Overview

- Packaging Overview

-

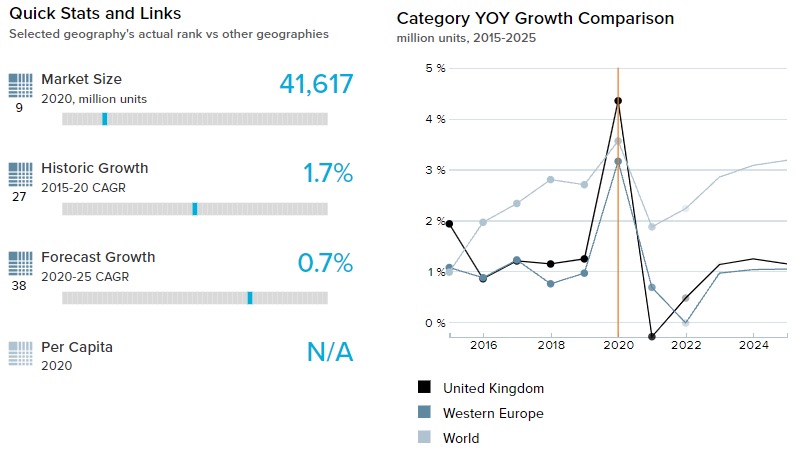

2020 Total Packaging Market Size (million units):

115,491

2015-20 Total Packaging Historic CAGR:

1.8%

2021-25 Total Packaging Forecast CAGR:

