Overview

- Packaging Overview

-

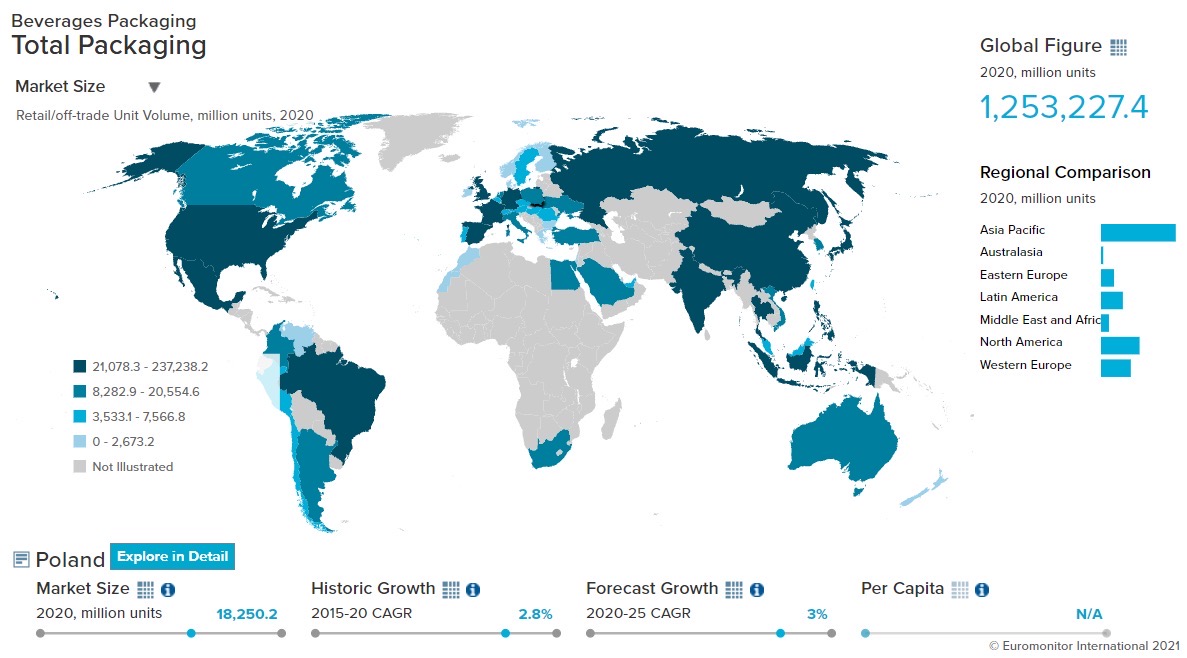

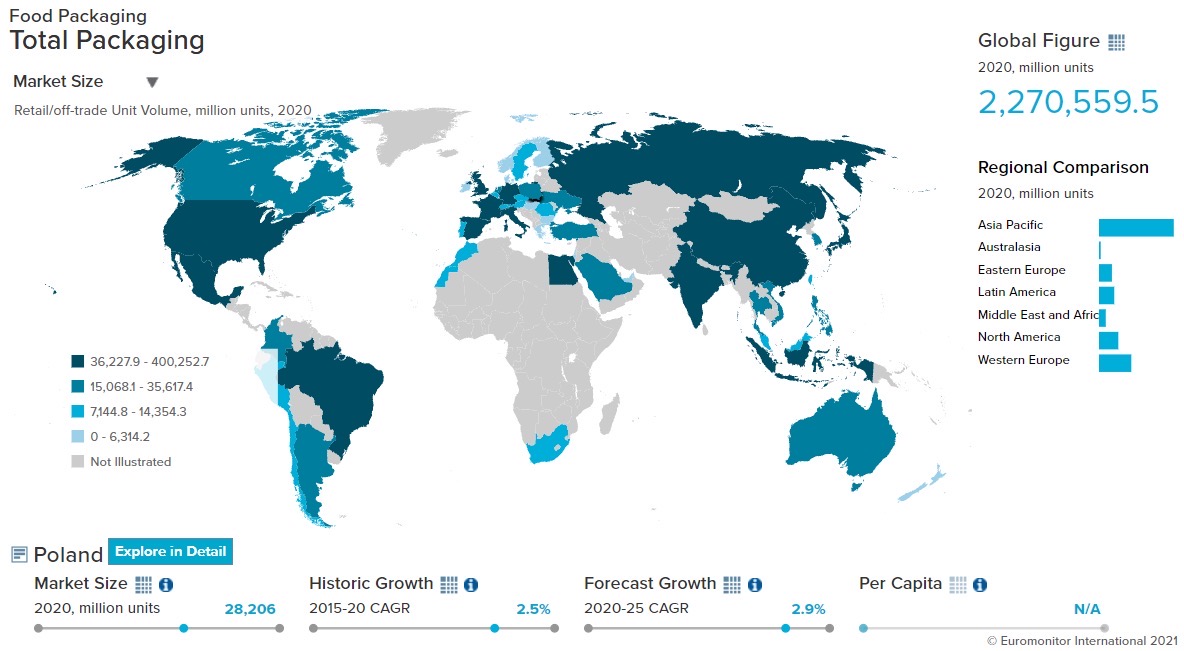

2020 Total Packaging Market Size (million units):

50,325

2015-20 Total Packaging Historic CAGR:

2.8%

2021-25 Total Packaging Forecast CAGR:

-0.2%

Packaging Industry

2020 Market Size (million units)

Beverages Packaging

18,114

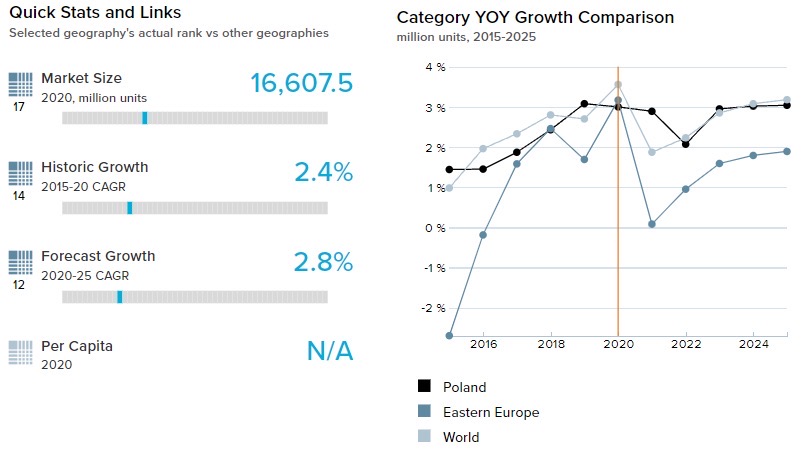

Food Packaging

28,206

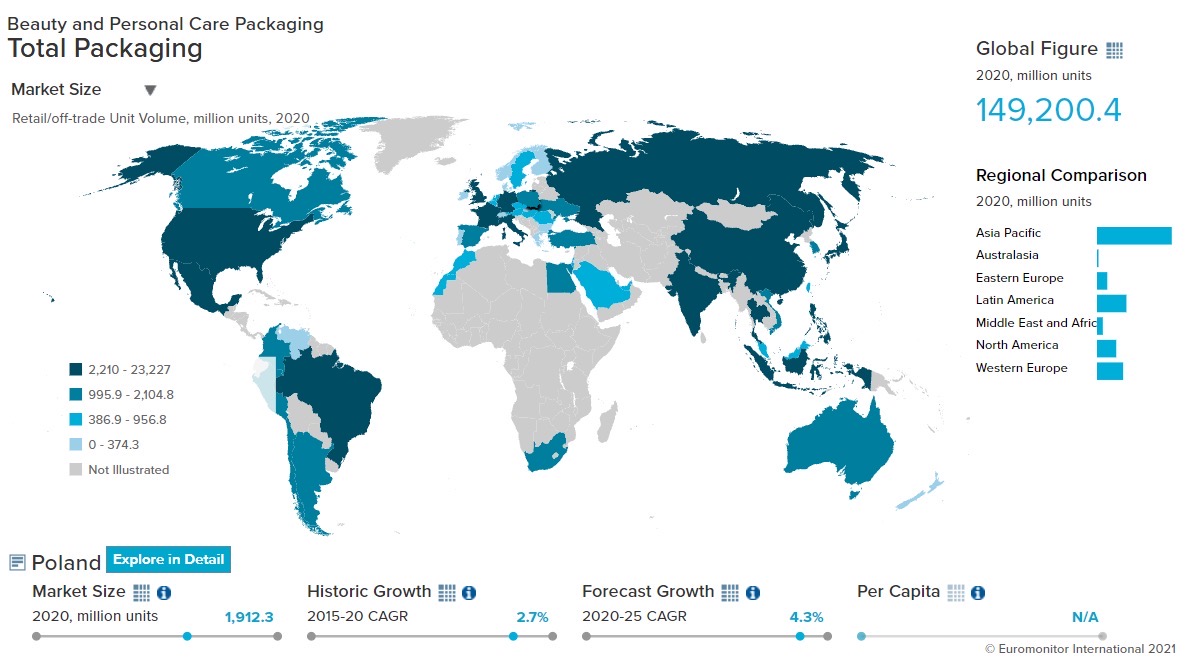

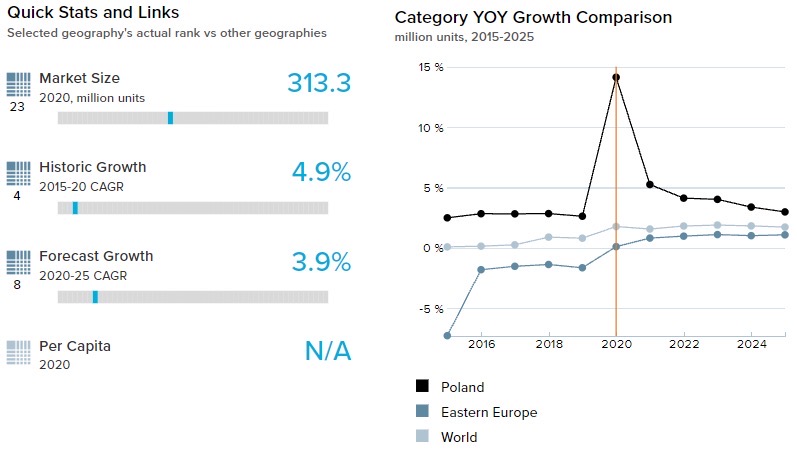

Beauty and Personal Care Packaging

1,912

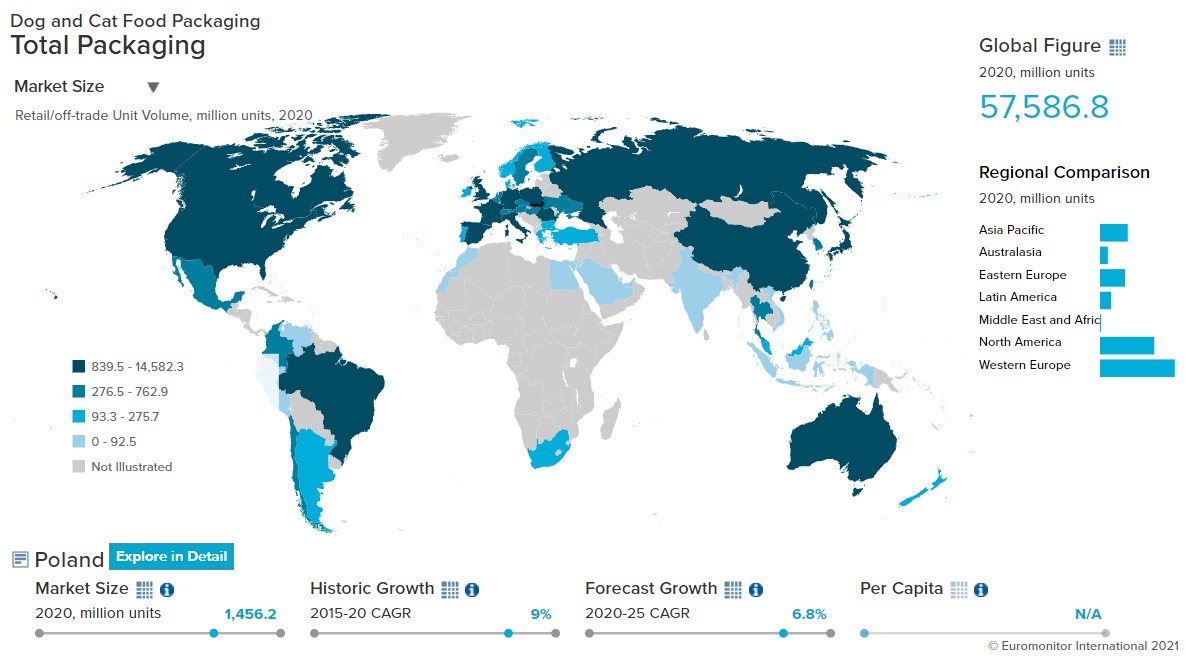

Dog and Cat Food Packaging

1,346

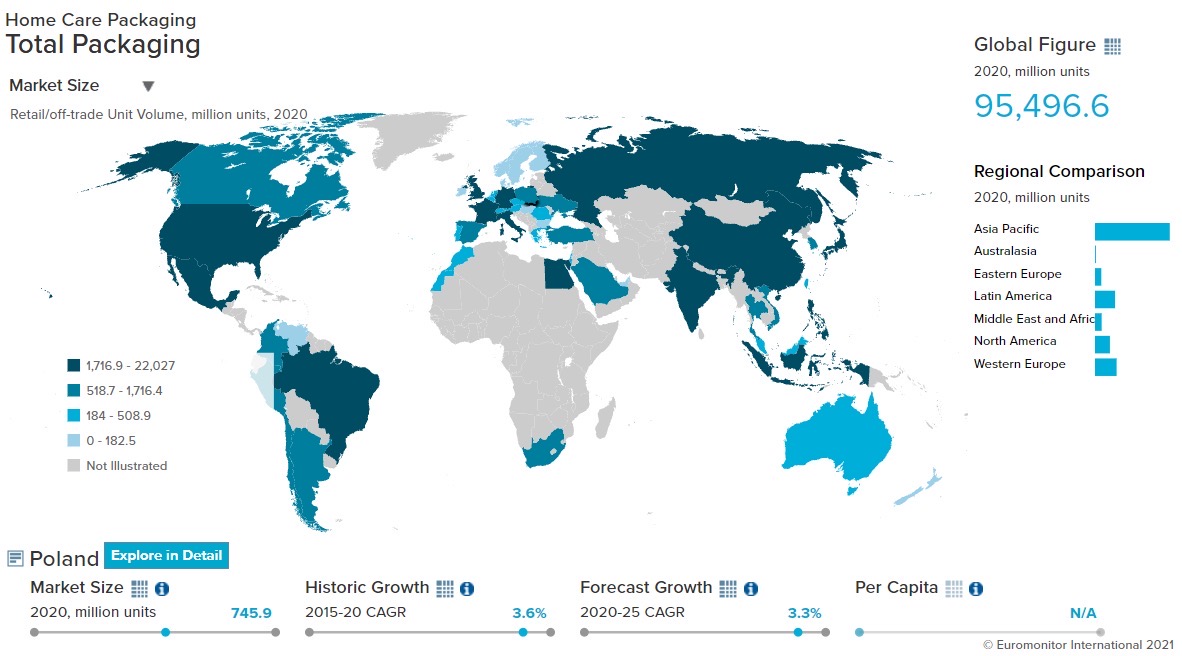

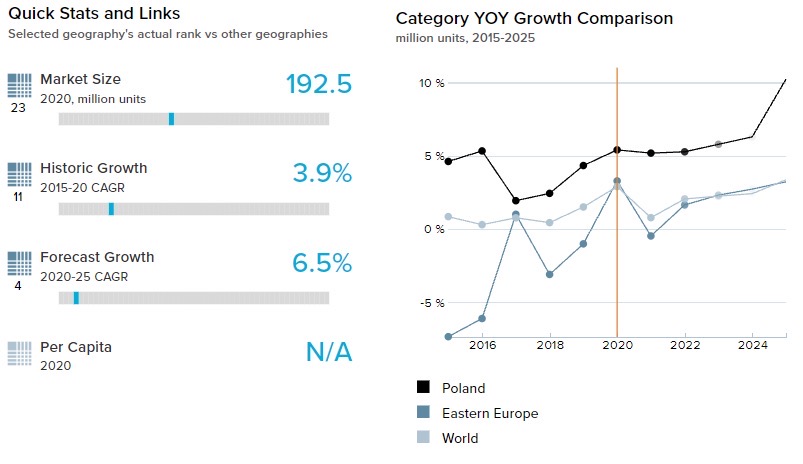

Home Care Packaging

746

Packaging Type

2020 Market Size (million units)

Rigid Plastic

14,794

Flexible Packaging

18,818

Metal

4,809

Paper-based Containers

2,553

Glass

7,572

Liquid Cartons

1,779

- Key Trends

-

Prior to the pandemic, small packages were on-trend as they were perfect for on-the-go consumption. COVID-19 reversed this, and people are now buying more bulk and multi-packs, as they provide convenience in terms of storage, reduces frequent trips outside, and provides a better value. Owing to this, increased sales of large packs such as 15kg and 25kg in dog and cat food, 1,000ml and 5,000ml bottles in beauty and personal care products, and milk formula of 800g or more have been observed. Further, the popularity of e-commerce has boosted the demand for big formats because consumers do not have to worry about carrying them home.

- Packaging Legislation

-

The EU adopted a strong stance on plastic pollution and aims that plastic bottles will have to contain at least 25% of recycled content by 2025 and 30% by 2030. To help fight against plastic pollution, the Polish Government has tightened the norms and brought very thin plastic bags under the “junk law”. So now, they are subjected to a recycling fee. thereby increasing their price and discouraging the use of thin plastic bags.

- Recycling and the Environment

-

In Poland, there is an increasing trend to return plastic bottles in exchange for cash or discount vouchers. In addition, leading players in soft drinks are coming up with innovative packaging solutions which reduce the consumption of plastic. For example, Coca-Cola came up with a paper-based multi-pack holder known as “KeelClip,” which replaces the plastic shrink wrap used earlier.

- Packaging Design and Labelling

-

Younger Polish consumers are attracted to eye-catching packaging designs. Brands are responding to this trend by coming up using attractive colors and different sizes to attract them. At the same time, brands are also providing concise information about the product’s properties and ingredients through their labeling to help consumers make their purchase decision. Another factor that brands are focusing on is environmental friendliness and zero waste, which they intend to communicate to younger Polish consumers through packaging design and labeling as they exhibit high expectations of ecological awareness. This was seen especially in mass color cosmetics, in which producers are coming up with innovative and attractive packaging to differentiate themselves.

Click here for further detailed macroconomic analysis from Euromonitor

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skincare, depilatories, and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks.

- Home Care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners, and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging, and soft drinks packaging.

Beverages

- Overview

-

- Flexible Packaging Landscape

-

- The COVID-19 induced lockdown decreased on-the-go consumption of coffee by 26.0% in volume terms in 2020 but led to an increase in at-home consumption. Therefore, flexible packaging formats with resealable zip/press closures were best suited for this situation, as they are light in weight and come in different sizes. As a result, pack types like plastic pouches showed a volume growth of 7.9% in 2020.

- The closure of food service outlets due to the pandemic affected coffee consumption more than tea consumption in 2020. This is because, in 2019, on-premise coffee consumption was 12.5% of total coffee consumed, while on-premise tea was just 3.4% of total tea consumed. As a result, while coffee took a harder hit in 2020, tea managed to register a volume growth of 4.0% during the year. The leading pack types within tea, folding cartons and flexible packaging, grew by 5.0% and 4.7% respectively in terms of volume over the same period.

- Trends

-

- Innovations in liquid cartons, especially in the gable top form, are helping them gain popularity in the juice market in Poland. For example, Tymbark launched its juice in gable top liquid cartons with a distinctive, four-sided tapered top with a screw cap, which does not leave any juice behind in the carton post-consumption. As a result, the gable top liquid carton showed a volume CAGR of 7.0% over 2015-20.

- The -increased consumer awareness of sugar intake over the past decade continued the declining trend to consume carbonates in 2020. The high sugar content of these drinks is a leading cause of various health problems including obesity. As a result, PET bottles, the main pack type of carbonates, declined by 2.8% in volume terms in 2020.

