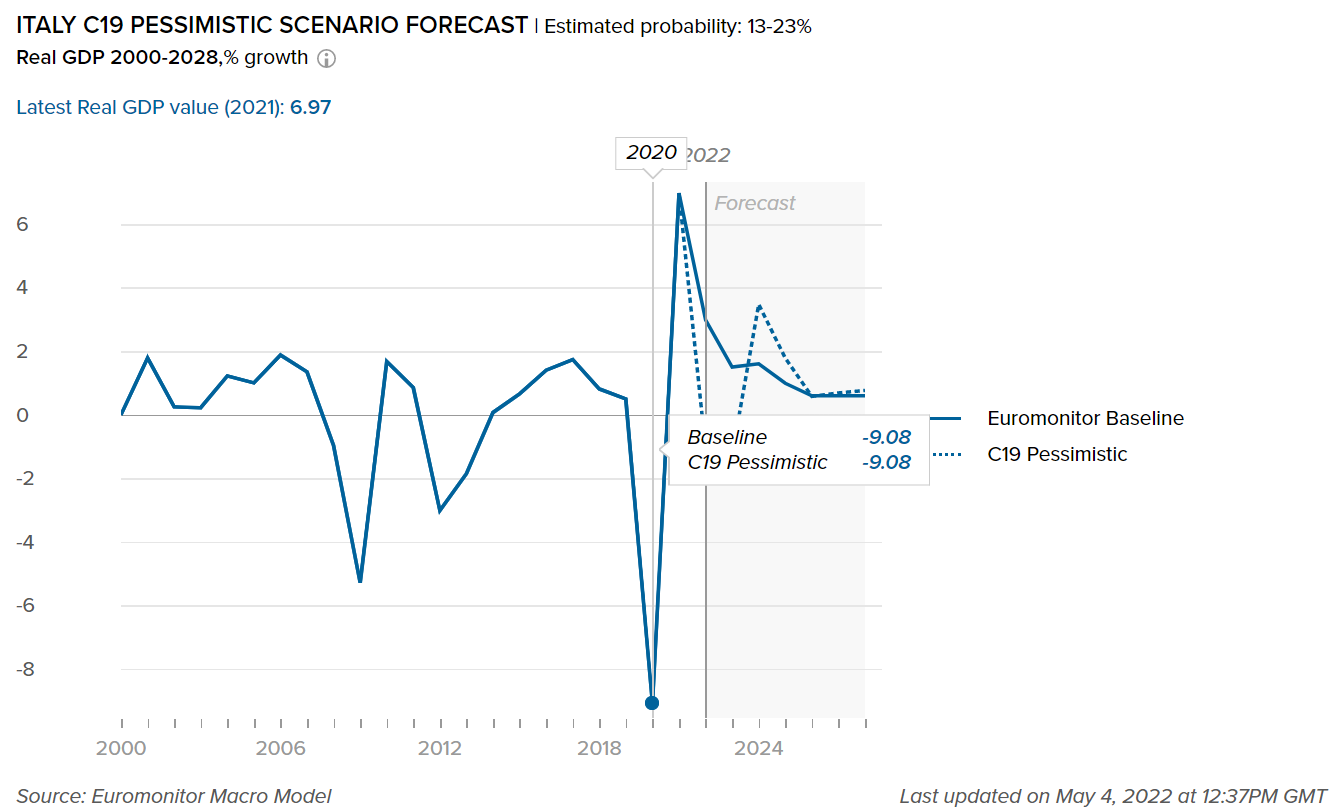

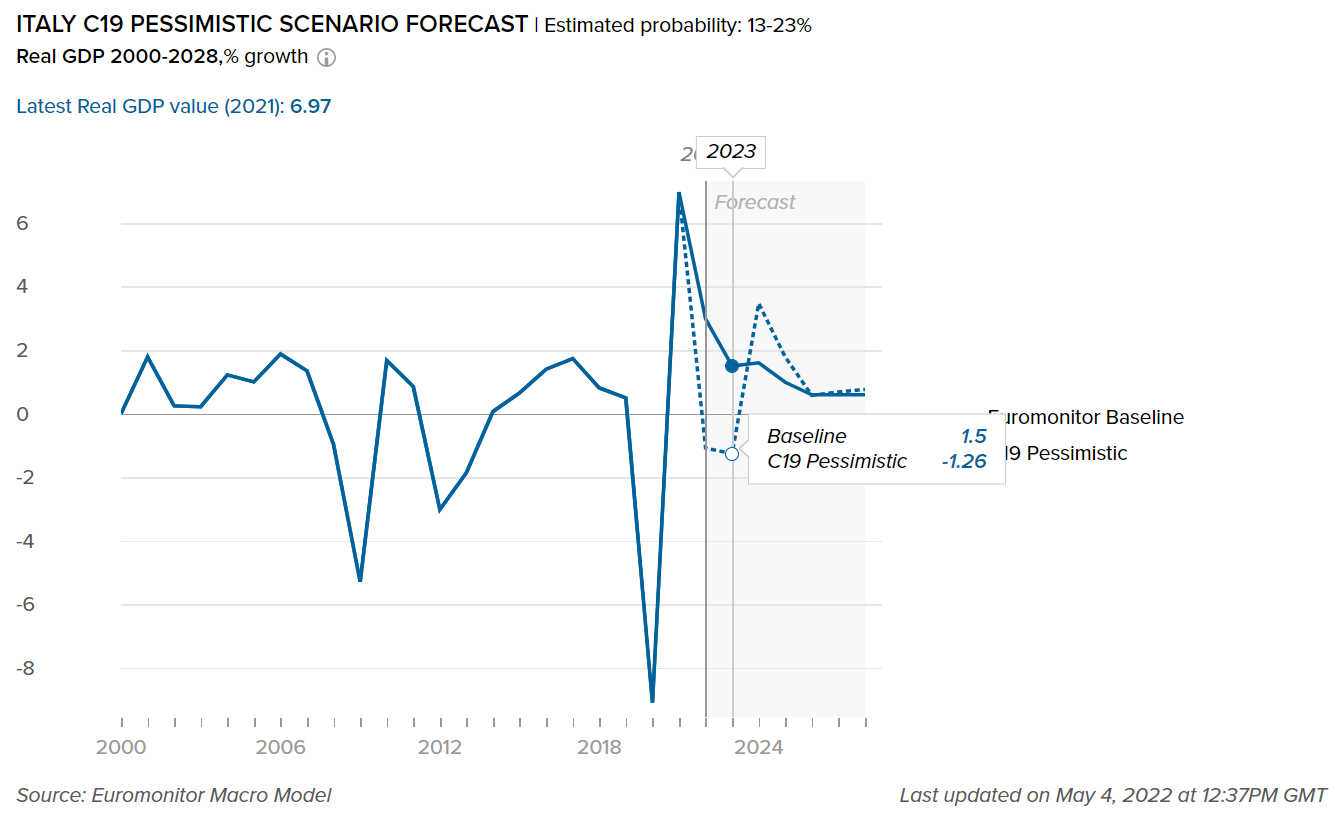

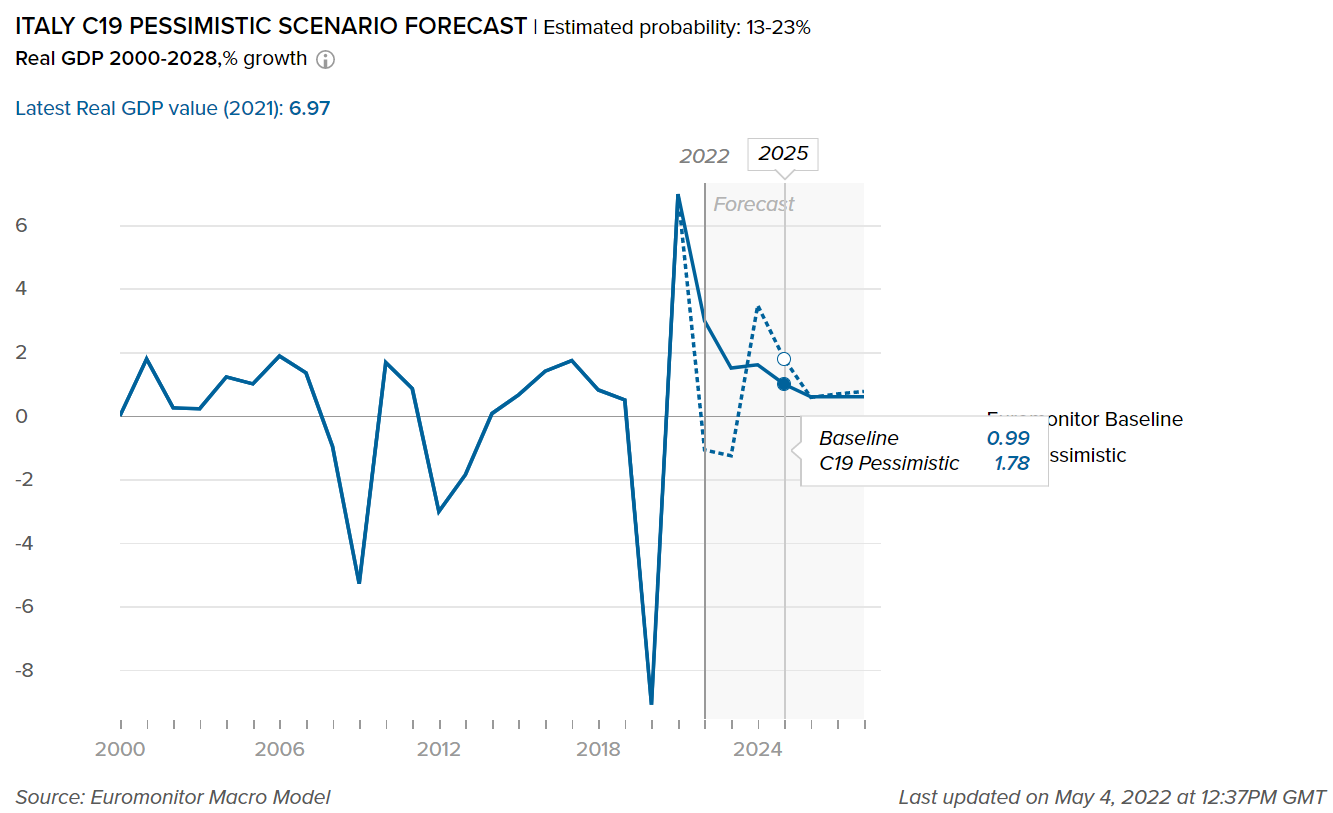

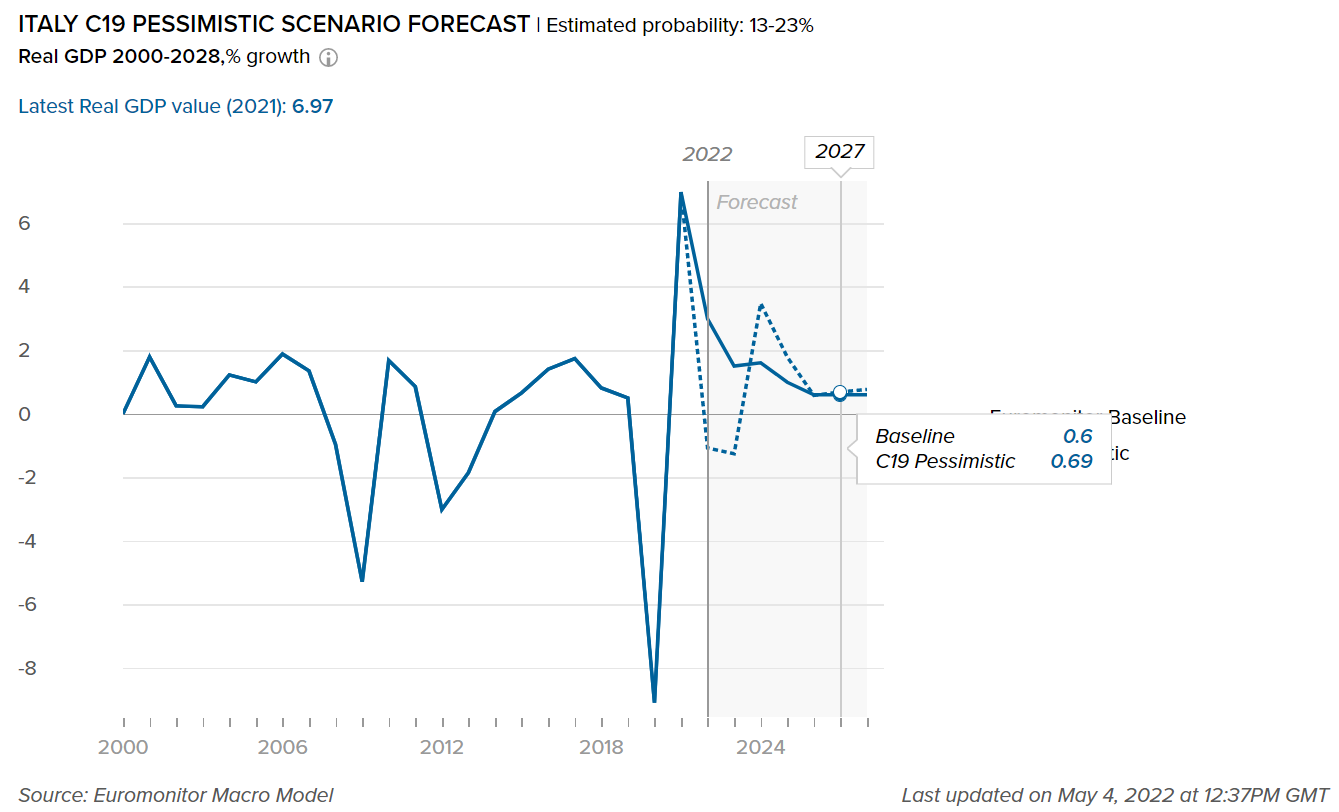

This graph shows our “most probable” and “worst-case” estimate scenarios of how COVID-19 will impact real GDP in Italy. Our “most probable” or Baseline scenario has an estimated probability of 45-60% over a one-year horizon. Our “worst case” or Pessimistic scenario has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the "best case" COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the "worst-case" COVID-19 scenario forecast that has an estimated probability of 13-23%.

Strong capital investment to support further economic recovery

- In 2021, Italy's real GDP expanded by 6.9% supported by improved domestic demand, attributable to pent-up private spending, increased public consumption, and gross fixed capital formation (GFCF). Despite the risks of new infection waves and rising inflation, private consumption is likely to continue to recover in 2022, with the labor market progressively recovering and pent-up demand continuing to be released.

- In value terms, healthcare and social services, utilities and recycling, and business services are expected to be some of the primary industries driving economic growth in Italy between 2021 and 2026. These industries' turnover is expected to expand by 12.3%, 14.0% and 8.6%, respectively, throughout the forecast period.