-0.7%

Packaging Industry

2020 Market Size (million units)

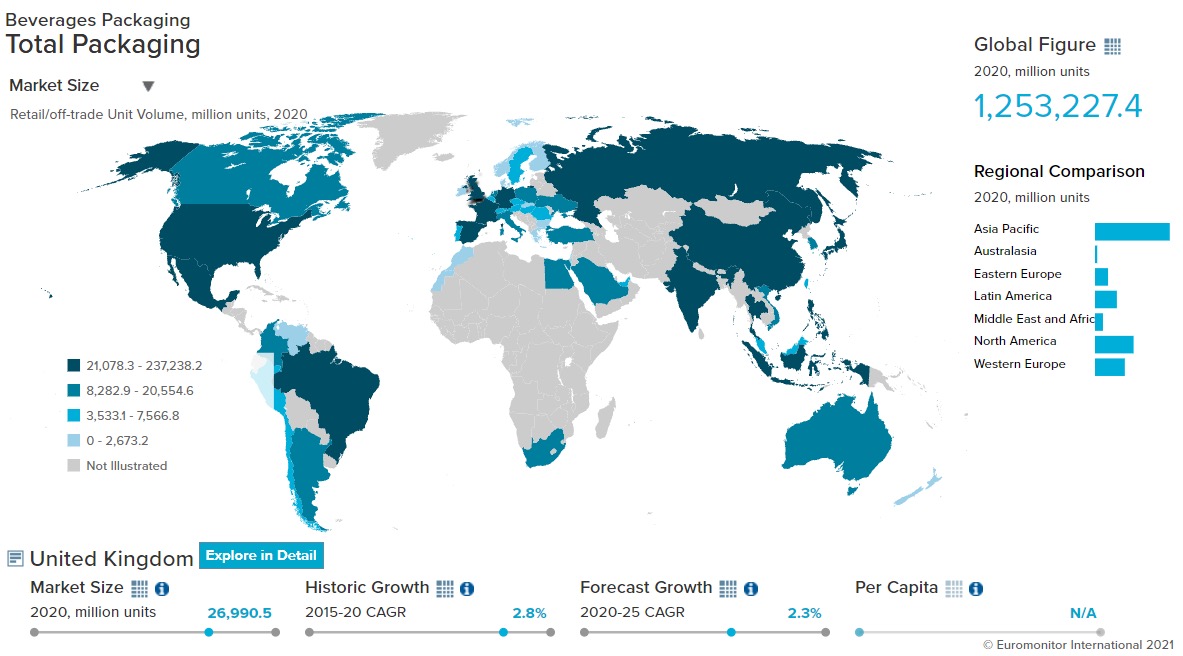

Beverages Packaging

27,061

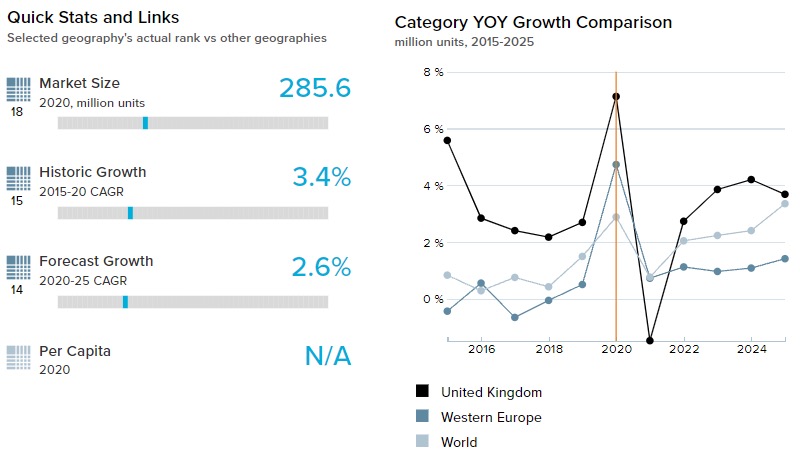

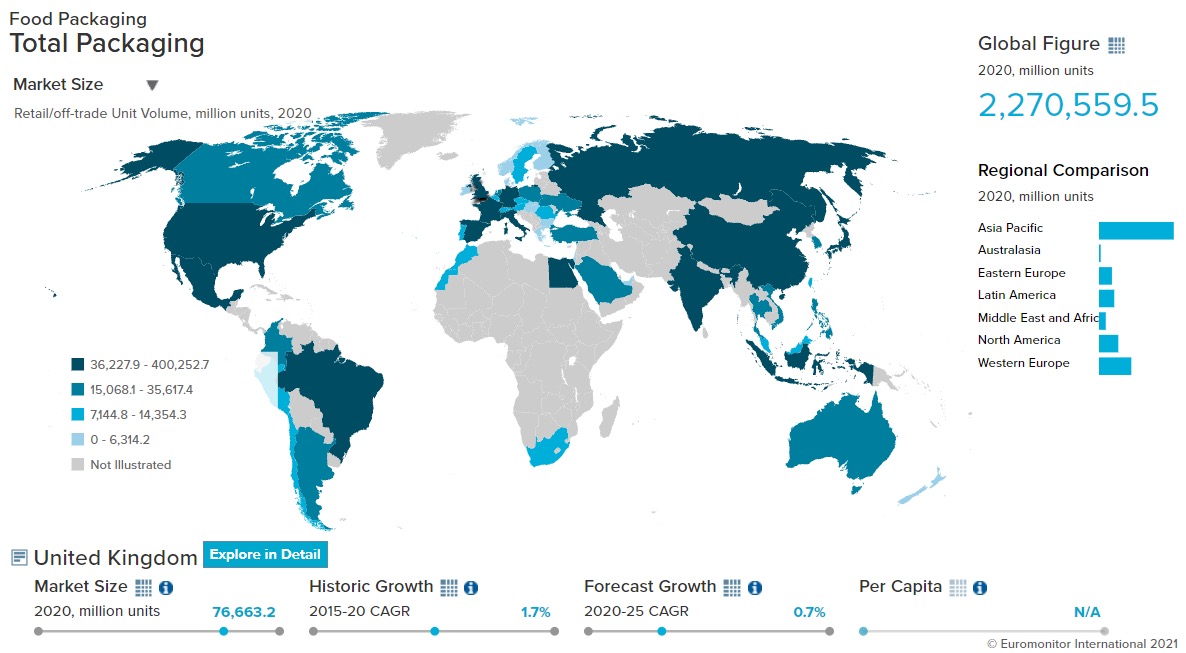

Food Packaging

76,663

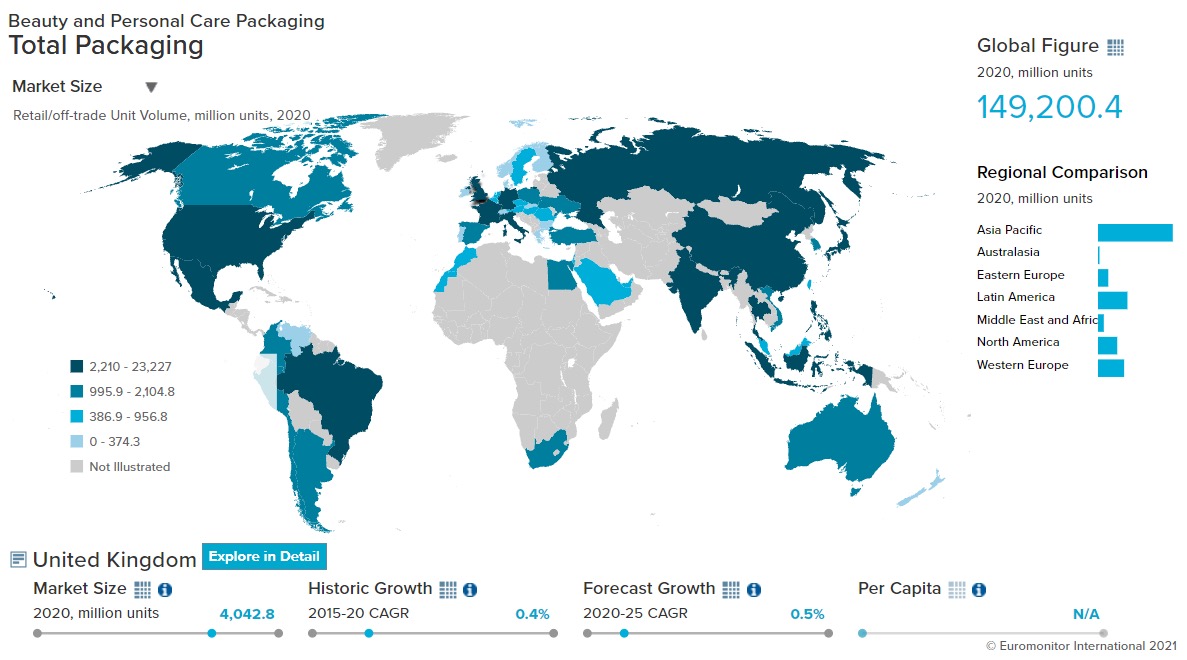

Beauty and Personal Care Packaging

4,043

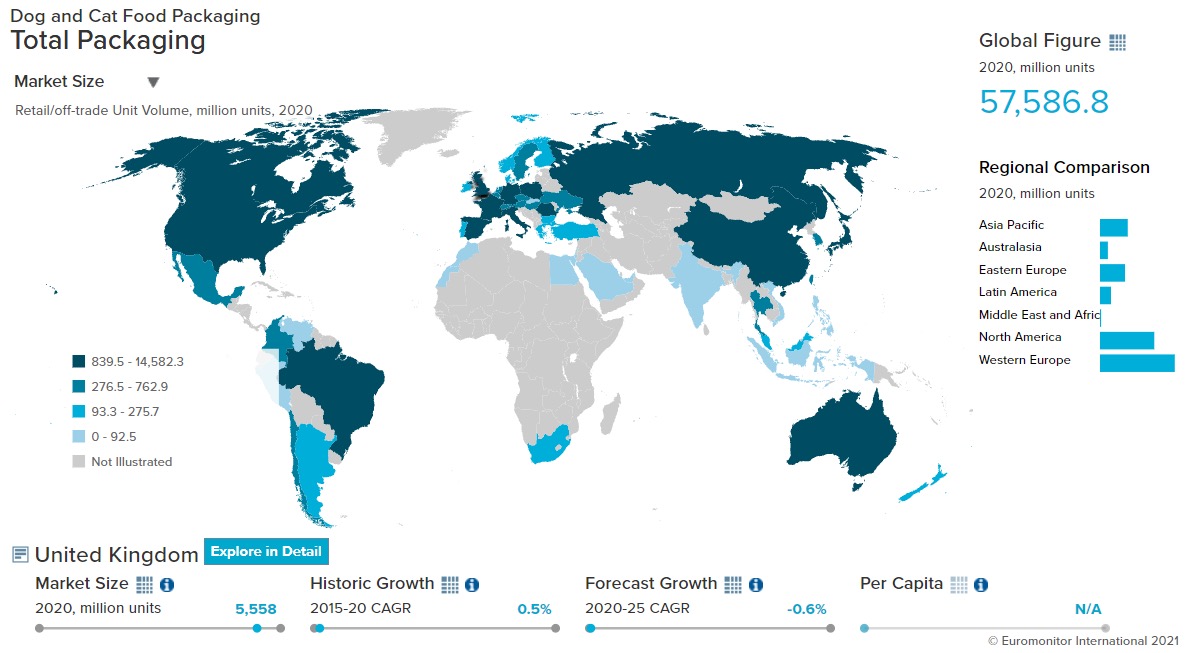

Dog and Cat Food Packaging

5,599

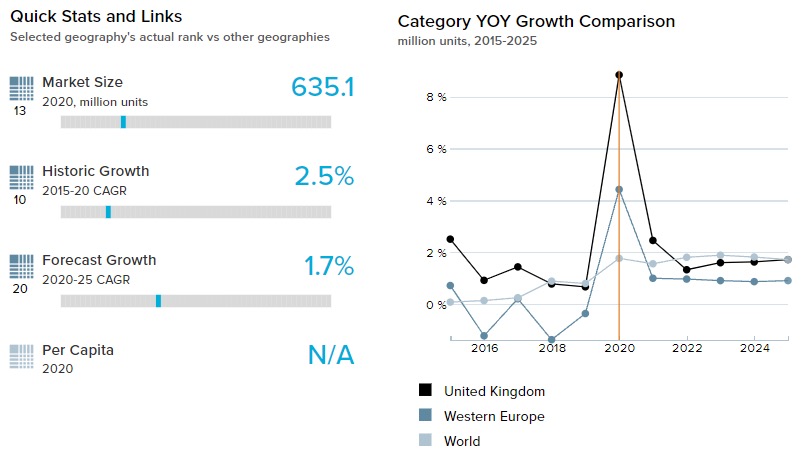

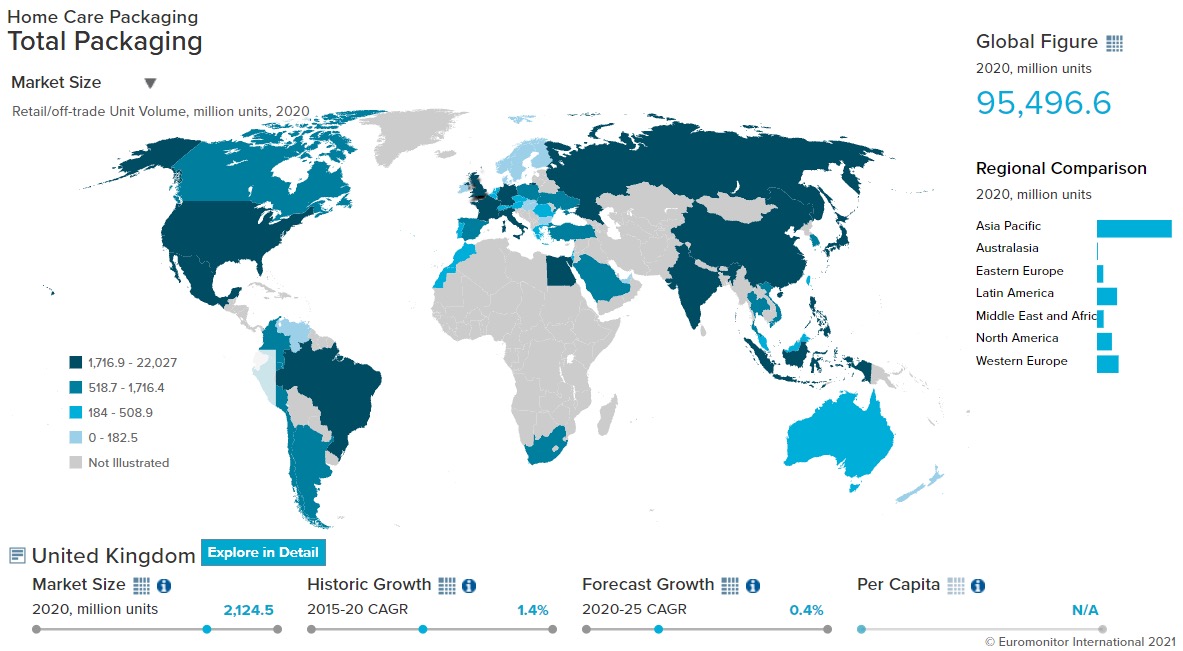

Home Care Packaging

2,125

Packaging Type

2020 Market Size (million units)

Rigid Plastic

32,694

Flexible Packaging

47,911

Metal

14,502

Paper-based Containers

9,573

Glass

8,024

Liquid Cartons

2,730

- Key Trends

-

The demand for convenience in terms of storage, transportability, usage, or disposal is shaping the packaging industry of the UK. Owing to the convenience in terms of usage, thin-walled plastic containers are preferred for dog and cat food while disposal convenience made the usage of single-use plastic in disposable hand sanitizers and plastic pouches in yogurt increase. Moreover, the popularity of e-commerce is also helping the sale of flexible plastic pack types such as flexible plastic and flexible aluminum/plastic in dog and cat food and home care products owing to the ease with which they can be transported and stored.

- Packaging Legislation

-

In May 2021, the government announced that the fee on plastic bags has been raised from 5p to 10p. The earlier charge of 5p applied to only those businesses that employed more than 250 people. But the recent directive is now applicable to all businesses in England. As per the Department for Environment, Food, and Rural Affairs (DEFRA), there has already been a 95% drop in plastic bag sales in England since 2015. By extending the fee to all retailers, it is hoped that the use of single-use carrier bags will decrease by 70-80% in small and medium-sized businesses.

- Recycling and the Environment

-

In November 2020, the UK’s Department for Environment, Food, and Rural Affairs (DEFRA) issued new waste recycling targets, in line with the EU directive. As per this, the recycling targets for plastic were reduced from 61% to 59% for 2021, and from 65% to 61% for 2022. Glass targets reduced from a proposed 84% to 81% in 2021 and from 87% to 82% in 2022 while paper recycling targets for 2021 and 2022 have risen by 4%. DEFRA also confirmed that since there is no longer a packaging waste recovery target as per EU directives, there is no general recovery obligation for 2021 and 2022.

- Packaging Design and Labelling

-

Packaging waste is a major concern in the UK as it makes up over two-thirds of its waste. Therefore, several companies are actively involved in research and development initiatives to reduce packaging waste. For example, Scotland-based Insignia Technologies is focusing on smart labeling to tackle waste. This smart labeling is trying to replace the traditional and inaccurate “best before” dates which encourage consumers to throw out food unnecessarily. The smart label will be attached directly to food products and use certain materials and ink which detects changes in temperature and carbon dioxide. These labels change color to let consumers know that the product is no longer fresh.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- Flexible packaging was one of the pack types that showed the largest growth of CAGR 5.1% or an increase of 36.8 million units in the retail off-trade unit volume of coffee over 2015-20. This increase can be attributed to the boost in sales of flexible aluminum/plastic and flexible plastic pack types, owing to their low price point and lightweight structure. These formats grew with a volume CAGR of 6.9% and 4.6% respectively over 2015-20.