- Outlook

-

- Alcoholic drinks packaging is expected to suffer from various challenges over 2021-25, including an increase in excise duty taxes, which could hamper alcoholic drinks sales. An imposition of a sugar tax, which could impact non-alcoholic beer consumption and the long-lasting effects of COVID-19 could shift consumption of healthier drinks like juice. Due to these factors, alcoholic drinks are not expected to do well over 2021-25 resulting in a consequent decline of CAGR -0.4% in alcoholic drinks packaging within the country over the same period.

- Poles are becoming increasingly aware of the benefits of consumption of water for their bodies. As a result, they are trying to inculcate positive habits at an early age with their children. Also, with lockdown restrictions expected to ease in the coming years, there will be increased sports activities and on-the-go consumption. Due to this trend, bottled water is expected to perform well. As a result, PET bottles, the main pack type of bottled water, are expected to show a volume CAGR of 6.5% over 2021-25.

Click here for more detailed information from Euromonitor on the Beverages Packaging industry

Dog and Cat Food

- Overview

-

- Flexible Packaging Landscape

-

- Owing to the convenience in terms of storage and transportation, flexible packaging continued to lead dog and cat food pack types with a volume share of 59.7%, and volume growth of 9.4% in 2020.

- Plastic pouches gained share from flexible plastic in dog and cat food as manufacturers are adopting them to pack single-serve products, as they can be easily molded into different pack sizes. For example, Acana Polska’ launched a line of convenient single-portion dog treats in plastic pouches. As a result, plastic pouches showed a volume growth of 9.7% in dog and cat food in 2020.

- Trends

-

- Pet owners are trying to minimize the frequency of their trips outside to buy pet food due to the fear of contracting the COVID-19 virus. As a result, the demand for larger packs like 25kg and 15kg flexible plastic packs increased in 2020. These pack sizes showed a volume growth of 9.0% and 8.5% in dog and cat food in 2020.

- There is an increasing awareness about the nutritional requirements for pets among their owners and how packaged foods can help in fulfilling specific dietary requirements versus food prepared at home. As a result, flexible aluminum/plastic pouches in dry pet food and metal packaging in wet pet food showed increased demand, growing 10.0% and 8.0% respectively in volume terms in 2020.

- Outlook

-

- Shopping through e-commerce will continue to grow, as it provides the convenience of getting products delivered at home and allows customers to quickly compare various brands. Pack types that are suitable for transport, like plastic pouches and aluminum trays, are expected to show a volume CAGR of 9.4% and 9.0% respectively over 2021-25.

- The sustainability of packaging is expected to force many multinational brands to shift to more environmentally friendly packaging. For example, Royal Canin changed its packaging design to increase the proportion of recyclable plastic packaging and is planning to change its entire canned product line to recyclable packaging.

Click here for more detailed information from Euromonitor on the Dog and Cat food Packaging industry

Beauty and Personal Care

- Overview

-

- Flexible Packaging Landscape

-

- Flexible packaging volume share in beauty and personal care packaging increased substantially, from 14.1% in 2019 to 16.4% in 2020. This increase was led by strong growth in bath and shower products due to increased focus on personal hygiene in the pandemic.

- Larger pack types started doing well in 2020 due to two reasons. First, it helps reduce the frequency of outside trips for shopping during the pandemic. Second, it provides a better price per ml, which is preferred by many customers during uncertain economic conditions caused by COVID-19. As a result, 1,000 ml plastic pouches and 5,000 ml HDPE bottles showed a volume growth of 32.6% and 29.4% respectively in beauty and personal care in 2020.

- Trends

-

- COVID-19 induced lockdowns and work from home regimes drastically reduced outside trips, which negatively impacted beauty and personal care sales and the packaging segments subsequently showed a volume decline of 1.6% in 2020. Spending budgets on this category has decreased as people spent most of the time alone and considered it as non-essential during the year. Owing to this trend the main pack type of beauty and personal care, rigid plastic, declined 4.3% in volume in 2020.

- There is an increased focus on personal health and hygiene due to the pandemic, resulting in increased demand for bath and showering products. Increased hand washing led to increased demand for bar soap and liquid soaps. As a result, flexible plastic and plastic pouches, which are the main pack types of bar soap and liquid soap respectively, showed a volume growth of 25.2% and 32.5% in 2020.

- Outlook

-

- Over 2021-25, beauty and personal care is expected to bounce back as restrictions are likely to ease and people venture out again. With this, it is expected that the smaller pack types will once again start performing well. This will most likely benefit plastic pouches as they are light and come in various sizes and are likely to show a volume CAGR of 7.0% over 2021-25.

- As per research conducted on behalf of the Polish Union of Cosmetics Industry in 2019, packaging used in beauty and personal care products was the second most important factor to customers. The research also pointed out that consumers do not expect an outright ban on plastic, but a gradual change to sustainable packaging. Therefore, sustainable packaging is expected to remain a very important factor in consumers’ purchases over 2021-25. As a result, glass bottles (since glass is perceived to be the most environmentally friendly material among Polish consumers), are expected to show a volume CAGR of 5.3% over 2021-25.

Home Care

- Overview

-

- Flexible Packaging Landscape

-

- There was a reduction in the disposable income of Polish consumers due to job losses and salary cuts during the pandemic, which forced them to opt for low-priced solutions in many product categories. Plastic pouches, which are inexpensive and lightweight, showed a volume growth of 22.9% in the home care segment, driven by the increased sales in laundry and dishwasher detergent, in which the pack types grew 26.0% and 27.1% respectively in volume terms in 2020.

- COVID-19 induced lockdowns and office restrictions meant people spending more time at home. This increased their at-home consumption of meals which led to increased demand for dishwasher detergent. This boosted the demand for blister/strip packs and HDPE bottles, which showed a volume growth of 16.6% and 7.8% respectively in 2020.

- Trends

-

- In the wake of COVID-19, people have become more cautious about their surroundings, trying to make them as clean as possible. This trend helped increase the demand for surface cleaners. HDPE and PET bottles, two of the main pack types of surface cleaners, showed a volume growth of 2.6% and 4.6% respectively in 2020.

- The demand for larger pack types is increasing as more consumers are buying these pack sizes either through traditional stores or through e-commerce websites. This helps consumers decrease the frequency of outside visits, and provides a better price per unit value. As a result, pack sizes such as 3,000 ml and 4,000 ml HDPE bottles and 2,000 ml PET bottles showed a volume growth of 15.0%, 8.9%, and 6.3% respectively in 2020.

- Outlook

-

- Pre-COVID, there was an increasing focus on the development and buying of products that came in sustainable packaging, but the pandemic disrupted this trend. The trend is expected to regain momentum over 2021-25, as life returns to normal. Therefore, recyclable plastic pouches and glass jars are expected to grow at a volume CAGR of 19.2% and 11.9% respectively over 2021-25.

- Polish consumers are becoming more cautious about the packaging and ingredients of the products they purchase, and brands are expected to increasingly use labeling callouts to communicate the contents to the customers. Brands highlighting natural ingredients and recyclable packaging used can stand out from their competitors and gain customers’ attention. Therefore leading companies such as Procter & Gamble are working on the development of several new ecological sustainable products.

Click here for more detailed information from Euromonitor on the Home Care Packaging industry

Packaged Food

- Overview

-

- Flexible Packaging Landscape

-

- The demand for in-home ready meals was already there before the pandemic, but COVID-19 boosted this demand further. This helped to increase their sales, especially frozen and refrigerated ready meals. The main pack type, flexible plastic in frozen and thin-walled plastic containers in refrigerated, showed a volume growth of 7.2% and 9.7% respectively in 2020.

- Due to the busy lifestyles of the customers, baby formula demand picked up over 2015-20 and showed a volume CAGR of 7.0% during that period. Along with the ability to save time, parents also use baby formula since it has a long shelf life. Customers can buy larger pack types (800g or more), which have a lower per-unit price. Therefore, their main pack type, flexible aluminum/plastic, showed a volume CAGR of 13.9% over 2015-20.

- Trends

-

- In the wake of COVID-19, there is an increased focus on personal health and well-being. As a result, demand for fresh milk has increased, as it is believed to boost the immune system. Additionally, lockdowns greatly increased at-home consumption. The main milk pack types, brick liquid carton and PET bottles, showed a volume growth of 32.9% and 32.2% respectively in the same year.

- The demand for meat and seafood snacks increased as people become more health-conscious and want to switch from sugary treats to healthy protein-rich options. For example, kabanos, a smoked and seasoned sausage like beef jerky, is increasingly popular as a midday snack. Flexible plastic dominates the meat and seafood snack segment with a volume share of 59.0% and showed a volume growth of 6.2% in 2020.

- Outlook

-

- Healthy snacking trends are expected to continue in the next years. As a result, demand for chocolate confectionery is expected to be weak, growing at a volume CAGR of 1.1%, and its main pack type, flexible plastic showing a volume CAGR of 0.6% over 2021-25. However, demand for small pack types is expected to increase as it helps in portion control. As a result, plastic pouches which can be easily molded in smaller pack sizes is expected to show a volume CAGR of 11.4% in chocolate confectionery over 2021-25.

- Polish consumers, especially young ones, are becoming more aware of environmental issues. As a result, sustainability as a purchasing factor is expected to become more important over 2021-25. Manufacturers are expected to respond to this trend with more sustainable packaging. For example, international processed seafood player Mowi is planning to shift its packaging from plastic to folding easily recyclable aluminum trays over 2021-25.

Click here for more detailed information from Euromonitor on the Packaged Food Packaging industry

RECOVERY FROM COVID

- Overview of COVID-19 conditions in Poland

-

Polish government lifts bans on traveling and reopens public places

- According to the World Health Organization (WHO), Poland had 6,005,531 COVID-19 cases, with 116,268 deaths and 95 new daily cases as of May 26, 2022.

- On May 15, 2022, Poland’s total vaccination doses reached 54,465,653. Out of the population, 60.0% received the first dose of vaccination, while 59.2% received a second dose.

- The Polish government lifted all travel restrictions and tourism bans in the country starting March 28, 2022. As a result, travelers are no longer required to present vaccination certificates while crossing the borders. In addition, they are not required to quarantine after entering the country or undergo and show negative COVID-19 test results.