- Rising energy and commodity prices, as well as rising cost pressures due to persistent supply restrictions, drove inflation in Italy to 1.9% in 2021, up from deflation (negative inflation) of -0.1% the previous year. In 2021, the most significant price rises were seen in alcoholic drinks and tobacco products, food and non-alcoholic beverages, and hospitality services, among other important consumer goods and services.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

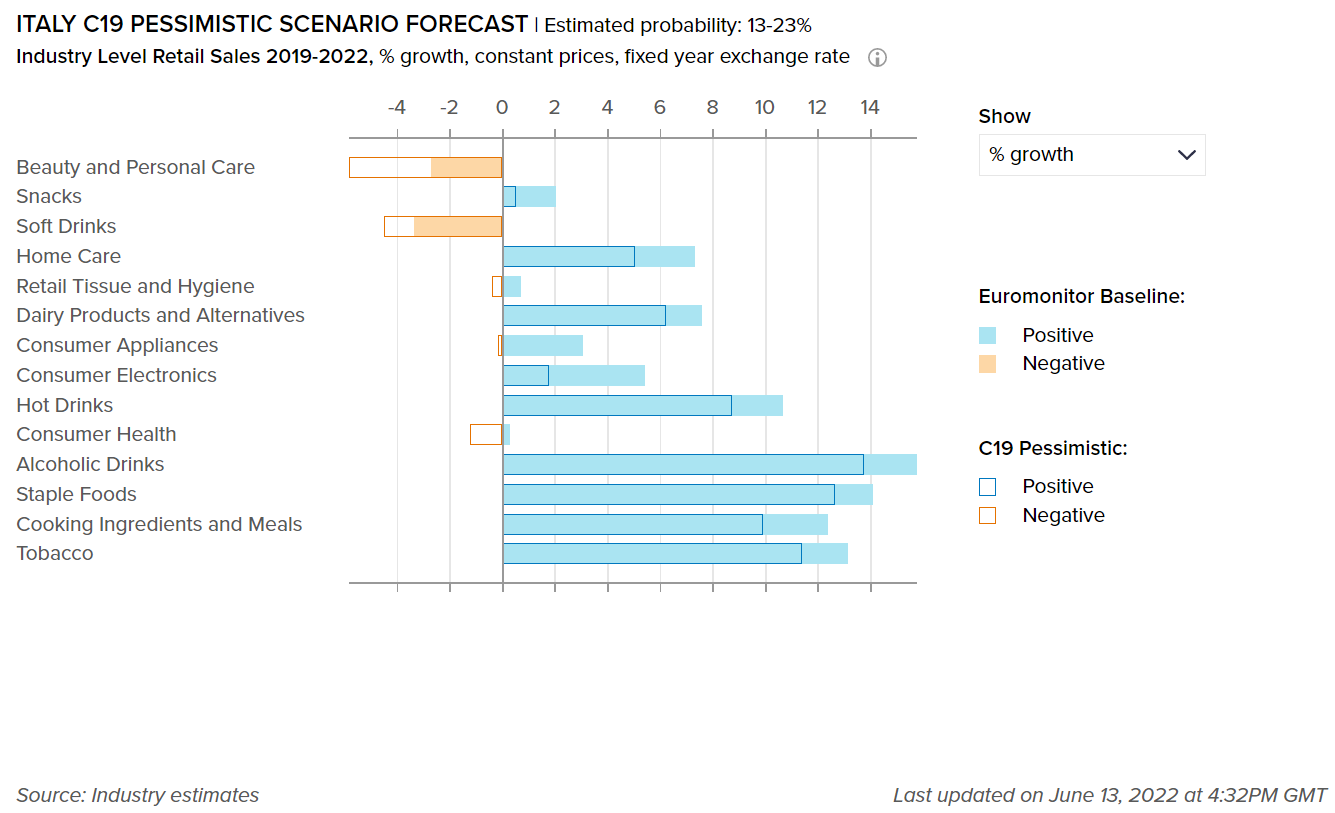

The graph below displays the adjusted forecasts of the percentage growth for the categories mentioned, highlighting the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast, which has an estimated probability of 45-60%.

Baseline forecast refers to the "best case" COVID-19 scenario forecast that has an estimated probability of 45-60%.