- Trends

-

- The COVID-19 induced closures of on-trade food establishments had very little impact on alcoholic drinks sales due to the rise in home consumption in 2020. The supply also remained unaffected during the pandemic as grocery retailers, which dominate off-trade sales of alcoholic drinks, remained open even during the lockdown. Moreover, some consumers even shifted to e-commerce channels to purchase such beverages. This helped alcoholic drinks packaging show a volume growth of 11.7% in 2020 thanks to the growth of metal beverage cans, which witnessed an 11.1% increase in volume terms in 2020.

- Sustainable packaging initiatives and the use of recycled material for hot drinks packaging gained pace over 2015-20. Coffee players like Illycaffè partnered with TerraCycle, a global leader in recycling, to facilitate the collection and recycling of its plastic and aluminum coffee capsules. Their customers can opt for home collection of waste by registering on their website. The initiative helps to promote recycling of plastic with consumer participation.

- The demand for larger packs such as 1,000ml and above and multi-packs gained pace in 2020 as it helped the customers to stock soft drinks at home. For large pack sizes, PET bottles were preferred owing to the ease with which they can be stored and resealed. As a result, 1,000ml, 1,500ml and 2,000ml PET bottles showed a volume growth of 11.8%, 9.6%, and 8.6% respectively in 2020. In multi-packs, metal beverage cans were preferred owing to their strength and ability to be easily transported. This helped metal beverage cans record a volume growth of 4.6% in 2020.

- Outlook

-

- Metal beverage cans are expected to gain share from glass bottles in alcoholic drinks over 2021-25. Metal cans offer brand owners alarge surface area for brand communication and an opportunity for eye-catching designs. Metal cans are also expected to emerge in single-serve sparkling and white wine, as it will help brand owners to stand out from their competition. As a result, metal beverage cans are expected to show a volume CAGR of 6.3% over 2021-25.

- Implementation of a plastic packaging tax is expected to be in place by 2022, which is likely to shape the packaging trends of the soft drinks industry. Almost all the main soft drinks players pledged to incorporate recycled PET content across their product ranges. Leading players already invested in sustainable packaging, with brands like Highland and Coca-Cola launching 100% recyclable packaging in the bottled water segment.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- A greater number of pet owners opted to use e-commerce to buy pet foos. Plastic pouches, owing to their lightweight and convenience in storage and usage, is ideal packaging for this channel. As a result, plastic pouches were one of the fastest growing pack types in 2020, registering a volume growth of 11.6%.

- The UK government announced that it would introduce a new tax on produced or imported plastic packaging from 2022, with a thought that the law would negatively impact plastic packaging. While in the long run, this objective might be achieved, in the short run, consumers’ desire for convenience in terms of usage and storage outweighs the objective. As a result, flexible plastic and aluminum/plastic pouches, which recorded a combined volume share of 67.3% in dog and cat food in 2020, showed a volume growth of 5.5% and 2.5% respectively in the same year.

- Trends

-

- The COVID-19 induced extended periods of homestay deepened the bond between pets and their owners due to the lack of outdoor activities. This strengthened the pet humanization trend and helped smaller pack sizes that can be hand fed to their pets. For example, Mars introduced a range of cat treats called Sheba Creamy Snacks under its brand Sheba. These were packed in 12g sachets that could be consumed in one go. As a result, smaller pack sizes like 18g and 40g showed a volume growth of 7.0% and 7.9% respectively in dog and food products in 2020.

- Sustainability of packaging is one trend that remains strong in the United Kingdom. For example, the Crumbles family of dog treats were packaged in plastic-free, compostable, and recyclable paper bags. In May 2019, Nestlé Purina came up with its sustainability reports which stated that it had cut the use of 3,542 tons of packaging since 2015, with 67% of the packaging it uses is widely recyclable.

- Outlook

-

- The demand for premium dog foods is expected to increase over 2021-25 owing to the ongoing pet humanization trend. Pet owners expect that good quality food must be provided to their pets along with convenience of usage. As a result, thin-walled plastic containers, that can be easily opened, are expected to show a volume CAGR of 1.5% over 2021-25.

- In urban areas, smaller homes make it difficult to keep medium to large pets. The growing trend of urbanization for younger workers is expected to negatively impact pet ownership, along with COVID-19 induced economic uncertainty. As a result, dog and cat food packaging is expected to show a volume decline at a CAGR of -0.6% over 2021-25.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- The COVID-19 induced focus on hygiene products helped flexible packaging gain share in beauty and personal products. Flexible packaging, like plastic pouches, was the main pack type of hygiene-related products such as bath and shower products, which showed strong value growth of 26.2% in 2020. This helped flexible packaging increase its volume share from 14.5% in 2019 to 15.7% in 2020. This increase was supported by the increased sales of plastic pouches in liquid soaps, especially the 500ml pack as it helped stock liquid soap and comes in a refill package. As a result, plastic pouches recorded a strong volume growth of 26.8% in 2020.

- As people were confined to their homes due to lockdown restrictions and closure of workplaces, there was boredom and increased anxiety. Many preferred self-pampering as a method to de-stress. This included taking long baths and taking good care of their skin. Within bath and shower products, bath additives sales increased and increased the usage of its main pack type, flexible plastic. As a result, various flexible plastic pack sizes such as 250ml and 1,000ml showed a strong volume growth of 22.6% and 21.5% respectively in bath and shower products in 2020.

- Trends

-

- While hygiene-focused products saw an increase in demand, other categories like deodorants and sun care suffered, as they were perceived to be non-essential. Inbound and outbound tourism stopped, and people were reluctant to go to crowded places like parks and beaches due to the fear of contracting the COVID-19 virus. As a result, its main pack type, metal aerosol cans for deodorants and HDPE bottles for sun care2, showed a volume decline of 6.1% and 10.0% respectively in 2020.

- Due to the fear of contracting the virus, consumers paid more attention to hygiene and sanitation requirements. Not only did this trend benefit soap, but it also benefitted skincare products, especially hand care. Frequent hand washing and sanitization usually resulted in dry hands and hand creams were used to rehydrate them. This boosted the sales of one of its main pack types, squeezable plastic tubes, which showed a volume growth of 2.3% in 2020, owing to its ease of usability.

- Outlook

-

- Waterless beauty is a trend that is expected to be adopted by both consumers and manufacturers. Waterless products mean lighter weight which means more products can be shipped in one go, reducing carbon footprint. Also, it would mean that content could be packed in smaller pack sizes, reducing the packaging material required. For example, Avon launched the Avon Distillery range, comprising highly concentrated products presented in small packaging formats. As a result, smaller pack sizes such as 25ml and 50ml are expected to show a volume CAGR of 7.9% and 3.4% respectively over 2021-25.

- The sustainability of packaging and the use of recycled and refillable packaging is expected to become an important purchase factor for consumers and brands. Manufacturers have already taken steps for sustainability and are expected to invest more into achieving their targets. For example, Baylis & Harding introduced their new range under the Goodness brand, comprising sustainable products presented in 100% recycled plastic bottles and incentivizes consumers with reward points in exchange for used bottles. Avon has pledged to ensure that all of its packaging will become reusable, recyclable, or compostable by 2030 and has also set a goal that 100% of its carton packaging will be made from recycled materials or certified sustainable sources by 2025.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- The popularity of e-commerce channels increased as lockdown restrictions were imposed to curb the spread of COVID-19. This shifted packaging needs for both the consumers and manufacturers. Durability and lightweight became important factors as these ensured that the products could be delivered to the customers in perfect condition. This benefitted flexible packaging, especially flexible plastic which showed a volume growth of 11.3% in 2020, owing to its lightweight and suitability for transportation.

- Trends

-

- Prior to COVID-19, consumers were paying attention to the packaging material as they were concerned about plastic waste and its effect on the environment. But COVID-19 temporarily halted the progress towards a sustainable and circular supply chain as consumers were more concerned about hygiene and the safety of reusable packaging. Single-use plastics in the form of disposable sanitizers were widely used as they helped consumers maintain personal hygiene and were easy to discard. This helped flexible packaging and rigid plastic, which showed a volume growth of 7.1% and 6.3% respectively in 2020.

- Early on it was reported that the COVID-19 virus can be transferred by touching contaminated surfaces, so sanitization of homes, schools, and offices among others became the top priority. This trend boosted the sales of surface cleaners, especially surface sanitizers. Their main pack types are HDPE bottles and PET bottles, which recorded a volume share of 50.5% and 27.0% respectively in 2020, and showed a volume growth of 10.9% and 13.2% respectively in the same year.

- Outlook

-

- As vaccination rates are expected to rise, the fear of COVID-19 is likely to be reduced. This is likely to help bring back the sustainability trend which was hindered by the onset of COVID-19. Some players were working on sustainable packaging even during the pandemic. For example, Henkel, in association with Greiner Packaging, produced sustainable Pro Nature toilet cleaner bottles using 50% recycled material, to achieve their goal of reducing 50% fossil-based virgin plastics by 2025. Other organizations are also expected to follow this trend and are likely to revise their recyclability and plastic waste elimination targets.