- Moreover, the Polish government also lifted bans on public places such as bars, clubs, restaurants, and other places that are targeted by tourists. However, people will be required to wear well-fitting masks in indoor areas, on public transport, and in crowded places.

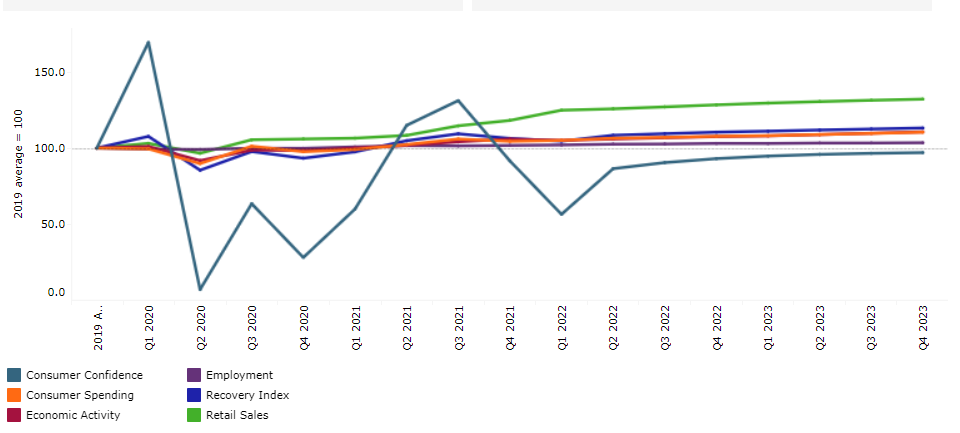

The chart below shows Euromonitor International’s Recovery Index.

The quarterly reported Recovery Index is a composite index that provides a quick overview of economic and consumer activity. It keeps track of the latest quarterly economic/consumer data and forecasts in key economies to gauge when economic activity and consumer demand are likely to return to the pre-pandemic levels of 2019.

A score of 100 and over indicates a full recovery in which economic output, the labor market, and consumer spending all return to/exceed 2019 levels.

Detailed methodology is provided in the Appendix.Quarterly Recovery Index and Related Indicators, Poland