Alcoholic drinks endured the effect of the pandemic, supported by rising off-trade demand

- Closures of stores and foodservice outlets during the pandemic had two repercussions in terms of alcoholic beverages. First, general out-of-home consumption of alcoholic beverages decreased, while off-trade demand increased dramatically. Spirits, which are commonly consumed in on-trade settings, were the most negatively affected. However, off-trade demand for wine, cider, and, to a lesser extent beer, increased significantly in 2021, resulting in substantially faster off-trade growth than in prior years during the review period. According to Euromonitor’s Baseline scenario forecast, alcoholic drinks witnessed 12.6% growth over 2019-2022.

- Some categories fared better than others within alcoholic drinks, with wine, for example, experiencing the smallest reduction in volume, and RTDs experiencing the largest. Due to the general health and wellness trend, which surged in the aftermath of the pandemic, as consumers became concerned about the link between obesity and virus immunity and susceptibility, low-alcohol and non-alcoholic beverages grew in popularity.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst-case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors mentioned in Italy. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the "best case" COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the "worst-case" COVID-19 scenario forecast that has an estimated probability of 13-23%.

Diminishing concerns about the virus and return to normalcy drive a lower need for beauty and personal care products

- According to Euromonitor’s Baseline scenario forecast, the emergence of COVID-19 had a substantial influence on value sales of beauty and personal care in Italy over 2019 -2022, with a 2.6% value decline. Following the price decline in 2020, most distribution channels (particularly beauty specialist retailers) increased unit prices as players sought to make up for some losses, resulting in diminishing demand.

- Categories that had benefited from the COVID-19 outbreak in 2020, such as bath and shower, witnessed a downturn in 2021 as sales stabilized. This was attributed in part to a decrease in demand for hand sanitizers and liquid soap, with concerns over hand cleanliness easing significantly as a result of Italy's successful vaccination campaign and a decrease in cases. Similarly, 2021 also saw a decline in hair care, mainly due to the drop in demand for colorants, with consumers returning to hair salons to receive professional hair coloring and treatment services.

- Impact on Flexible Packaging

-

The following tables display adjusted market sizes for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per June 2022 data

2022 market size as per June 2022 data

% Difference between June 22 and February 22 data for 2022

Beauty and Personal Care Packaging

3,156

3,149

-1.1%

Home Care Packaging

2,622

2,629

2.3%

Packaging Type

2021 market size as per June 2022 data

2022 market size as per June 2022 data

% Difference between June 22 and February 22 data for 2022

Rigid Plastic

27,803

28,312

0.26%

Flexible Packaging

30,522

31,018

-0.14%

Metal

6,279

6,243

-0.01%

Paper-based Containers

7,884

7,909

-0.12%

Glass

8,324

8,475

0.03%

Liquid Cartons

3,607

3,662

0.00%

Sustainability is becoming ever more important in Italy’s packaging industry

- Concerns about the environment and sustainability are becoming more prevalent among all stakeholders. However, there are a number of obstacles to overcome in this field. Retailers, for example, continue to prioritize price as they believe that low costs are what customers desire, despite their growing environmental concerns. The cost of recycled PET is higher than that of new plastic, which is limiting the adoption of recycled plastic bottles in many industries. Furthermore, with just a few plastic bottle manufacturers equipped to produce PET bottles with handles, most bottles with handles are made of HDPE.

- Winni's Naturel from Madel is one of the green home care brands being launched in Italy that has been emphasizing how environmental sustainability practices are extended across all its life cycle operations, with the goal of being the leader in sustainable home care. Furthermore, Icefor, a dishwashing line with the Ecolabel mark on its packaging, uses green packaging that is lighter in weight to reduce greenhouse gas emissions during shipment.

- Within home care packaging too, Henkel invested in upgrading the packaging of its detergents to make it transparent and 100% recyclable, decreasing its carbon impact by 600 tonnes of plastics. Among other efforts to be both unique and appealing to environmentally-conscious consumers through packaging efforts; Henkel's new General Eco concept is a liquid detergent presented in 100% recycled PET (rPET) bottles.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recover Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is the best official measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.