- Brands are taking steps to promote the use of refills and reusable packaging to limit the plastic waste in the environment and people are expected to opt for more of these pack types. For example, Unilever, as a part of their #GetPlasticWise campaign, is testing the feasibility of refill bottles for liquid detergents for which they launched refill trials in the UK for its brands including Persil, Cif, and Simple. As a result, pack types such as squeezable plastic tubes and other plastic bottles which are suitable for one-time use are expected to show a volume decline at a CAGR of -2.3% and -6.4% respectively over 2021-25.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- A major consideration in buying processed meat and seafood is the shelf life of the product, as it is usually stored for some time and not consumed instantly. This is more prevalent for seafood as it is more susceptible to spoilage than meat. To tackle this problem, plastic pouches and flexible plastic became popular for processed seafood due to their ability to provide vacuum packaging. This type of packaging reduces the amount of oxygen present in the pack and thus, increases its shelf life. As a result, plastic pouches and flexible plastic showed volume CAGR of 10.0% and 2.3% respectively over 2015-20.

- With COVID-19 limiting the social life of consumers, they looked for new and different ways of treating and entertaining themselves. Comfort foods such as sweet treats were often used as a form of self-indulgence. This benefitted the main pack type for sugar confectionery, flexible plastic, which had a volume share of 49.5% in 2020 and showed a volume growth of 2.8% in the same year.

- Trends

-

- The use of plastic, be it flexible or rigid plastic, increased in prepared baby food products during the pandemic. This is because parents were afraid that the food might get contaminated with the virus. Therefore, they demanded those pack types which were more hygienic and safer against the dangers of the COVID-19 virus and ensured the preservation of food products. Even though plastic might be harmful to the environment, changes in consumer focus during the pandemic resulted in a growing preference for safe and secure plastic products. As a result, thin-walled plastic containers and aluminum/plastic pouches showed a volume growth of 26.3% and 11.9% respectively in prepared baby food in 2020.

- Health and wellness trends which were stimulated by the COVID-19 pandemic resulted in a boost in sales of healthy products such as yogurt in the dairy industry. Yogurt sales benefitted as consumers tried to incorporate these products into their daily nutritional intake to support their immunity. As a result, its main pack type, thin-walled plastic containers, recorded a volume share of 71.1% in 2020 and showed a volume growth of 2.5% in the same year. The most noticeable growth was in plastic pouches, which showed strong growth of 13.0% in 2020, owing to the ease of consumption and disposability provided by the pack type.

- Outlook

-

- In the UK, about 35% of children are overweight or obese by the time they leave primary school, which is a major concern for the government. Therefore, to tackle this, the government has revealed plans to test out a new program in 2021 that uses ready meals as a solution. This is expected to increase the demand for ready meal packaging over 2021-25. As a result, its main pack types such as flexible plastic, aluminum trays, and folding cartons are expected to be the main beneficiaries and are likely to record a volume CAGR of 2.5%, 1.7%, and 0.6% respectively over the same period.

- New product developments in baby food products are expected over 2021-25 in response to the increasingly busy lifestyles of consumers. Following this trend, Danone, in March 2021, announced the launch of the first-ever milk formula product in the UK to be sold in a pre-measured tab format. This tab format will make the product more convenient and easier to use for busy parents, will create less mess while feeding, and help accurately measure the formula. A folding carton will be used as an outer box, which is already fully recyclable in the UK and therefore driving the sustainability trend. Other players are also expected to follow suit and the use of folding cartons in milk formula is expected to increase, thereby likely to show a volume CAGR of 10.6% over 2021-25.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in United Kingdom

-

The UK lifts all travel-related COVID-19 restrictions

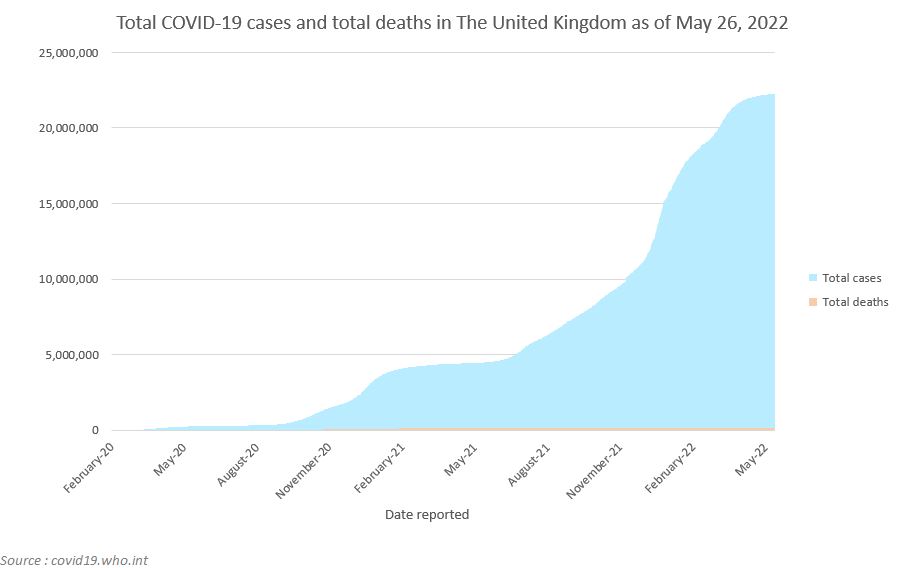

- According to the World Health Organization (WHO), the UK had 22,271,126 COVID-19 cases, 178,221 deaths, and 332,278 cases per million inhabitants as of May 2022.

- In April 2022, as the UK continued to lift all COVID-19-related bans, the country was faced with a renewed surge in COVID-19 hospitalizations due to the new Omicron subvariant detected. Nonetheless, the country further loosened restrictions; lifting all requirements for international travelers and announcing that as of late March 2022, people arriving in the UK will no longer need to take a COVID-19 test, even if they have not been vaccinated.

- According to the WHO, on May 15, 2022, the UK’s total vaccinations reached 142,796,436. The total number of fully vaccinated people per 100 reached 73.2.