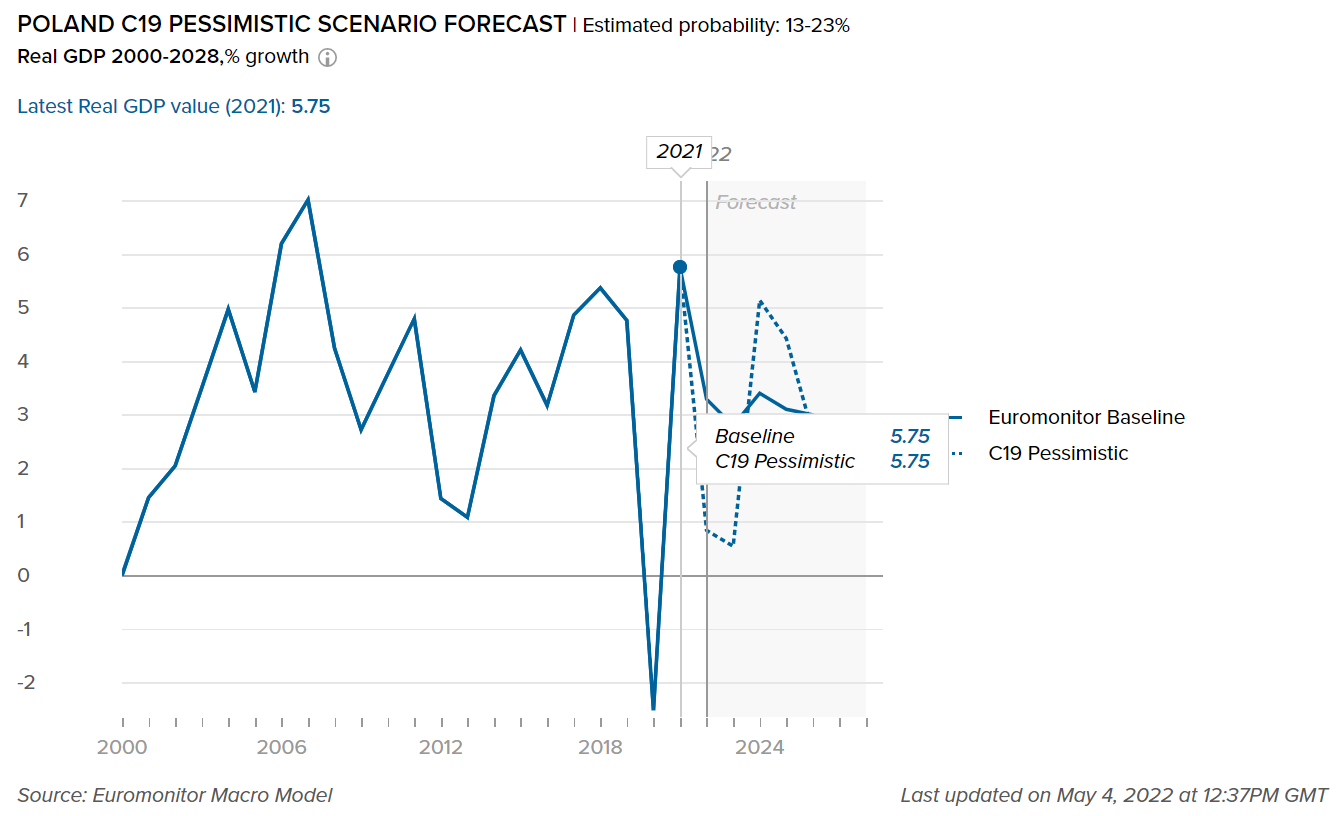

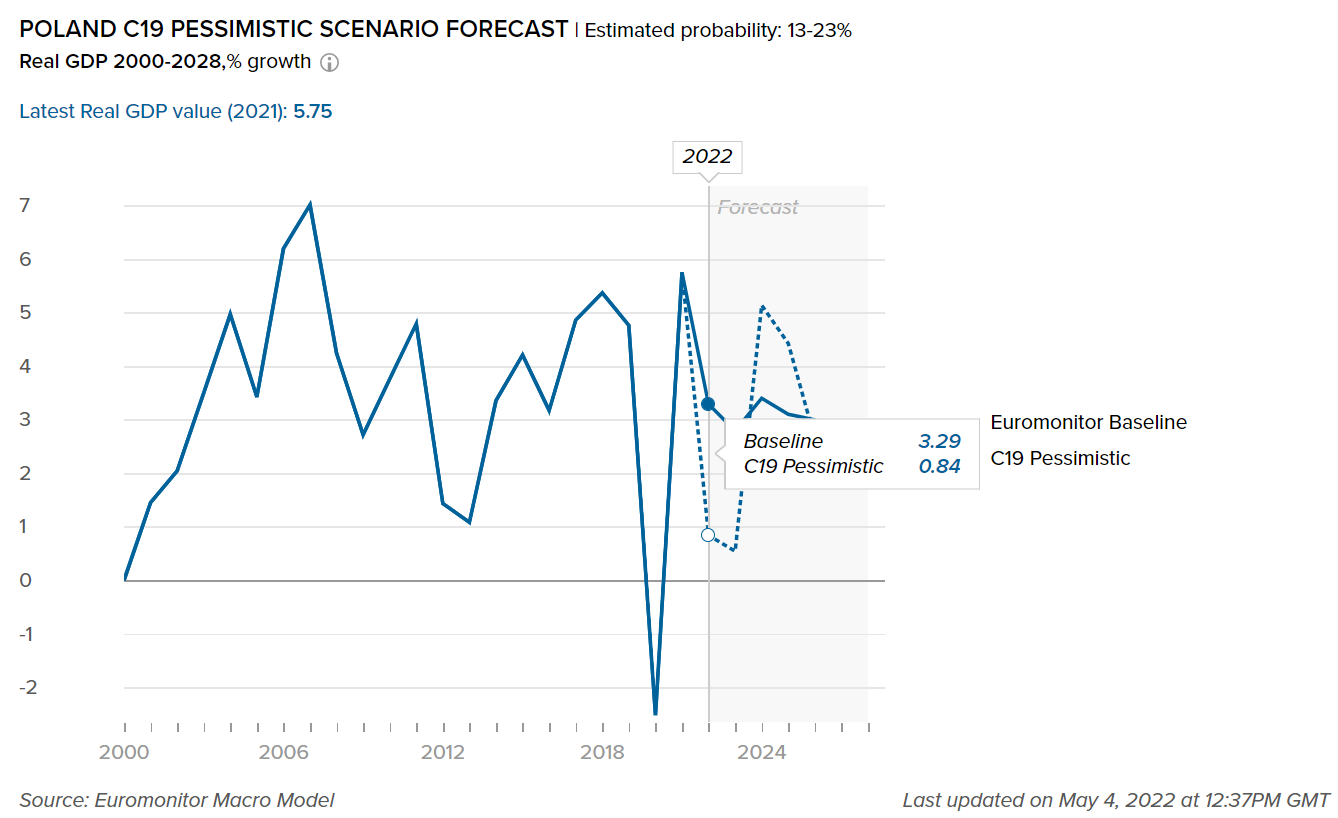

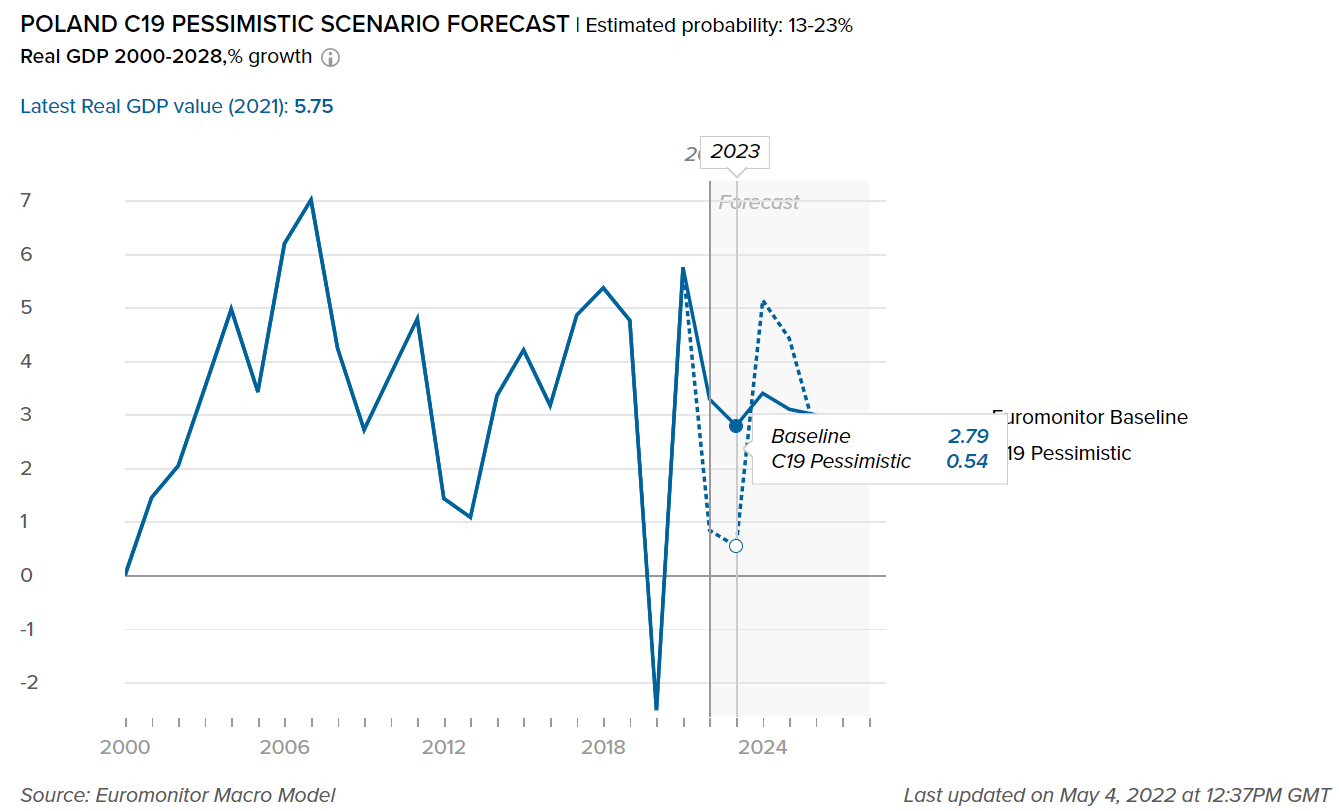

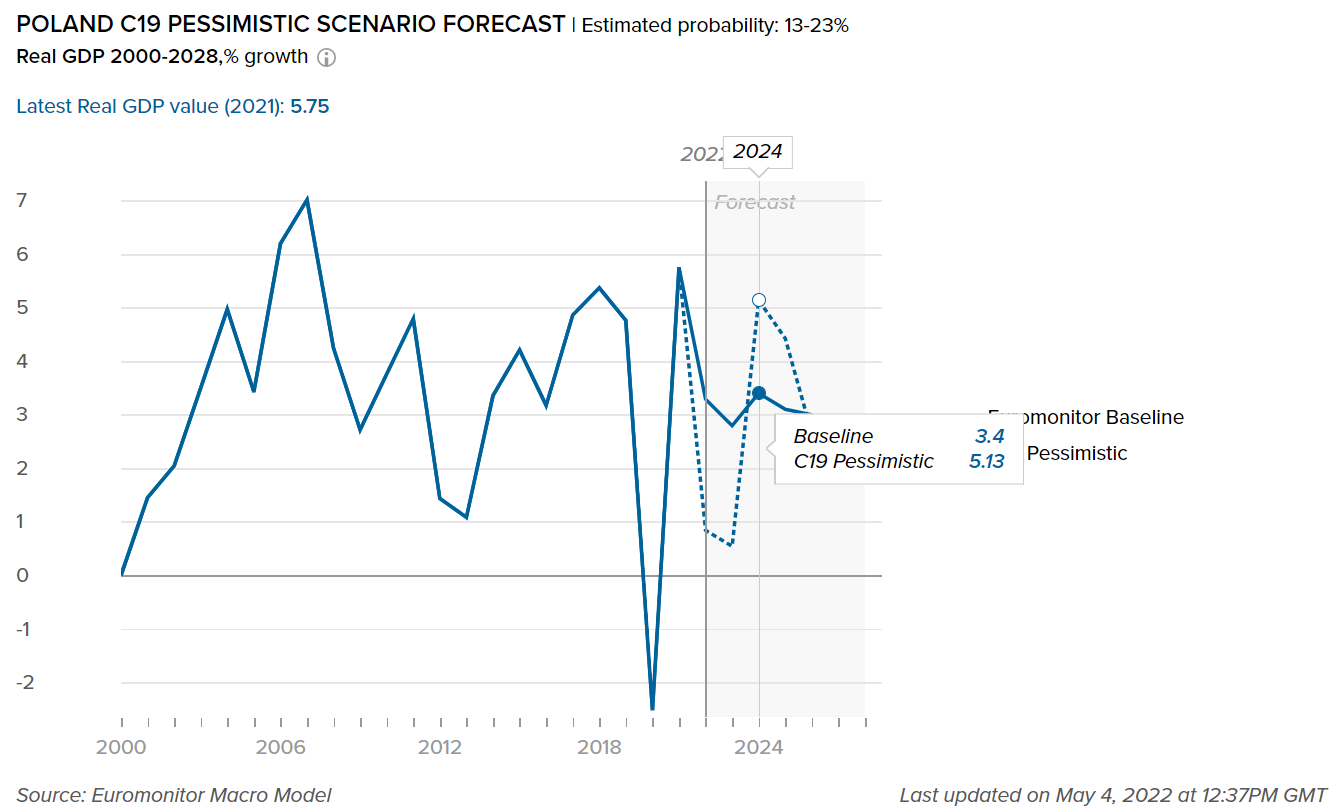

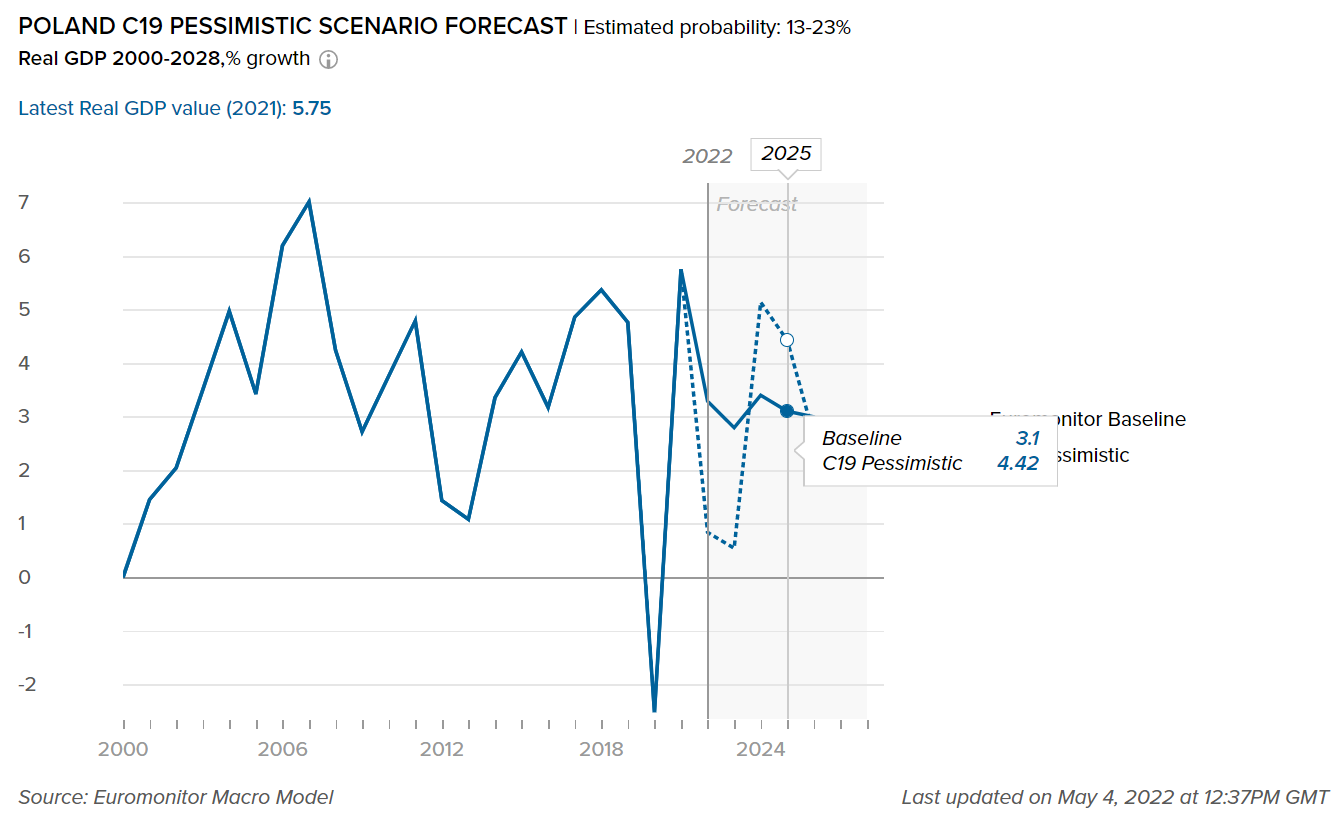

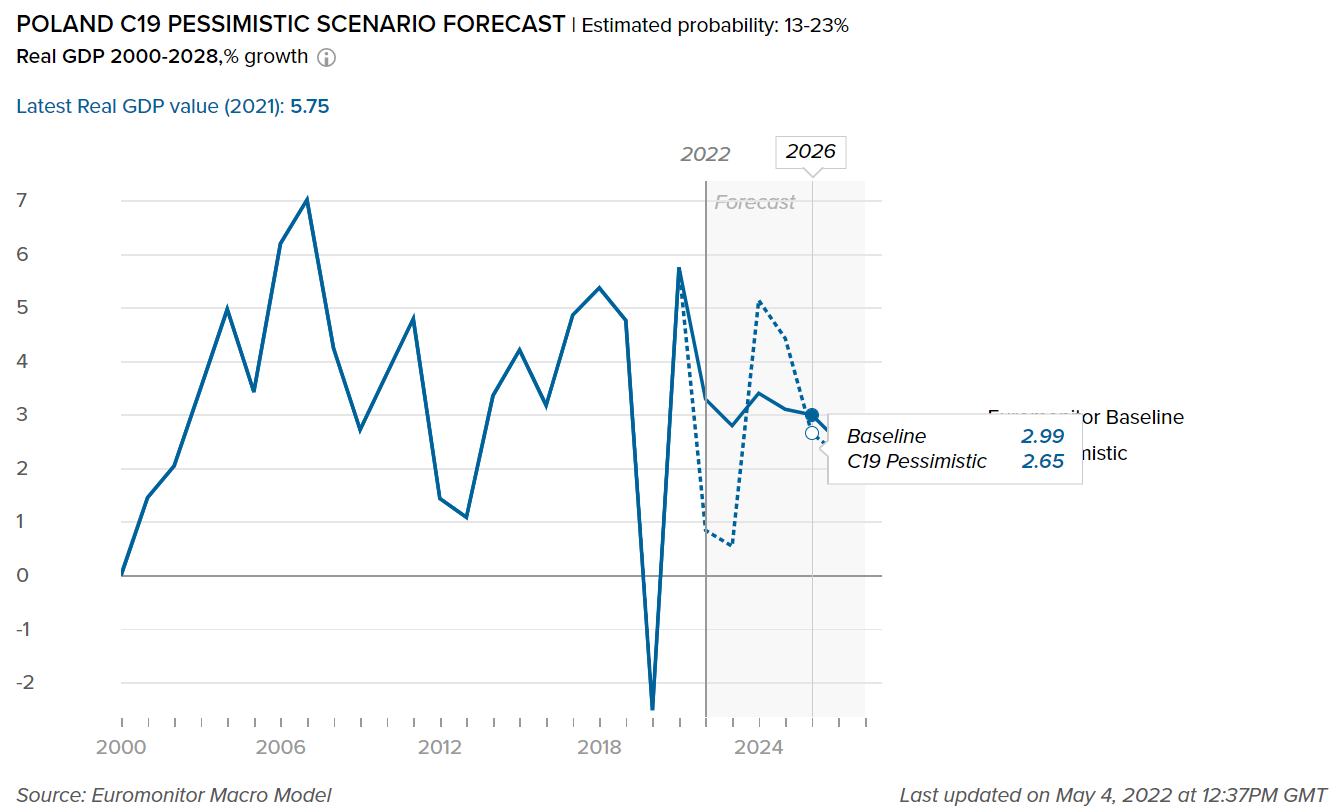

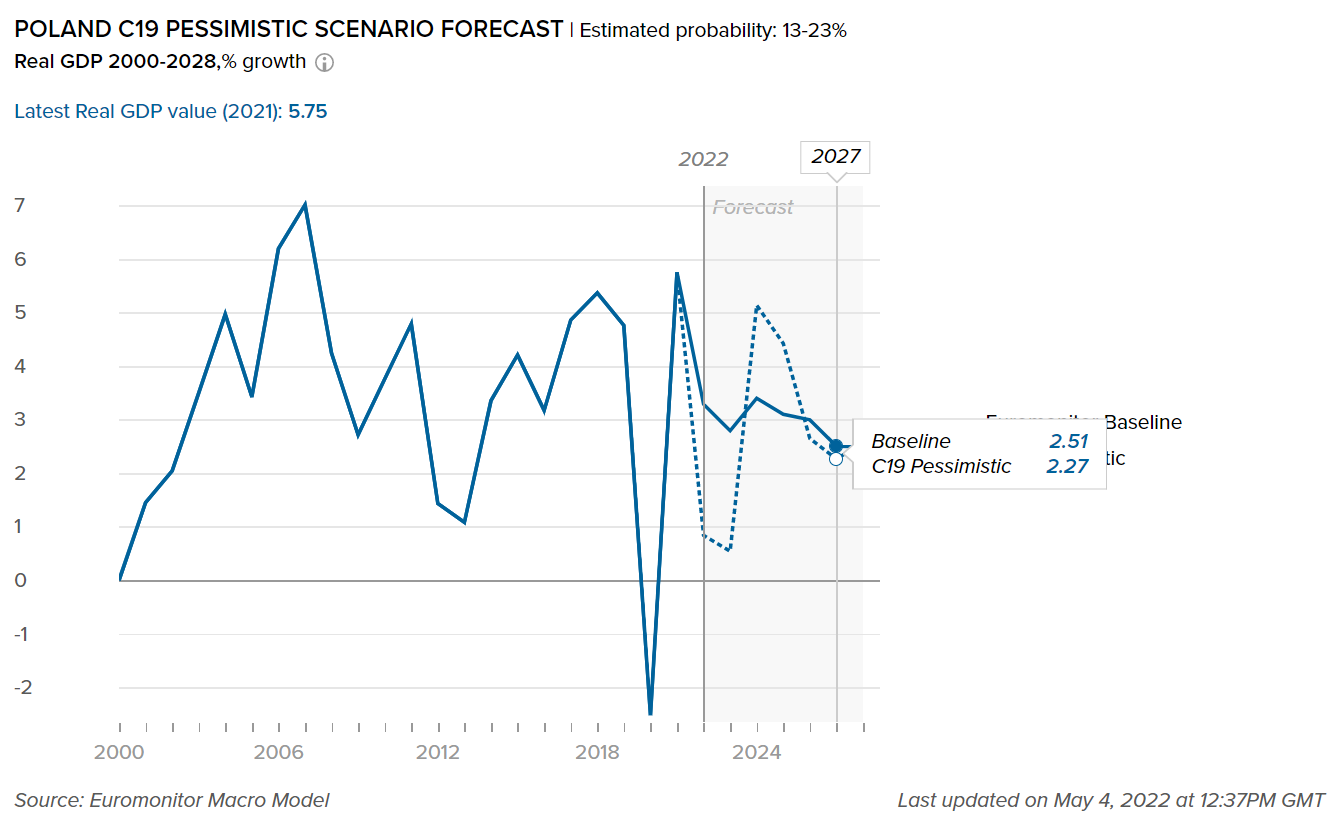

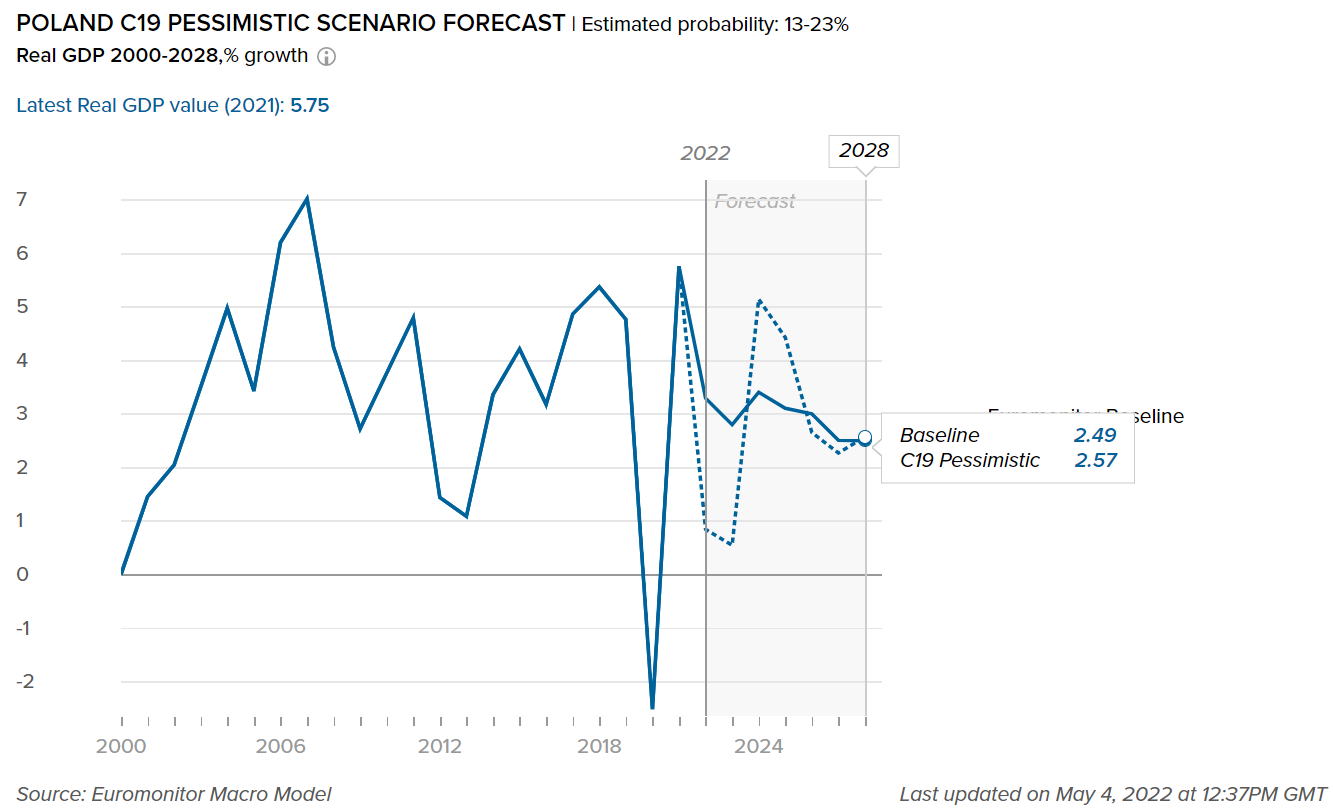

- Impact on GDP

-

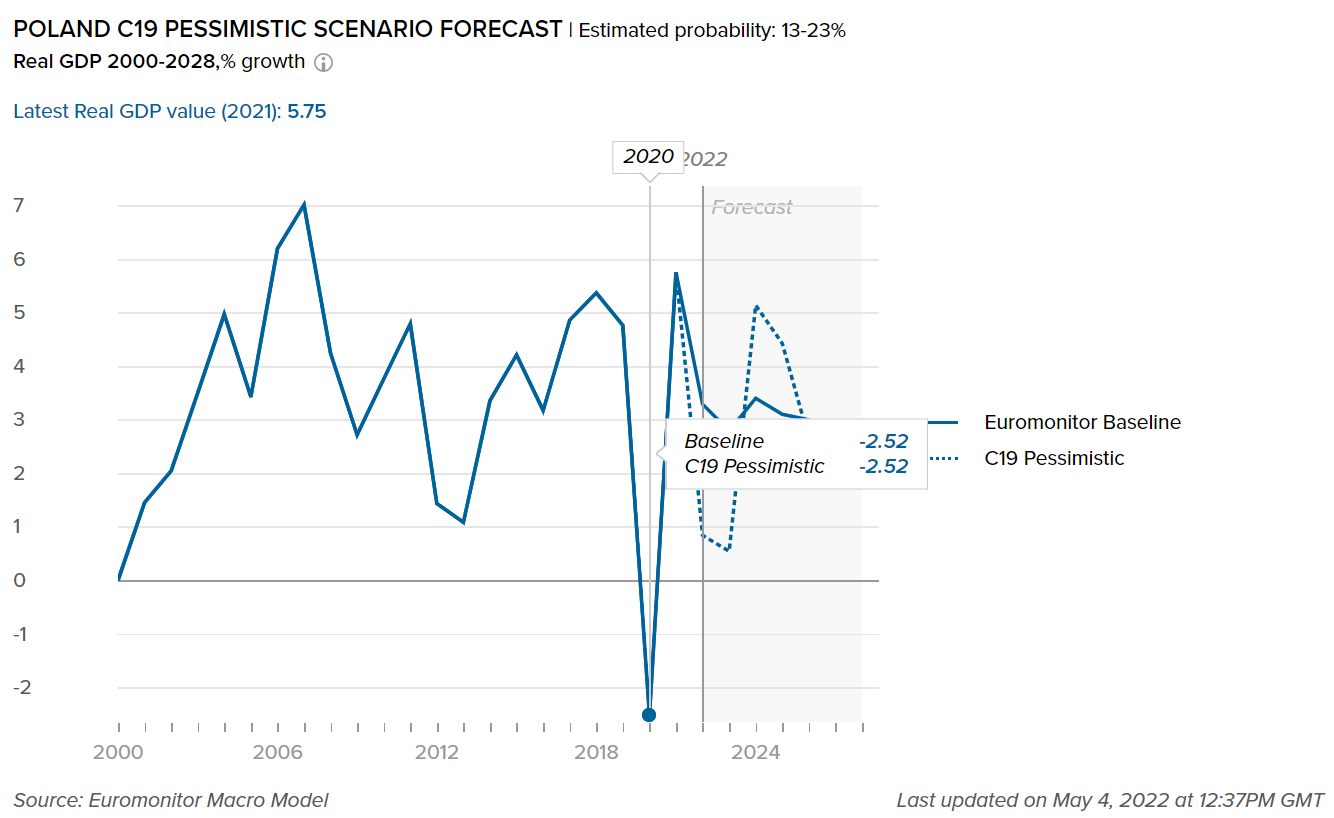

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the real GDP value in Poland. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon. For more details, please refer to the detailed explanation of the COVID-19 scenarios in the scenario definitions section.

Please note that the forecasts will be adjusted every three months, according to the expected number of cases, recoveries, and deaths due to COVID-19 in this country, as well as shifting socioeconomic conditions (the most recent update was May 2022).