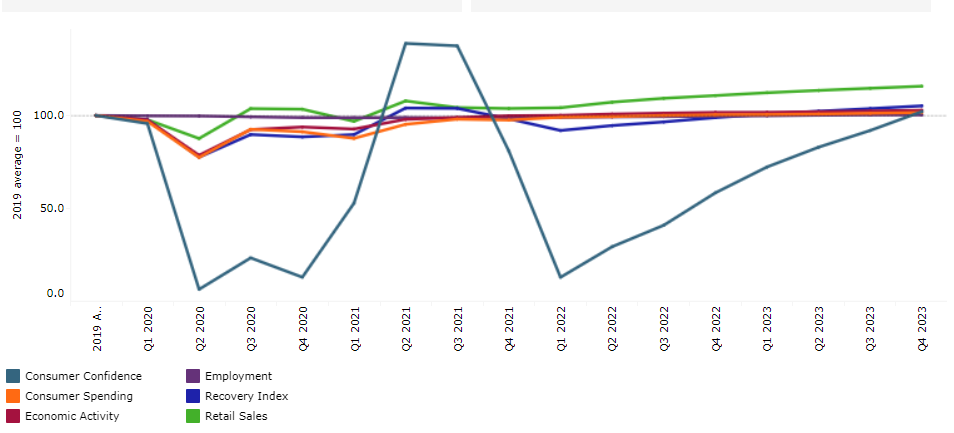

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, United Kingdom

- Impact on GDP

-

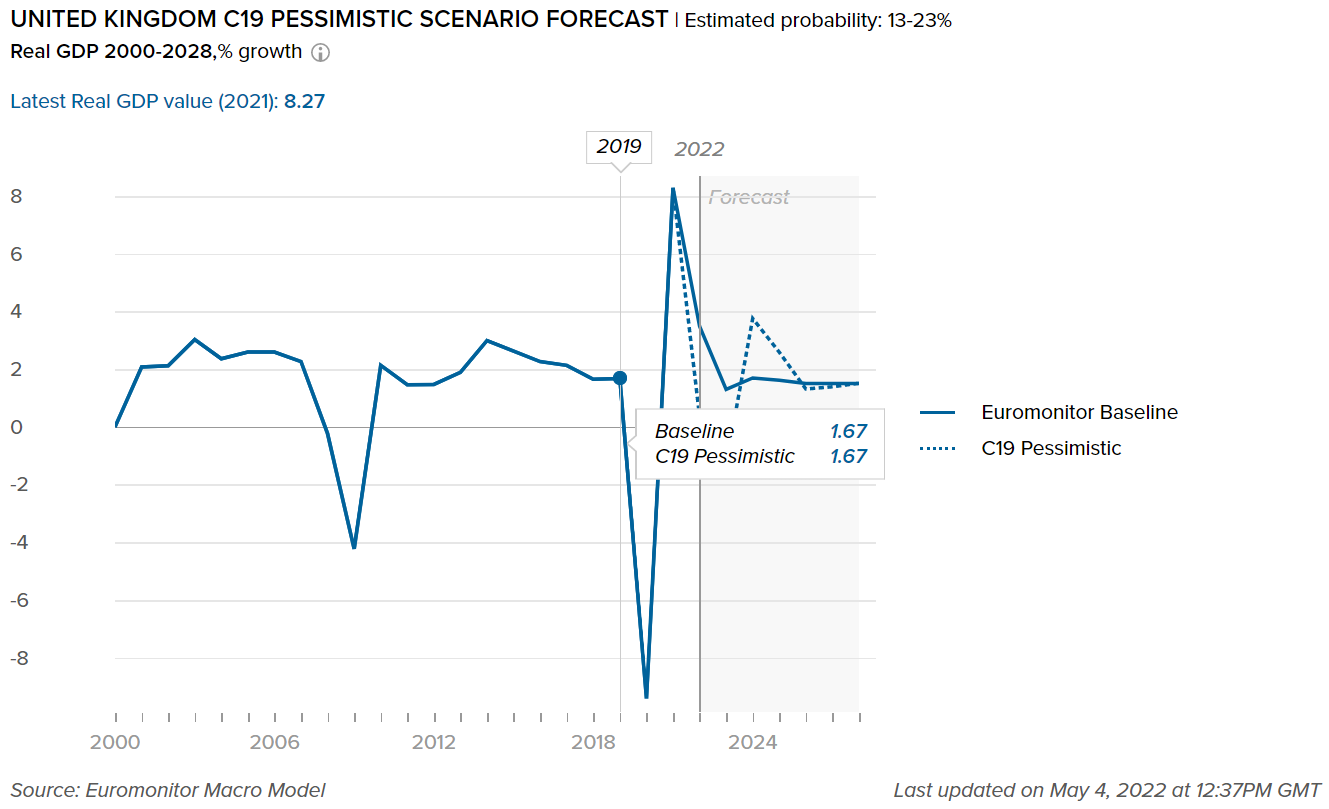

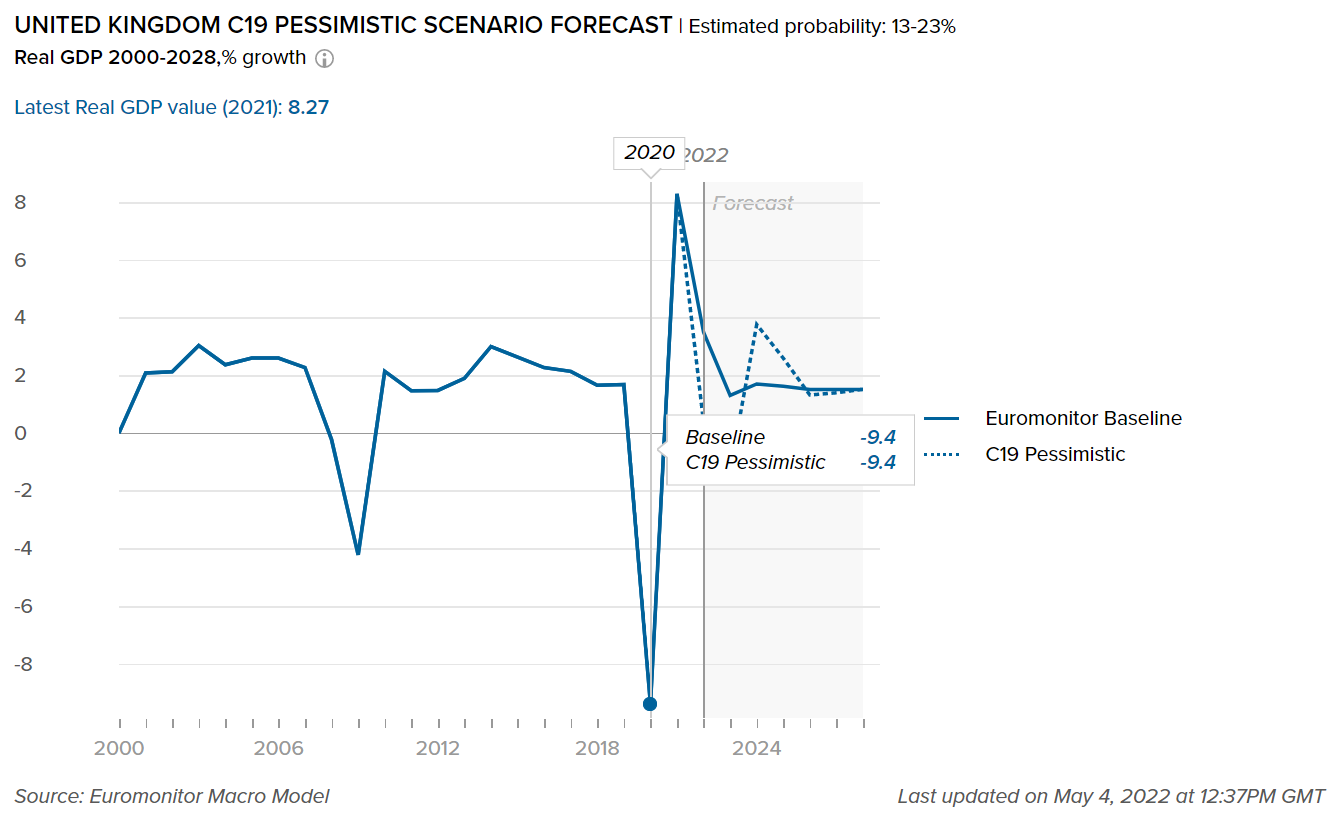

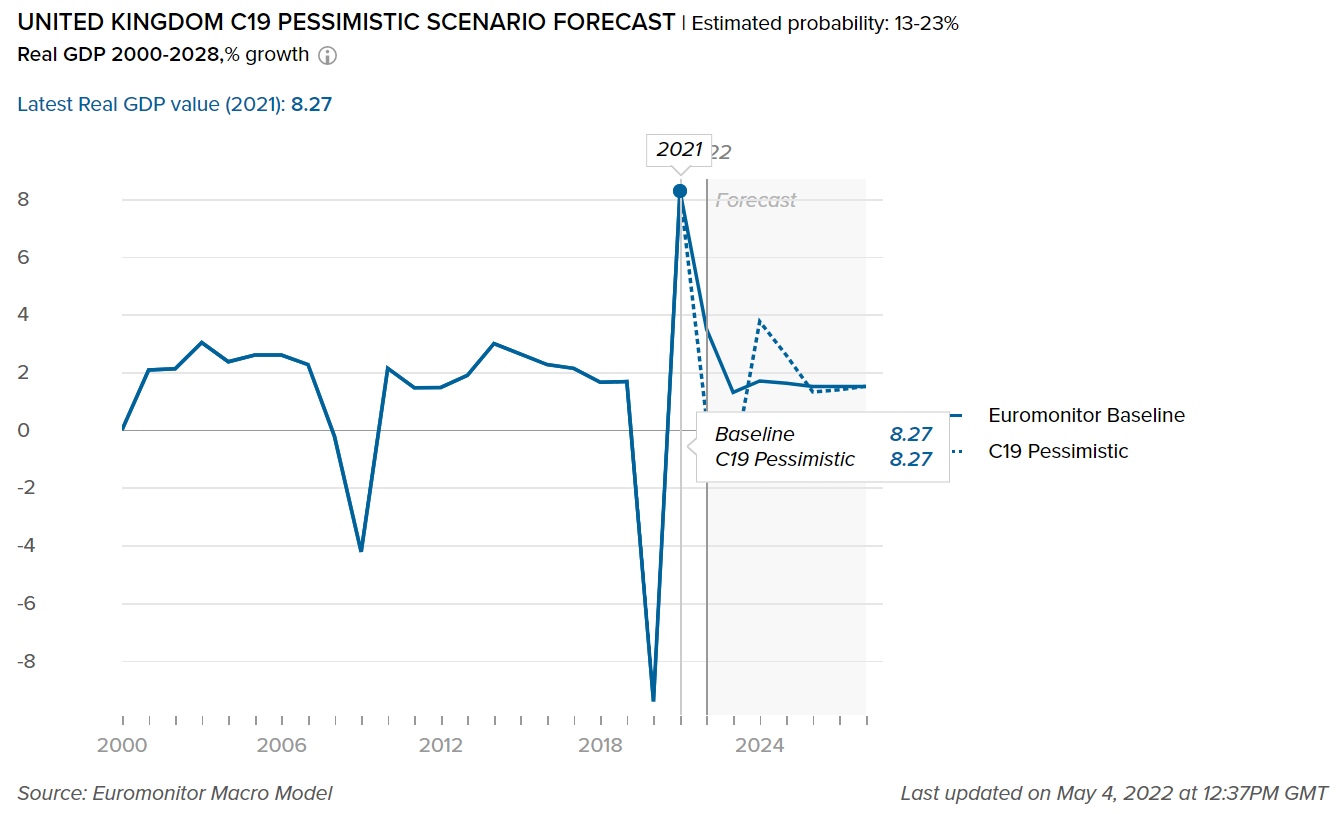

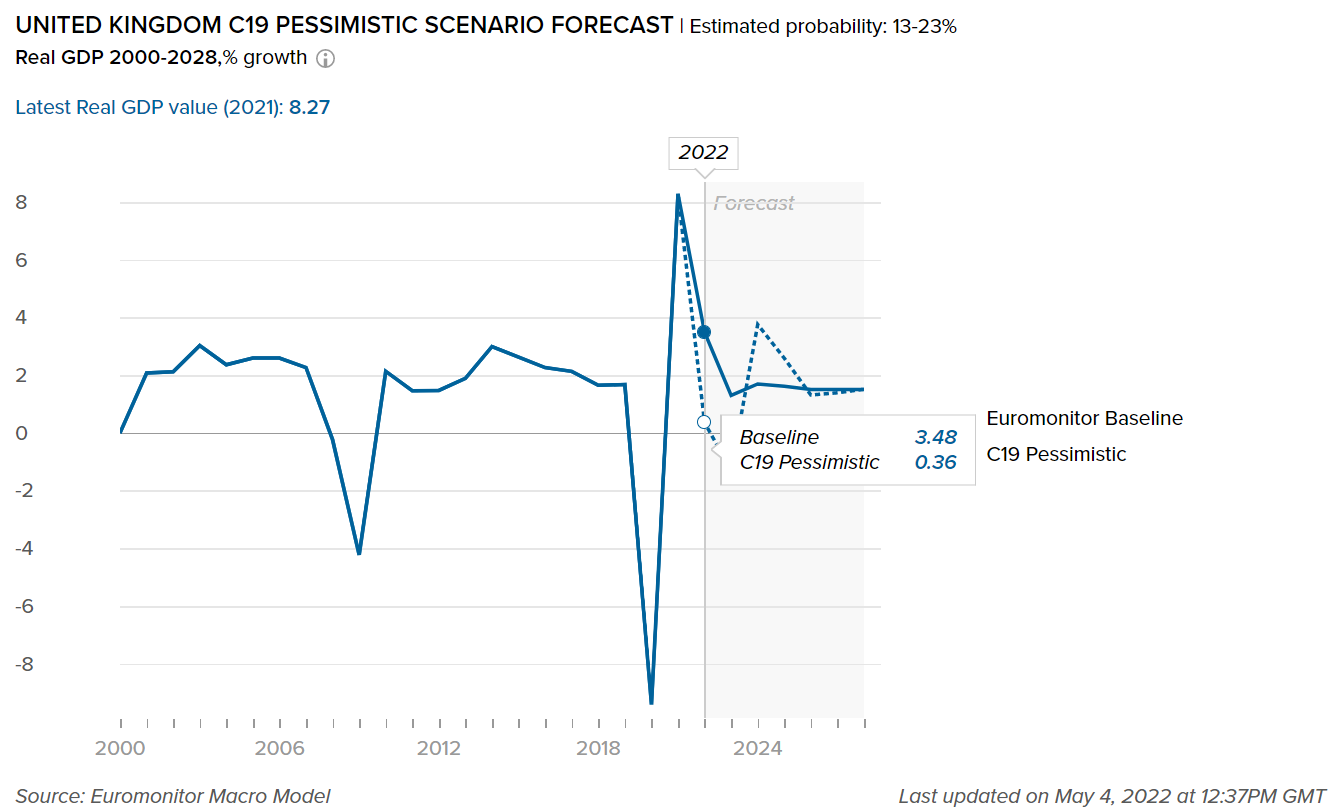

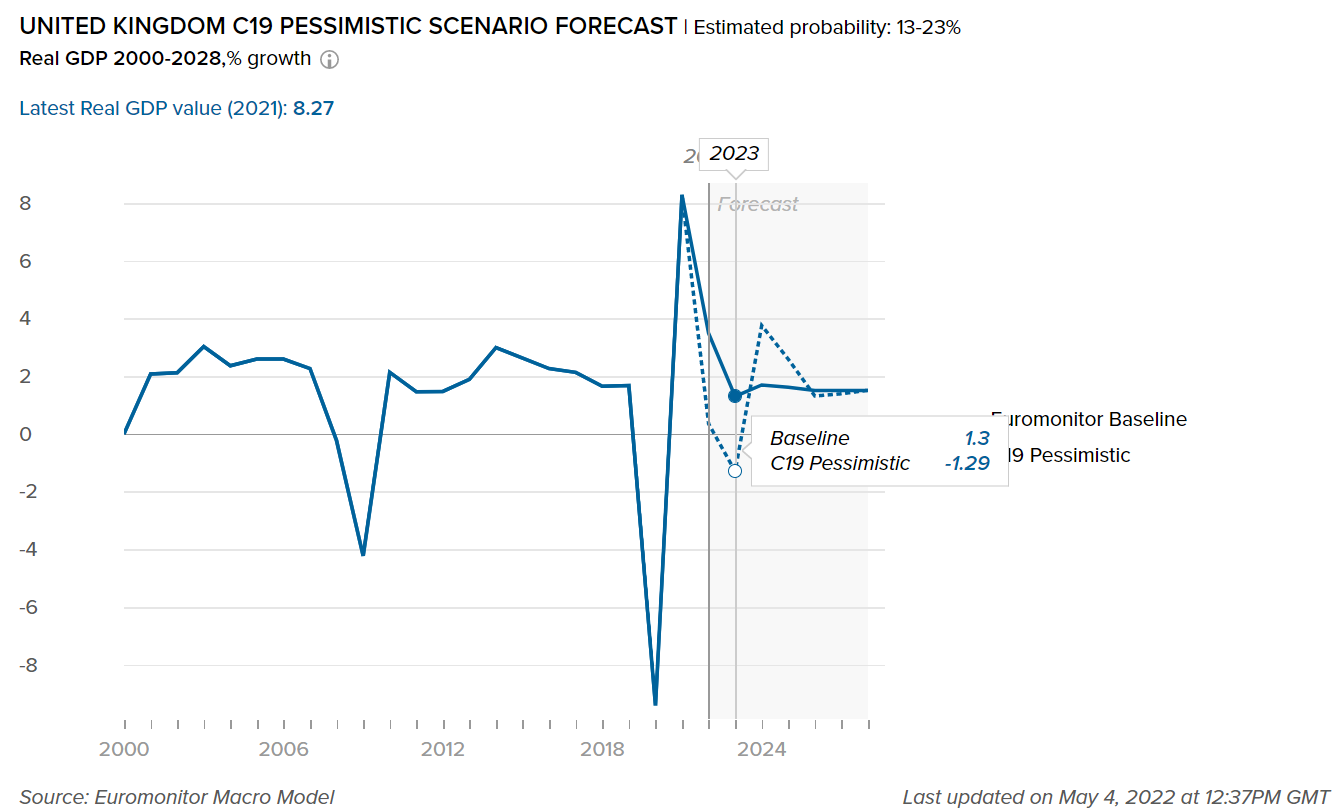

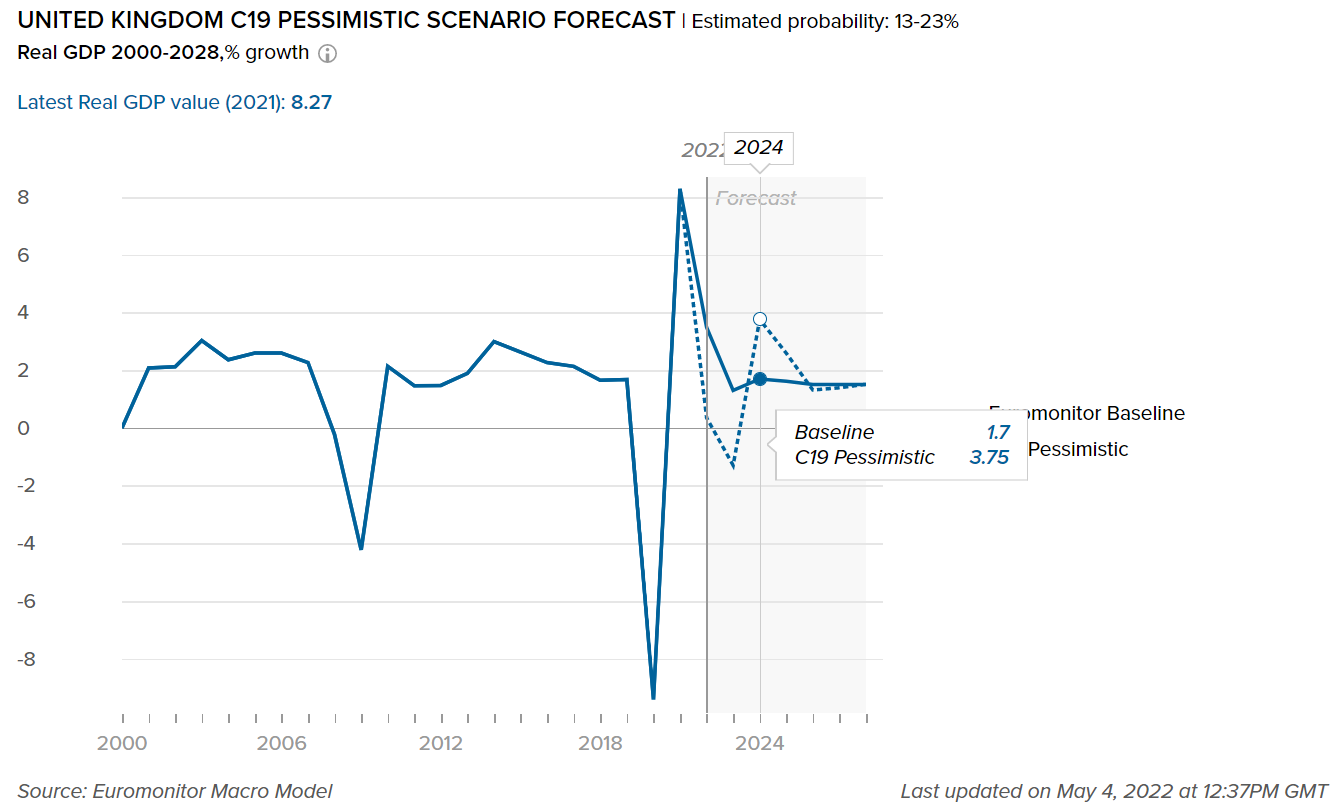

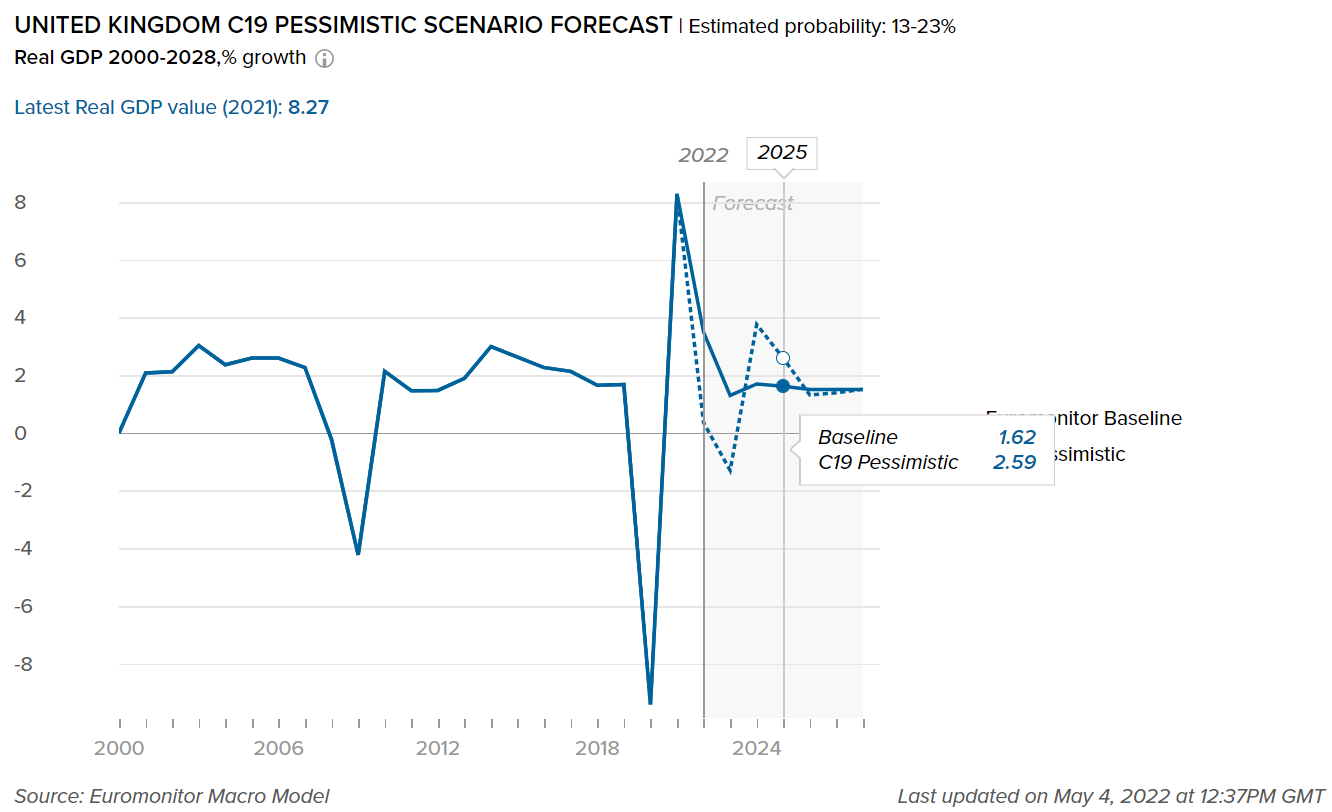

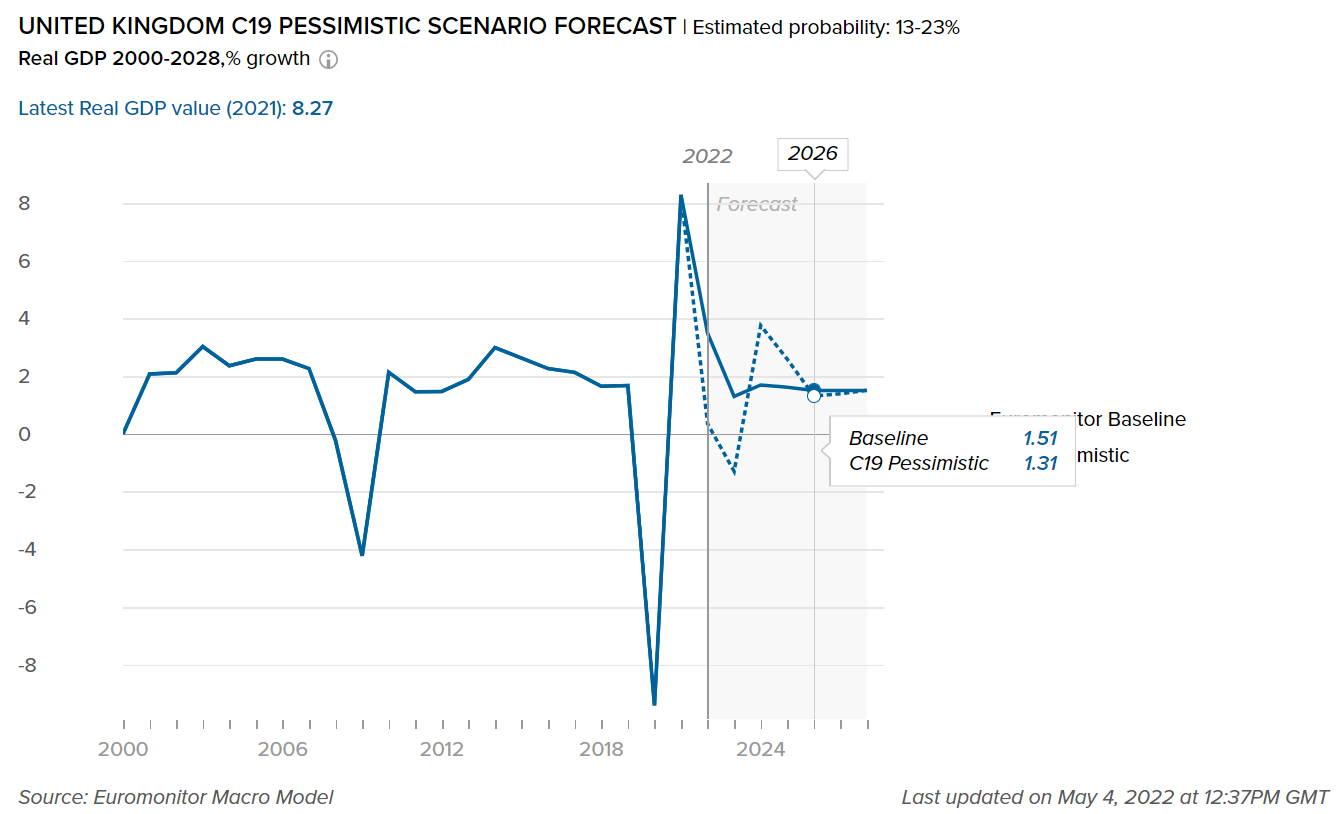

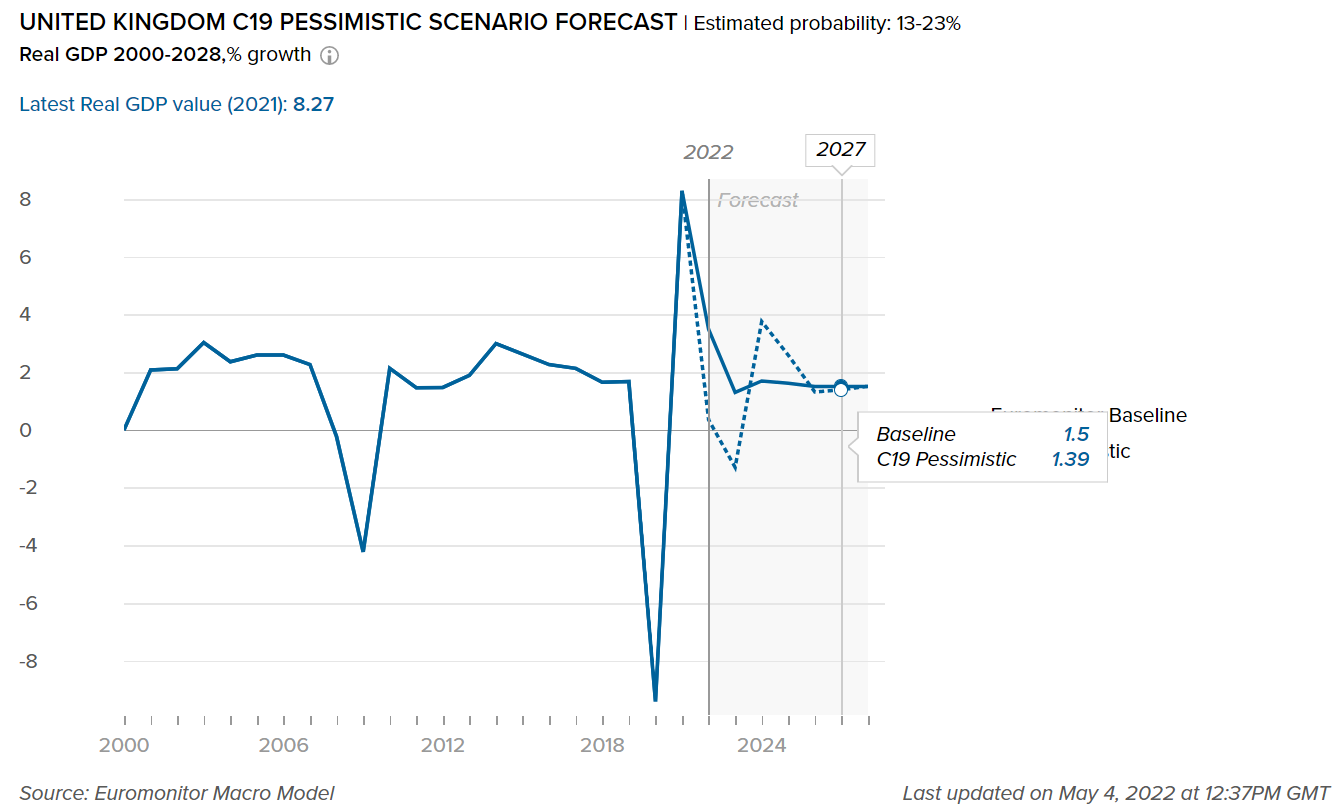

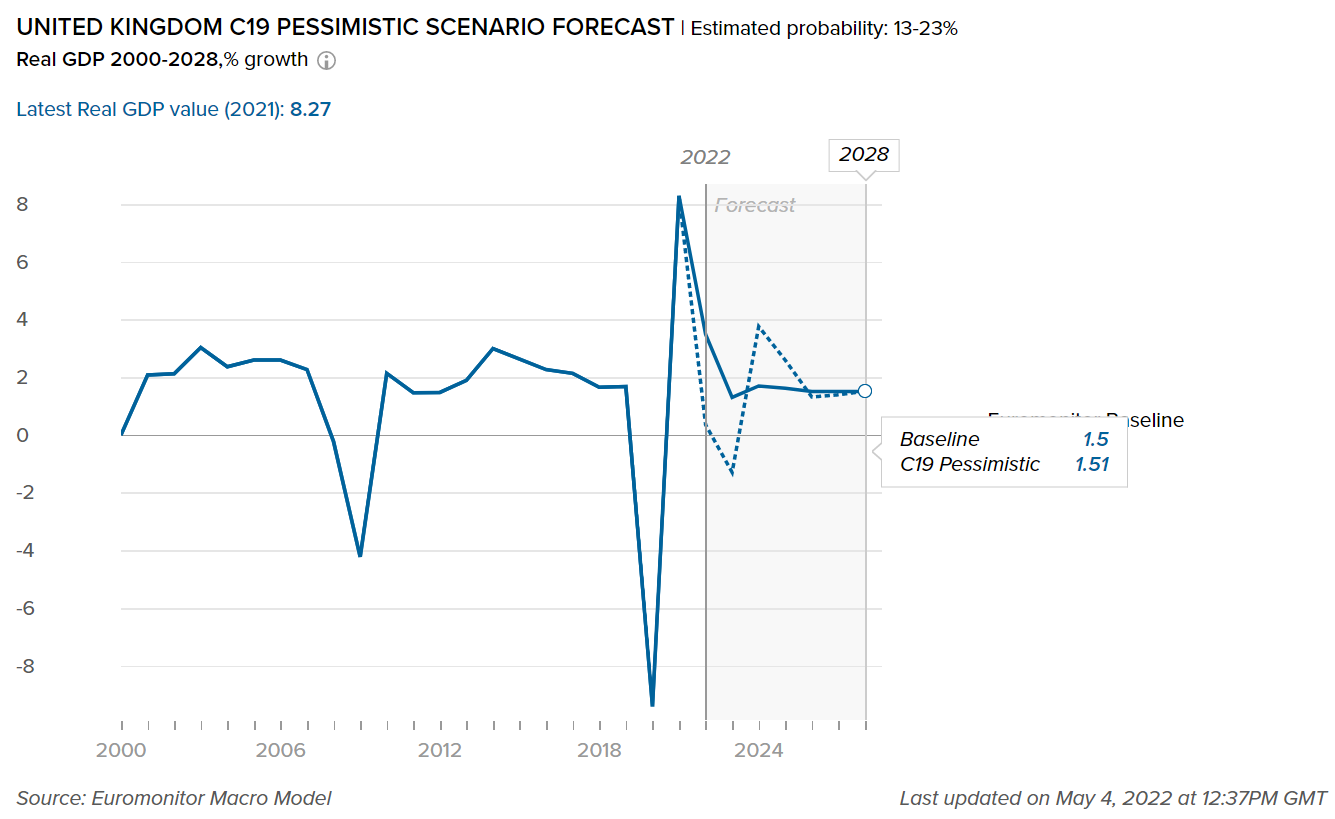

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in the United Kingdom. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the Scenario Definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Following one of the worst contractions in Western Europe, the UK economy bounced back in 2021

- Following a steep contraction of 9.4% in 2020 as a result of the COVID-19 pandemic shock, real GDP in the UK increased by 8.2 % in 2021, mainly due to improved private and public spending. In 2021, the UK's GDP per capita was USD46,638 compared to an average of USD40,083 in Western Europe. Although the UK economy is anticipated to recover to pre-pandemic levels in real terms by 2022, the persisting labor shortages, supply bottlenecks, and faster-than-expected monetary tightening continue to cloud the near-term economic outlook.

- In 2022, the UK unemployment rate is predicted to be 4.5%, higher than pre-pandemic levels, but lower than the Western Europe average of 7.8%. The ending of the furlough program on September 30, 2021, did not affect unemployment. However, the UK’s labor market has been showing signs of tightening, as sharply rising numbers of vacancies and gradually declining unemployment have been pointing to difficulties in filling vacancies.

- Even though the EU-UK Trade and Cooperation Agreement preserved tariff-free trade between the two parties, the UK's exit from the European single market resulted in higher non-tariff barriers to goods and services mobility between the UK and EU member states. New border procedures, such as safety inspections and customs declarations, made trade with EU members less flexible and more expensive, and are projected to cause shipment delays for some time.

- On the other hand, the UK applied to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and began discussions on a new free trade agreement with India in January 2022, having already secured agreements with Japan, Canada, and Australia, among other countries.

- Impact to Sector Growth

-

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below displays the adjusted forecasts of the percentage growth for the categories mentioned to highlight the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

Packaged food products continue their growth on the back of safety and convenience

- Although the lockdown limitations were lifted in the second quarter of 2021, some of the habits that people were forced to adopt during the pandemic were kept to some extent. Working from home was still used as part of a hybrid working approach, which appears to be popular with both employees and employers. This, combined with increased home isolation during the lockdown period, kept demand for cooking ingredients and ready meals strong, as consumers sought convenience, as well as health credentials in the foods they consumed.

- Organic packaged food in the UK is showing high growth potential within the packaged food category. With the pandemic highlighting the need for well-established supply chains in producing high-quality end-products, more consumers are opting for organic options, which are considered safer. Food safety is a major factor in why people seek organic products, but it is not the only one. Organic products are sought after, according to Euromonitor International's Voice of the Consumer: Health and Nutrition Survey 2021, because they are considered "better for you," and at the same time address environmental issues. In this sense, the expansion of organic packaged food is mostly driven by overarching trends toward health, nutrition, and sustainability.

- New items were introduced to the market in response to this need. Edible Oils Limited, manufacturer of Flora and Mazola oils, presented the U:Me brand, including an organic rapeseed oil for roasting and frying. With more meals prepared at home, customers have become more aware of the products they use, and they are keen to learn more about some of their favorite items.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors mentioned in the UK. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Despite the recovery of some segments, the beauty and personal care industry is still posting value declines

- Overall, beauty and personal care had a better year in 2021 than it did in 2020, though it still has yet to fully recover from the pandemic's effects. According to Euromonitor’s Baseline scenario forecast, beauty and personal care products declined by 5.9% over 2019-2022. However, demand for hand sanitizers remained high in 2021, especially at the start of the year, which the UK spent in lockdown, as concerns lingered over the COVID-19 pandemic and as regular hand washing is known to be an effective way to combat the spread of germs. Nonetheless, the demand for these products decreased compared to the previous year as the vaccine rollout gathered traction and many consumers may have had surplus products left from 2020. On the other hand, sales of depilatories also continued to decline in 2021 as a result of rising preference among UK consumers for longer-term solutions to hair removal, such as laser treatment.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

3,994

4,011

0.1

Home Care Packaging

2,116

2,112

-2.8

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

33,095

33,083

-0.37

Flexible Packaging

47,849

47,255

0.00

Metal

14,082

14,115

0.20

Paper-based Containers

9,699

9,618

0.04

Glass

8,095

8,131

0.44

Liquid Cartons

2,792

2,782

0.00

The UK introduces its Plastic Packaging Tax on April 2022

- To push sustainability efforts, the UK government implemented the Plastic Packaging Tax (PPT) on April 1, 2022. The tax's purpose is to encourage the use of recycled plastic in plastic packaging rather than virgin plastic. This will make it easier to collect and recycle plastic packaging waste in the UK. Any plastic packaging item that contains less than 30% recycled plastic and is made in the UK, imported into the UK, or imported into the country as a filled product, will be subject to tax, with HMRC charging GBP200 per ton. Non-plastic packaging such as folding cartons, glass bottles, and metal aerosol cans are anticipated to benefit from the new regulations.