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Poland’s well-diversified economy is expected to attract foreign direct investment

- Poland was able to attract foreign direct investment (FDI) over 2020-2021 owing to its strong economic development, access to the European market, EU funding, and a well-educated workforce. In addition, a well-diversified economy allowed international investors to take advantage of multiple opportunities. As the negative impact of the COVID-19 pandemic fades over 2022-2026, FDI is anticipated to remain a vital engine of the Polish economy, while EU financing is likely to be reduced in the future, especially given the government's increasing dominance over the judiciary.

- In 2021, Poland’s corporate tax rate was 19.0%, a relatively low rate that benefited business operations and profit distribution. In March 2022, the Polish government proposed plans that will reduce the income tax rate paid by individuals from 17.0% to 12.0% for those earning up to PLN120,000 (USD27,160) per year, which would apply to 25.0 million people. The Polish parliament has successfully voted on the measures of this plan which has now come into force from 1st July 2022 retrospectively. The changes, labeled as the ‘anti-Putin shield’, are expected to protect the economy from the negative impact of high prices caused by Russia’s invasion of Ukraine and increase consumer purchasing power.

- Impact to Sector Growth

-

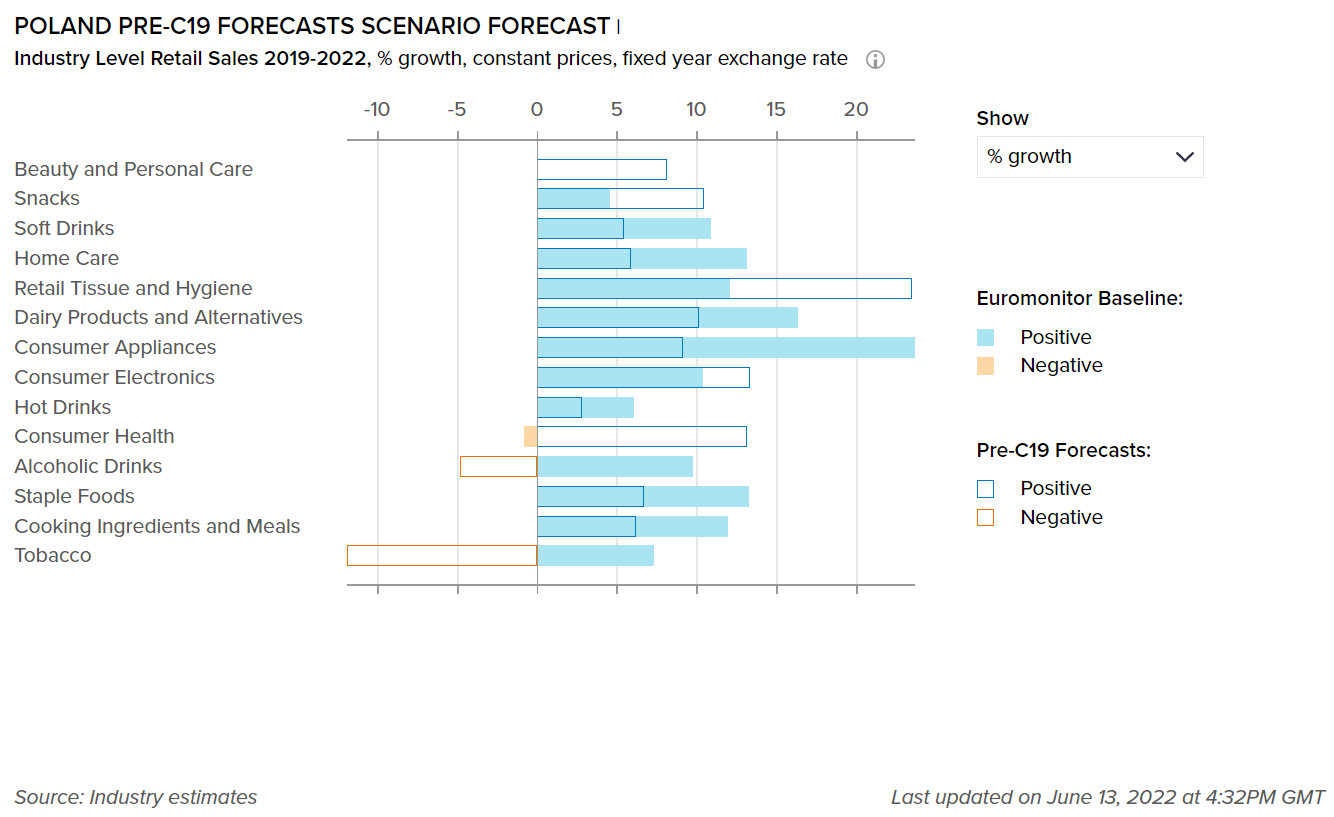

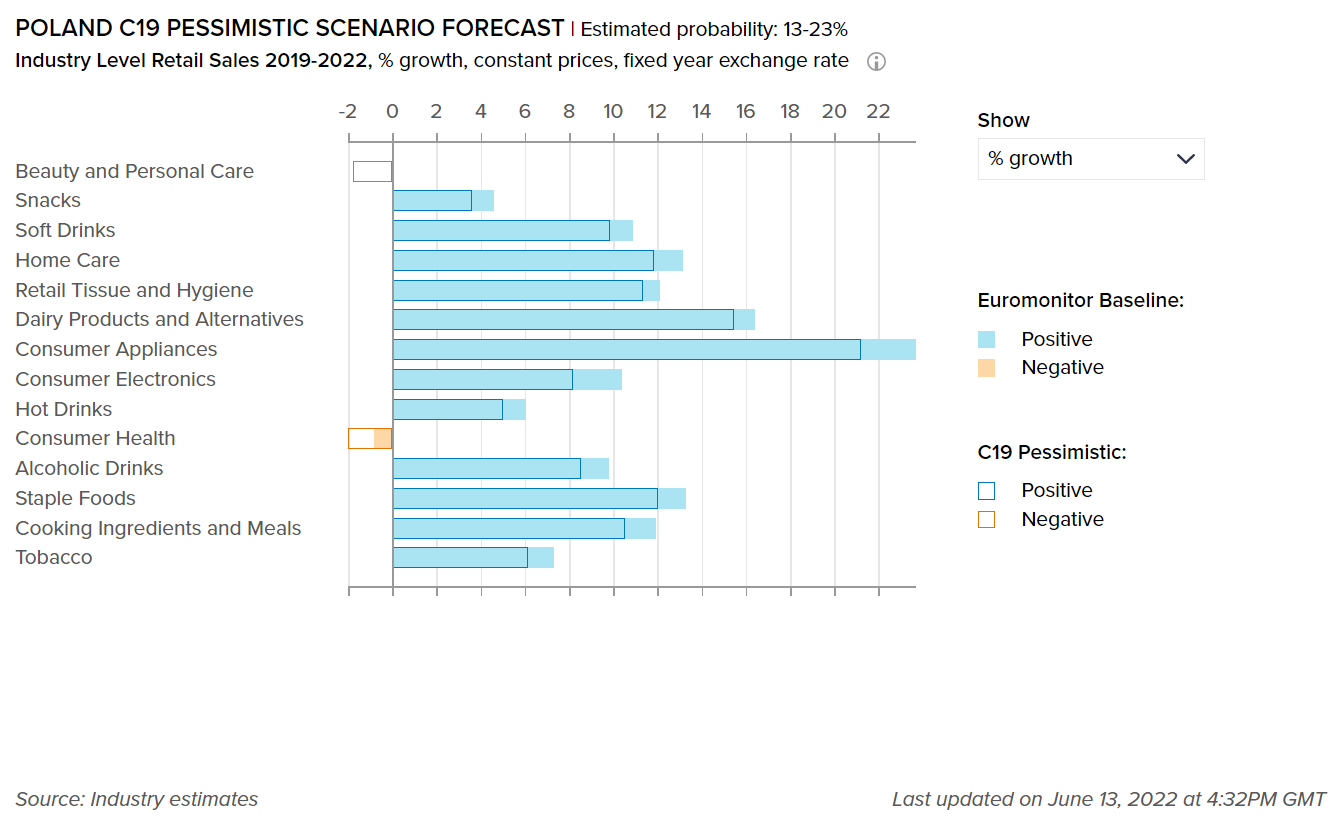

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socioeconomic conditions.