- In 2022, there will likely be a growing number of items in home care that integrate recycled plastics in packaging, or refillable business models in closed-loop systems, as sustainability continues to impact new product development and strategies. Persil, for example, introduced 100% recyclable bottles. The bottles are now produced with 50% post-consumer recycled plastic, are 100% recyclable, and the dosing ball that was previously included with each bottle has been removed, reducing the quantity of virgin plastic in Persil bottles by over 1,000 tonnes yearly.

- As part of its #GetPlasticWise campaign, Unilever is evaluating the possibility of refill bottles for liquid detergents. The company launched refill trials in the UK for its brands Persil, Cif, and Simple. Unilever is experimenting with two refill models: touch-free refill machines that dispense Persil laundry liquid in reusable aluminum or stainless-steel bottles, and in-home refills, with Cif Ecorefills which offer an in-home refill experience to customers, using 10x concentrated refill for sprays allowing customers to use a Cif spray bottle for life. Ecorefills also use 75% less plastic than traditional cleaning bottles.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies.

The spread of a more infectious and highly vaccine resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe disease from new coronavirus variants, with moderate vaccine modifications.

Vaccination campaigns progress in developing economies is slower than expected.

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and released pent-up demand.

Longer lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment and wages relative to the baseline forecast in 2022-2023.

- Recovery Index

-

Recover Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is officially the best measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.