The graph below displays the adjusted forecasts of the percentage growth for the categories mentioned to highlight the impact of COVID-19 between our pre-COVID-19 estimates and the “most probable” (Baseline) forecast which has an estimated probability of 45-60%.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

Gradual easing of restrictions set to increase beauty and personal care and home care sales

- After a poor performance in 2020 due to lockdown and store closures, beauty and personal care grew by 5.5% in 2021, although it did not return to pre-pandemic levels. The main drivers included the gradual easing of restrictions and the return of consumers to old patterns of behavior, including more outside activity, more frequent visits to shops, and the return to the workplace. Over 2022-2026, the complete removal of restrictions on travel and tourism and return to normalcy will likely drive the sales for categories such as sun care, deodorants, and fragrances, which were hit hard in 2020. Moreover, the gradual recovery from the recession is also set to improve the sales of premium beauty products.

- In home care, new product development is expected to remain a key driver of growth in categories such as surface care, dishwashers, laundry care, and toilet care. Products with antibacterial properties, which are made with natural and organic ingredients, and are harmless, are expected to be of the highest interest to consumers. In addition, consumer focus on the environment is also set to be a key factor behind the demand. Thus, players will have to invest in more sustainable production practices. For example, Yope, a Polish home care brand, provides natural home care products that are harmless and do not leave any toxic waste that may hamper the environment.

Please note that the forecasts are adjusted every three months according to the expected number of cases, recoveries, and deaths due to COVID-19 in the country, as well as shifting socio-economic conditions.

This graph shows our “most probable” and “worst case” estimate scenarios of how COVID-19 will impact the percentage growth for the sectors mentioned in Poland. Our “most probable,” or Baseline scenario, has an estimated probability of 45-60% over a one-year horizon. Our “worst case,” or Pessimistic scenario, has an estimated probability of 13-23% over a one-year horizon.

Baseline forecast refers to the “best case” COVID-19 scenario forecast that has an estimated probability of 45-60%.

C19 Pessimistic refers to the “worst case” COVID-19 scenario forecast that has an estimated probability of 13-23%.

Alcoholic drinks rebounded in 2021, albeit at a slower pace, owing to the continuation of lockdowns during the initial months of the year

- Alcoholic drinks rebounded in 2021, with growth in both off-trade and on-trade sales. However, while off-trade sales exceeded pre-pandemic levels during the year, on-trade was unable to reach those levels. This was due to the continuation of lockdowns, including the closure of foodservice outlets at the beginning of 2021. In addition, the slow roll-out of vaccines and slow economic recovery also limited the growth of alcoholic drinks during the year.

- Following the outburst of the pandemic in 2020, the health and wellness trend has since accelerated. As a result, over 2022-2026, consumers are expected to pay more attention to what they purchase and thus, focus on the nutritional information on staple foods packaging. In addition, they are likely to look for products that provide functional benefits, for example, organic foods are expected to increase in popularity as consumers are set to avoid additives as much as possible. This demand for healthier staple foods may also lead to premiumization, with consumers willing to pay a mark-up for better quality products.

- Impact on Flexible Packaging

-

The following tables display adjusted market size for 2021, market size forecasts for 2022, and the percentage difference between the February 2022 and June 2022 estimates for the year 2022.

Please note that for the current quarterly update, the following table covers beauty and personal care packaging and home care packaging industries only.

Packaging Industry

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Beauty and Personal Care Packaging

2,021

2,079

-1.0

Home Care Packaging

808

844

2.9

Packaging Type

2021 market size as per Jun 2022 data

2022 market size as per Jun 2022 data

% Difference between Jun 22 and Feb 22 data for 2022

Rigid Plastic

15,132

15,583

0.07

Flexible Packaging

19,296

19,736

-0.10

Metal

4,990

5,192

-0.03

Paper-based Containers

2,659

2,757

-0.08

Glass

8,023

8,387

0.17

Liquid Cartons

1,811

1,840

0.00

Polish government’s SUPD likely to impact plastic packaging of hot drinks

- The Polish government plans to implement regulations in the EU’s Single-Use Plastic Directive (SUPD) by the start of 2024. This initiative is likely to increase the availability of alternatives to plastic in packaging, mainly affecting hot drink pack types such as plastic pouches and flexible plastic, which account for almost half of all hot drink packaging in Poland. As per the draft regulation, PLN1 would be charged for every single-use plastic package (or product) to cover the cost of its waste management. It is expected to help drive manufacturers to consider other packaging alternatives to reduce per-pack costs.

- In early 2022, the Polish government launched a formalized deposit return scheme that covers PET bottles with a volume of up to 3 liters and glass bottles with a volume of up to 1.5 liters. This is set to be a major step in the recycling of soft drinks packaging, as the deposit return system previously only covered glass beer bottles and was not formally operated. Over 2022-26, the formalized approach to bottle recycling is expected to drive the use of more rPET pack types instead of virgin plastic.

- In 2021, the impact of the COVID-19 pandemic continued to impact the purchasing of home care products in the country. Large numbers of consumers were still spending more time at home than usual due to home working/learning, seeing them continue to pay greater attention to more rigorous home cleaning activities, boosting sales of products, and their packaging, in categories such as surface care or bleach. As a result, notable pack types such as HDPE bottles, PET bottles, and flexible plastic, continued to perform well in 2021 owing to the continued impact of the pandemic. In addition, consumer preferences benefited home care disinfectants and HDPE bottles, as the packaging format is the sole pack type used within the category.

- Definitions

-

- Beauty and Personal Care Packaging: This is the aggregation of packaging for baby care, bath & shower products, deodorants, hair care, color cosmetics, men's grooming products, oral hygiene, perfumes & fragrances, skin care, depilatories and sun care. Black market sales and travel retail are excluded.

- Dog and Cat Food Packaging: This is the aggregation of dog and cat food packaging.

- Packaged Food Packaging: This is the aggregation of packaging for baby food, Bakery, canned/preserved beans, canned/preserved fish/seafood, canned/preserved fruit, canned/preserved meat and meat products, canned/preserved tomatoes, canned/preserved vegetables, other canned/preserved food, confectionery, chilled fish/seafood, chilled lunch kit, chilled processed meats, fresh cut fruits, dairy, dessert mixes, rice, frozen bakery, frozen desserts, frozen meat substitutes, frozen processed fish/seafood, frozen processed potatoes, frozen processed poultry, frozen processed red meat, frozen processed vegetables, other frozen processed food, ice cream, meal replacement, noodles, oils and fats, pasta, ready meals, sauces, dressings and condiments, snack bars, soup, spreads and sweet and savory snacks

- Home care Packaging: This is the aggregation of packaging for laundry care, dishwashing products, surface care, chlorine bleach, toilet care, polishes, air fresheners and insecticides.

- Beverages Packaging: Beverage packaging is the aggregation of alcoholic drinks packaging, hot drinks packaging and soft drinks packaging.

- Scenario Definitions

-

Scenario Assumptions

Baseline

C19 Pessimistic

Estimated probability

45-60% over a one-year horizon

13-23% over a one-year horizon

Global GDP growth

2.0% to 4.0% in 2022

1.8% to 4.2% in 2023

-1.0% to 1.0% in 2022

-0.5% to 2.0% in 2023

COVID-19 situation

A combination of high vaccination rates with milder virus variants and widespread availability of antiviral drugs make COVID-19 an endemic disease in advanced economies

The spread of a more infectious and highly vaccine-resistant COVID-19 mutation requires intense lockdowns/social distancing measures in 2022-2023, delaying the economic recovery from the pandemic

Vaccinations

Existing vaccines remain highly effective against severe diseases from new coronavirus variants, with moderate vaccine modifications

Vaccination campaigns progress in developing economies is slower than expected

Impact on economy

Services activity would pick up in 2022 on the back of loosening COVID-19 restrictions and releasing pent-up demand

Longer-lasting and much stricter distancing measures cause large drops in consumption, business revenues, employment, and wages relative to the baseline forecast in 2022-2023

- Recovery Index

-

Recover Index Methodology

Euromonitor International’s Recovery Index is a composite index that provides a quick overview of economic and consumer activity and helps businesses predict recovery in consumer demand in 48 major economies. The index takes into consideration total GDP and factors that determine consumer spending - employment, consumer spending, retail sales, and consumer confidence. Index scores measure the change relative to the average per quarter for 2019.

Category

Weighting

Focus

Economic Activity

20%

Tracks and forecasts the level of real GDP, as this is a broad measure of everything that workers and capital produce in a country.

Employment

20%

Looks at the employed population and average actual weekly working hours in each quarter, as these indicators help track households’ primary source of income besides government financial support.

Consumer Spending

25%

Looks at private final consumption expenditure in each quarter, as this is officially the best measure of consumer spending in real terms.

Retail Sales

25%

Focuses on seasonally adjusted real retail sales data as a timely indicator of economic performance and strength of consumer spending.

Consumer Confidence

10%

Looks at the standardized consumer confidence index to see how consumers across countries feel about their situation and when they will start feeling better about the future.